SERA - Sera Prognostics Update: Recent Supportive Data Increases Probability Of Commercial Success For Preterm Birth Risk Screening

2023-03-28 06:16:32 ET

Summary

- Sera Prognostics sells PreTRM, a CLIA-lab-based assay to determine the risk of a woman having a preterm birth - a birth prior to 37 weeks of gestation.

- Having gone public in an IPO in July 2021 at $16, the Company was trading below $1.30 prior to releasing positive topline data on AVERT, a ~2,000-patient single-site study.

- The key to success will be the outcome of PRIME, a 6,000-patient study being run in partnership with Elevance Health, which is also an investor.

- On their recent earnings call, the Company reported revenue below expectations and issued guidance below analyst consensus - suggesting commercialization headwinds.

- On their recent earnings call, the Company also pointed to the end of 2023 for the interim data readout from the PRIME study, a few months delay from their estimates last year.

SERA Prognostics - Overview

Sera Prognostics ((SERA), or the Company), a Salt Lake City, Utah diagnostics company trading on the NASDAQ, sells PreTRM, a test that provides physicians an assessment of the individualized risk of premature delivery in a pregnancy. A determination of high risk enables physicians to increase their monitoring and proactive interventions in those women with higher risk.

The test is based on a proprietary predictive algorithm of the serum level of two proteins, insulin-like growth factor-binding protein 4 (IBP4) and sex hormone-binding globulin (SHBG), coupled with clinical variables consisting of a woman's height and weight. The initial algorithm output was reported from the Proteomic Assessment of Preterm Risk [PAPR] study, a study of serum from 5,501 patients published in February 2016.

The Company ran a second clinical validation study, A MulTicenteR AssEssmEnt of a SponTaneOus Preterm Birth Predictor (TREETOP) . The TREETOP study enrolled 5,011 pregnant women from 18 sites across the United States from 2016 to 2019.

TREETOP publication

Figure 1: Kaplan-Meier curve of neonatal length of stay in days for all neonates, stratified into higher- [GOLD] and lower-risk [BLUE] groups as defined by the SERA algorithm. A) Data from the PAPR study. B) Data from the TREETOP study. Source - TREETOP publication .

With the biomarkers discovered and validated in PAPR the Company ran an intervention study to determine whether risk stratification and interventions in the higher PreTRM-risk pregnancies had an impact on the preterm birth rate, on neonatal length of stay and on the costs associated with the preterm birth. The Company worked with the Intermountain Health System, based on Salt Lake City, UT, to determine if the PreTRM test could reduce the likelihood of a spontaneous preterm birth (sPTB) and associated costs. The PREVENT-PTB study enrolled 1,191 women. The study was not powered to analyze a decrease in preterm births, but, importantly, showed a substantial decrease in the number of days preterm infants spent in the neonatal intensive care unit (NICU), despite the study being stopped well short of its original enrollment goal because of funding shortfalls.

PREVENT-PTM study repor

Figure 2: Kaplan-Meier survival curves comparing length of neonatal intensive care unit stay (days) among screened (red line) and unscreened (blue line) groups. Source: PREVENT-PTM Study Report .

The NICU length of stay (LOS) was not the initial primary endpoint, but was recognized as an important pre-specified endpoint of clinical and economic importance among infants admitted for sPTB. The study demonstrated a difference between the control and study groups, with a LOS in screened patients median of 6.8 days, and a LOS in unscreened patients a median of 45.5 days. This is an 85% reduction between the screened and unscreened patients.

The substantial decrease in the number of NICU days, despite the small trial size, allowed SERA to garner substantial investor interest and raise substantial additional capital. Included in the new book of investors was Anthem (now Elevance Health ( ELV ), who owned ~10% of SERA at the time of the July 2021 IPO ). Elevance entered a commercial agreement with SERA to purchase a minimum number of tests over multiple years (details were redacted in the agreement filed with the SEC). Elevance and SERA also partnered to initiate a 6,500 patient post-marketing study throughout the Elevance network of hospitals. The PRIME Study is currently enrolling patients in 14 sites around the country. The Company announced that it has enrolled over 2,800 patients, and expects to provide an interim data read out before the end of this year - a few months delay from our previous expectations.

