SHEL - Shell Midstream Partners May See A Bumped Bid Within Weeks

- On February 22, 2022, Shell made a rather strange zero-premium offer for its MLP, Shell Midstream Partners.

- This offer undervalued the midstream assets substantially, especially at a time when the assets are potentially under-earning.

- Timing of comparable negotiations suggest Shell may return with a more viable offer perhaps by September if not sooner.

- An offer closer to fair value may see an attractive short-term return for shareholders. Even if not, Shell Midstream is a robust long-term investment perhaps worth north of $20/unit.

- Hence the possibility of a short-term offer bump from Shell creates a potential attractive catalyst, but this is a reasonable asset to hold for the long term.

Shell Midstream Partners LP (SHLX) is a Master Limited Partnership or MLP, with a K-1 filing, and is a collection of midstream energy assets that Shell (SHEL) IPO'd in October 2014 for $23 per unit.

On February 22, 2022 Shell offered to buy the entity back for $12.89 per unit , with a non-binding preliminary offer. This was a zero-premium bid. It is likely, though not certain, that the offer will be increased based on peer transaction analysis.

Indeed, the units currently trade at an +11% premium to this preliminary offer signaling that the market sees a bump coming or greater value in the assets standalone. Furthermore, it is likely that some news will come soon working off the timeline for similar transactions.

Finally, as a backstop it is worth noting that Shell Midstream's assets are underearning today and relatively low capital intensity (primarily pipelines), so in the unlikely event no buy-in occurs, the Shell Midstream assets may still be attractively priced.

Parent Buy-Ins

Many Master Limited Partnerships are receiving parent buy-ins in this environment of high energy prices and low MLP valuations. It's fairly simple financial engineering for the oil majors.

For example, Shell Midstream Currently yields 8.3% when Shell's cost of debt is roughly 5.1%. Shell can therefore buy back the assets and capture a positive spread up to a Shell Midstream unit price of just over $23/unit (theoretically).

Similar Transactions

Looking at similar transactions can be instructive. Of course, this is a limited set of deals, so we shouldn't get carried away in the statistical analysis, but a generally pattern of a low-ball offer, followed by a bump to enable to deal to pass the conflicts committee is fairly commonplace.

| MLP |

| Buyer |

| Days To Offer Revision |

| Bump |

| Notes |

| BP Midstream Partners |

| BP |

| 137 days |

| +15% |

| Equity offer |

| Phillips 66 Partners |

| Phillips 66 |

| n/a |

| n/a |

| Equity offer, came with initial offer reviewed by conflicts committee |

| Noble Midstream Partners |

| Chevron |

| 87 days |

| +17% |

| Equity offer |

| Blueknight Energy Partners |

| Ergon |

| 196 days |

| +40% |

| Had sold oil assets, aggregates business |

| Hoegh LNG Partners |

| Höegh LNG Holdings Ltd |

| 170 days |

| +118% |

| LNG infrastructure |

| Shell Midstream |

| Shell? |

| 150 days and counting |

| ? |

| Non-binding proposal currently |

The above table makes clear that there should be some kind of event soon for Shell Midstream. Of course, that may not be a positive event for shareholders, we'll discuss that next, but this process is now slower than both BP's And Chevron's. Blueknight's process took another 46 days, which would take the process to just after Labor day. Hoegh LNG's took another 20 days, which would suggest an event mid-August. There's no reason Shell Midstream couldn't set a new record in delaying the process, but with an 8% dividend you get paid to wait (sort of, obviously inflation is at 9% today).

Note also that the deals then took a few months to finally close, but the prices traded close to the confirmed offer price. Also, various offers were equity in the parent, which ultimately generally increased the prices paid given the recent general run-up in energy prices. I've used the price of the equity at the time of the proposal in the table above.

Potential Premia

When assessing potential premia, it is worth noting that a bump for Shell Midstream is expected. The company trades at an almost 12% premium to the non-binding offer today. That would create downside for equity holders if Shell did not revise its offer, though equally it is not clear that the initial offer would pass the conflicts committee or potential legal challenge. A simple average of the experience of the four deals above with bump suggests a +48% increase (skewed upward by Hoegh LNG), with all increases greater than the current premium in the Shell Partners Price. It is also worth noting that the initial proposal was a zero-premium offer perhaps intended to set the bar as low as possible, and improve the optics of any bump.

