S - SentinelOne: Why I Am Bullish In 2024

2024-01-12 09:45:21 ET

Summary

- In 2024, I project strong commercial success for SentinelOne, expecting over 30% YoY topline growth and improved profitability.

- The demand for cybersecurity is increasing, supported by CIO surveys and the adoption of GenAI, which will benefit SentinelOne's momentum.

- Considering updated valuation metrics, I estimate the intrinsic value of SentinelOne to be around $27.6 per share.

After my Q1 "Buy" recommendation for SentinelOne (S), I am revisiting my thesis for the cybersecurity company with a focus on 2024 and beyond: Heading into the new year, I argue that SentinelOne is poised for more commercial success, likely achieving >30% YoY topline growth and a bullish inflection on profitability. On that note, I point out that various CIO surveys signal a surge in cybersecurity demand, also carried by GenAi adoption, which may accelerate SentinelOne's strong momentum through 2025.

Despite this promising business outlook, the current trading price of SentinelOne shares appears cheap, with the stock trading on a 10x EV/sales, compared to almost 19x for key competitor CrowdStrike (CRWD). Considering updated valuation metrics, I estimate the intrinsic value of SentinelOne to be around $27.6 per share, with a favorable sensitivity skew on rates.

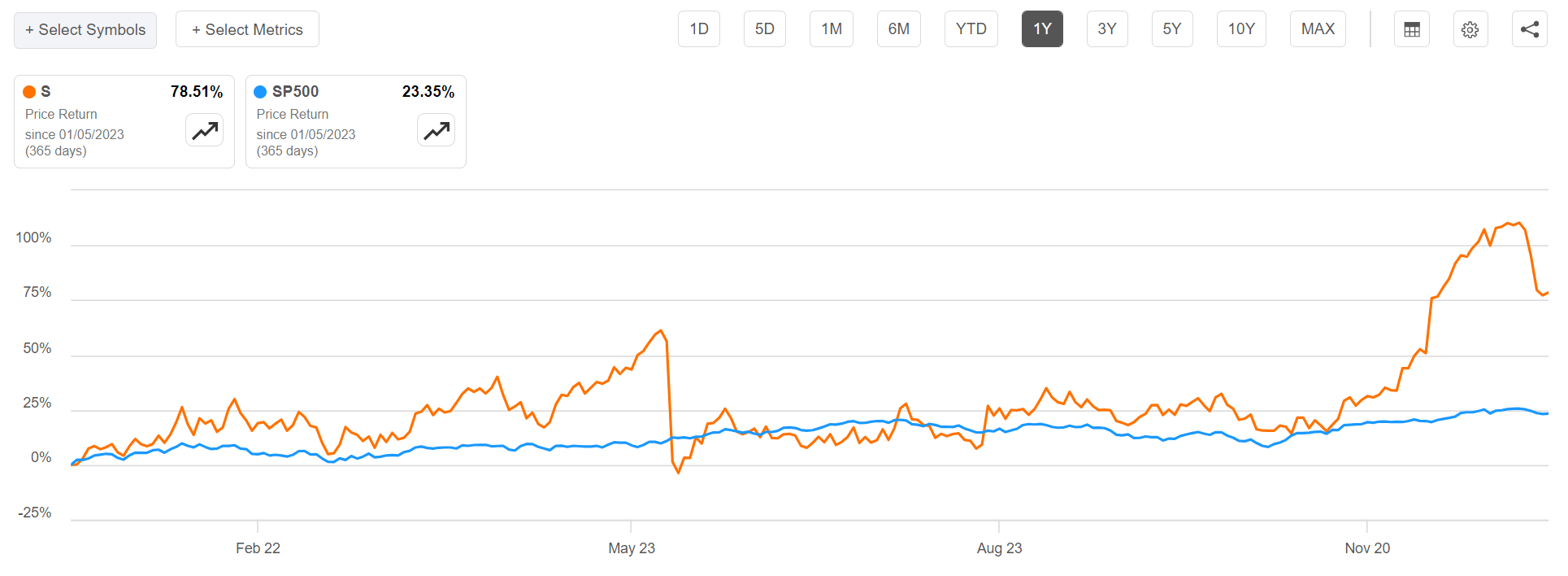

For context, SentinelOne stock has strongly outperformed the broad U.S. equities market in 2023. For the trailing twelve months, SentinelOne shares are up about 79%, compared to a gain of approximately 23% for the S&P 500 ( SP500 ).

