SCVL - Shoe Carnival: Good Business But A Hold At Current Valuations

2023-12-05 23:34:46 ET

Summary

- Shoe Carnival is a successful footwear retailer in the US, with consistent profitability since going public in 1993.

- They deserve credit for responsible capital allocation thus far.

- The company has achieved record highs in revenue, gross profit, operating profit, and net income in 2022.

Shoe Carnival ( SCVL ) is one of the biggest footwear retailers in the US. Founded in 1978, they’ve been publicly traded since 1993, and have been profitable every year except one since IPO. Below is the long term share performance, followed by the period of best returns:

dividend channel dividend channel

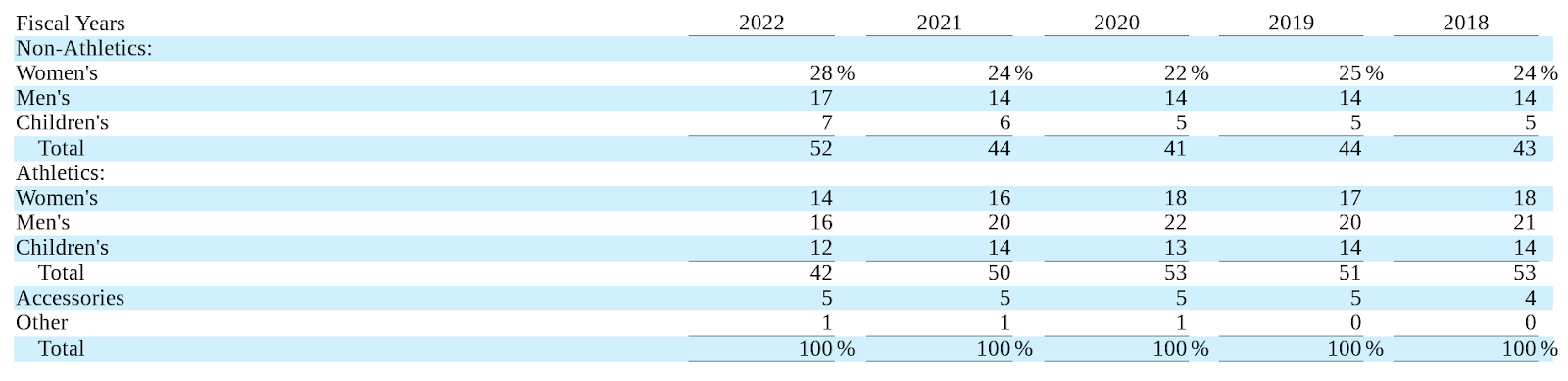

Below is their revenue breakdown:

{kind=link}

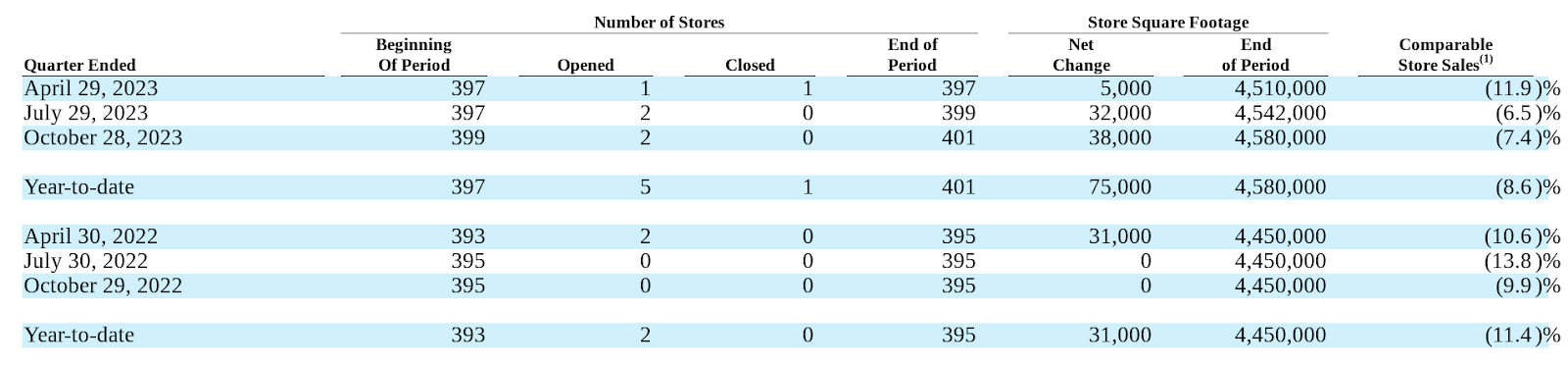

They operate almost 400 stores in 35 states, with the intention of reaching 500 stores by 2028. They also sell through e-commerce, which made up 10% of merchandise sales in 2022. Let’s look at the store count and square footage:

