SFL - SFL Corporation: Reasonable Q1 Results Cash Flow Likely To Improve

2023-05-16 11:14:23 ET

Summary

- SFL Corporation Ltd. results generally showed the stability that we have come to expect from this company.

- The stability comes from the fact that 93% of SFL's revenues are derived from multi-year contracts.

- The market for UDW rigs is improving, which should result in the company's cash flow increasing during the second half of the year.

- SFL Corporation continues to have a fairly high debt load, but the company historically has managed it reasonably well.

- The 11.18% dividend yield appears to be sustainable.

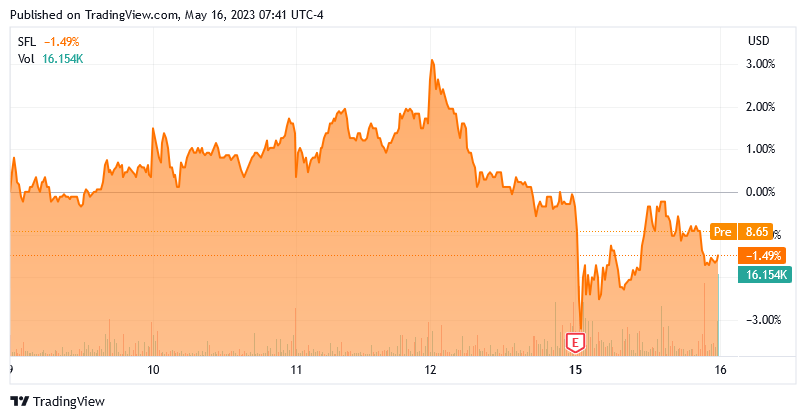

On Monday, May 15, 2023, ship leasing company SFL Corporation Ltd. ( SFL ) announced its first-quarter 2023 earnings results. At first glance, these results were mixed, as the company managed to beat analysts’ expectations for revenue but failed to hit analysts' earnings estimates. The market reaction to the earnings results was mixed, as SFL stock price fell sharply on the open but then rebounded as the day wore on:

{kind=link}

A deeper look into the company’s results reveals that SFL Corporation had a reasonably good quarter, as the company is experiencing a growing contract backlog and the market for ultra-deepwater drilling rigs is finally beginning to improve after years of stagnation. The company’s cash flow is holding up reasonably well, which is nice because this is what ultimately supports the 11.18% current dividend yield. That dividend yield is perhaps one of the best reasons for investing in the company, as it effectively guarantees a respectable return due to the overall stability of the company’s finances.

SFL Corporation Q1 Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from SFL Corporation’s first-quarter 2023 earnings results:

- SFL Corporation reported total revenue of $173.266 million in the first quarter of 2023. This represents a 12.41% decline over the $197.817 million that the company reported in the previous quarter.

- The company reported an operating income of $49.937 million in the most recent quarter. This compares rather unfavorably to the $74.380 million that the company reported in the preceding period.

- SFL Corporation received a four-month contract for the Hercules ultra-deepwater offshore drilling rig. The rig will generate total revenue of about $50 million over the course of this contract.

- The company reported an adjusted EBITDA of $102.619 million during the reporting period. This represents a 19.52% decline from the $127.508 million that the company had last quarter.

- SFL Corporation reported a net income of $6.332 million in the first quarter of 2023. This compares very unfavorably to the $48.454 million that the company reported in the fourth quarter of 2022.

It seems certain that the first thing that anyone reviewing these highlights will notice is that SFL Corporation’s financial performance generally declined compared to the previous quarter. This is somewhat misleading as the company’s results were negatively impacted by a few non-cash items during the quarter. In particular, SFL Corporation took a $7.2 million mark-to-market loss on some of the equities that it has in its portfolio and had a $7.4 million impairment charge against the value of two of its chemical tankers. It is important to note that this did not actually result in any money leaving the company as a result of these charges. These are akin to unrealized losses on investments, and it is possible that a strengthening market will reverse them at some point in the future.