Elevance and SERA worked with HealthCore, the Elevance analytics subsidiary, to predict the economic effects of adjusting the monitoring and proactive interventions based on Sera's PreTRM screening test by analyzing more than 40,000 commercially insured pregnancies. The model published in the journal ClinicoEconomics and Outcomes Research predicts a reduction in the number of NICU days by 20%, and a gross cost savings was calculated to be $1,608 per pregnant patient, not including an assumed price of $745 for running the test. ( Source: SERA Corporate Presentation , CEOR publication)

On February 15, 2023, the Company issued press release announcing positive top line data from the AVERT trial . There were over 2,000 patients enrolled in the study, and both primary end points were met and were statistically significant (Neonatal Mortality Index & Neonatal NICU length of stay). More details will come when the investigator, Dr. Matthew Hoffman from Christina Care Health Services in Delaware, publishes the data. There are caveats in the data. 1) This study was from a single health system, similar to the PREVENT-PTM trial. 2) The full data has not been published so it is hard to draw any hard conclusions. 3) Given that this was an investigator initiated trial, it is likely that this group is more proactive than most on the maternal care. For PreTRM to be effective two things need to happen. First, the assay needs to be able to flag high-risk patients. Second, the doctor and the patient need to both take steps to mitigate the factors of risk. Given the published articles from Dr. Hoffman ( one example on low dose aspirin ), it is clear that their group excels the second part of the equation.

To date, the Company has clinical evidence that PreTRM could be an effective assay to reduce the risk of pre-term birth. The PRIME trial will be the key to building market adoption and to understanding the economic benefit.

Stock Price and Lessons from Earnings Call

The Company IPO'd in July 2021 at stock price of $16. Just prior to the IPO, the Company did a $100 million private placement. The Company currently has a small sales force working to sell the PreTRM test focusing on health systems including self-insured employers, integrated delivery networks (like Kaiser Permanente), and managed Medicaid groups. In 2022 revenue from tests was only $268,000, which was below the Company's guidance $500,000 of revenue for the full year 2022 (provided early in 2022).

The revenues were below the original guidance. As part of the contract between Elevance and the Company, Elevance was required to purchase a minimum purchase that increased over the duration of the contract. These purchase minimums appear in the financials as deferred revenue, which increased $2.8 million in 2022. This suggests that Elevance is not sending as many tests to the Company as was estimated in the original contract. The Company has not communicated the cost charged per test in the contract, but a $300 cost would suggest that Elevance has a credit for over 9,000 tests. This gap causes questions that have not been addressed by management. Especially since, assuming $300 per test, the 2022 revenue of $268,000 suggests that the Company sold less than 1,000 tests in 2022. There is 9X that number of tests in credit waiting to be performed.

{kind=link}

As of December 31, 2022, the Company had approximately $104 million in cash and cash equivalents, and the Company had approximately 31 million common shares outstanding. There are another 11 million warrant and option shares outstanding. The 8 million stock options issued to employees have a weighted average exercise price of $3.62.

The company burned around $9 million in cash in operating activities in Q4 2022. Assuming a similar loss in Q1 2023, the cash balance at the end of Q1 2023 is likely around $95 million - which is about $3.07 in cash per common share.

On the conference call, management communicated an expected timing of the interim look at the PRIME trial data as before the end of 2023. This is later than my original expectations, which essentially delays insight on the commercial success risk to late Q4 2023. The positive top line data from the AVERT study announced on Feb 15th, 2023 increases the probability of getting positive data from the PRIME study.

On the conference call, management provided updates on progress to two key value-creating efforts. First, they have completed the validation of the process to ship samples at ambient temperature, versus on dry ice. This makes it easier for customers and reduced the costs associated with logistics. Management was coy about the specific efforts to reduce their COGS in our discussions in early 2022. There is likely additional work to be done to achieve a sub $100 COGS, which will come in time with additional scale.

Second, the Company completed the validation of their preeclampsia prediction assay. This additional assay should be able to be accomplished from the same sample sent for the pre-term birth assay, potentially increasing the price/value of each customer sample to the Company. The Company included a pipeline chart in their 10-K. This pipeline could add value in the long term, but adds to the expenses in the short term.

