SNOW - SentinelOne: Operating From Strength With $1.1 Billion In Liquidity And No Debt

2023-10-05 08:30:00 ET

Summary

- While it's been a challenging 2023 for SentinelOne, the company continues to operate from a position of exceptional strength.

- It has arguably the best tech in cybersecurity, and it sits atop a giant chunk of durable, high margin ARR (~$650M), $1.1B in cash, and no debt.

- Today, we will start by addressing the recent rumors circulating SentinelOne's business, as well as some of the controversies the business has faced in 2023.

- In short, I believe SentinelOne stock offers 10x returns in the decade ahead, against a risk profile that is lower than 10x returns would suggest. That is, I believe SentinelOne offers an asymmetric risk = return profile, which is the precise setup I target.

Rumors & Logic

It has certainly been an interesting 2023 as a partner to the business of SentinelOne ( S ), or S1 for short.

Following S1's Q1 2023 (using calendar year throughout this note for simplicity's sake), it was revealed that the business apparently had uncovered issues regarding its recording of its annual recurring revenue, or ARR for short. To be sure, while S1 had accounting issues, it apparently did not commit acts of impropriety as some initially speculated.

To add clarity to the whole situation, S1 accounted for usage-based consumption in its ARR throughout 2022 following the launch of a new data platform offering, and, in late 2022 and early 2023, some of that usage did not materialize.

S1 then had to restate its ARR metrics, which, alongside a weaker guide for Q2 2023, spooked investors, creating a 35% selloff following its Q1 2023 report, which was released June 1st, 2023.

If that weren't enough controversy, weeks ahead of its Q2 report, published August 31st, 2023, rumors began circulating that S1 was looking to sell itself. Additionally, it was revealed that S1 terminated a cloud-security partnership with Wiz, a cloud-security business that has captured Fortune 100 customers and which is revered in the cybersecurity startup scene.

[Both of these rumors proved to be totally false and unsubstantiated, as an aside.]