With that said, it is admittedly unlikely that the impairment charge against the ships will be reversed. That does not change the fact that these items negatively impacted the company’s results but did not actually result in money leaving the company, and as I have pointed out numerous times in the past, cash flow matters much more than net income.

We do notice that SFL Corporation’s revenue declined quarter-over-quarter. However, the reported revenue figure is somewhat misleading. This is because the company received $11.6 million during the quarter as a charter hire that was not considered to be revenue according to U.S. GAAP rules, but it did still result in new money coming into the company. The company received $11.8 million in the same fashion during the fourth quarter of 2022 though, so this alone has no difference on the quarter-over-quarter decline that we see. One of the company’s ultra-deepwater rigs, Hercules , was undergoing a special periodic survey during the quarter and thus generated no revenue for SFL Corporation. That is almost certainly the biggest reason for the revenue decline that the company experienced in the most recent quarter. SFL Corporation’s seven dry bulk carriers that are working in the spot market also experienced a revenue decline as they only earned $4.6 million in the quarter compared to $9.0 million in the previous one. The company provided no reason for this, but this is not uncommon as the first quarter is almost always the weakest for dry bulk spot rates.

This year was especially bad, as Freightwaves points out . Fortunately, it is expected that this condition will improve as the year rolls on. The Hercules will continue to be a drag on the company’s performance going forward though as it will not complete the special periodic survey until June, so it will not generate any revenue until that time. This rig has two $50 million contracts after the maintenance work is complete though, so it should be able to provide a boost to SFL Corporation’s revenue in the second half of the year.

In the introduction to this article, as well as in SFL Corporation’s earnings press release, it was stated that the market for ultra-deepwater offshore drilling rigs is finally starting to improve after several years of stagnation and weakness. From the press release:

“The market for ultra-deepwater drilling rigs is firming up rapidly, and there are very few rigs similar to Hercules with both harsh-environment, fully winterized and ultra-deepwater capabilities. We are investing significantly in the rig currently, but cash flow from Q3 will be substantial, and market prospects from medio 2024 when the rig will be available for new employment look very promising.”

