SERA - Sera Prognostics: Buy The PreTRM Moat

2023-06-08 18:58:38 ET

Summary

- Sera Prognostics is a promising company with a mission to improve pregnancy outcomes through its blood test product, PreTRM, which identifies biomarkers linked to premature birth.

- Premature birth is a significant issue, with 1 in 10 babies born prematurely in 2021, and it is the leading cause of death in newborns at 34%.

- The company's strong balance sheet, low price/book value, and global total addressable market make it a strong buy for investors, in my opinion.

Sera Prognostics ( SERA ) is one of the more exciting companies I have come across in some time. It was recently in the news when its CEO stepped down, marking the start of a new era focusing on commercialization after years of R&D. Sera's mission is simple: to improve pregnancy outcomes for new and growing families. I review the economics of its commercial product, the potential of its product pipeline, as well as the financials and cash position. I find that this stock a buy on the basis of a global total addressable market, a low price/book value, and a strong balance sheet.

PreTRM

Sera's commercial product is a first in class blood test that is clinically proven to identify biomarkers linked with premature birth in babies. By identifying at-risk mothers, healthcare professionals can mitigate risk by effectively treating and educating the mother predisposed to premature birth. For example, a paper documented in the NIH National Library of Medicine recommends:

"Appropriate measures for reducing the preterm birth risk in the outpatient/ambulatory care sector are the vaginal application of progesterone if the cervix is found to be shortened in the second trimester, abstinence from nicotine in smokers, and avoidance of long hours and heavy physical work during pregnancy."

According to the company website, which sites further clinical research, prematurity is the leading cause of death in newborn babies at 34% of deaths. Per the CDC , approximately 1 in 10 babies were born prematurely in 2021, the latest data I could find. The problem is therefore massive.

