GOOG - Shopify: Financial Discipline Is Taking Hold

2023-10-31 13:08:43 ET

Summary

- Sale of Deliverr gets Shopify out of capital-intensive logistics business.

- Guidance implies substantial improvement in gross margins and free cash flow.

- EPS estimates for 2024 through 2026 appear to be low and will likely be raised after Q3 2023 report.

- Recent reports from META, Pinterest and Amazon imply strong advertising and e-commerce end markets.

It's been a while since I last released an article. Our office closed down shop in 2022 and we took some time off from what we perceived to be an overpriced market in the areas that we like to invest - namely in innovation and growth companies. In 2021 and 2022 we sold out of all of our positions that we have previously written about.

While a lot of growth stocks have risen and subsequently fallen, there are still some down over 70% from highs with their long term stories still intact. One company stands out to us as a potential winner that is undergoing a turnaround in its fundamentals and that just removed a giant albatross that was weighing on its financials.

About Shopify

I'm talking about Shopify ( SHOP ), a platform used by business owners, content creators, and designers to build websites. Founded in 2006, founder Tobi Luke created an open-source template language called Liquid, which is written in Ruby and has been used since its founding. This language powers the simplistic, what-you-see-is-what-you-get (WYSIWYG), website templates used by millions of businesses.

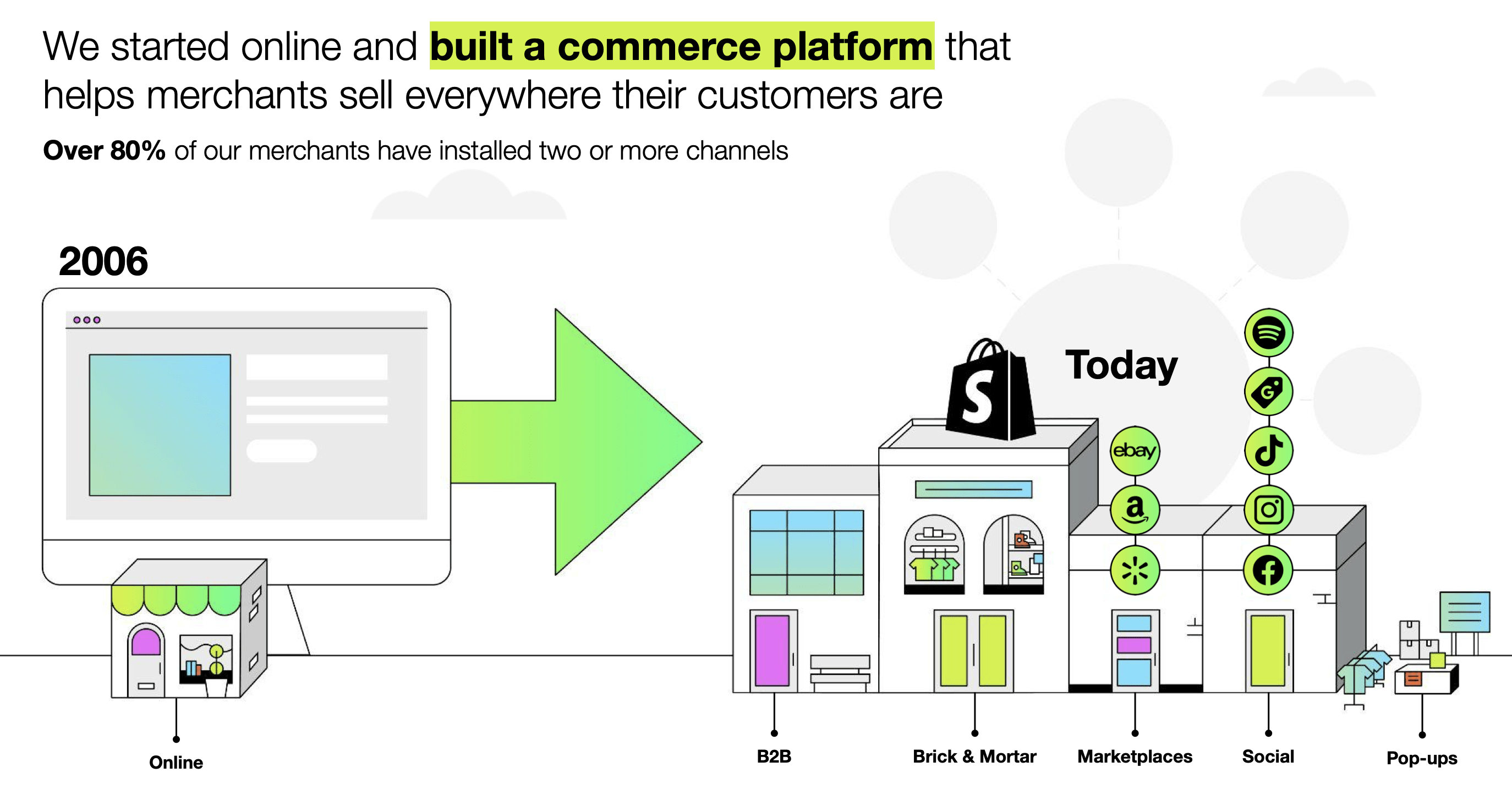

The company's platform helps merchants easily display, manage, advertise and sell their products across over a dozen different sales channels, including web and mobile storefronts, physical retail locations, pop-up shops, B2B, social media storefronts, native mobile apps, buy buttons, and marketplaces. More than 80% of Shopify merchants have installed two or more channels.

{kind=link}

Some of the world's largest brands use Shopify, including Nestle, Steve Madden, Lord & Taylor, Heinz, Crate & Barrel, and more.

{kind=link}

The Business Model

The company generates revenues from monthly fees (Subscription Solutions) it charges merchants to be on the platform as well as from fees on every transaction made by its customers (ie Merchant Solutions). It also has a thriving marketplace of apps developed by developers that are used by its merchants and Shopify takes a cut of the revenues generated from those apps, similar to Apple's ( AAPL ) App Store.

Subscription solutions revenues increased from $1,342.3 million in the year ended December 31, 2021 to $1,487.8 million in the year ended December 31, 2022, representing an increase of 10.8%.