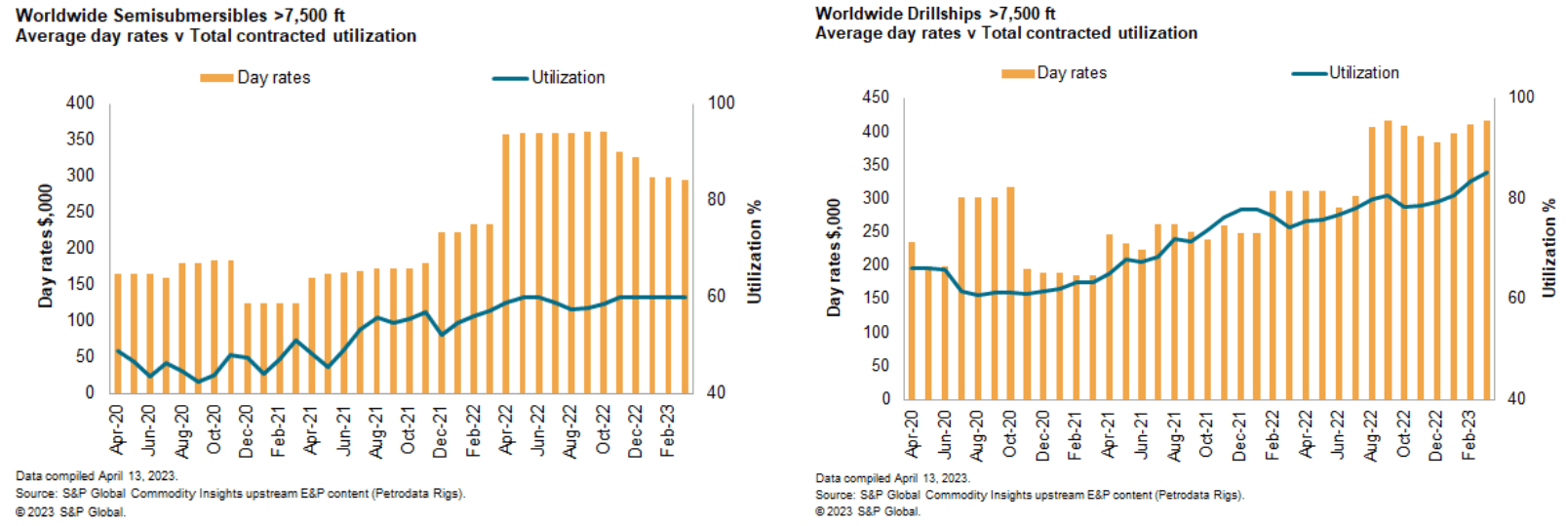

We can certainly see improving utilization for ultra-deepwater rigs across the industry, as the sustained high energy price environment that we have seen over the past few years has revitalized interest in offshore opportunities:

{kind=link}

As we can see, the utilization rate for the global ultra-deepwater drillship fleet is rapidly increasing. While the global utilization rate for the ultra-deepwater semisubmersible fleet is not improving as rapidly, it is still at the highest level that it has been in years. The hostility of the United States and Europe to Russia, as well as the rather unfriendly political climate towards American shale, is also working in favor of offshore drilling since it is limiting the options that upstream producers have to satisfy the world’s need for traditional sources of energy.

For its part, SFL Corporation owns two offshore drilling rigs, but only Hercules is capable of operating in ultra-deepwater environments. It is a semisubmersible, so it is not in the category of high utilization drillships but as the company points out, it is one of the few ultra-deepwater rigs that is capable of operating in harsh environments, such as what would be found in the North Sea. The fact that the market for these has been improving, albeit not as fast as we would like, is evident in the fact that this rig currently has two $50 million contracts that it will start to work on in the middle of the summer. This should provide the company with a nice revenue boost that should last until sometime around the middle of next year at the earliest. It would be nice if the company could secure another contract for the rig to start around that time, but it has not secured one as of yet.

Earlier in this article, I stated that SFL Corporation is quite stable financially. This is because the company’s business model revolves around long-term contracts. In short, SFL Corporation leases out the ships in its fleet to its customers over very long periods of time. As we can see here, the average length of these contracts varies by vessel type, but it is consistently several years:

SFL Corporation

During the first quarter of 2023, 93% of the company’s revenue came from these contracts, while only 7% was exposed to the much more volatile spot market. We can clearly see then that the overwhelming majority of the company’s revenue comes from long-term contracts. This is nice because it should ensure that the company’s revenue remains somewhat similar from quarter to quarter. That makes it much easier for the company’s management to budget for various expenses, as well as adding a great deal of support for the dividend. It is similar to the way a salaried person will have an easier time carrying a large mortgage than someone who is self-employed or works on commission. We will discuss the sustainability of the company’s dividend shortly, but the takeaway here is that SFL’s revenue and by extension cash flow generally prove to be relatively stable over time. We can see this reflected in its most recent results.

Financial Considerations

It is always important to investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the proceeds to repay the existing debt. This can cause a company’s interest expenses to increase following the rollover, depending on the conditions in the market. When we consider that the central banks of every nation in the G20 except for Japan and China have raised their interest rates over the past year, this is a very real concern today. In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, any event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. Although SFL Corporation has reasonably stable revenue and cash flow due to its contract-driven business model, there have been other companies that employed such a model and went bankrupt so we still should not ignore this risk.

One metric that we can use to judge SFL Corporation’s ability to carry its debt is the leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely pay its debt if it were to devote all of its pre-tax cash flow to that task. As of March 31, 2023, SFL Corporation had a net debt of $2.4127 billion. The company’s adjusted EBITDA in the first quarter was $102.619 million, which works out to $410.476 million annualized. That gives the company a leverage ratio of 5.88x, which seems very high. SFL Corporation is much like a midstream company in that it has very stable cash flows and a very capital-intensive business. These companies we do not like to see above 5.0x, but 4.0x is preferable.