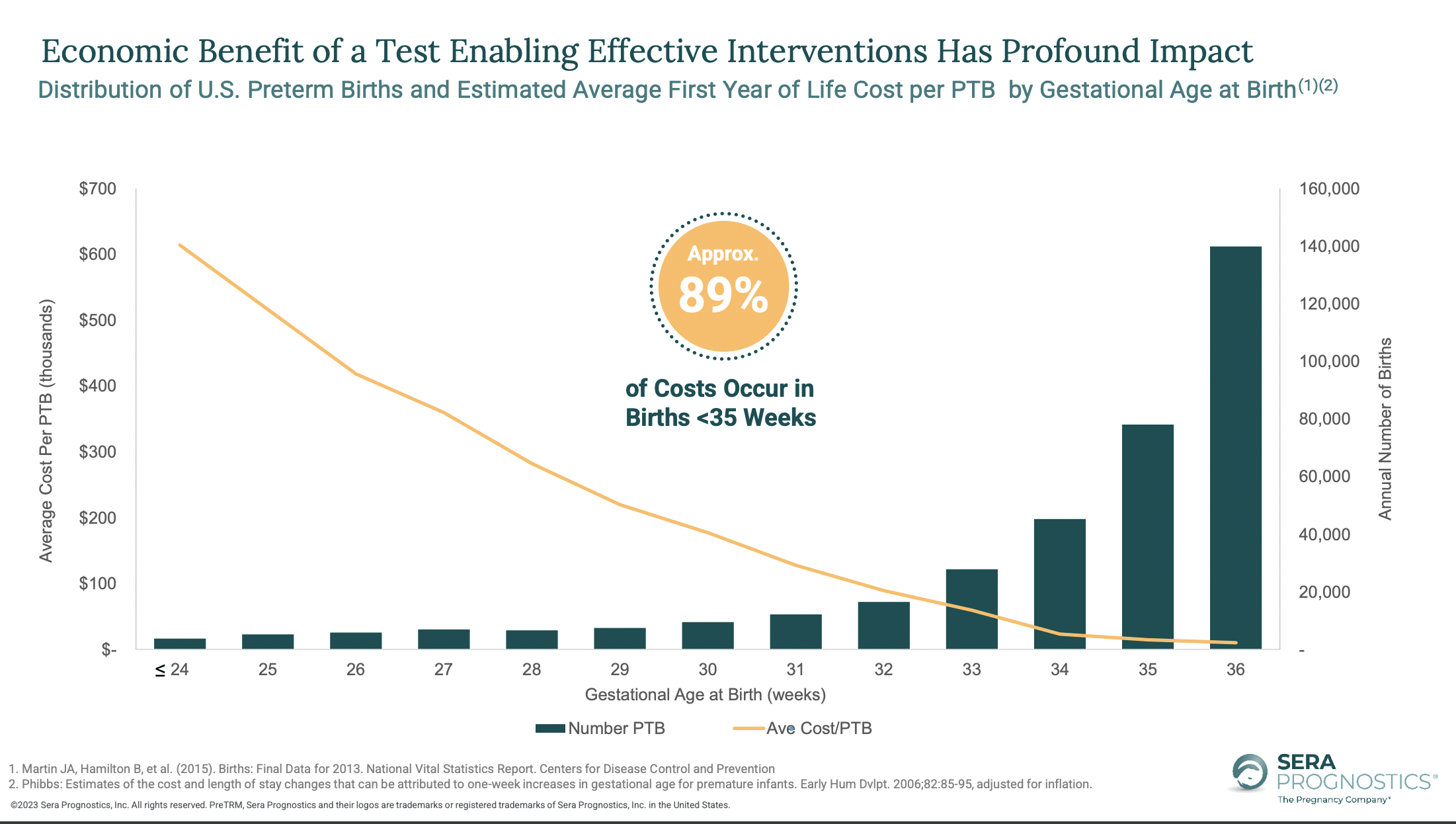

In its 2023 Corporate Presentation , Sera includes the chart below. The bars show the number of births that occur at various lengths of pregnancy. The yellow line shows the average cost. As pregnancy length increases, cost decreases. More than 90% of the total cost of births in the U.S. come from premature babies. It is therefore in the interest of the healthcare system's resources as a whole, not to mention profit maximizing insurance companies, to take measures to address premature birth, and having clarity that a mother is at risk is the first step, and this clarity Sera offers in its product. It also alleviates stress on families, who don't want their loved one to suffer from birth defects and disabilities, which are also at an increased likelihood in premature births.