{kind=link}

2024 May Support A Cybersecurity Bull Market

Heading into 2024, the broader landscape for IT budgets appears to be improving, supported by insights from Q3 conference discussions indicating shorter sales cycles for new clients and quicker billing cycles for existing customers. The momentum is especially supportive for cybersecurity spending, as rising geopolitical tensions and evolving security challenges linked to GenAI advancements push the need for capable cyber defense (think deep-fakes, data poisoning, and adversarial attacks). Notably, in 2023 the threat landscape continued to deteriorate compared to the previous year. Qualys reported a total of 26,447 disclosed vulnerabilities for the year, topping the number of vulnerabilities disclosed in 2022 by more than 1,500. This increases the number of vulnerabilities for the seventh consecutive year.

In that context, insights from the Piper Sandler 2024 CIO Survey reinforced this optimistic outlook (Source: research note dated 11th December) , and revealed that security spending tops the investment priority list of key IT budget decision makers. In fact, a significant majority of respondents expects increased spending on cybersecurity in 2024, particularly in key categories like Cloud Security, Endpoint Security, Threat Intelligence, and Network Detection & Response—disciplines that align well with SentinelOne's core strengths. Similarly, findings from the UBS Evidence Lab AI Survey also highlight the expectation of expanding cybersecurity budgets, pointing to GenAI adoption and related consequences as a focal point within security concerns (Source: Research note dated 17th December) .

Expect Margin Expansion On >30% YoY Topline Growth

SentinelOne is poised to leverage a growing demand for cybersecurity, as the company offers industry-leading capabilities in EDR and MDR through its Singularity platform. Moreover, the company is continuously advancing its product portfolio: In 2023 SentinelOne introduced Purple AI, AI-based security across endpoint, and plans to expand its cloud product line by establishing a comprehensive CNAPP platform in the upcoming year.