Fortunately, SFL Corporation will probably see some improvement over the rest of this year, especially when Hercules resumes work which should lower this ratio. We will want to keep an eye on this over the next few months to see how much the company’s debt improves. With that said, SFL Corporation has always had a pretty high debt load and it has not really caused any problems yet, so the company seems to be able to manage it.

SFL Dividend Analysis

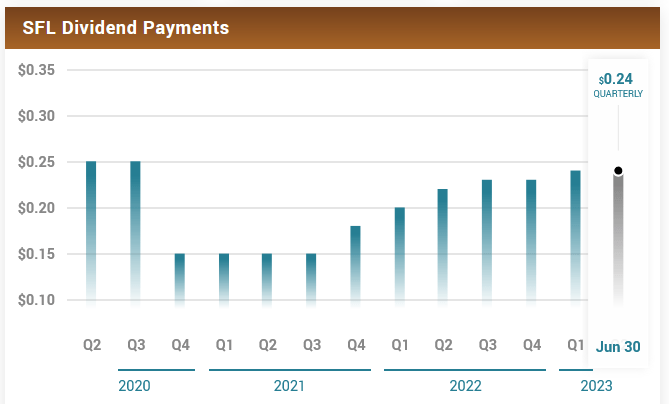

One reason why many investors are attracted to SFL Corporation is the attractive dividend that the company has historically paid. It continued to do so in the first quarter, as it announced a $0.24 per share payment, which gives the stock an 11.18% yield at the current price. Unfortunately, SFL Corporation has not been particularly consistent with its dividend over the years, as it cut it twice in 2020 in response to the troubles that accompanied the pandemic-driven lockdowns. The company has raised it since then, but it is still not back to the level that it had prior to the cuts:

{kind=link}

The company paid $0.35 per share prior to the dividend cuts, so as just mentioned the payment is currently less than the pre-pandemic level. This is something that could be concerning to those investors that want to use it as a steady source of income, particularly considering that the company enjoys fairly stable cash flows. However, it is important to keep in mind that the stock has been repriced for the new dividend, so anyone buying today will still receive a very attractive yield. The fact that the company has cut the dividend in the past has no impact on someone buying today, so the most important thing is how well SFL Corporation can maintain its current dividend.

The usual way that we judge a company’s ability to cover its dividend is by looking at its free cash flow. The free cash flow is the cash that was generated by a company’s ordinary operations that is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that can be used for things such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on March 31, 2023, SFL Corporation had a negative levered free cash flow of $121.1 million. This is obviously not enough to pay any dividends, but the company still paid out $116.6 million over the course of the year. This is something that is certain to be concerning to any investor.

However, SFL Corporation finances itself much like a utility or a midstream company due to its generally stable cash flows and long-term contract-based business model. This means that the company pays its dividend out of its operating cash flow, while things such as capital expenditures are covered with debt. That makes sense since the company’s largest expense is acquiring new ships, so it can finance those purchases and then use the cash flow from the ship to pay off the loan. It does not need to buy the ship with cash. This is similar to how a real estate company might take out a new mortgage every time it purchases a property.

During the trailing twelve-month period, SFL Corporation reported an operating cash flow of $354.7 million, which was more than sufficient to cover the $116.6 million that it paid out in dividends and still leave quite a lot of cash left over for other purposes. Overall, the company can probably sustain its current dividend.

Conclusion

In conclusion, SFL Corporation Ltd.'s first-quarter results were reasonable, but nothing amazing. The big takeaway here is the improving market for ultra-deepwater offshore drilling rigs that should result in a cash flow boost for the company during the second half of this year. Other than that, SFL Corporation Ltd. looks like a reasonable way to obtain a very attractive dividend yield due to its relative financial stability.

For further details see:

SFL Corporation: Reasonable Q1 Results, Cash Flow Likely To Improve