{kind=link}

Next, let’s take a look at the return metrics versus peers:

| Company |

| Revenue 10-Year CAGR |

| Median 10-Year ROE |

| Median 10-Year ROIC |

| EPS 10-Year CAGR |

| FCF/Share 10-Year CAGR |

| SCVL |

| 4% |

| 8.7% |

| 8.7% |

| 18.7% |

| n/a |

| Caleres ( CAL ) |

| 1.8% |

| 11.9% |

| 8.5% |

| 22.6% |

| 4.1% |

| Foot Locker ( FL ) |

| 3.5% |

| 20.3% |

| 16.1% |

| 3.3% |

| n/a |

| Genesco ( GCO ) |

| -0.9% |

| 9.9% |

| 7.9% |

| 1.9% |

| n/a |

| Designer Brands ( DBI ) |

| 3.9% |

| 13.9% |

| 12.5% |

| 3.4% |

| -0.7% |

In 2022, they achieved record highs in revenue, gross profit, operating profit, and net income.

Capital Allocation

In the table below, we see how capital was allocated in USD millions:

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| EBIT |

| 44 |

| 42 |

| 47 |

| 38 |

| 38 |

| 50 |

| 54 |

| 22 |

| 208 |

| 146 |

| FCF |

| 8 |

| 24 |

| 31 |

| 42 |

| 21 |

| 67 |

| 48 |

| 51 |

| 117 |

| -27 |

| Dividends |

| 5 |

| 5 |

| 5 |

| 5 |

| 5 |

| 5 |

| 6 |

| 5 |

| 8 |

| 10 |

| Repurchases |

| 7 |

| 18 |

| 42 |

| 30 |

| 46 |

| 38 |

| 7 |

| 30 |

| Debt Repayment |

| 177 |

| 40 |

| 25 |

| SBC |

| 3 |

| 1 |

| 4 |

| 4 |

| 5 |

| 10 |

| 6 |

| 4 |

| 6 |

| 5 |

The capital allocation has been pretty straight forward. They never made an acquisition until 2021 when they bought Shoe Station for $67 million, a private, family owned business. Acquisitions are a part of expected store growth, but I think they will spend more time nurturing their first acquisition ever instead of quickly the next one.

I’m a big believer in “cannibal” companies, as I’ve mentioned before, so I’m pleased that more is put towards buying back shares than to dividends. No matter how those two are split, the company has clearly matured to the point where it’s returning around half of FCF to shareholders.

Risk

The biggest long term risk is stagnant growth in revenue and earnings. They can always lose ground to Amazon in terms of ecommerce to some extent. My own opinion is that shoes are an item more people would prefer to try on, in person, compared to other categories of clothing.

The fundamentals are intact, and the company is financially strong. Their cash balance is $59.8 million while long term debt sits at $307 million. I also definitely like the 34% insider ownership, especially for a company this size.

