SFL - SFL: Start 2024 With 30% Returns For This Undervalued Shipper

2024-01-02 05:57:08 ET

Summary

- SFL Corporation has multiple tailwinds in both the car-carrying and offshore drilling segments.

- These tailwinds will drive over 30% growth in EBITDA, which should flow back to investors through increased dividends.

- I conservatively project a quarterly dividend raise from $0.25/share to $0.33/share over the course of 2024.

- The implied share appreciation from the dividend raise is approximately 30% with total returns being even higher.

Thesis

SFL Corp (SFL) is a diversified shipping company that owns 73 vessels that serve various industries. From cargo containers, to cars, and deep-water drilling, SFL does it all. With a backbone structured around long-term contracts, SFL has been able to pay a dividend for nearly 20 years.

That is all about to change, and for the better. SFL is entering a period of revenue growth that will meaningfully expand its discretionary cash flow. Two main drivers will spur over 25% earnings growth.

1. The receipt of four new car carrying vessels that are booked to premium long-term contracts will boost EBITDA by over 20%.

2. The Hercules drilling vessel will generate enough additional free cash flow to cover a quarter of the dividend by itself. This vessel is leased under short term contracts to allow exposure to rapid expansion of deepwater drilling rates. 2025 may be even better than 2024.

These factors will translate into 33% dividend growth up to $0.33/share while also allowing for debt reductions to improve the balance sheet.