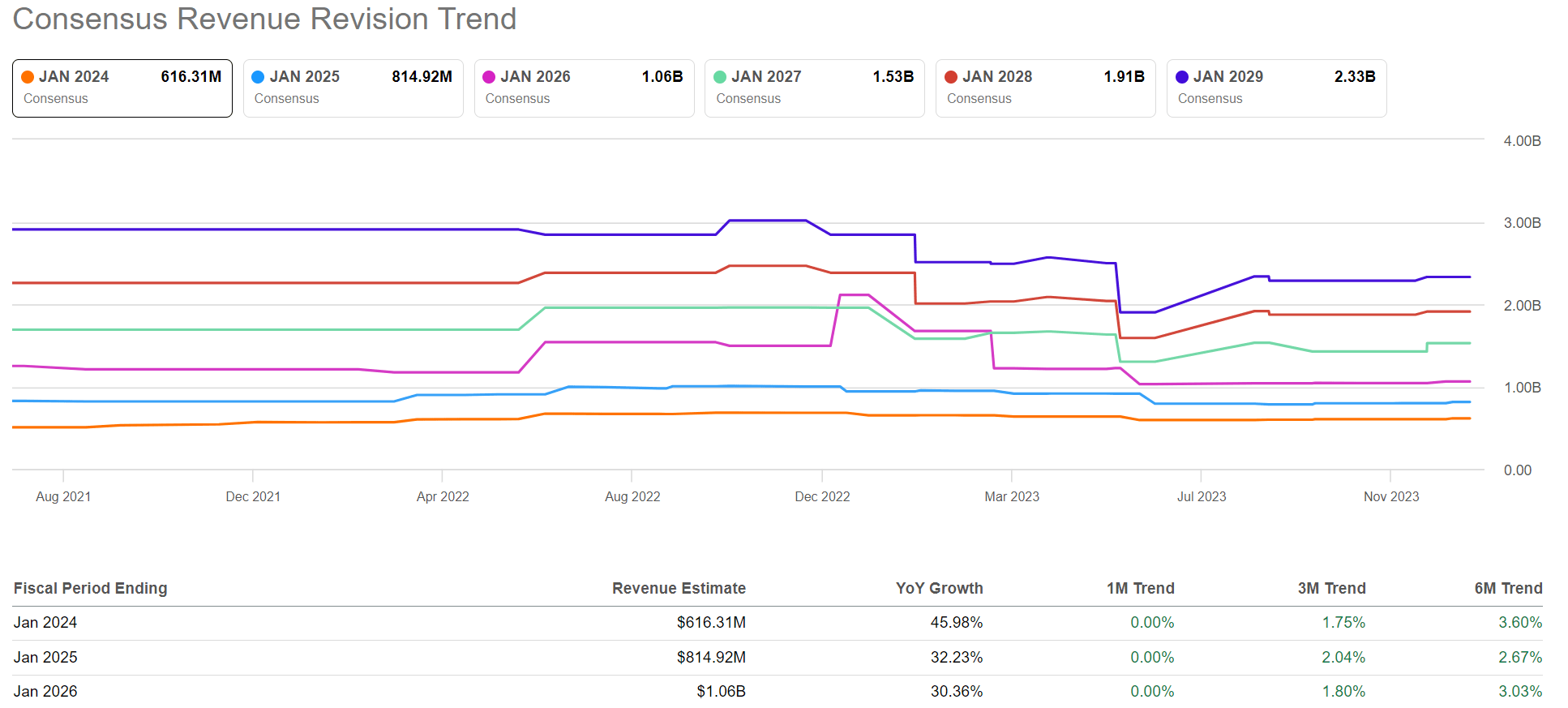

In Q3 2024 , SentinelOne surpassed expectations by generating $164 million in total revenues and $52 million in net new ARR. Revenue growth equalled to 42% YoY and topped consensus projections by $8 million. Moreover, upselling of non-EDR modules, coupled with improving scale and cost efficiencies, led to gross and operating margins of 79% and -11%, respectively—beating Street estimates of 76% and -22%. Extrapolating SentinelOne's strong trajectory in the most recent quarter into the calendar year 2024, and also adding a margin of safety, it is reasonable to project >30% YoY growth in topline.