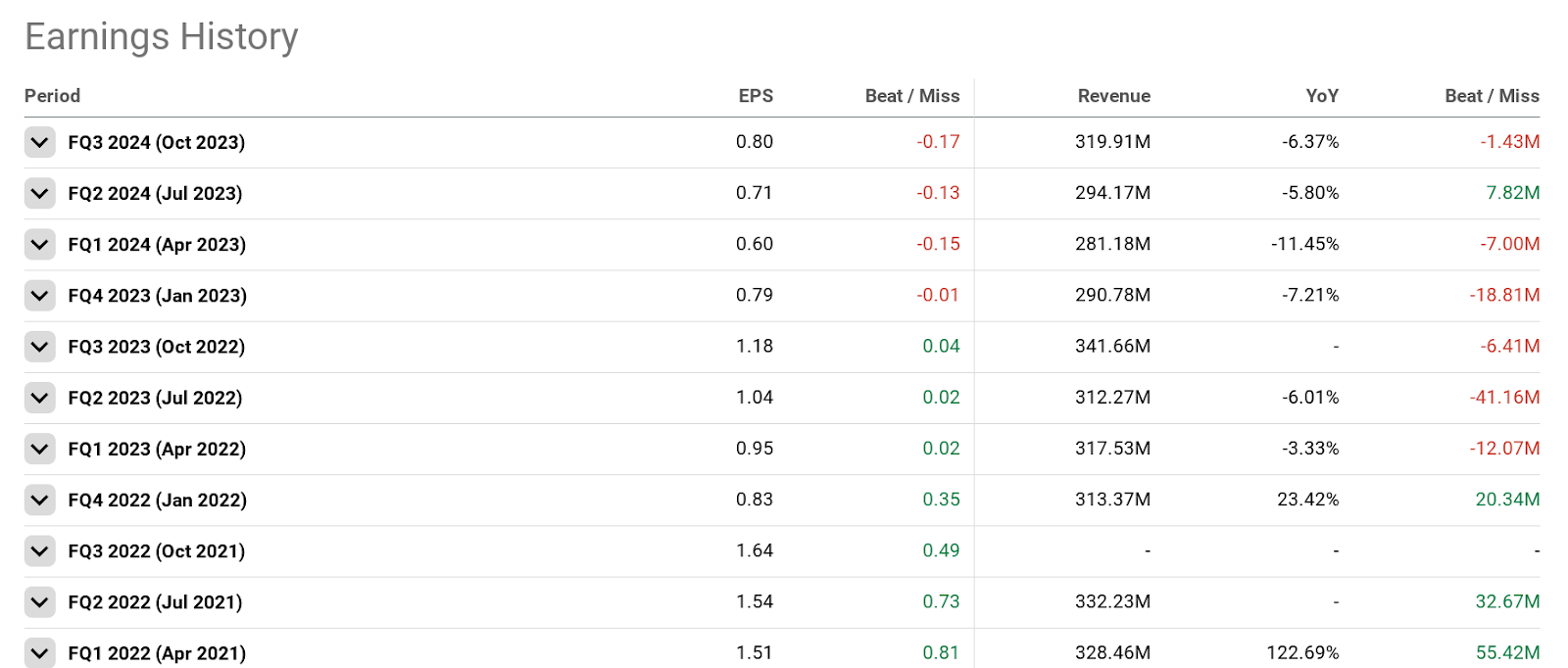

Q3 Earnings

Let's look at recent earnings:

{kind=link}

The recent misses are nothing to worry about in the long run. They are actually providing more opportunities to buy rather than showcasing any weakness. As I said in the risk section, the company is in good shape, and a few missed earnings shouldn’t mislead investors into thinking that the quality is now lower.

Valuation

First let's look at historical multiples followed by comp to peers:

macrotrends macrotrends macrotrends

| Company |

| EV/Sales |

| EV/EBITDA |

| EV/FCF |

| P/B |

| Div Yield |

| SCVL |

| 0.5 |

| 4.7 |

| 14.2 |

| 1.2 |

| 1.9% |

| CAL |

| 0.4 |

| 4.5 |

| 5.6 |

| 2.1 |

| 0.9% |

| FL |

| 0.4 |

| 6 |

| -24.4 |

| 0.9 |

| 9.6% |

| GCO |

| 0.2 |

| 4.2 |

| -2.3 |

| 0.6 |

| n/a |

| DBI |

| 0.3 |

| 4.7 |

| 5.1 |

| 1.6 |

| 1.6% |

The multiples appear low at first glance, but when we see how the competitors are being priced, it doesn’t look as cheap. So next we’ll look at the DCF model:

moneychimp

I used 2020 EPS, with the assumption that the record high earnings in 2022 will mean revert, as it did decline from that point in 2023. Since I expect shareholder yield to be a major driver of total return going forward, the growth of EPS isn’t the whole story.

In a case like this, buying at the right time has more to do with locking in a higher dividend yield in order to enhance the effect of shareholder yield. Now isn’t the right time, even though it's certainly not insanely overvalued. The dividend yield is too low to justify it right now, which leads to me giving this stock a “hold” rating

Conclusion

SCVL has been a good company and survivor in the tough game of retail, when so many others couldn’t sustain it. They deserve credit for responsible capital allocation, and for being very patient with acquisitions. All of the fundamentals indicate a sound, mature, business that will focus more on shareholder yield over growth. The price may not be right today, but the company is worth keeping an eye on, mainly for dividend opportunities over the long run.

For further details see:

Shoe Carnival: Good Business, But A Hold At Current Valuations