SCVL - Shoe Carnival: Financials Show A Strong Company And A Good Buy For The Long Term

2023-09-08 08:29:52 ET

Summary

- Shoe Carnival is trading at a low P/E ratio of 7x, making it an attractive investment opportunity.

- The company has strong financials, with no debt and a healthy working capital ratio.

- There are potential risks, such as dependence on two major vendors and the company's relative unknown status in the market.

Investment Thesis

Shoe Carnival ( SCVL ) is trading at a P/E ratio of about 7x currently, which prompted me to look into this shoe store in more detail. With outstanding EPS growth driven by cost-cutting measures that increased margins substantially, coupled with outstanding profitability and efficiency metrics, I believe the company is a buy at these prices and I can see it perform well if the company plays its cards right.

Financials

I will focus on full-year numbers below, so all graphs will be as of FY22 because I like to see the full picture of where the company's been heading and avoid q-o-q fluctuations as these do not portray an accurate trend due to some seasonality in the business.

As of Q2 '23, the company had around $47m in cash and equivalents against zero debt. This is always a great position to be in because it allows the company to be more flexible in how it wants to operate and not be weighed down by the burden of annual interest expense on debt. I would like to see the company be more aggressive at expansions or rewarding shareholders in some other way. Safe to say the company is at no risk of insolvency.