{kind=link}

Management Team

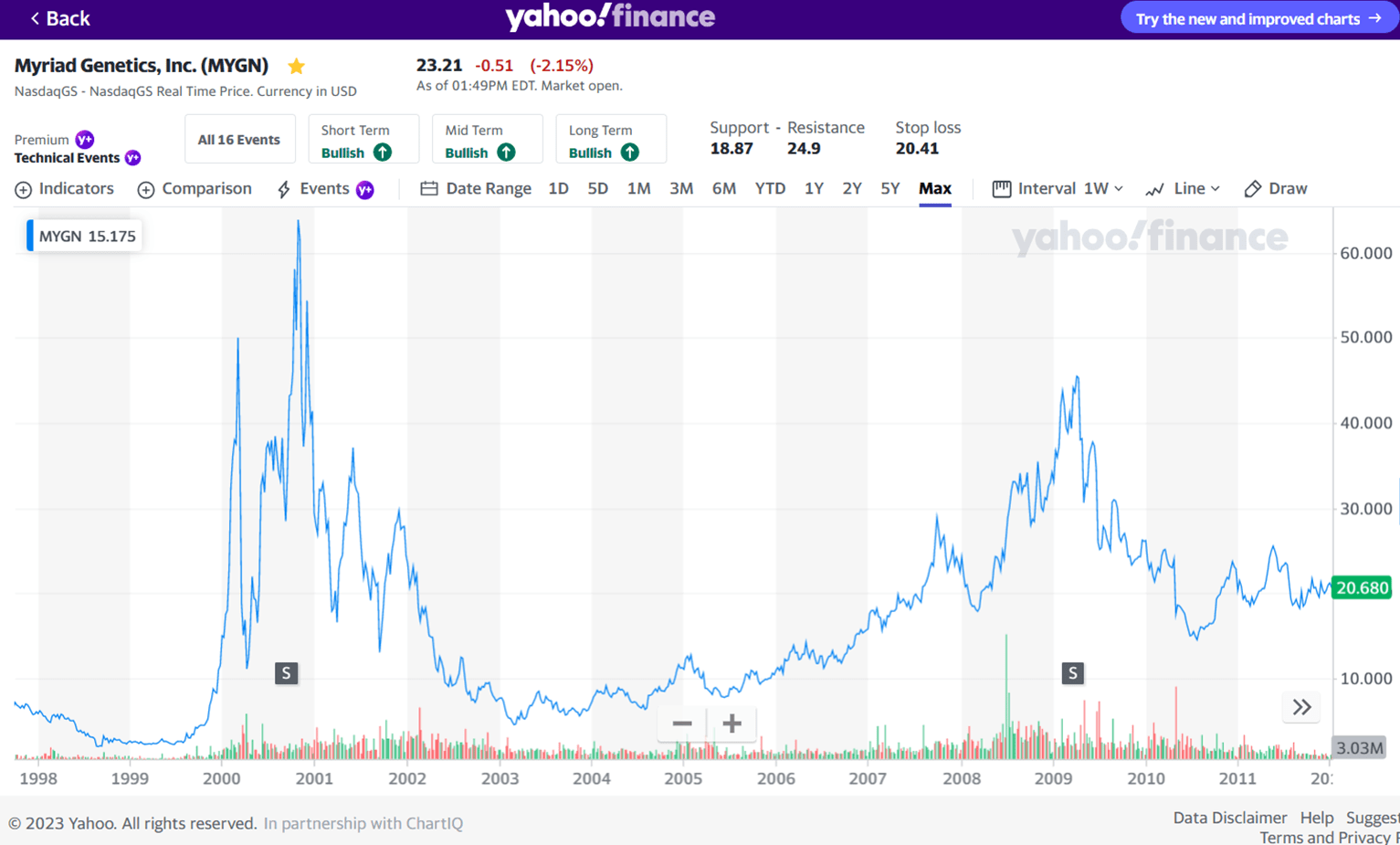

The CEO (Greg Critchfield), CFO (Jay Moyes), CSO (Jay Boniface) and General Counsel (Benjamin Jackson) were all at Myriad Genetics ( MYGN ), which launched one of the most successful CLIA laboratory diagnostics in history targeting the BRCA gene in women as a risk factor for breast cancer. Greg Critchfield led Myriad Genetics from July 1998 through March 2010. During that time, they completed the development of their breast cancer test, launched their test through the CLIA lab pathway, then developed an on-site kit that required FDA 510(k) clearance. Stockholders were rewarded with as much as 17X, depending on their ability to perfectly time their sale.