Underlying Valuation

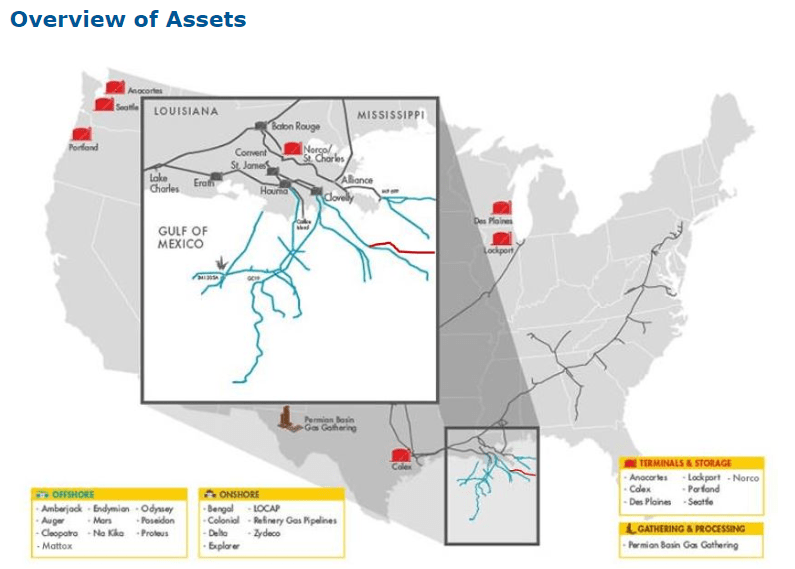

It is worth noting that Shell Midstream owns a range of midstream assets with a focus on onshore and offshore pipelines.

{kind=link}

Wolfe Capital wrote a well-founded letter to the conflicts committee explaining a reasonable valuation for the Shell Midstream assets at around $20/share. This notes that the business hasn't yet returned to pre-COVID profitability, is also temporarily impacted by Hurricane Ida (a September 2021 event) and that the businesses' stake in the Colonial Pipeline should be included in any offer.

What If Shell Walks Away?

One of the more interesting aspects of this setup, is I would be ok with Shell walking away at anything other than a material bump in the price offered. Normalized EBITDA is perhaps +20% above current LTM levels, and then the business is set to benefit from rate increases over time in addition before the most recent cut, which appears to be a response to non-recurring operational issues, the distribution was 53% above current levels.

A Scenario Approach

Taking a scenario approach yields $ 19.4/share for 34% upside.

| Scenario |

| Valuation |

| Probability |

| Notes |

| Reasonable bump |

| $20 |

| 80% |

| Broadly consistent with average MLP bumps and Wolfe valuation, with slight discount to 'walk away' valuation reflecting Shell Midstream isn't at full earnings power yet. |

| Attempt to force low offer |

| $13 |

| 10% |

| Seems highly unlikely to pass conflicts committee. May not be worth the reputational damage to Shell. |

| Shell walks away (medium-term valuation) |

| $21 |

| 10% |

| Assumes 25% distribution bump due to Ida/Colonial and a 7% yield (MLP ETF currently yields 8.1%, but Shell Midstream assets are lower capex and higher quality than average). Note that these assets IPO'd for $23/unit in 2014. |

Risks

Clearly, much in the hands of Shell Midstream's conflict committee. They is no guarantee that what I would consider to be a sensible offer bump occurs or that there is sufficient legal opposition to block what I would consider a potential lowball offer.

Some of the value of Shell Midstream is due to normalization of earnings power at multiple assets - particularly in terms of Hurricane Ida recovery. This is of course uncertain.

The energy environment over the coming years is highly uncertain and historically volatile. If the footprint of energy production and consumption changes material, Shell Midstream's assets could be stranded, reducing their earnings power.

Shell Midstream is a K-1 filer that may create tax issues for certain holders.

As seen in 2021, many of Shell's midstream assets are subject to operational risks such as hurricanes, spills and hacking attempts.

I argue above that Shell Midstream may benefit if Shell works away, though that may be true, on a multi-year view, the shares could easily trade down on sentiment in the months after Shell ceasing negotiations

Conclusion

Shell Midstream assets are attractive and potentially underearning today. A potential improved offer from Shell could come within weeks offering a potential catalyst. If it doesn't, it may still make sense to hold the units and get paid an 8% yield as the units potentially re-rate and distributions are potentially increased. The main risk is a potential attempt at acquiring the company at a lowball valuation, but it is unclear the conflicts committee would accept that. The most likely outcome seems some sort of bump in a few weeks, and you could do worse than that in the currently volatile markets.

For further details see:

Shell Midstream Partners May See A Bumped Bid Within Weeks