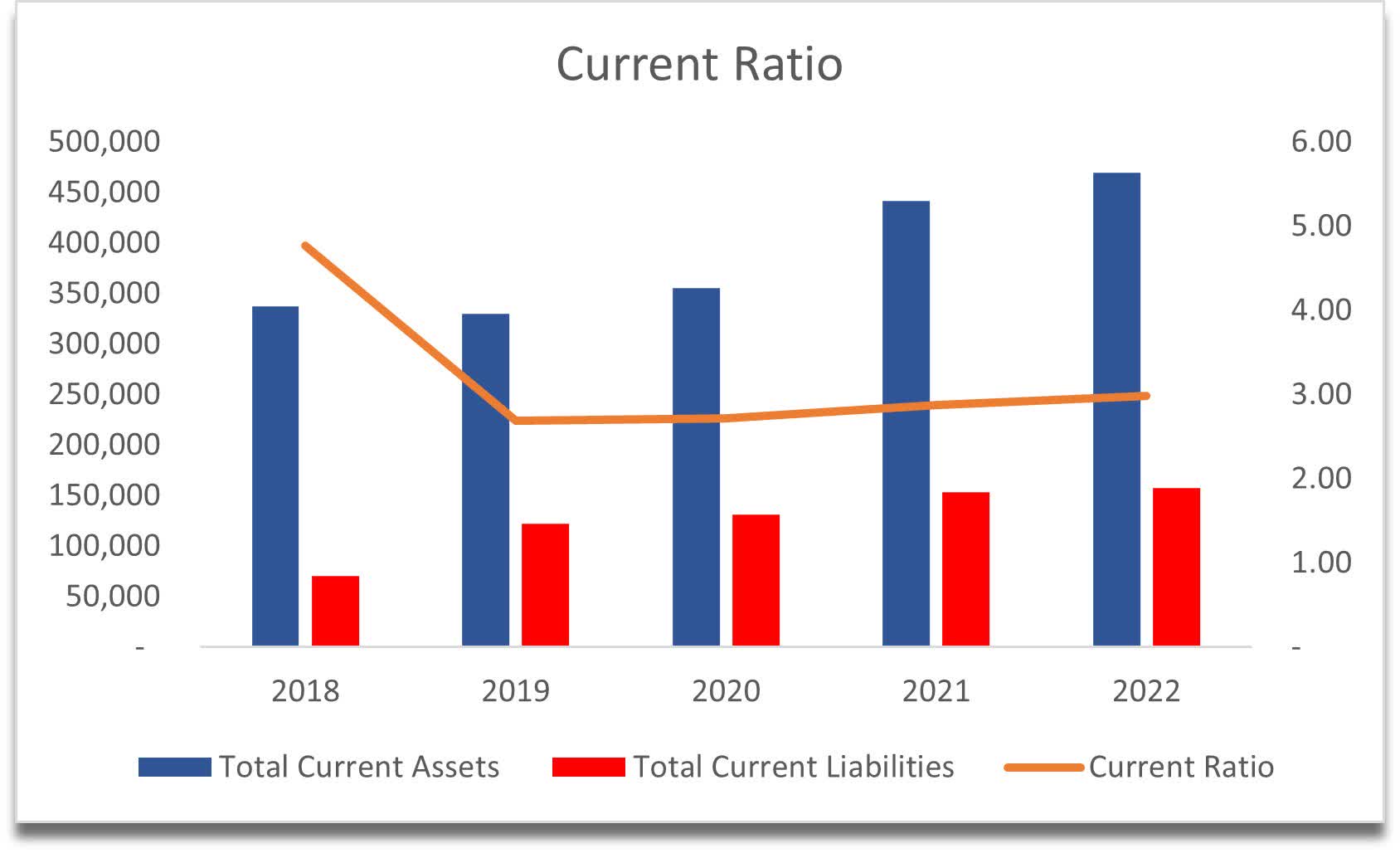

The company’s working capital ratio or the current ratio is around what I consider to be an efficient ratio, slightly on the upper end. I believe that a good balance between the ability to pay off short-term obligations and having enough cash for proactive expansion is in the range of 1.5-2.0. The ratio has been slightly above that range, however, it’s not by much. I would like to see it come down to around 2 in the future, which would mean that the company is more efficient with its resources and not hoarding the cash pile. We can see that it has come down from around 5 in FY18 which is good. It is safe to say that the company has no liquidity issues also.