{kind=link}

The CEO joined SERA as a Director in Aug 2010 after leaving MYGN and took over as CEO in Nov 2011, and the CFO joined SERA in March 2020, essentially coming out of retirement.

My discussions with management in early 2022 lead me to believe that they were cognizant and cautious about spending. The reduction of sales expenses in Q4 2022 was in line with that spending caution.

The Opportunity - A Path to Becoming a New Standard of Care

There are approximately 3.6 million births in the US per year . Of those, approximately 10% were born preterm. According to the March of Dimes , the costs of preterm birth in the US was over $25 billion in 2016. The highest propensity was in African Americans at 14.2%, and the lowest propensity was in the Asian/Pacific Islander population at 8.8%.

The PreTRM test is designed and marketed for women carrying a single baby, who are otherwise not deemed to be high risk. Having a previous preterm birth, genetic red flags, twins, or triplets are factors that would cause a physician to increase the monitoring and/or proactive interventions to help keep the baby in the womb as long as possible. If a physician is provided with the assessment that a woman potentially has a high risk pregnancy, there are multiple interventions that could be done to attempt to prevent a preterm birth:

- Increase surveillance

- Additional cervical length measurements

- Progesterone injections

- Low-dose aspirin

- Antenatal steroid therapy

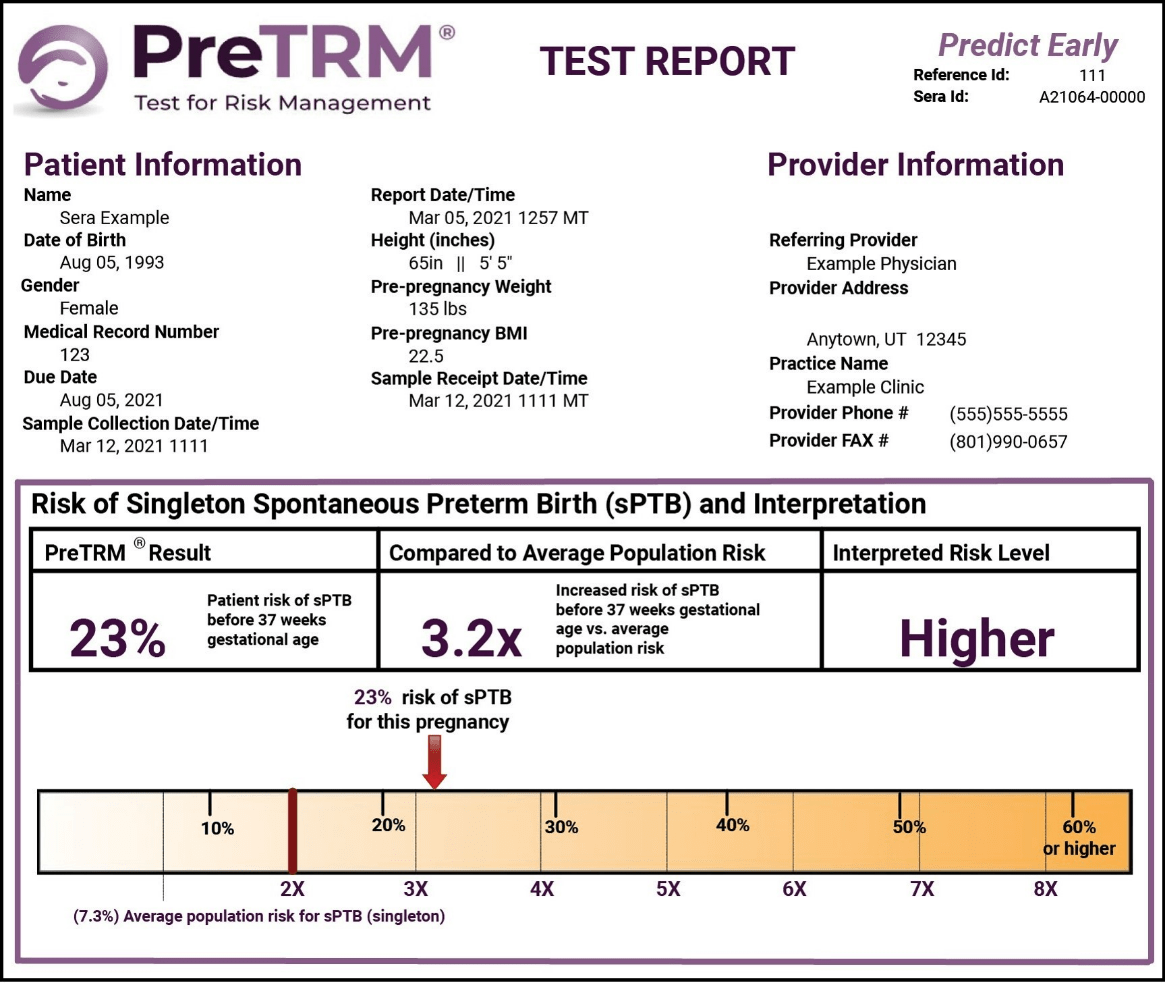

Below is a sample preterm birth risk assessment report that would be delivered to the physician.

{kind=link}

The PREVENT-PTM study showed a 70% reduction in the total NICU days for those patients who were screened, versus those that were not screened. In a discussion with management, they indicated that in the study, the notice of increased risk did not always translate into a physician using of one or more of the possible interventions. There was noise in the study, and the Company does not own the patient data so cannot do its own patient by patient analysis to understand the noise. Anecdotally, some patients