Merchant solutions revenues, the faster growing segment, increased from $3,269.5 million in the year ended December 31, 2021 to $4,112.1 million in the year ended December 31, 2022, representing an increase of 25.8%.

Stickiness in Spades

One of the core concerns any tech investor has is how sticky the company's platform is. If switching from one platform to another is simple, then the durability of the company should be called into question.

With Shopify, you have a unique stickiness factor built into search engine rankings that makes switching from Shopify to another platform like Wix ( WIX ) intimidating for the user.

A website's search rankings drive a lot of the business that a company will do. The field of search engine optimization involves making changes to your website to drive more traffic from search engines like Google ( GOOG ).

When a business makes wholesale changes to their site, they need to spend a lot of time planning the changes and executing them. Switching to a new platform requires looking closely at your websites structure and planning for any changes that the new platform uses that differs from the existing platform you're using. Examples include:

- Site navigation - Some platforms will not automatically insert link trees (e.g., at the top of a page it might say websitename > collectionname > productname to help navigate users back to main category pages or the home page)

-

URL naming - One platform might name URLs with the following structure: websitename.com/collectionname/products/productname.html and another one might use websitename.com/productname.htm myonlineshop.com/collections/shoes/products/brown-shoe.

This matters to the search engine. Changing platforms means redirecting the traffic from every old page to every new page via what is called a 301 redirect. - Post migration - Submitting a new sitemap to the search engines to speed up their awareness of the changing site's architecture and navigation.

- Change of Address Request - You need to submit a change of address request to Google Search Console (and Bing, etc) notify them that your site has moved.

- Submit Change Of Address Request In Google Search Console And Complete Bing Site Move Tool

- Monitor Google Analytics for traffic changes.

According to Search Engine Journal , "If you don't plan and execute a migration correctly, organic traffic can be cut by 50% within weeks of migrating."

Imagine that you're a large business with thousands of web pages. This could take many months to prepare for and execute and after you complete your migration you have to hope that nothing goes wrong.