{kind=link}

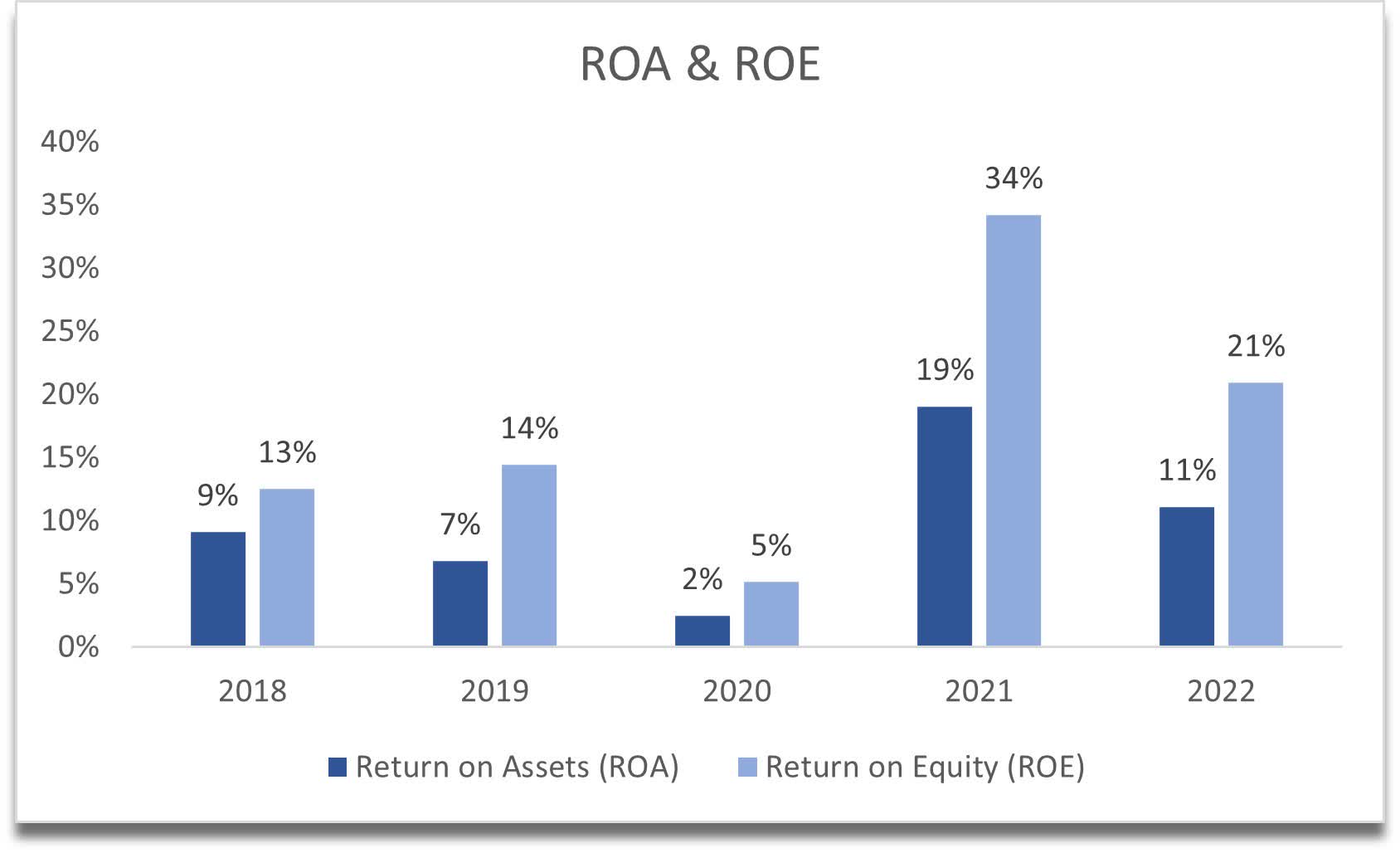

In terms of efficiency and profitability, SCVL’s ROA and ROE have recovered phenomenally since the pandemic panic of 2020. The numbers are even better than the pre-pandemic levels, which tells me that the management knows what it is doing with the company’s assets and shareholder capital. We can see that there was a slight downtick in FY22 numbers, however, FY22 has been a tough year for many companies and Shoe Carnival is no different. I wouldn’t be surprised if we see these tick up again in the near future.