who tested positive for the high risk screen rejected additional interventions, and added to the NICU days of the screened patients. Given the small size of the study, the focused geography of the enrolled patients, and the anecdotal noise, it is not surprising that the Company, and Elevance, are attempting to reproduce the study with a much larger sample size. If the PRIME study is able to reproduce the data with high statistical significance, then it is probable that the PreTRM test becomes the standard of care. Additionally, the study should be able to provide further pharmacoeconomic data to determine the full value of providing the screening test.

The Company estimates that there are about 3 million potential patients that would qualify for PreTRM testing, which is about 83% of US births. If PreTRM becomes the standard of care, and the Company is then able to charge $500 per test, then the total addressable market in the US is $1.5 billion.

Valuation Scenarios

In my original article, I included three models relating to the outcome of the PRIME study: "Win", "Grey" & "Lose", with target stock prices of $20, $6 or $2.35, respectively. After learning more about the Company, including a site visit, and digesting the new data from the 10-K, there are a few adjustments that I made to the models.

- Because of the reduced revenues in 2022 versus my expectations, and the statement by management that 2023 revenue would be less than $1 million, I have adjusted the % penetration in all models, and slowed the growth rate in the out-years.

- The "Grey" PRIME data scenario becomes a negative NPV model, as my estimated pace of adoption does not outpace the Company's expenses. I therefore will not include a "Grey" scenario, since that now is worse than the "Lose" scenario. It is my hope that Management and the Board would take the same view, and decide to liquidate the Company in the event that the data is not statistically compelling. Otherwise, it becomes a zombie company.

- I have pushed out the PRIME data reveal to the end of Q4 2023, which reduces the amount of cash in the Company at the moment of truth.