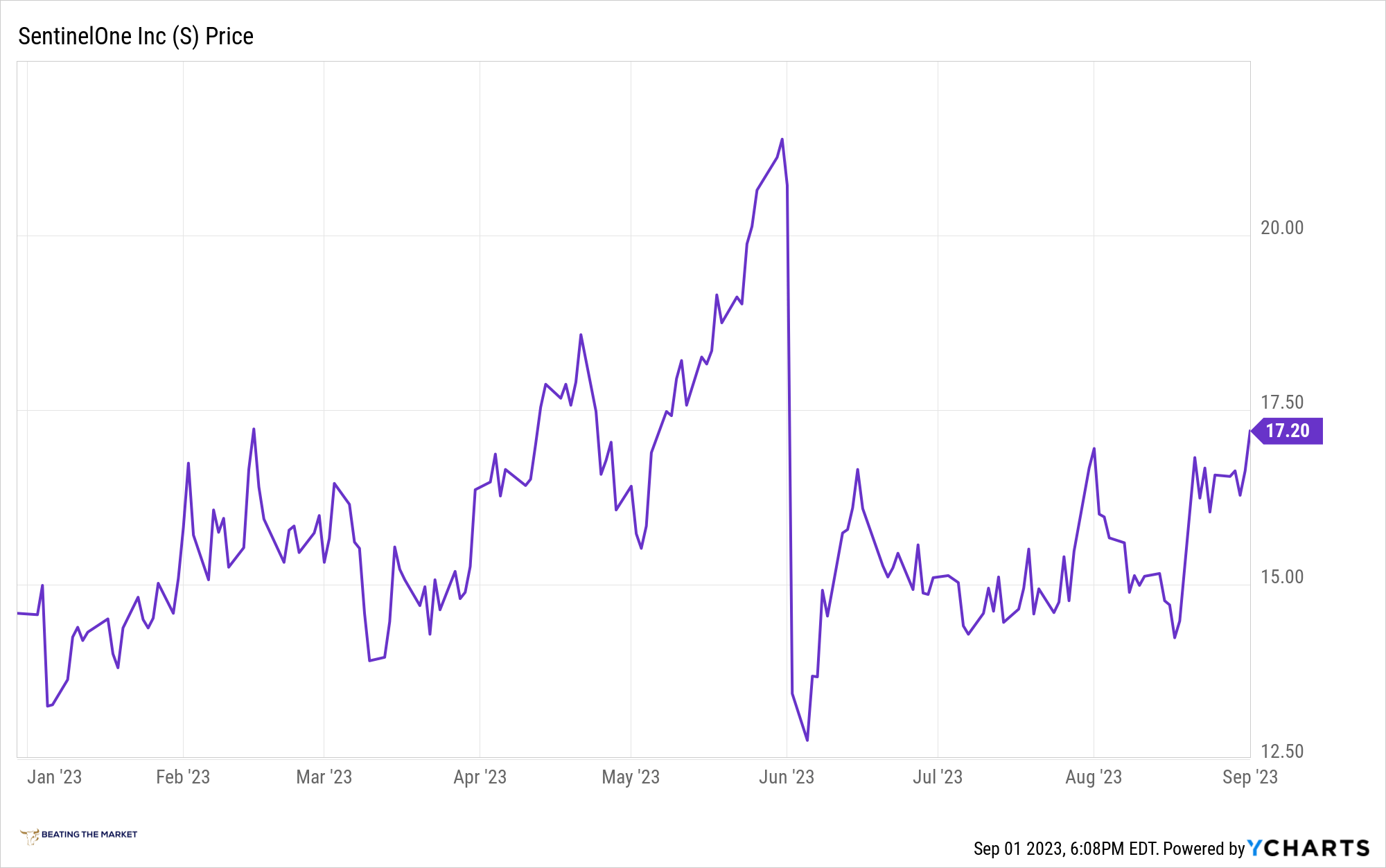

All of this has contributed to the rollercoaster share price performance depicted in the chart below:

S1's Wild Ride

{kind=link}

Indeed, it's been a ride.

But! following yesterday's report, we now have clarity on each of these points of controversy. We now have resolutions to each of these points of controversy.

1. S1's accounting issue has been addressed. Following the Q1 2023 report, I understood quite well how they could find themselves in the situation in which they found themselves. In Q1 2023, S1 had only been operating its usage-based business for about a year. Historically, S1 was exclusively a seat-based, subscription model, so the usage-based model was new to them from an accounting perspective, and it was new to them as a public company, where mistakes are very visible. Additionally, Snowflake ( SNOW ), yes, the mighty Snowflake, which is purely a usage-based business, experienced 0% growth in the month of April in Q1 2023. The degree to which this was surprising cannot be overstated. The reason Snowflake experienced 0% growth was that a few very large accounts reduced data storage on the platform, leading to a large near term reduction in the company's growth. The identical situation played out for S1, i.e., there was a reduction in consumption of its data platform, and this created the ARR accounting issues. As of today, S1 says it has taken the necessary steps to remediate this accounting issue, and we should not see this happen again looking forward.

Before turning to our costs and margins, I'd like to provide an update related to the ARR adjustment we announced in Q1. After conducting a comprehensive review, we implemented robust controls, improved processes and enhanced our ARR reporting structure.

In addition, we partnered with a big four accounting firm to objectively validate our processes and controls. Our systems are fully remediated and we're glad this issue is behind us.

Dave Bernhardt, CFO, Q2 2023 SentinelOne Earnings Call (emphasis added).