Long-Term Contracts

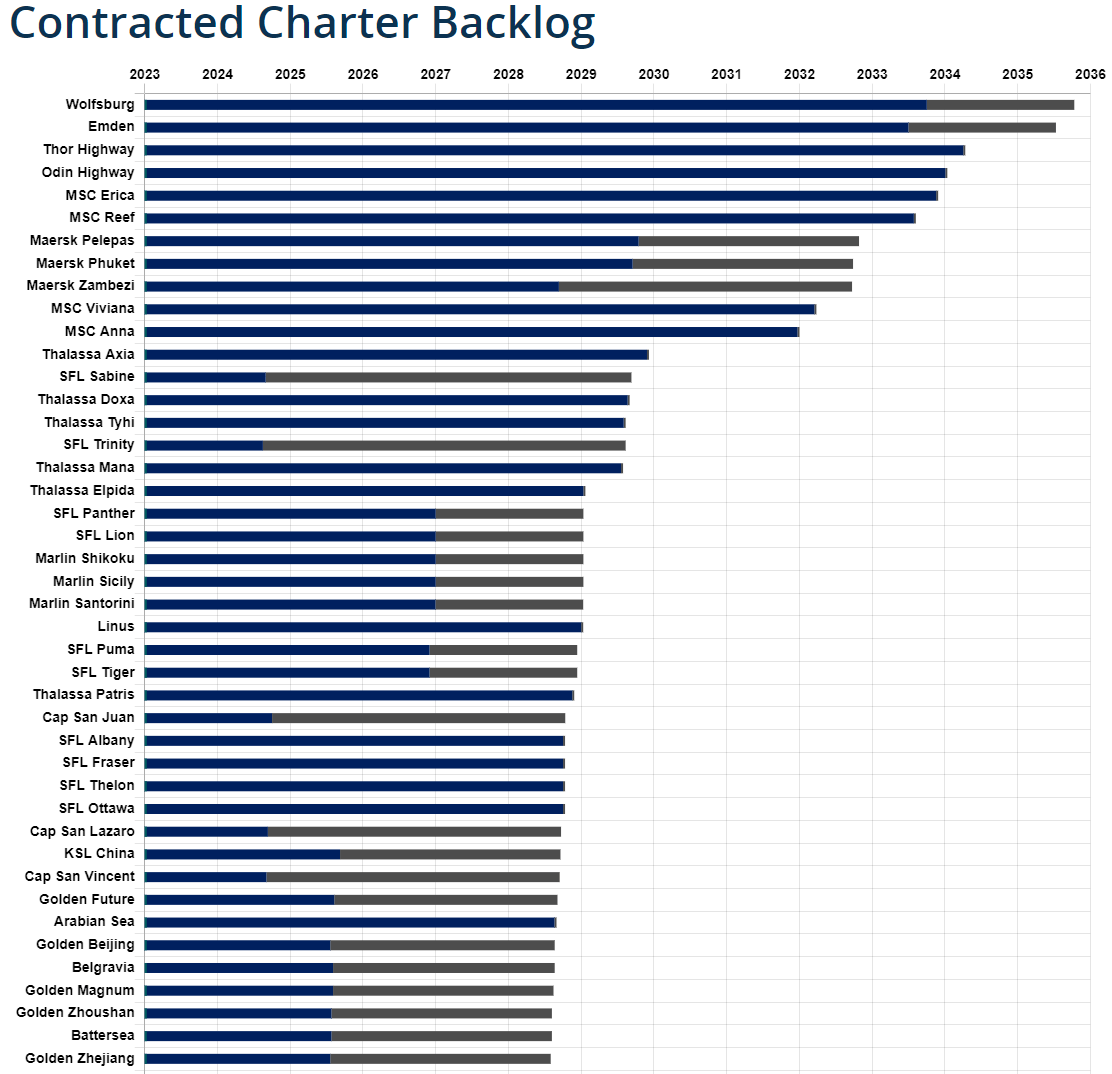

SFL's operating goal is to structure its business around long-term contracts with blue chip customers. The current backlog stands at $3.4 billion with an average remaining charter term of 5.9 years. This model, spread over a fleet of 73 vessels in five operating segments, provides diversity to limit the risk associated with one industry, vessel, or customer.

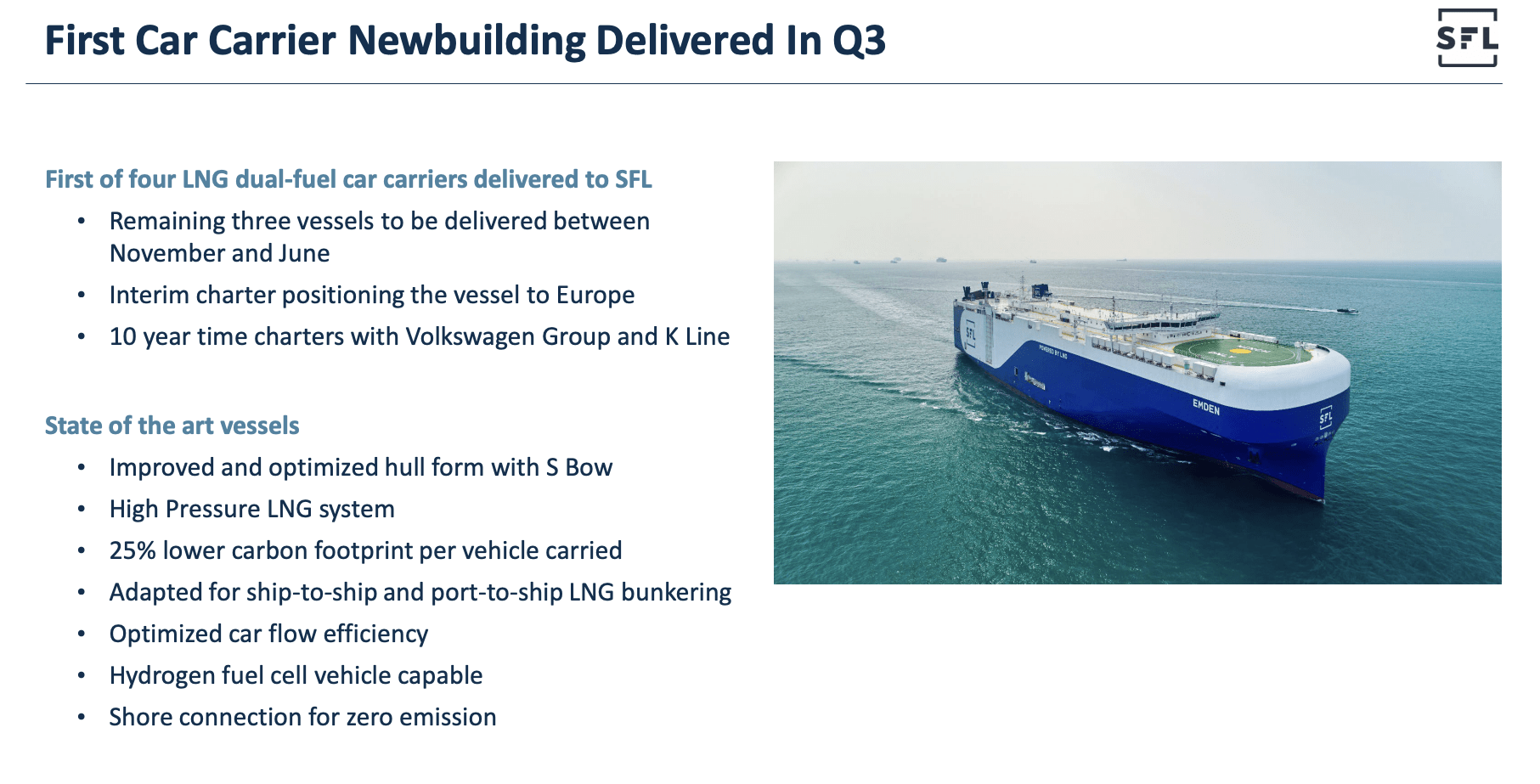

SFL can convert this operational stability into stability for its shareholders. While the dividend has not always grown, SFL has paid a dividend since 2004 and is currently on pace for its second year of dividend growth following a reduction in 2020-2021. This trend appears to have plenty of momentum behind it with four new car carrying vessels being delivered between Q4 and Q1 2024. All of these vessels are leased to 10-year contracts with options for further extension.