{kind=link}

Sera Prognostics

Product Pipeline

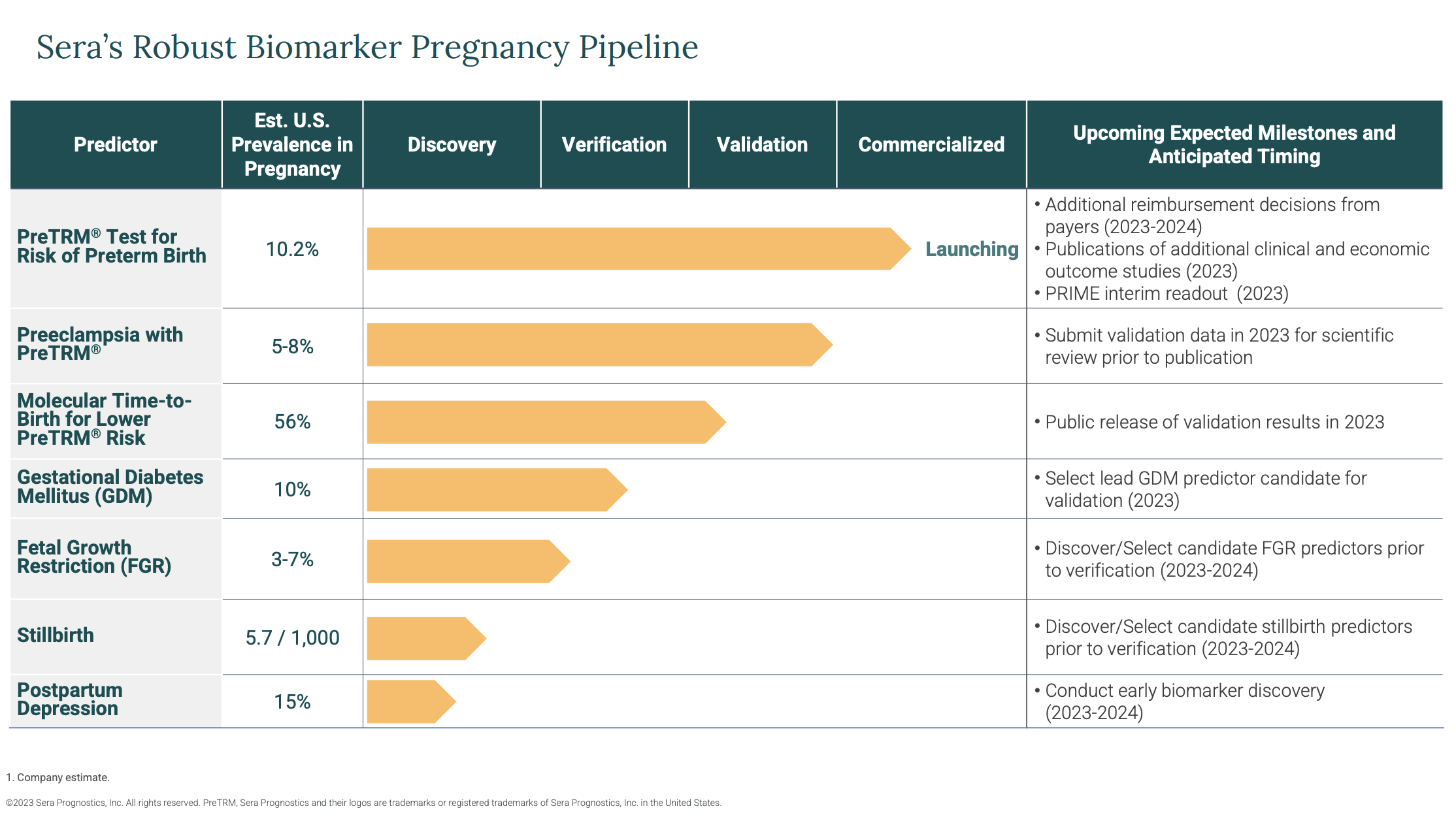

The image below, also from the 2023 Corporate Presentation, shows the stages of various biomarker based products Sera has in its pipeline. While PreTRM is the only commercialized product which they are currently launching, they have several other products such as PreTRM for Preeclampsia, high blood pressure and organ failure during pregnancy, which is estimated in 5-8% of pregnancies. They are also verifying a molecular time-to-birth solution, and verifying a predictor for Gestational Diabetes Mellitus, a condition in which the baby impedes the mother's blood sugar regulation, which is estimated in up to 10% of pregnancies per the CDC . Sera is in the mid stages of verifying a predictor for Fetal Growth Restriction, where a baby grows abnormally slowly, and this occurs in up to 7% of pregnancies according to the NIH . They are in the discovery stage of researching biomarker testing for postpartum depression, with a one-in-eight occurrence rate according to the CDC . Sera is therefore much more than its commercial product, as it has various products with large total addressable markets in various stages of the commercialization process.

{kind=link}

Sera Prognostics

Financials

Sera has grown revenue at a three year CAGR of about 95% and year-over-year it has more than tripled. Gross profit margins however have deteriorated from over 55% to around 28.8% in the span of just two years. This is likely due to inflation and increased funding of free trials for research and marketing purposes.

Despite positive gross margins, R&D and SG&A expenses both massively outweigh revenue, causing quarterly net losses that have fluctuated between $4 million and $13 million between the years 2020 and 2023. Q1 2023 R&D expense was $4.1 Million and SG&A was $7.3 Million, against revenue of around $0.1 Million. The SG&A spending has decelerated rapidly in net declines the past two quarters and R&D spending is growing somewhat steadily.