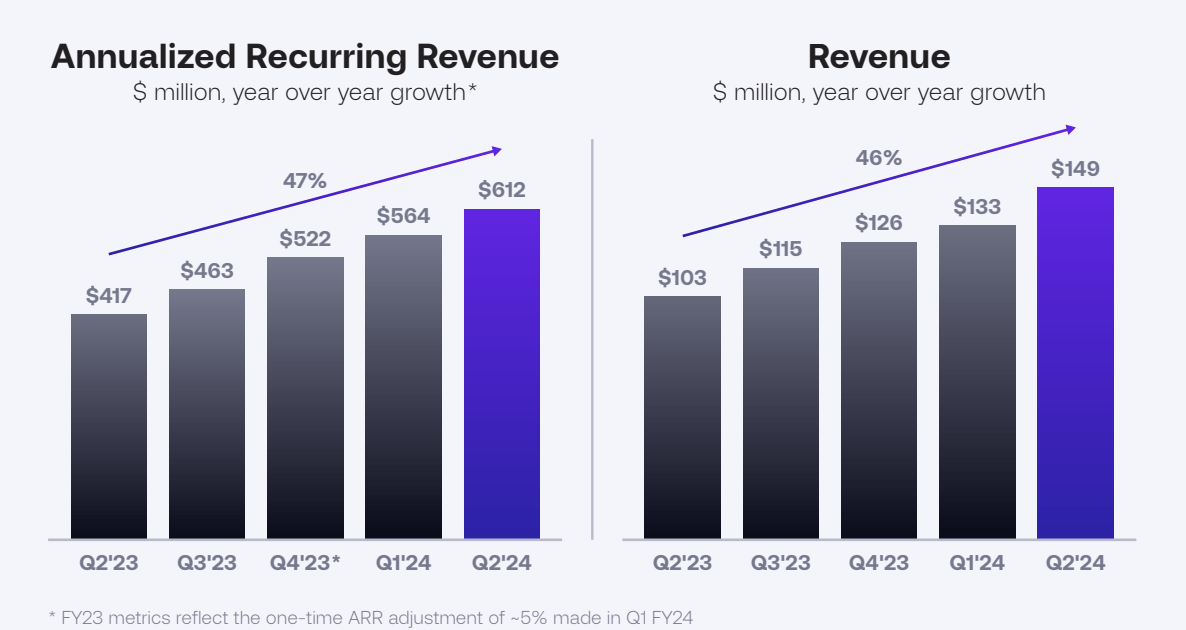

2. As I expected heading into this print, S1's guide for Q2 was excessively conservative, and this was proven true. S1 beat its guide by a mile, with sales for the quarter coming in at $149M vs. S1's guide of just $141M. We will discuss core business performance in a moment. Here's a snapshot of the absolutely stellar results from Q2 2023 (emphasis added):

Revenue grew 46% in the second quarter, and our ARR grew 47% to $612 million. We added net new ARR of $49 million in the quarter, achieving strong sequential growth of 17%. Our growth was also balanced across geographies with higher growth in Europe and Asia. Revenue from international markets grew 57% , representing 36% of revenue. We continue to achieve a healthy mix of new customers and existing customer expansion.

Dave Bernhardt, CFO, Q2 2023 SentinelOne Earnings Call

3. S1 is not selling itself. While nothing is guaranteed ultimately, I am very confident that S1 will not sell itself. I remarked often in response to the sale rumors that it simply made no sense. The business has one of the fastest growing cloud offerings in the world at the moment. Below, I will demonstrate that S1's products are industry leading. I've spoken with users of the platform who have raved about it. Mr. Weingarten is a genuine thought leader in the industry who has built one of the most technologically advanced and effective platforms in the world. S1 consistently places 1st in the annual MITRE ATT&CK evaluation, and its offerings are highly rated on platforms like Gartner Peer Insights. S1 only burned $5M in cash in the quarter, grew ARR at 47%, and it has $1.1B in cash & investments and no debt. The business achieved record gross margins of ~77% in Q2 2023. The business has robust gross profit margins, generates very healthy gross profits, which it can use to reinvest and evolve the platform, now operates approximately free cash flow breakeven, and has a truly mountainous liquidity position alongside no debt.

Mr. Weingarten is a brilliant technologist himself who is only about 40 years old. I believe and have vehemently believed that he would help lead and steward the cybersecurity industry for decades to come, while his public market peers will retire in the next 5-10 years. To quit now simply made no sense to me in light of these objective data points. In this vein, I found Mr. Weingarten's commentary noteworthy (he's worth listening to on every call, but here's some commentary on selling the company).

First, S1's Consistent Dominance In The MITRE ATT&CK Evaluation

Pax8

SentinelOne

SentinelOne had two reconfigurations around network activity but was able to score highest in the area of prevention. The company has now been at the top of these charts for three years running.

Source .

Let's hear from Mr. Weingarten apropos of selling S1 and the dissolution of the former configuration of the Wiz partnership. The quote is a bit long, but I believe it's necessary for us to read these ideas from the man stewarding our capital at the helm of S1 (emphasis added):

We don't comment on rumors or speculation, but let me be clear. I mean our focus is on building an independent company for the long-term. we're delivering substantial growth and margin improvement. And most importantly, we have the best technology and a clear strategic road map to disrupt a $100 billion market with the potential to multiply our current market share in the coming years. I think also our teams are executing well. Competitive positioning remains incredibly strong. We delivered excellent results. All in all, I think you're just seeing us being laser-focused on delivering the best innovation we can, the best protection we can for our customers, maximizing our business potential. We believe we can do that the best as possible as a public independent transparent company. And I think that is as clear as I can be.

On the Wiz thing, if you kind of bundle it on the acquisition rumors and all that stuff, I mean, again, I'm not going to comment on that, but it's all pure speculation on their part and far from fact. So it's, again, a head scratcher to me.

If we kind of pivot to the partnership, we did not terminate the partnership. I think that's again misconstrued. We actually canceled a reseller agreement, a reselling agreement . So we still partner with Wiz, we still work with them on the field level. We still think there's some form of complementary technology there, and we're focused on delivering customer outcomes.

So when customers want to use Wiz, will support that. The technical integration is still there. Wiz is a nice little startup, we like working with them. But again, in terms of the reselling agreement, we didn't see any contribution from that. We didn't feel like that's something that is fulfilled on their end, so we decided to terminate that. Our cloud-native application platform is growing, I think, in a stellar pace. We're definitely ahead of our targets. We just announced cloud data security. That's a major expansion to our workload protection platform that's part of that overall seen up envelope.