{kind=link}

Rewarding Shareholders

In the first three quarters of 2023 , SFL has generated $262.6 million in cash from operations on revenues of $542.7 million. These strong cash flows have been used to help fund a strong dividend that supports an 8.8% yield as well as commencing a $100 million share repurchase program in Q2 of this year. At the current rate of share retirement, the combined quarterly return equates to $0.25/share in cash and $0.04/share in equity or a 9.9% return in total.

By general market standards this is already a healthy return that is backed by years of contracted revenue stability. However, as we dig deeper, this analysis will show that this return is just the tip of the iceberg for SFL.

Investors have an opportunity to participate in a high yielding stock that has high growth potential hiding in plain sight.

Carrying Cars for Profit

In addition to a high yield, SFL also has sufficient positive cash flow to also grow the business and improve the balance sheet. This effort has been aided by selling older vessels to recycle capital and ensure the fleet remains young and efficient. Thus far in 2023, SFL has invested over $200 million in new vessels which most notably includes four new car carrying vessels, two of which have entered service this year. By mid-2024, the remaining two new vessels should be complete and contributing to both the top and bottom lines for the company.

These four new vessels are expected to contribute approximately $23.5 million in EBITDA per vessel per year, or $94 million combined. At a price tag of approximately $77.5 million per vessel, this is an excellent use of capital. These vessels have a payback period of just over 3 years on a pre-tax basis.

{kind=link}

Having these vessels secured at premium rates for 10-years to Volkswagen, the second largest car manufacturer globally, is a big deal to SFL. To give some perspective on the potential impact, SFL has made $325 million in EBITDA thus far this year and $433 million if annualized. The addition of these vessels brings the projected annualized total to $527 million. This equates to roughly 22% EBITDA growth from these vessels alone.

Growth in Oil is Growth for SFL

If the growth in the car carrier segment was not compelling enough, SFL's offshore program is also in an up-cycle. Over the last decade, profitability for offshore E&P companies has been challenged because of depressed oil prices starting from the onset of the US shale boom and continuing through the disruption caused by the COVID-19 pandemic. Withering demand for offshore drilling rigs has caused several big players in this space to declare bankruptcy (Seadrill and Nobel). Such financial distress has all but stopped the construction of drill ships over the last several years.

SFL only has two vessels in this category, the Linus and Hercules vessels. The Linus vessel is a harsh environment vessel that is contracted out to ConocoPhillips until 2028. This vessel has contracted market adjustments every 6 months to produce stable and rising cash flows.

Conversely, the Hercules vessel is an ultra-deep water semi-submersible vessel that has been employed on relatively shorter-term contacts. SFL has been hesitant to allow Hercules to be committed to a long-term contract to prevent from missing out on the full upside of the current cycle.

Rates for these types of vessels have been screaming upwards over the last year now that projects off the coasts of Guyana, Suriname, and Namibia are in various stages of production and exploration. These projects are more than sufficient to keep the existing fleet at high levels of utilization.

Wood Mackenzie projects that drilling vessel supply will continue to remain extremely tight through 2027 with the current project slate. This is a huge tail wind for SFL despite having only two vessels. The Hercules vessel most recently secured a contract at a rate of $500k/day. This is over 10 time the rate of a tanker vessel and over 5 times the rate of the brand-new car carrier vessels. Therefore, changes in this market can have a large impact for SFL.

Wood Mackenzie

The table below summarized the current contract landscape for the Hercules vessel.

| Location |

| Duration |

| Rate |

| Canada (Exxon) |

| 135 days - Start Q2 2023 |

| $50 million or $370k/d |

| Namibia (Galp Energia) |

| 115 days - Start Q4 2023 |

| $50 million or $435k/d |

| Canada (Equinor Canada) |

| 200 days - Start Q2 2024 |

| $100 million or $500k/d |

At the start of Equinor contract, the Hercules will realize $130k/d in additional revenue compared to the most recent quarter. Using an average day rate of $461.5k/d, this vessel will be able to generate an additional $33.5 million of revenue over the course of 2024. More importantly, since this does not require any additional operating expenses, this additional revenue flows straight to the bottom line.

2025 may be even more prosperous for the offshore segment. Multiple CEOs from the big offshore players have commented during quarterly conference calls on where they feel the offshore drilling market is headed.