"Win" Scenario

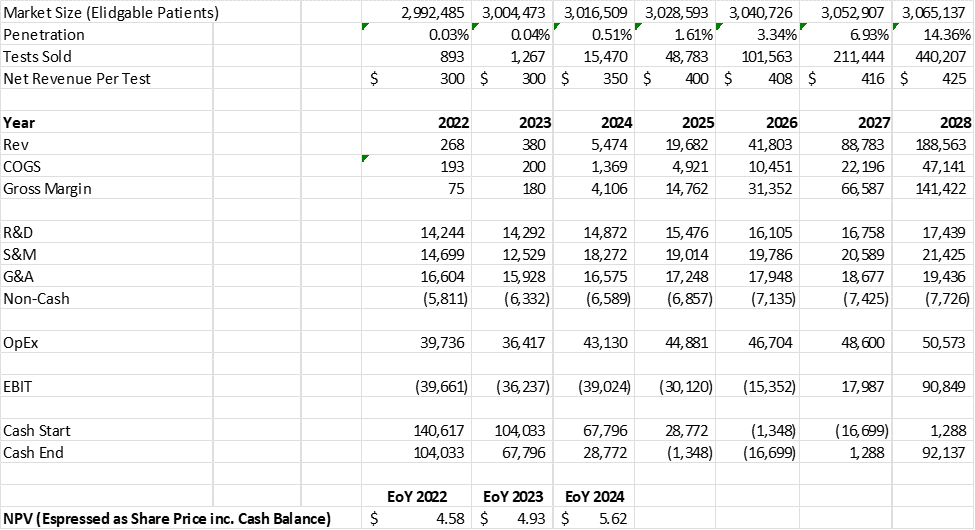

Given that Elevance has invested in the Company and helped craft the PRIME study, one can assume that the success or failure of the PRIME study would determine the level of adoption of the PreTRM test by Elevance's insured network (~400,000 total births per year). That adoption level will then determine the success or failure of the SERA. If the PRIME study validates the cost savings from providing the assessment of preterm birth risk, then Elevance (as well as any other insurance company) would do the math and adopt the screening test as a standard of care. In that "Win" scenario, I would assume the following for the model:

- a 25% ultimate penetration, with 20% quarterly growth starting in 2025, with a ramp to 1% penetration by the end of 2024 to account for the early adopters that are currently engaged with the company

- a price point of $350 after the interim data in 2024, and then $400 once the data is published and validates the economics in 2025

- A ~50% increase in sales and marketing expenses upon positive interim PRIME data starting in Q1 2023

- 50% COGS until 2024, 25% COGS as scale increased and the ambient temperature sample collection is fully adopted.

- Only modeling Pre-Term test in the US market - the Preeclampsia test and ex-US expansion would provide upside to the Company

These "Win" scenario assumptions generate a proforma NPV of $146 million, or $5.62 per common share at the end of 2024. Given the slower penetration rate assumptions versus my previous model, the model now suggests that the Company will need to raise at least $20 million in early 2025 to fully fund their commercial launch to profitability.

{kind=link}

"Lose" Scenario

If the PRIME study is a failure, then the Company is likely dead, or perhaps a zombie. The responsible thing to do would be to wind down operations and preserve as much money as possible to create value for shareholders by either becoming a reverse merger candidate or by giving the money back to investors (wouldn't that be refreshingly crazy!). In the "Lose" scenario, I would assume the following for the model:

- No business past Q4 2023

- The Company winds down operations in Q1 2023 and spends less than $5M.

- The Company becomes a reverse merger candidate and trades for a premium of unspent cash.

These "Lose" scenario assumptions generate a negative NPV at the end of 2023, but the company would still have approximately $68 million, or $2.19 in cash per common share, at the end of 2023. I assume it would cost about $5M to close operations, or about $0.16 per common share, assuming 31 million common shares. The outstanding warrants and options would be substantially below basis therefore not included in the calculation.

Internal Analysis

Overall, if one assigns probabilities to the different scenarios, one could calculate a range of stock prices that would make sense to pay for the stock in 2023 prior to the PRIME data, depending on what probability one would assign to PRIME providing statistically significant data to support a "Win". At the current market price, based on my models, the market is assigning a high probability of success to the data in the PRIME study.

Internal Analysis

Financing Risk

The Company raised a significant amount of cash before going public. There is a very low risk of the Company raising money and would likely not consider any additional funding until after they release their interim data analysis in late-2023 and have some stock price lift. In my "Win" scenario, the Company would need to raise money in 2025 to support full commercialization. With a "Win", the Company will have plenty of options for additional funding.

Analyst Coverage

Wall street analysts have price targets around $5 for the Company. In an Oppenheimer update following the AVERT press release, the analyst Francois Brisebois assigned a price target of $5, up from $4.50, but down from $17 in early 2022.

Interestingly, in the early 2022 note, Mr. Brisebois estimated $0.5M in revenue for 2022, and $20M for 2023. In a February note, Mr. Brisebois estimated $0.3M in revenue for 2022 and $2.1M for 2023.