And we want ourselves to be focused on our own capabilities. And I think that's natural. We're also seeing tremendous traction in that market. Obviously, triple-digit growth for our cloud business year-over-year for a few good quarters now and a couple of years now is obviously giving us a lot of confidence that we can continue and grow that, and we'll continue to develop our own native capabilities alongside that.

Tomer Weingarten, CEO, Q2 2023 SentinelOne Earnings Call.

In short,

- S1 has addressed its accounting issues, which were not nebulous. It was easy to see how a young, public company could get what they got wrong.

- S1 is not selling itself, and it is still one of the leading, if not the leading, cybersecurity platform from a technology perspective, growing customers at 30% despite battling against genuine Goliaths in the industry and against a very difficult macroeconomic environment.

- S1's cloud business is growing triple digits. It is still partnered with Wiz but not in the exact manner in which it was partnered with Wiz formerly.

Speaking of S1's cloud business, let's now turn to a consideration of that business and its industry.

SentinelOne's Very Noteworthy Cloud Business

While S1 has not confirmed the size of its cloud security business, analysts in the grapevine have speculated that it's about 10% of sales presently, growing at ~100%.

Notably, it was speculated that it's been growing at ~100% for the last six months or so, and, on S1's most recent call, we received confirmation that that has been the case (emphasis added):

Alex Henderson: Nice rebound in the quarter. Clearly, if you listen, and I'm sure you did, to the CrowdStrike ( CRWD ) presentation. They delineated the scale and some of the growth rates around some of their products. And I was hoping maybe you could take a page out of their book and give us some of the -- some granularity around some of these key products that you call out, whether it be the cloud product, Vigilance, Ranger, pick your category? Thanks.

Tomer Weingarten: I think at our scale, I mean, we're not at a point that we're ready to disclose that. I think we're giving you good indications as to what part of our portfolio is going. We're giving you an indication that more than 30% of our revenue contribution is coming from outside of endpoint. We're giving an indication we gave last quarter that cloud is growing incredibly fast, triple-digit year-over-year represents well over 20% of quarterly ACVs on average, if you kind of look at the rearview mirror in the last 12 months.

So all in all, I think that can give you some sense. I also think that for us, data analytics and security data lake, the Singularity data lake, these capabilities are just coming online. And they're coming online pretty fast. So hopefully, as we gain a little bit more scale, I think we'll be able to disclose much more on how we look at our business. But right now, obviously, we're just focused on growing as fast as we can between these core TAMs that we identified are strategic to our growth.

Q2 2023 SentinelOne Earnings Call.

Earlier on the call, Mr. Weingarten remarked (emphasis added):

Obviously, triple-digit growth for our cloud business year-over-year for a few good quarters now and a couple of years now is obviously giving us a lot of confidence that we can continue and grow that, and we'll continue to develop our own native capabilities alongside that.

Tomer Weingarten, CEO, Q2 2023 SentinelOne Earnings Call.

And this level of growth makes S1 one of the fastest growing cloud workload protection vendors in the world, as a study of the below chart would indicate.

IDC

I believe this chart to be central to our ownership of both S1 and CrowdStrike.

The Cloud Workload Security (Protection) industry is projected to continue its torrid growth rate for the next decade, and I believe this projection makes sense based on a couple data points.

First, the growth of cloud computing will likely continue for decades to come.

IOT Analytics

We’ve spent a fair bit of time analyzing what we’re seeing, and I’ve spent a good chunk of time myself looking as well, and we like the fundamentals of what we’re seeing in AWS. The new customer pipeline looks strong. The set of ongoing migrations of workloads to AWS is strong. The product innovation and delivery is rapid and compelling. And people sometimes forget that 90-plus percent of global IT spend is still on-premises. If you believe that equation is going to flip, which we do, it’s going to move to the cloud. And having the cloud infrastructure offering with the broadest functionality by a fair bit, the best securing operational performance and the largest partner ecosystem bodes well for us moving forward.

Andy Jassy, CEO, Amazon Q1 2023 Earnings Call (emphasis added).

With continued elevated growth of cloud workloads, there will correspondingly be continued elevated growth of cloud workload security demand.

Cloud Workload Protection Industry

Data Bridge Market Research

And this is the total addressable market, or TAM, in which S1's cloud security business has grown at 100%+ for the last few quarters.

Notably, S1 is the most highly rated Cloud Security platform according to Gartner's Product Reviews:

Singularity Cloud By S1 Is The Highest Rated Cloud Workload Protection Platform On Gartner Peer Insights

{kind=link}

Based on this, it makes sense the S1's Cloud Security business has grown at the rate at which it has grown.