{kind=link}

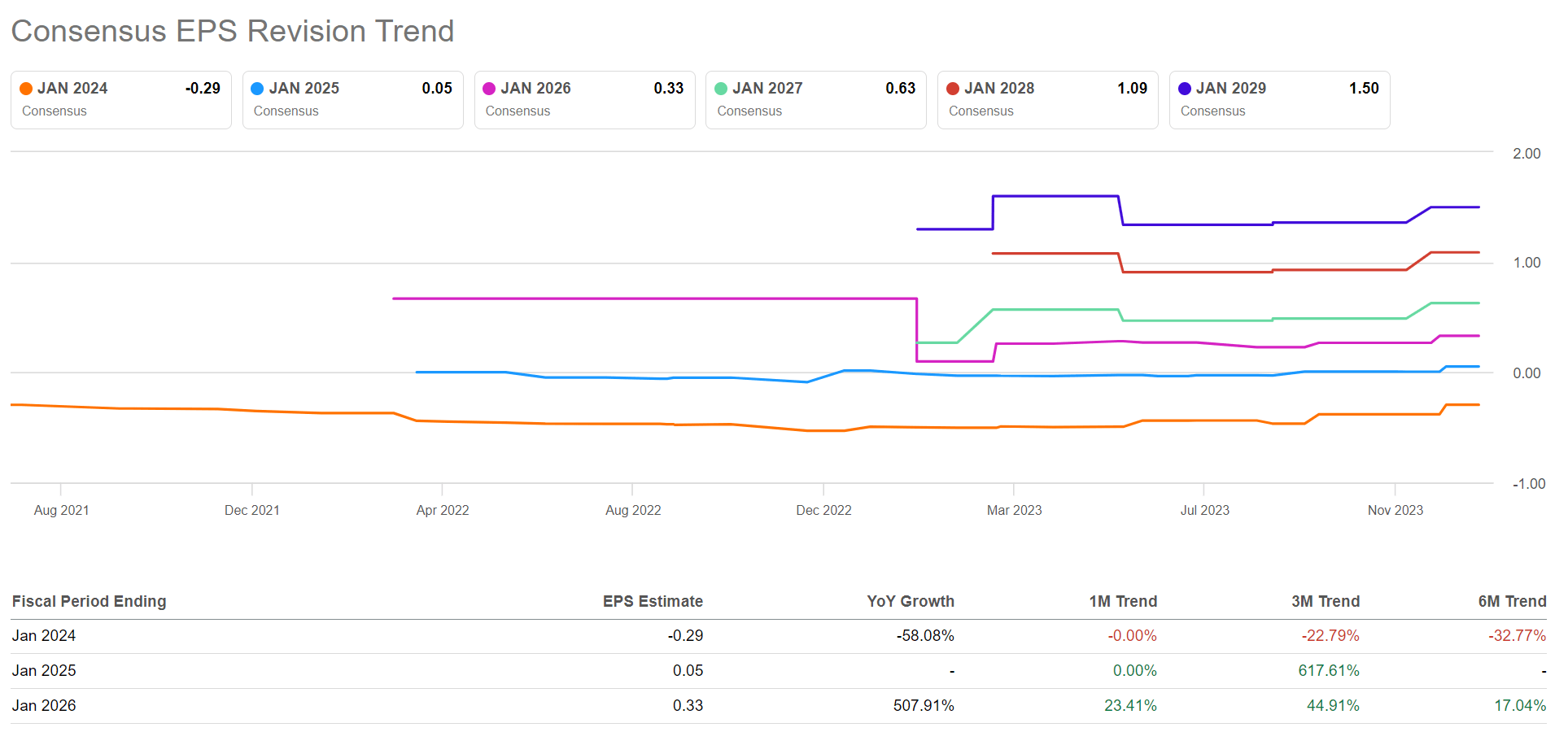

Moreover, on the backdrop of a favorable pricing environment and focus on operating discipline, SentinelOne may manage to break even on profitability, with consensus expecting 0.05 cent of EPS in FY 2025. This assumption is anchored on SentinelOne's recent track-record to grow topline at a faster rate than costs, with CFO Dave Bernhardt saying to "thoughtfully manage [our] costs" and "committed to [building on this progress] and achieving positive free cash flow in the second half of our next fiscal year".

{kind=link}

SentinelOne Could Be An Acquisition Target

2024 will likely see a trend toward IT vendor consolidation, as buyers look to streamline their purchasing processes in a highly fragmented landscape. Specifically in cybersecurity there are arguable too many names that may lead a consolidation charge, pointing to players like Palo Alto Networks, Zscaler, CrowdStrike, Fortinet, Microsoft, Cisco, and Okta. Moreover, falling interest rates are poised to be supportive for buyout financing.

On that note, I highlight that SentinelOne is likely to be a key target, rather than a buyer. Already in August 2023, rumors surfaced that SentinelOne management might be looking for buyer. In that context, SentinelOne reportedly hired investment boutique Catalyst Advisors to evaluate the possibility of a sale. Additional rumors suggested that Cisco (CSCO) and Wiz might have evaluated a bit. Although SentinelOne CEO and founder Tomer Weingarten recently said that "the company is not for sale", this commentary may be only postering to negotiate for a higher takeover bid.