Or imagine you're a small business without the experience or resources needed to manage the technical details that this includes. You would likely have to either learn this yourself or hire someone that has the experience doing this.

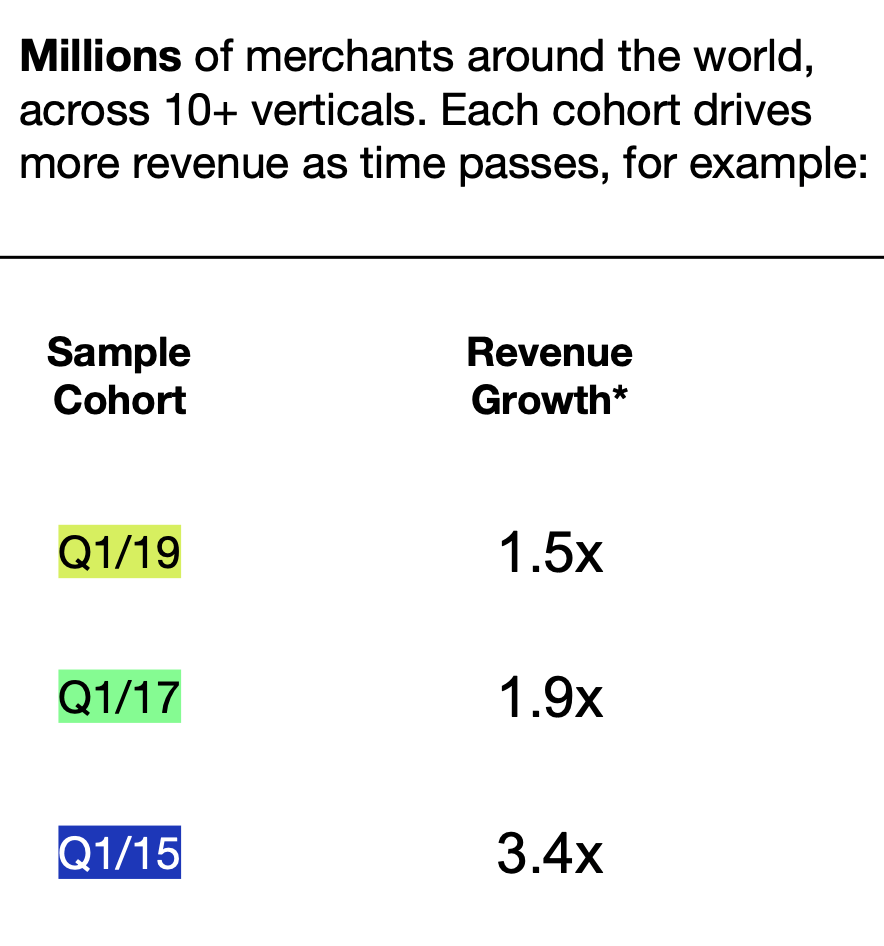

This stickiness shows up in the company's revenue cohorts. That is, Shopify tracks and disclose revenues coming from cohorts of customers that sign up in historical periods to show how their revenue continues to compound.

Below is a sample of cohorts of customers from various time periods and the revenue growth they've seen from these cohorts as of Q2 2023:

{kind=link}

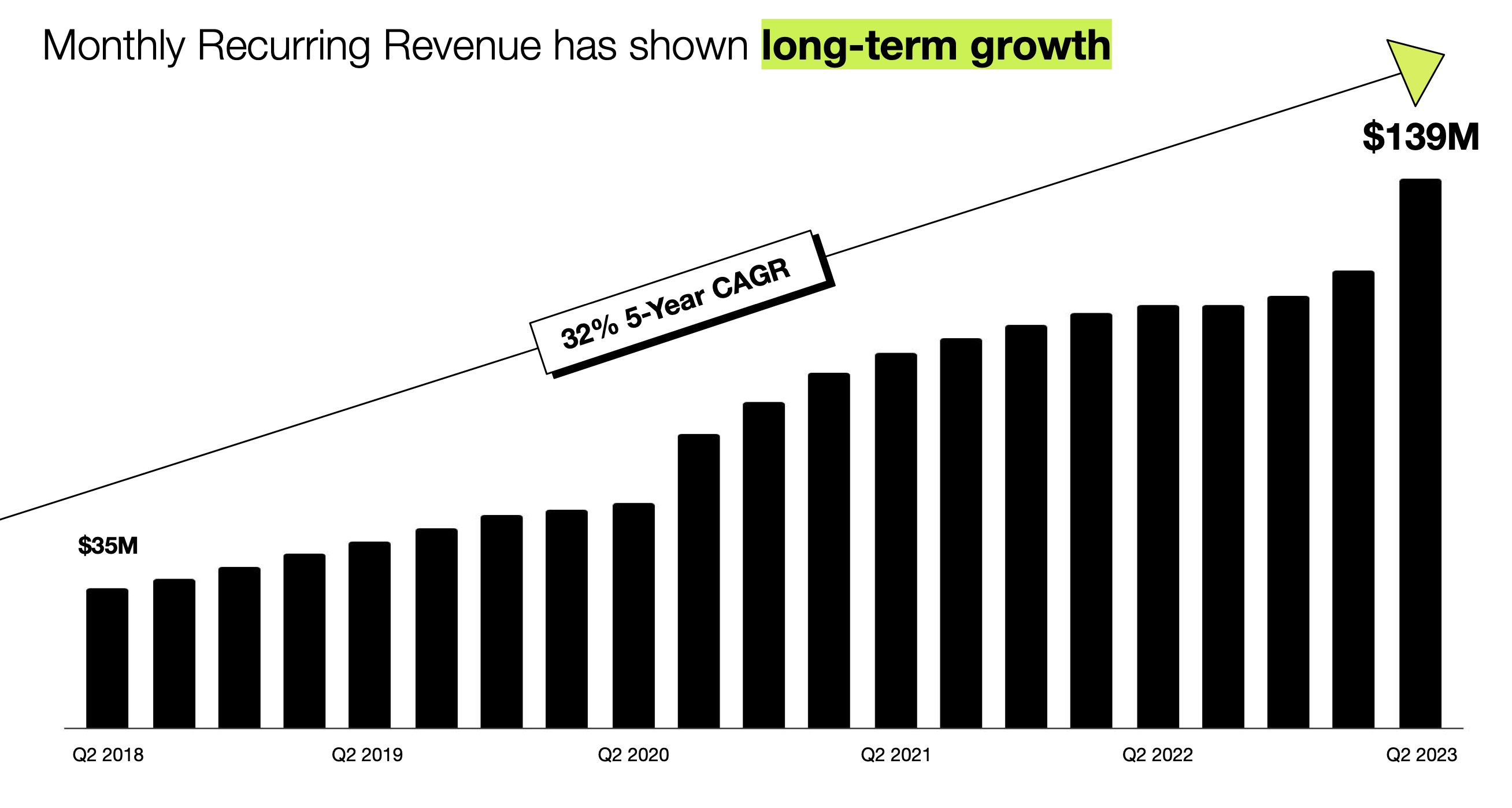

The stickiness has enabled Shopify to build an ever growing customer list that is starting to flex its financial muscles. Below is a chart showing the monthly Subscription Revenues, where you can really visualize said stickiness.

{kind=link}

You will notice the spike in Q2 2023, which is the result of a price hike the company instituted that seemingly went through without much attrition. The result is an ever growing pile of revenues that are high margin. While a $560 Million annualized revenue run rate is certainly not enough on its own to warrant a $60 Billion market cap, your mind can wander as to the potential size this could become, particularly when this was just $140 M annualized five years ago.

If this piece grows at a 20% CAGR over the next five years it can get to $1.38 Billion in 2027. Using a 10x price to sales ratio, this could equate to roughly $13.8 Billion of value or about 26% of today's enterprise value.

Sale of Deliverr

In an attempt to compete with Amazon ( AMZN ) and offer logistics services and warehousing to its customers, Shopify acquired Deliverr in 2022 . This turned out to be a colossal mistake, shifting the company from a capital light business model to a capital intensive model at a time when the market was increasingly focused on near term profits.