With these total addressable market data points in mind, I believe S1's cloud business could sustain elevated growth for the decade to come and beyond. It very well could alone(!) justify S1's entire enterprise value currently, and I do not believe that's an exaggeration in any sense, especially when we consider Wiz's valuation.

Turning To S1's Q2 2023

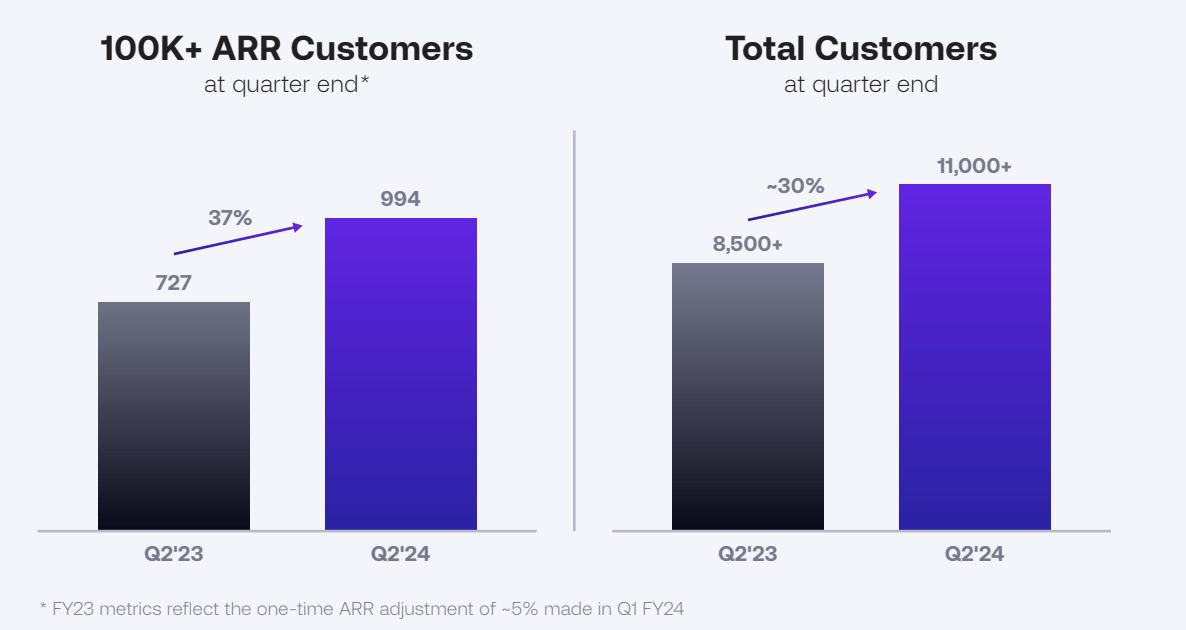

Our momentum with large enterprises was particularly strong, as our customers with ARR of $100,000 or more grew 37% year-over-year to 994, even faster than total customer count. Our business mix from customers with ARR of $100,000 or more continued to increase, due to our success with larger enterprises, our partner ecosystem, and broader platform adoption.

S1 had a very strong quarter in terms of customer growth, as can be seen below.

SentinelOne Q2 2023 Shareholder Letter

{kind=link}

Notably, S1's total customers metric, which grew at 30%, does not include customers from its MSSP network, suggesting that S1's technology is deployed to many more end users than its total customers metric suggests.

At any rate, 30% growth of customers in this macro-environment is stellar in my eyes.