{kind=link}

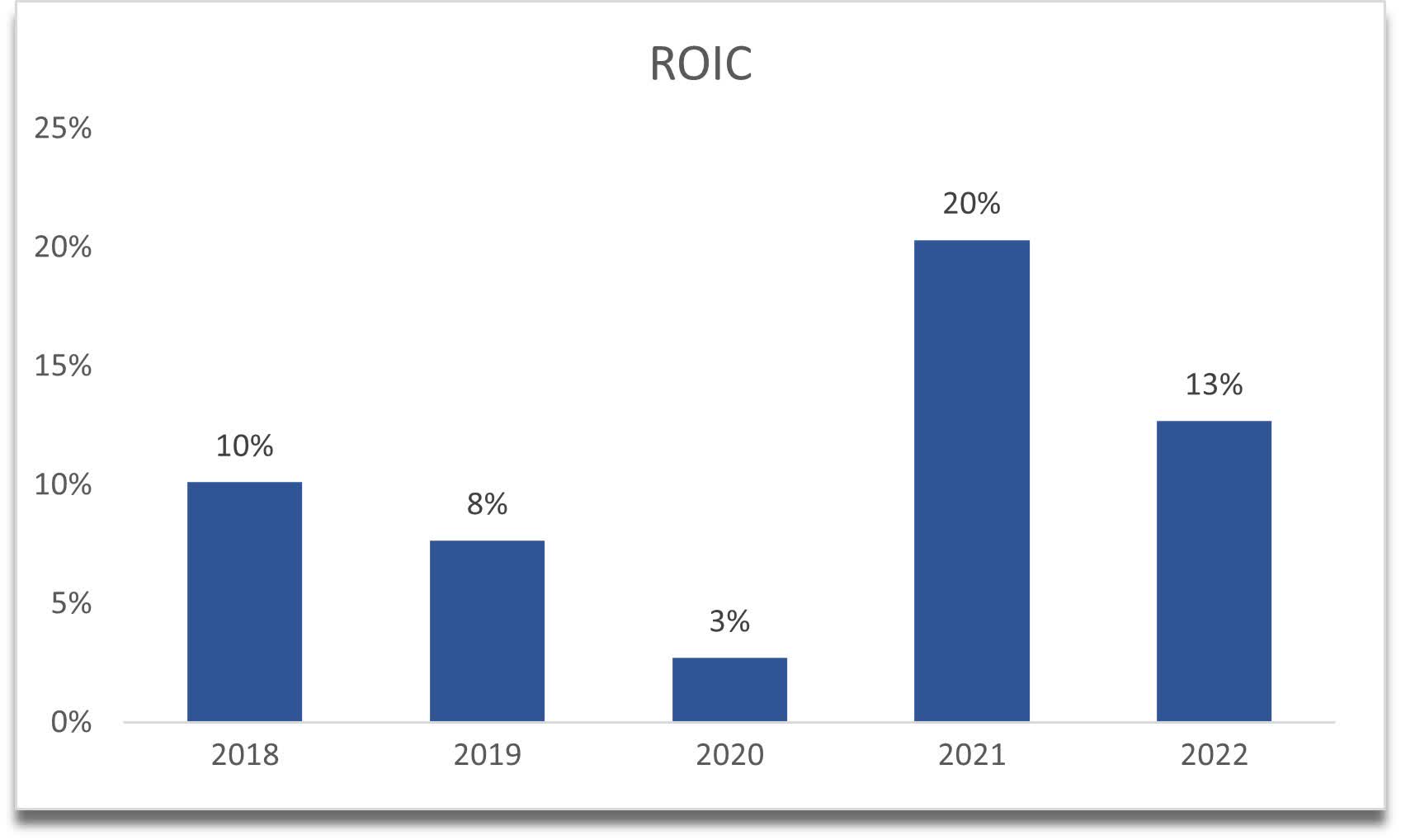

A similar story can be seen in return on invested capital or ROIC. We can see a fantastic turnaround since the pandemic, followed by a slight downtick in FY22. Nevertheless, the company's ROIC is still above my 10% minimum, and I think it's going to go back up in the future. This tells me that the company has a strong moat and a competitive advantage in the business.