The company had already made forays into logistics, which weighed heavily on margins. The capital expenditures required to build out the infrastructure needed to compete with Amazon on same day deliveries were likely to weigh on Shopify's earnings for a long time.

As interest rates rose sharply during 2022, investor's emphasis shifted to profitability in the near term and it was clear that investors wanted no part of this Capex buildout, particularly with a low margin business like logistics, and particularly against the behemoth that is Amazon.

The bottom in Shopify's stock fell out when it announced the acquisition of Deliverr , dropping 30% in that week alone.

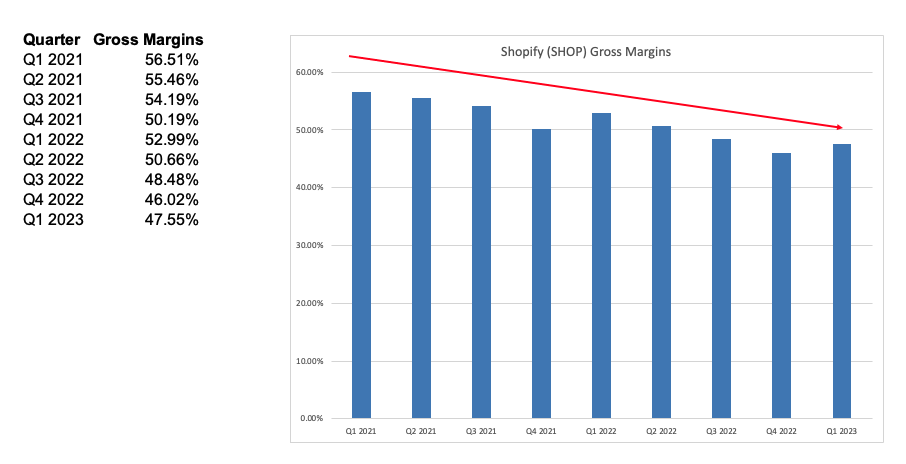

The hit to gross margins as the company shifted to logistics has been dramatic. A portion of the decline is attributable to Merchant solutions, which is lower margin, but another portion pertains to increased spend on logistics. The chart below shows the trend, from 56% in Q1 2021 to 46% in Q4 2022.

Shopify Gross Margins (Author)

{kind=link}

So not surprisingly, when the company announced the sale of Deliverr and did a complete about face on their intention to expand their logistics ambitions, investors cheered.

Back to a Capital Light Business

With Deliverr and capital intensive expansion plans out of the way, investors can now focus on the longer term opportunity that Shopify has in becoming the operating system for brands selling their wares online.

Some recent product introductions show their ambitions to capture a growing share of merchants operating expenses:

- Integrated Shop Pay Installments into Shopify Point-of-Sale allowing retail merchants the ability to offer in-store shoppers the same payment flexibility offered online.

- Completed the U.S. roll out of Shop Cash , a rewards program that allows shoppers to earn Shop Cash on eligible Shop Pay purchases and redeem it in the Shop app.

- Launched Shopify Bill Pay , a new tool that streamlines expense management by enabling merchants to manage and pay vendors directly in the Shopify admin.

- Launched Shopify Tax, which offers robust tax compliance tools for U.S.-based merchants that sell to customers in the United States, including sales tax liability insights, product category suggestions, and precise calculation technology to collect tax based on specific addresses within 11,000+ United States tax jurisdictions.

If we think about the potential here for Shopify to expand horizontally across all of the operating expenses that a merchant incurs, the potential is enormous.

Shop Cash and Point of Sale gets them into the real world POS market. Shopify Bill Pay gets them into the financial operations segment that Bill.com ( BILL ) operates in, while Shopify Tax puts them into the same segment as Avalara, two companies valued at $8 Billion or more, each.

All of these new product introductions are much higher margin tools than logistics and will help turn SHOP into a cash flow machine.