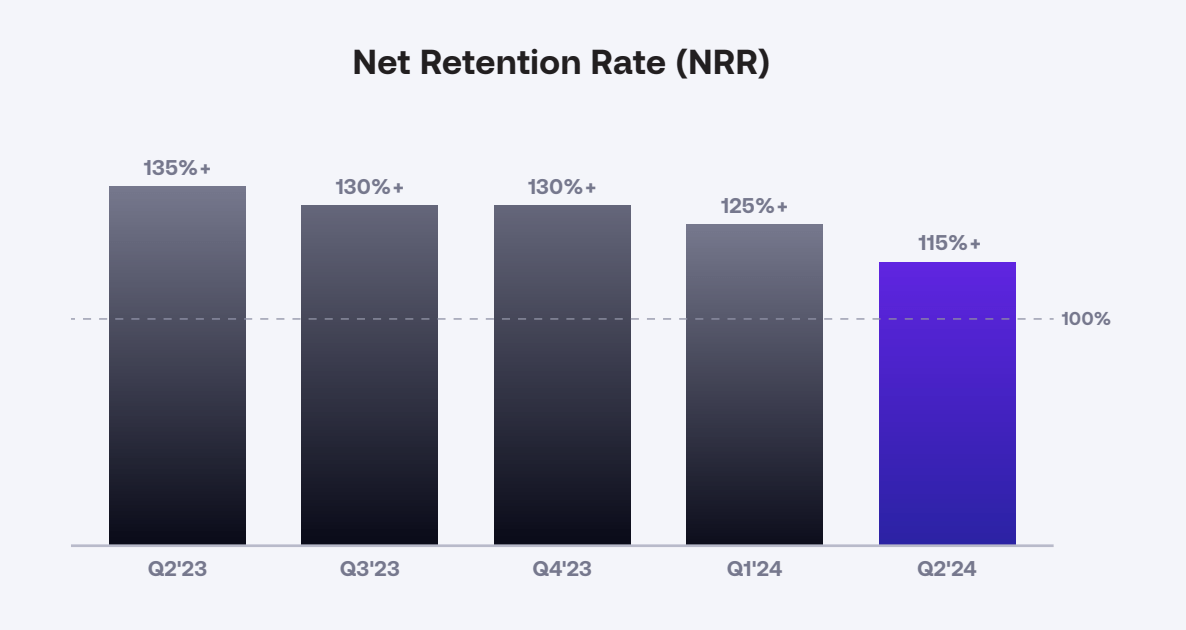

Turning to NRR, S1's NRR disappointed me a bit, but, on the call, it was revealed that sans Attivo's business, which is an identity platform S1 acquired in the past, its core business' NRR was 120%, which is incredible and in line with the performance I would expect from S1.

SentinelOne Q2 2023 Shareholder Letter

{kind=link}

That said, even 115% NRR for a company of S1's age is fantastic. This represents the 95th percentile+ (I don't know precisely where it ranks, but it's certainly, certainly best of breed) of all SaaS businesses on earth, most of whom have NRRs hovering around 100%; in this economy, likely lower.

I think it's worth taking a moment to note this: Our SaaS businesses, from Snowflake to monday.com ( MNDY ) to CrowdStrike to SentinelOne to Okta ( OKTA ), are truly the best of the best next gen SaaS businesses on earth. Period.

In no uncertain terms, these are the Usain Bolts of the SaaS industry.

I say this with every ounce of humility as a partner to these companies. This is the statistical reality however.

Turning to the recently quite controversial ARR metric, as we can see below, S1, like Snowflake and Okta, grew ARR and revenue at its healthiest rate in quite some time.

SentinelOne Q2 2023 Shareholder Letter

{kind=link}

As of today, S1's ARR is now likely hovering at roughly $650M. The business trades at an enterprise value of about $4.675B, implying an EV to ARR multiple of about 7.19x. Based on S1's Q2 2023 report, I believe it remains about 50% undervalued; however, I do understand the market's contention here on some level: We are in some version of stagflation. For instance, here are some data points impacting the valuation of S1 currently:

- Interest rates on credit cards are the highest they've been in over 30 years.

- We just experienced the fastest interest rate hiking cycle in American history after 1.4x'ing the money supply.

- The combination of giant inflation and wickedly tight credit has created a genuine affordability crisis for the lower and middle class in America and likely in many countries around the world.

- Unemployment recently began to rise, and job openings are collapsing 08-09 style.

- Inflation is still persisting!

These economic realities will likely keep the valuations of many of our companies depressed, suggesting that we can continue to accumulate them at discounts to fair value.