Sera's financing is mostly equity based, as it currently has an average of around 31 million fully diluted shares outstanding, a notable growth from around 15 million in 2022. Sera has no long term debt, and bought back stock while paying down debt in 2022. In March of 2023, Sera had paid in capital of $311.9 million, up from $306.5 million in March 2022 representing a capital raise of around 5.4 million. Total debt amounts to around 2.6 million. In March of 2023, Sera had $9.1 million in unearned revenue, another important source of cash that is financing operations.

The chart below shows Sera's cash burn rate. Cash peaked in June of 2021 at $90.9 million. In March of 2023, cash was $27.2 million. Over the span of around 21 months, or seven quarters, Sera burned $63.7 million in cash, or $9.1 million per quarter. At the current holding of $27.2 million, it has a runway of approximately 3 quarters at this spending rate.

Valuation

Sera has an enterprise value of just $3.8 million. This is because it has cash and short term investments amounting to $70.8 million. Cash per share is $0.88, and the book value per share is $2.91. Long term investments amount to $28.9 million. It has gross PP&E of $17.5 million. These are some serious assets Sera owns at just a market capitalization of around $101 million.

As Seeking Alpha Quant shows, on the basis of EV to sales TTM, EV-to-sales forward, and price-to-sales forward and TTM, Sera is overvalued compared to sector medians. As this company is pre-revenue for the most part, I don't think believe sales ratios adequately capture the value of this company. The book value is a much better ratio, and on this basis, Sera is undervalued compared to the sector median. Moreover, taking the 2024 revenue estimate, which is supposed to explode all the way to $7.73 million rather than the 2023 revenue estimate which is just forecasted around $832,000, the forward ratios look much better compared to sector medians

Risks

Investing in micro-cap companies has its fair share risks. Technically, a relatively small amount of capital can move the price significantly, causing volatility, and generally wide bid/ask spreads which can adversely affect the market value of an investment at any given time. In a similar vein, a very low trading volume prevents liquidity risks. The way around this difficulty is to use limit orders rather than market orders and slowly, carefully accumulate shares. This is not a trade, but rather an investment. Fundamentally, there are some risks here too. First is the fact that Sera is operating at a loss and financing its losses with unearned revenue and equity offerings. It will likely need to accelerate its cash burn rate to produce the biomarker testing from which it has unearned revenue, and dilution is a serious risk here if they cannot obtain a credit facility. The large amount of short term investments will provide this company with liquidity if it needs it, and further mitigating this risk is the fact that earnings expectations are quite low, as they are forecasted to be negative and grow little in the face of a new management attitude. The problem of operating losses is therefore likely priced into the future, although revenue growth is not and future cost controls are not, hence my buy call.

Conclusions

Sera Prognostics has a deep moat in the biomarker testing it has developed and is commercializing to help address premature births. There are no competitors that I can find after scouring the web for hours. Thermo Fisher ( TMO ) has developed a biomarker test that has recent FDA approval to detect Preeclampsia, however this product does not predict premature birth and only beats Sera in the Preeclampsia market. In all other pipeline markets, Sera still has a chance at achieving the first product on the market in the U.S, and being the first isn't always the best. In pregnant women, there is a large and steady TAM, and given the economics of the problem, it is in insurance providers' best interest to cover this testing to prevent costs later on down the road. I am bullish on new management's new cost control plans and enhanced sales strategies, which can be reviewed here . I do not think it is unlikely that in 10 years Sera is a billion dollar company. Alternatively, it could be ripening for an acquisition from a big pharmaceutical company like Thermo Fisher given its proprietary biomarker knowledge. For these reasons, I reiterate that Sera Prognostics is a buy.

For further details see:

Sera Prognostics: Buy The PreTRM Moat