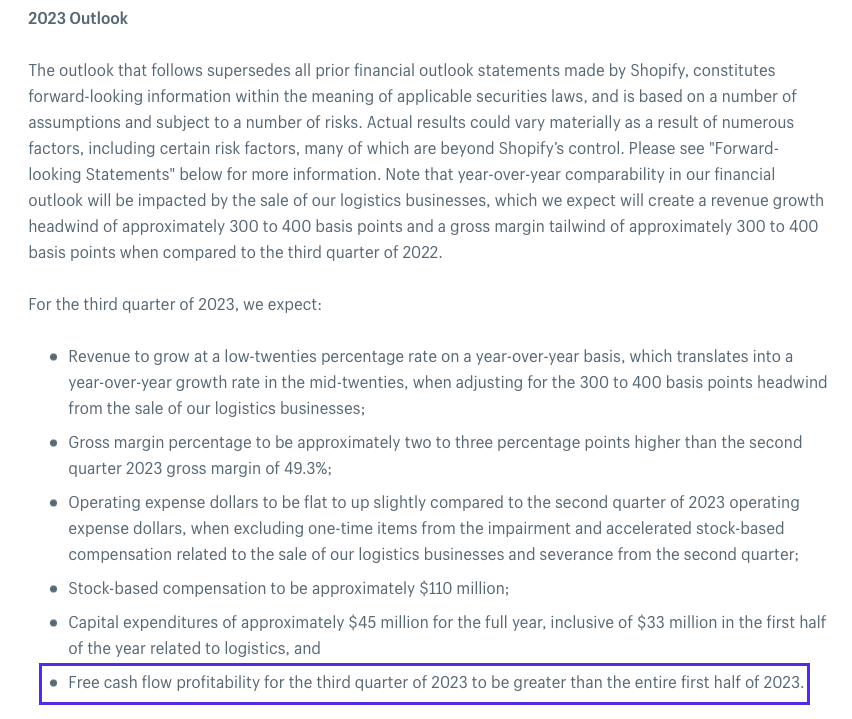

To that end, managements guidance for FCF in Q3 was eye opening:

{kind=link}

For Q1 and Q2 2023, Shopify reported FCF of $183 Million combined. Guidance implied free cash flow of close to $200 Million for just Q3 2023 alone. This would be an improvement of almost $500 Million from Q3 2022 of negative $300 Million.

Analyst Estimates Look too Low

Using guidance of low 20% revenue growth for Q3 2023, coupled with operating expenses flat from Q2 2023 (see below), and gross margins of 51.8%, here is what Q2 2023 numbers should come in at:

Revenues: $1.67 Billion

Gross Profit: $864 Million (51.8%)

Operating Expenses: $818 Million (flat from adjusted Q2 2023 expenses)

Operating Income: $46 Million

Interest Income: $47 Million (assumes net $3.8 Billion cash balance at 5%)

TOTAL Income: $93 Million

Shares: 1.28 Billion

GAAP EPS: +$0.07

Stock Based Compensation: $110 Million (above)

Non GAAP Profits: $203 Million

Non GAAP EPS: +$0.16

Operating Expense Guidance (Shopify Conference Call)

Management typically guides conservatively, so realistically we should expect non GAAP EPS to come in around $0.20 vs $0.14 estimates. At a $0.80 annualized run rate with EPS growth expectations of 50% in 2024, SHOP is now trading at under a PEG of 1.0.

Non GAAP EPS Estimates of $0.78 for 2024 already look way too low. I would expect those estimates to go up to well over $1.00 after this quarter. That also means that estimates for 2025 (+$1.05) and 2025 (+$1.50) are too low. Realistically, we should expect those numbers to go up to $1.40 and $2.00.

Conclusion

Now that Shopify has put the logistics excursion in its rear view mirror, investors can get back to valuing this company on the basis of a high growth software company with expanding margins.

My estimates for 2024/25/26 non GAAP EPS are $1.05 / $1.40 / $2.00 EPS. With roughly $7 Billion in net cash and a current enterprise value of $53 Billion, this implies the following valuations:

EV/2024 EPS: 39X

EV/2025 EPS: 29X

EV/2026 EPS: 20.7

The valuation is very compelling to me at these levels. I would expect this to generate returns in excess of 15% for the next 3-5 years.

For further details see:

Shopify: Financial Discipline Is Taking Hold