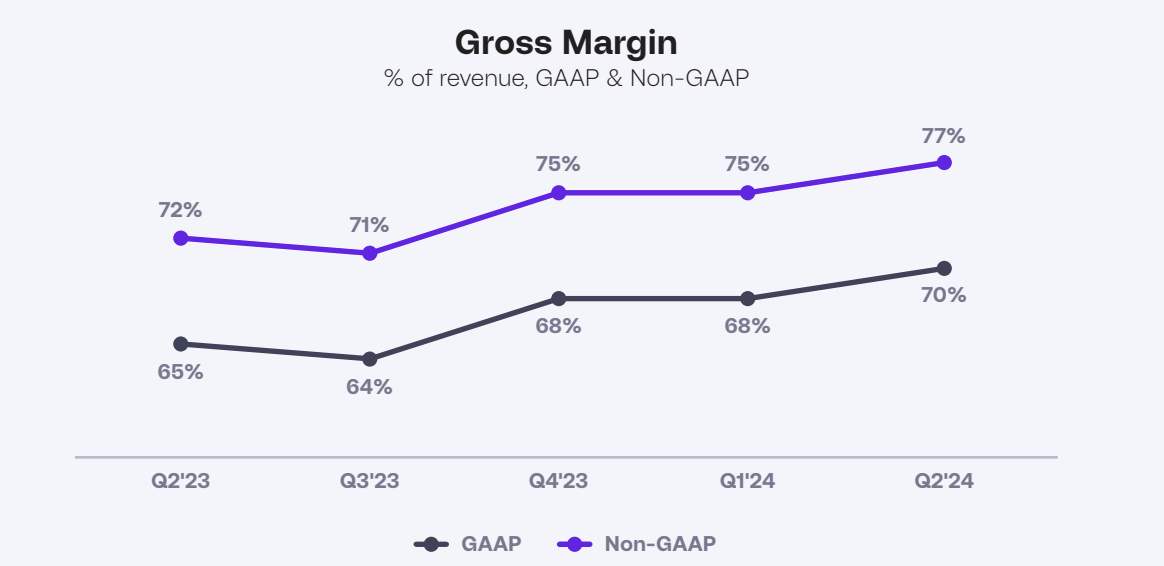

Turning to S1's gross margins, they came in at their highest levels ever.

SentinelOne Q2 2023 Shareholder Letter

{kind=link}

This is fantastic as it gives S1 even more cash with which it can reinvest in its business and drive elevated growth for decades to come.

It also removes strain on S1's mountainous cash hoard of ~$1.1B, which we will analyze in just a moment.

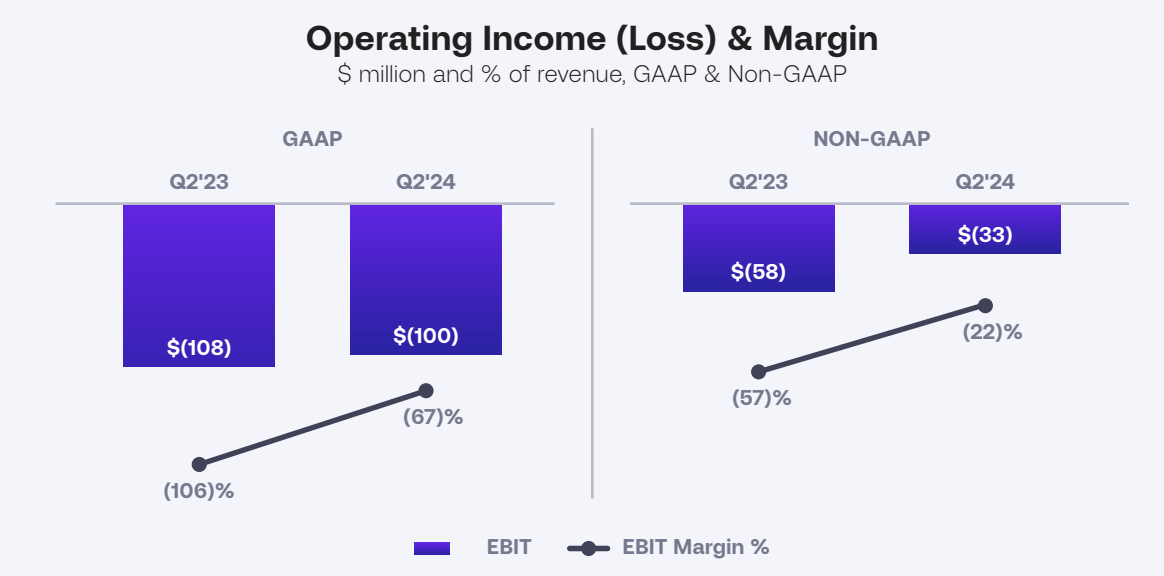

Turning to S1's bottom line, it's been improving, though it's still at a loss.

I don't take substantial issue with this because I understand S1 is still a young company, and I trust Mr. Weingarten to steward our capital in intelligent ways that create industry leading products for our customers, which thereby creates elevated sales and underlying profits growth for years and decades to come.

SentinelOne Q2 2023 Shareholder Letter

{kind=link}

Before we close today, I'd like to take just a moment to discuss S1's balance sheet.

Concluding Thoughts: S1's Pristine Balance Sheet

Net cash used in operating activities was $(12) million, compared to $(62) million a year ago. Free cash flow was $(15) million in Q2, compared to $(67) million a year ago.

Dave Bernhardt, CFO, Q2 2023 SentinelOne Earnings Call.

S1 burned only $5M in cash in the quarter, though its free cash flow was -$15M.