Adjust Target Price to $27.6

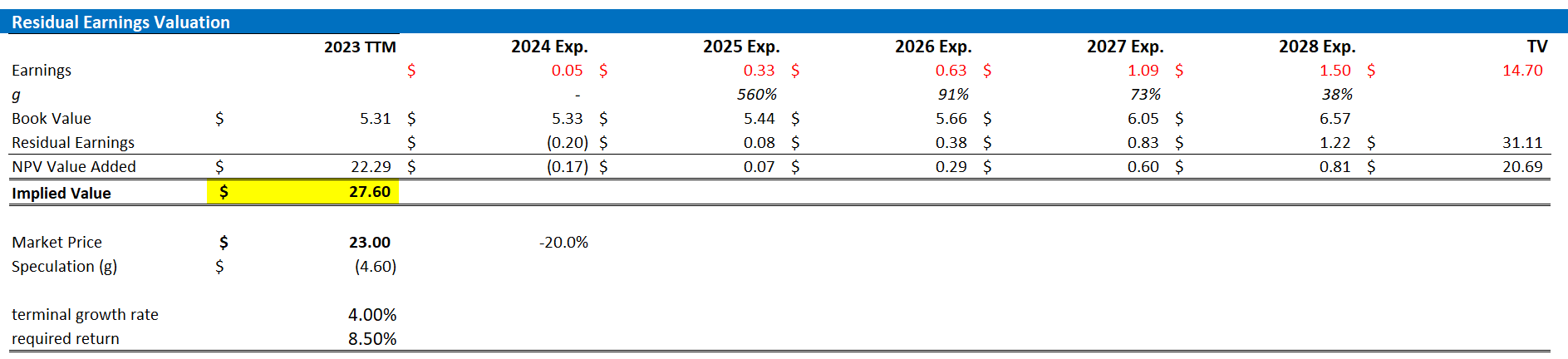

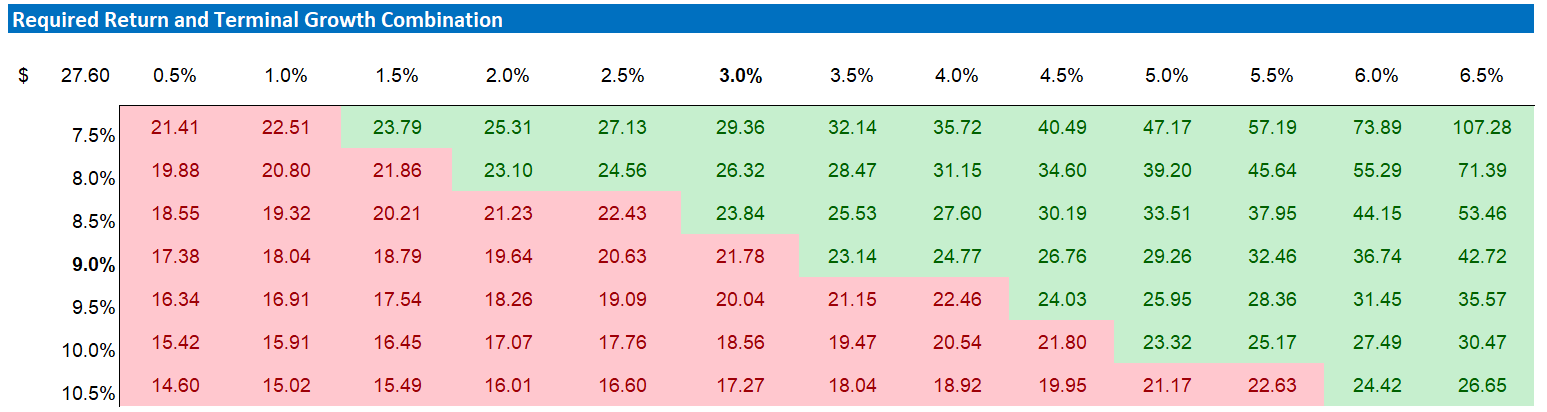

Reflecting a bullish backdrop, and in line with updated analyst consensus EPS estimates for SentinelOne through 2028, I adjust my residual earnings model for the company's stock: For FY 2024, I now estimate that SentinelOne's EPS will likely fall within the range of between $0.0 and 0.1 (non-GAAP). For FY 2025, and FY 2026 I set my EPS expectation at $0.33 and $0.6, respectively. Lastly, while I maintain my cost of equity assumption at 8.5%, I raise my terminal rate outlook by 50 basis points, to 4%, mostly as a consequence of the accelerating demand for cybersecurity products.

On the backdrop of the adjustments highlighted above, I now calculate a fair implied stock price for SentinelOne stock equal to $27.6.

Note: the table enclosed references calendar year, not financial year!

SentinelOne financials, author's estimates and calculation

{kind=link}

Below is also the updated sensitivity table.

SentinelOne financials, author's estimates and calculation

{kind=link}

A Note On Risks

Investing in SentinelOne stock, like every equity investment, also comes with risks: Firstly, investors should note that SentinelOne is currently operating at a loss, with no guarantee that the company will ever reach operating profitability. Secondly, adverse macroeconomic conditions, such as inflation and supply chain disruptions, might negatively impact SentinelOne's clientele, potentially pressuring SentinelOne's financial prospects. Thirdly, I point out that there are quite a few notable names competition in the cybersecurity sector, e.g., Palo Alto, Fortinet, CrowdStrike, Microsoft, etc. If competitive dynamics were to accelerate, SentinelOne's profitability margins and EPS estimates may need to be revised lower. Fourthly, the current volatility in SentinelOne's share price is influenced by investor sentiment toward risk and growth assets. This means that shares may fluctuate even though the company's underlying fundamentals remain unchanged. Specifically, I point out the importance of interest rate levels, as higher yields would increase discount rates and thus adversely affect the present value of long-term cash flows.

Investor Takeaway

In 2024, I project strong commercial success for SentinelOne, expecting over 30% YoY topline growth and improved profitability. My bullish sentiment is encouraged by an increasing demand for cybersecurity, supported by CIO surveys and the adoption of GenAI, which will benefit SentinelOne's momentum. Considering updated valuation metrics, I estimate the intrinsic value of SentinelOne to be around $27.6 per share. As a function of both strong commercial momentum and valuation, I reiterate a confident "Buy" recommendation for SentinelOne stock.

For further details see:

SentinelOne: Why I Am Bullish In 2024