Robert Eifler provides Nobel's projection for what rates would be required to justify building a modern drilling vessel.

"Hypothetical new build with comparable capabilities as the current Tier 1 seventh generation drillship would likely cost at least $850 million to build and require at least 3 years, if not longer, for delivery. In order to underwrite that asset, a rational buyer would require a contract of 10 years at $650,000 per day or greater or some variation of rate and term along those lines."

"So, we're approaching the $500,000 day rate threshold, a bit more slowly than we had previously expected. But if you scratch a little deeper, what you find is that the UDW market is still in fact tightening, due to the steady absorption of the sideline capacity.

Additionally, major projects in Namibia and Suriname are poised to drive incremental rigs requirements and established UDW basins such as Angola and Nigeria continued to trend higher. The methodical absorption of sideline capacity has had a bifurcating effect on day rates over the short-term."

Matt Lyne, COO at Valaris also shared his views on the offshore drilling market.

So, I mean, we feel really good about where the market sits today and the longevity of the cycle. So, I guess, if we look at a couple of the supply metrics to kind of lead us down that path, which will directly relate to continued improvement in the day rate, lead times for tendering for contracts are increasing. And we're also seeing, as you were pointing out, customers increasing duration by connecting their programs to make it more attractive.

And why would they be doing that would be, if they see potential or they see supply decreasing, which incentivizes them to pick up rigs for longer to ensure they have the assets they need to drill.

Utilization is increasing, which is obviously resulting in a reduction in supply. And so looking at these main factors from a supply side metrics, it paints a positive picture on the direction of the market.

As one could imagine, rising rates on these vessels also increases their net worth. I assume the current net worth of the Hercules vessel to be 70% of a newbuild given the tight supply of vessels and the long lead time to construct a new vessel. Using the $850 million price tag given by Nobel CEO Robert Eifler, this would give the Hercules vessel a value of $595 million. This creates two interesting investment perspectives.

1. With a market cap of approximately $1.5 billion, SFL represents a compelling discount to NAV play. The combined value of the four new builds and the Hercules is roughly $900 million. This values the remaining 68 vessels at just $600 million.

2. The opportunity to monetize the Hercules vessel would give SFL incredible financial leverage to expand the fleet or reduce its debt if it chose to do so. While this would obviously hurt overall revenue, there is a lot to be said for locking in the equivalent of multiple years of revenue in one stroke of the pen.

Seadrill Q2 2022 Investor Presentation

The Bottom Line

The combined effect of the new car carrier vessels and the increased rate for the drilling vessel Hercules results in an increase of $127 million in EBITDA or 29% growth. Assuming a tax rate of 25% leaves $95 million in excess cash flows annually as SFL exits 2024. With $136 million in CAPEX spending still remaining for the three remaining newbuild car carriers, I will assume interest expenses to rise an additional $10 million per year (7.5% interest rate), leaving $85 million remaining.

The expense of the dividend at its current value is approximately $121 million annually. Allocating half of the projected discretionary funds to the dividend would result in a 33% increase to $0.33/share while also leaving surplus cash for debt reduction. This will have the combo effect of driving share appreciation to match the dividend growth. If SFL were to continue to trade at a 9% yield, the corresponding share price would rise to $14.67/share, implying 30% upside to the current share price. I would expect even further price appreciation should a higher percentage of cash flow be allocated to the dividend.

Risks

The current debt load of SFL is not significant enough to call it a "problem" but is high enough to be considered an overall drag on investor returns. The current interest payment plus the projected increase in debt associated with financing newbuilds will take the annual interest expense to north of $170 million. This is over 20% of annual revenue, so getting this figure down would be beneficial in freeing up incremental free cash flow.

SFL has been able to make moderate amounts of progress this year by retiring over $100 million in net debt thus far in 2023. This may be a challenge in the near term with $136 million still required to complete the last two car carrying vessels. Moving forward, it would be wise for SFL to allocate a portion of the new cash flows to debt retirement.

Summary

Using the projections above, annualized EBITDA is slated to grow to over $550 million by the end of 2024 for over 25% growth. This growth is funded by four newbuild vessels entering service in addition to substantial charter rate growth by the Hercules semi-submersible drilling vessel. With little to no excess capacity in the under-water drilling market, I expect the trend in rate growth to continue into 2025 as well.

The combination of these drivers provides approximately $85 million in additional free cash flow to drive both dividend growth and debt reduction. Splitting this additional FCF evenly allows for dividend growth of 33% to $0.33/share or 11% at today's price of $11.72/share. I rate SFL as a strong buy with potential appreciation of approximately 30% coupled with a high yield. After collecting dividends, I anticipate total returns to exceed 30% over an 18-24 month holding period.

For further details see:

SFL: Start 2024 With 30% Returns For This Undervalued Shipper