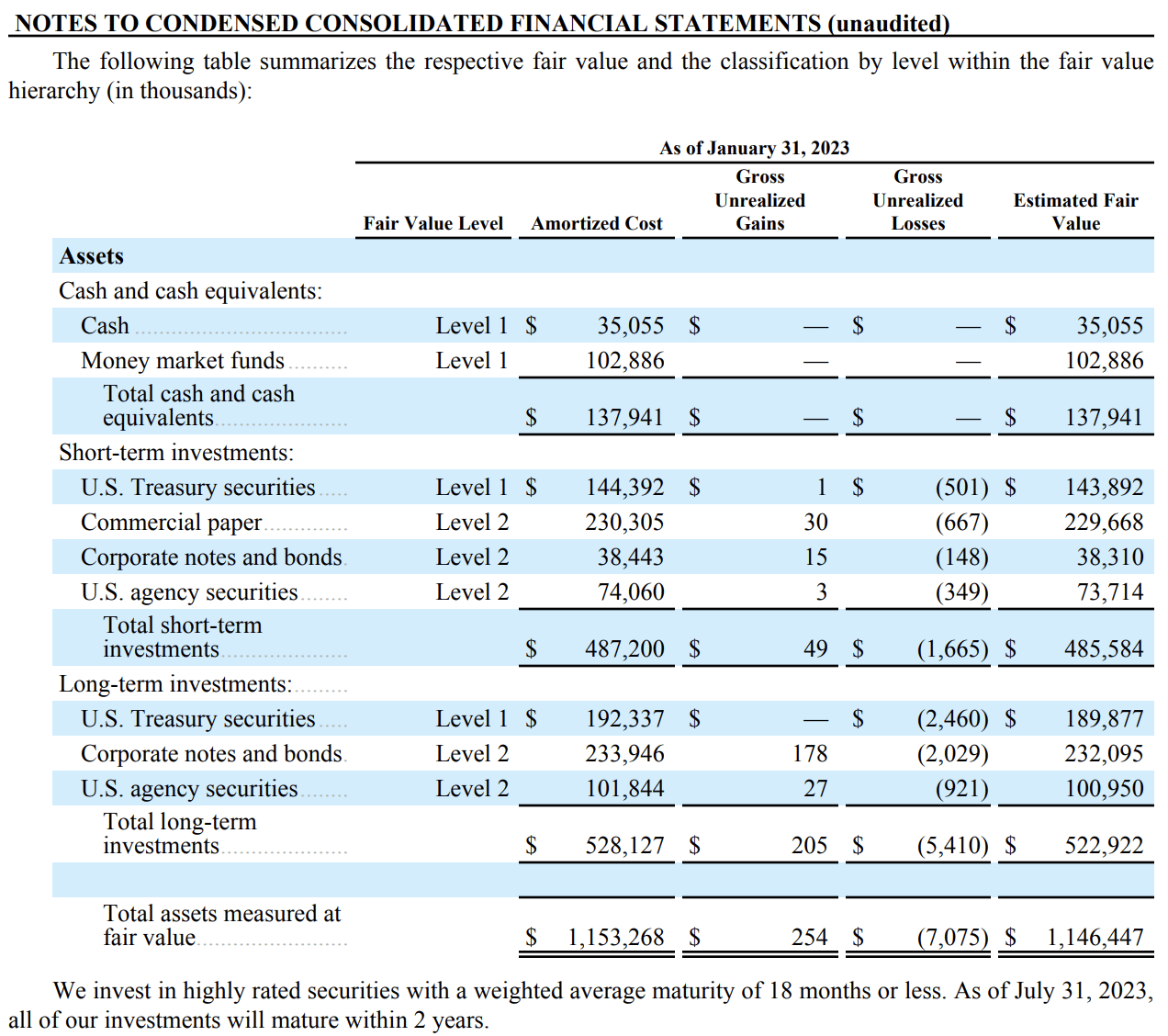

The $10M delta here was attributable to the configuration of S1's balance sheet , which we can see below.

{kind=link}

As we can see, S1 has invested its $1.1B in a variety of interest bearing securities, which has given it further latitude to operate free cash flow negative, pushing as hard as they can upward on growth rates and market share capture and innovation of S1's platform.

It really cannot be overstated how massive a $1.1B cash hoard alongside no debt is for a company of S1's maturity.

As with all of our businesses, the cash hoard is so large as to almost be a caricature of most young enterprises' economic realities.

It's almost ridiculous to have this much cash on its balance sheet.

But, notably, the cash hoards of our companies have been key to our theses. I would not feel nearly as emboldened to bet on these younger companies... to bet my entire life and livelihood on these young companies, e.g., Monday, Marqeta ( MQ ), and SentinelOne, as a few examples... were it not for their mountainous cash hoards and no debt.

In closing, following this quarter, I've never felt better about S1, and I, with great conviction this time, will #neversell for the decade ahead.

For further details see:

SentinelOne: Operating From Strength With $1.1 Billion In Liquidity And No Debt