{kind=link}

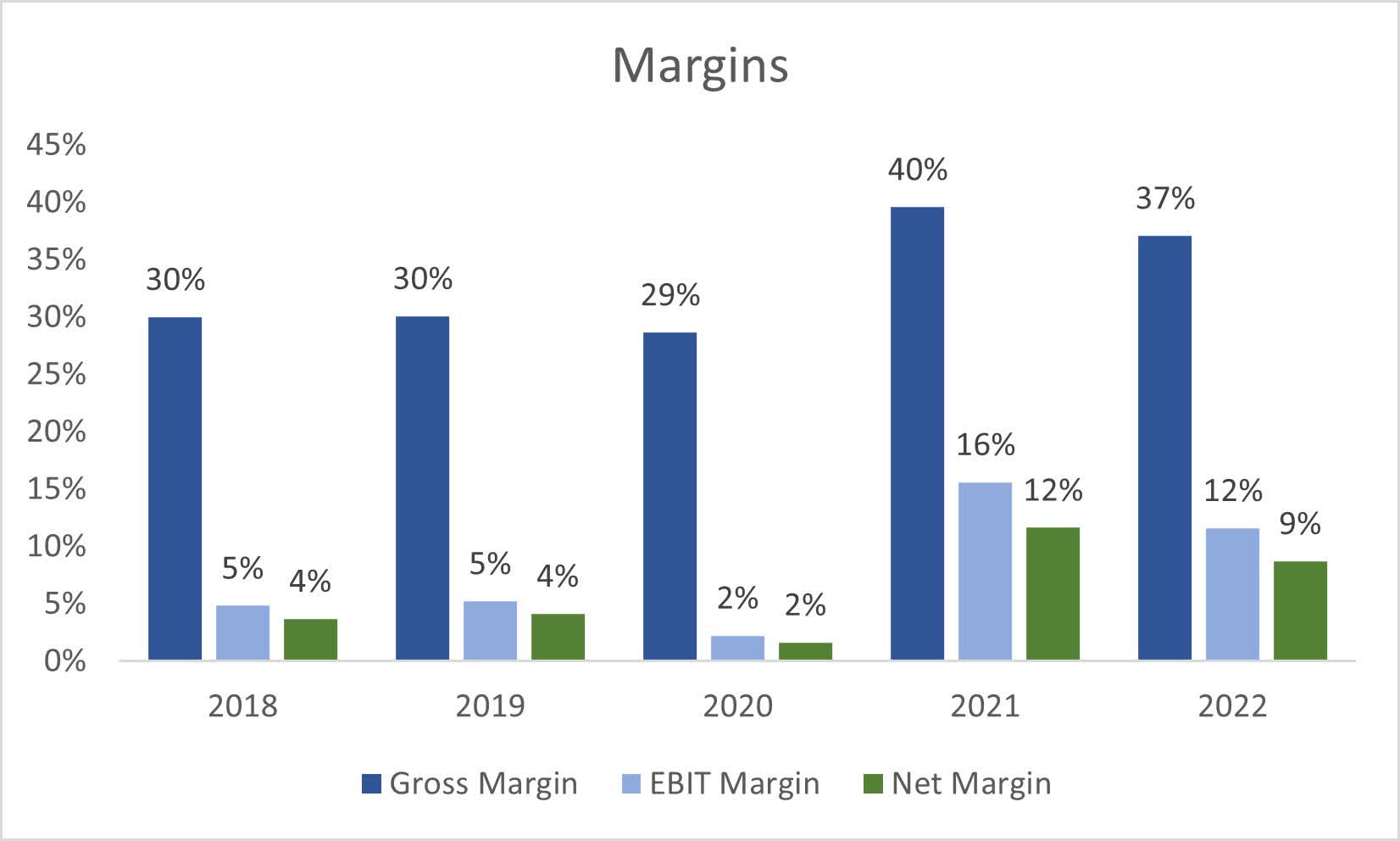

I am also very impressed with how the margins have improved over the last couple of years. I don’t think these will go back to the lows of FY20, and I think these will stabilize around these levels going forward. The management did a commendable job in improving the profitability and efficiency of the company, and I hope these cost-cutting measures will stick. Although, as of Q2 ’23, the company’s margins have come down slightly more, I don’t think this is very worrisome because there are still 2 more quarters to see how these develop in the end.