On the earnings call, after management issued guidance for less than $1M for 2023, Patrick Donnelly from Citibank expressed his concern about the low guidance and asked for the rationale behind not being able to grow revenues in 2023. Management replied with a non-answer.

No Recent Insider Buying Activity

No member of management or the board have purchased shares in the last 12 months. While the stock was trading below cash in 2022, the Chief Scientific Officer was selling a few thousand shares a week - terrible for investors to see. At some point, it would be great to see the management team and the board all buy stock. It is my guess that the market would respond well.

Potential Risks and Potential Surprises

1) PRIME: While the data generated to date looks promising, the small numbers of preterm birth events in the PREVENT-PTM study make the study directional. The additional support from the AVERT trial is helpful, but the press release did not include details and it was being run by leaders in pre-term birth research, so it is hard to understand how that would translate into a broad, multi-site study population. The Company is performing a larger study and recruiting patients from all over the country. The PRIME study serves as the pivotal study. Its outcome will determine the Company's success. A positive outcome relies on two factors. 1) The ability of SERA's assay to provide an accurate assessment of risk. 2) With a positive high-risk assessment, the patient and physician need to agree and execute on an intervention plan to try to mitigate the risks, AND the interventions need to work. If #1 and #2, then this could be the standard of care (the Win scenario). If not #1, regardless of #2, there will not be a statistically significant different between screened and non-screened, and the test will be deemed useless (the Lose scenario).

2) CLIA Lab: The Company operates its laboratory under the Clinical Laboratory Improvement Amendment (CLIA). This allows the Company to sell its laboratory test without submitting the test to the FDA. This has the benefit of allowing the Company to sell its test after it has validated the test and the laboratory. This also limits the Company's operating only one laboratory. In time, to expand geographically outside of the US, the Company will need to create test kits and submit those test kits to a regulatory authority for approval.

2) COGS: As of early 2022, the Company had an assumed cost of goods around $150 per test. With scale and automation, management said that they could reduce that cost to $100 per test. They have taken the first step by validating the ambient temperature collection kit. With true scale, they likely could further reduce COGS and create additional shareholder value. The expenses required to achieve additional COGS reduction are unknown, but likely worth the investment in the "Win" scenario.

4) Pipeline: The Company is working on a number of different neonatal tests, including preeclampsia, gestational diabetes, fetal growth restriction, and postpartum depression. It is unclear as to if the market assigns value to their pipeline. If anything, it could be seen as an extra cost and distraction. If the research expense for the other pipeline products is low, it is a net positive in the long term to be building the pipeline.

5) Valuation: Since the start of the pandemic, classical NPV valuation methodologies have been disconnected from public company market caps. This is especially true in the small cap space. In June 2022, 20% of biotech companies were trading for less than the cash on their balance sheet. This disconnect may persist for a long time. Therefore, the models used to generate the stock price estimates in this report should be seen as directional.

Conclusion

SERA has lost 75% of its value since the IPO in 2021. I believe the Company has been caught in the general life science risk-off sell-off that started mid-2021 and accelerated in 2022. The AVERT trial positive data, although not detailed, provided a recent boost to the stock price.

SERA has the advantage of a strong balance sheet providing it multiple years of operational cash, and a significant inflection point within 12 months. The PRIME study is a repeat of a previously successful study with a larger patient enrollment target across a larger geographic area and should have an interim data readout in late-2023.

If the PRIME study is positive, then it is likely that PreTRM becomes the standard of care within the Elevance insurance network, and perhaps across the industry. In this "Win" scenario, an NPV model suggests a stock price of over $5 is possible. If the PRIME study is a complete failure, then the Company should have just over $2 per share in cash to give back to shareholders.

With the recent rise in stock price, the market has increased the probability of success assigned to the PRIME study. The earnings update suggests that the Company's ability to grow sales will be highly dependent upon published data and will likely take much longer than originally modeled. Prior to the interim PRIME data, I would accumulate below $2.50, but sell above $4.00. Playing the PRIME data event could be a profitable bet as well.

For further details see:

Sera Prognostics Update: Recent Supportive Data Increases Probability Of Commercial Success For Preterm Birth Risk Screening