{kind=link}

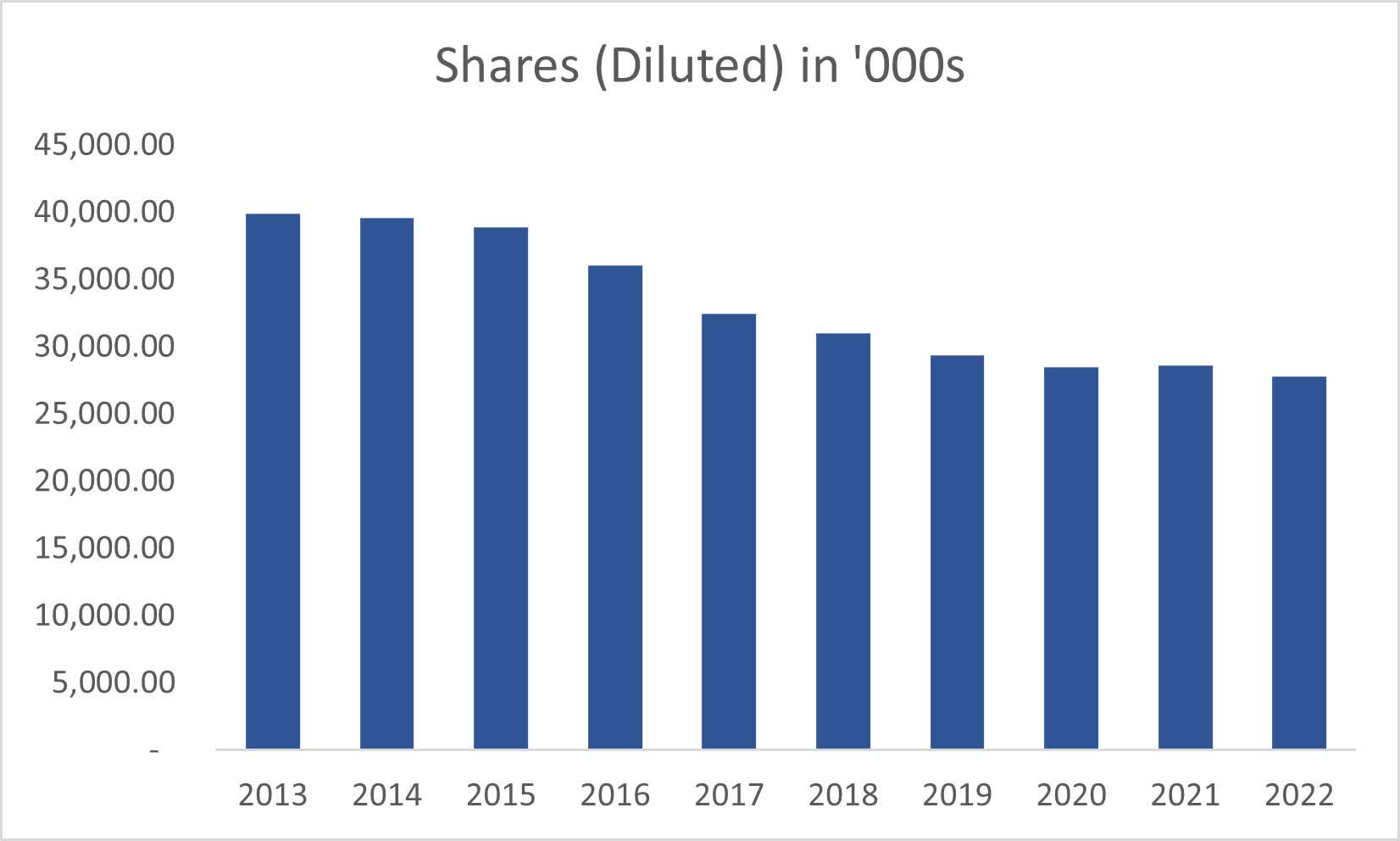

The company has also been reducing the share count steadily over the last decade, which is a good sign, especially if the share price is undervalued but we’ll see if it is in the next section.

{kind=link}

Overall, I don't see anything that would be a red flag so far, except for further slight deterioration in the margins as of Q2 '23, however, that is why I don't look at q-o-q numbers because these tend to fluctuate more and distort the overall trend of where the company's heading.

Risks

There may be some potential risks for the company that may stop me from opening a full position and letting it ride for years to come.

The company is dependent on two big vendors for a big chunk of their business, Nike and Skechers, which accounted for around 27% of net sales in FY22. The good thing is that this dependency reduced quite considerably from previous years, for example, the two vendors made up 43% in FY20. If for some reason, the company loses these two because of price disputes or something else, that will affect the company’s revenues significantly.

Margins may continue to deteriorate because the highs of FY21 were unsustainable and the company may revert to the low margins it saw pre-pandemic, which is less than half of profitability.

As the company is unknown to a lot of investors and mass media, the company may never reach its full potential as there isn't enough demand for the stock. The average volume is less than 300k shares traded daily, so expect volatility.

Valuation

On average, the company grew its revenues at around 5% CAGR in the last decade, with massive growth in FY21 due to the pandemic rebound, which I believe will normalize going forward. For this reason, I decided to take a simple approach and for my base case, I went with a 3% CAGR over the next decade, which will just keep up with inflation conservatism's sake. For the optimistic case, I went with around 7% CAGR, while for the conservative case, I went with a 1% CAGR to give myself a range of possible outcomes.

In terms of margins, for gross margins, I decided to deteriorate these by around 400bps in the first couple of years to account for some inefficiencies and unforeseen costs that will weigh on earnings. Over time, these will improve to the margins seen at the end of FY22. For operating margins, I decided to improve these by 200bps or 2% by the end of FY32. This will bring net margins from 9% at the end of FY22 to as low as 6% in FY23 and gradually improve to around 10% by FY32, which seems reasonable and conservative to me.

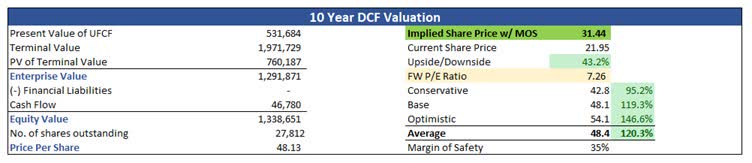

And because the company is relatively unknown, I will add a larger margin of safety to the intrinsic value calculation. I went with a 35% margin of safety, even though I liked the company's financials. With that said, Shoe Carnival’s intrinsic value is $31.44 a share, implying there is a 43% upside from current valuations.

{kind=link}

Closing Comments

The company's financials are outstanding. SCVL has no debt to weigh it down, which will protect it from any further downside in the economy, if we still see any. The company did decently during the 2020 pandemic, which only tells me how well the company is being managed by the current management.

I believe that the company's worth is even more than the intrinsic value assumed here because my assumptions were on a more conservative end and if the company can grow revenues at a slightly higher pace than what I estimated, the fair value would be much higher. However, I do like a good cushion, and I believe right now the company's a good buy at these levels and should perform well over the next years.

The company’s full potential may not be reached as the company is fairly unknown and doesn't get much media attention, which means a lot of people may not know about it. It is a good thing and a bad thing because, on the one hand, you can get in on a cheap stock and wait it out until the value is recognized and the bad because it may never be recognized.

For further details see:

Shoe Carnival: Financials Show A Strong Company And A Good Buy For The Long Term