CA - Shopify: I Am Still Cautious Despite Stellar Quarter

2023-11-07 08:00:00 ET

Summary

- Shopify's quarterly performance was strong, with a 25.5% YoY increase in revenue and substantially improved profitability metrics.

- The company's focus on innovation and expanding internationally positions it well to capture positive secular shifts in the e-commerce market.

- However, valuation analysis suggests that the stock is already priced for massive optimism, with limited upside potential and growth momentum is expected to decelerate due to high-interest rates.

Investment thesis

My first thesis about Shopify (SHOP), which was cautious, aged well since the stock notably underperformed the broader U.S. market over the last quarter. Today, I would like to explain why I am still cautious and reiterate the "Hold" rating despite stellar quarterly performance. I like the company's business from the secular point of view as it looks well-positioned to capture positive secular shifts. However, my valuation analysis suggests that massive optimism is already priced in as there is almost no upside potential, even if optimistic assumptions are incorporated. I also think that stellar growth momentum is poised to decelerate over multiple quarters as tight monetary policies across the developed world will weigh on the level of economic activity.

Recent developments

The latest quarterly earnings were released on November 2, when the company topped consensus estimates. Revenue demonstrated a strong 25.5% YoY increase, indicating strong momentum. Shopify's massive layoff in May, which meant a cut of 20% of the workforce, is working as the company demonstrated a strong expansion of its profitability metrics. The gross margin expanded YoY by more than four percentage points, but the major improvement was in the operating margin. It has improved YoY from -22% to 13%, which is a strong bullish sign.

Seeking Alpha

The fact that the top line increased YoY by almost a quarter despite massive layoffs suggests that the management's bold decision to cut a notable portion of the global workforce was sound and well-weighted. The profitability expansion allowed SHOP to generate $278 million in operating cash flow, which is the highest since the December 2021 quarter, when interest rates were at their lowest and there was no war in Ukraine. Such a strong operating cash flow suggests solid resilience of the business model even in the current harsh environment.

Having the operating margin improved significantly gives me a positive outlook for the company's financial position for the long term. As of the last reporting date, the company had a low leverage ratio and almost $5 billion in cash. Liquidity metrics are also in great shape. With a fortress financial position, Shopify is well-positioned to continue investing in growth, both by developing new features and lines of business in-house or via acquisitions.

Seeking Alpha

The upcoming quarter's earnings release is scheduled for February 15, 2024. Revenue is expected to sustain strong growth momentum as consensus estimates forecast almost a 20% YoY increase. The bottom line is expected to follow the revenue increase as the adjusted EPS is projected by consensus to expand from $0.07 to $0.30.

Seeking Alpha

Robust consensus estimates for the upcoming quarter suggest confidence in the company's near-term prospects. Indeed, Shopify's stellar revenue growth despite the current harsh environment of high-interest rates and vast macroeconomic uncertainty suggests that the company's "Merchant First" business model is resilient to headwinds. The management's focus on innovation also helps build trust and loyalty among its merchant base in my view.

The company reinvests more than a quarter of its sales into innovation, as suggested by the above chart. The management's strong commitment to innovation allows the company to keep up with the rapidly evolving technological environment as it offers its clients cutting-edge AI tools for merchants like Shopify Magic and Sidekick . These tools help merchants streamline and grow their businesses, which is crucial for Shopify's business model.

I believe its business model will be successful if the company ensures the merchant's network continues to grow at double-digits over the long run. Shopify positions itself as a comprehensive solution for merchants aimed to support them at each stage of growth, and the company's improvement in profitability as the business scales up suggests that the greater the network will be, the wider profitability metrics SHOP will be able to generate. According to Precedence Research , the global e-commerce market is expected to compound by 15% over the next decade. This is a massive secular tailwind for Shopify. The company's focus on improving merchant's experience and increasing the probability of success makes it an excellent choice for entrepreneurs to select SHOP as a one-stop-shop as an infrastructure to build a business. The success of other entrepreneurs is usually inspiring, and there are plenty of success stories of multimillion-dollar businesses built with the help of Shopify.

I also like that the management not only focuses on improving financial performance with the improved customer experience but also seeks opportunities to expand internationally. According to the latest earnings call , SHOP also experiences strong growth momentum in terms of the gross merchandise value [GMV] and number of merchants across the biggest European markets, including Germany, France, and the UK.

Despite the business demonstrating strong growth momentum even in the current, I am still cautious. Tight monetary policy in the U.S. is likely to last higher for longer . Unemployment metrics are still strong, and with oil prices flying high, there is a high probability that the inflation battle will take longer than was initially expected. Consumer spending is also strong , with room to keep interest rates high. Shopify's success depends on the GMV dynamics, and this is poised to decelerate under tight monetary policies across the developed world.

Valuation update

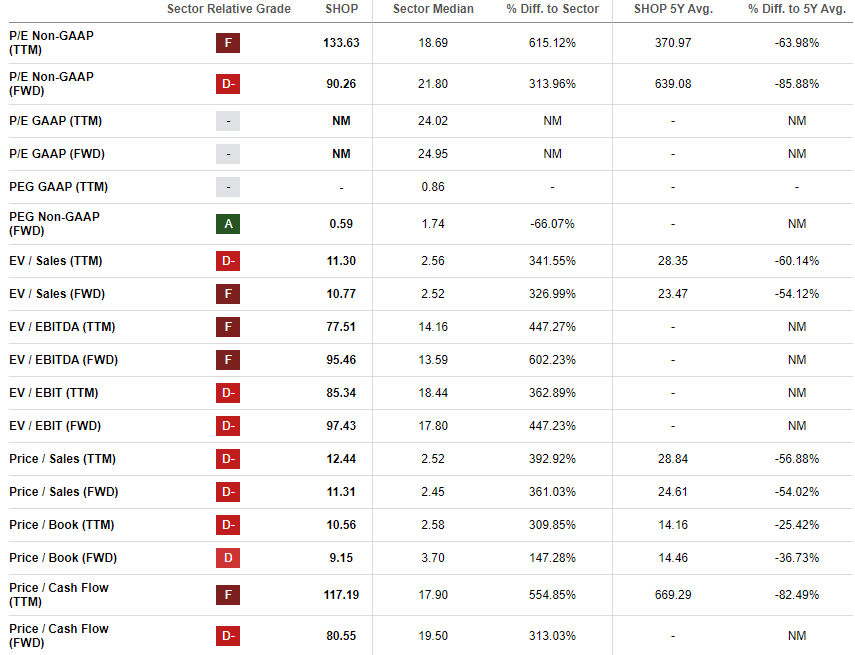

The stock price rallied by 72% year-to-date, significantly outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent "C+" valuation grade because of the mixed outcomes of ratios analysis. Current multiples are substantially higher than the sector median across the board. On the other hand, current multiples are notably lower than the five-year averages. This might indicate undervaluation since it is more appropriate to compare with the company's historical averages as SHOP's revenue growth rate by far outperforms the sector median.

{kind=link}

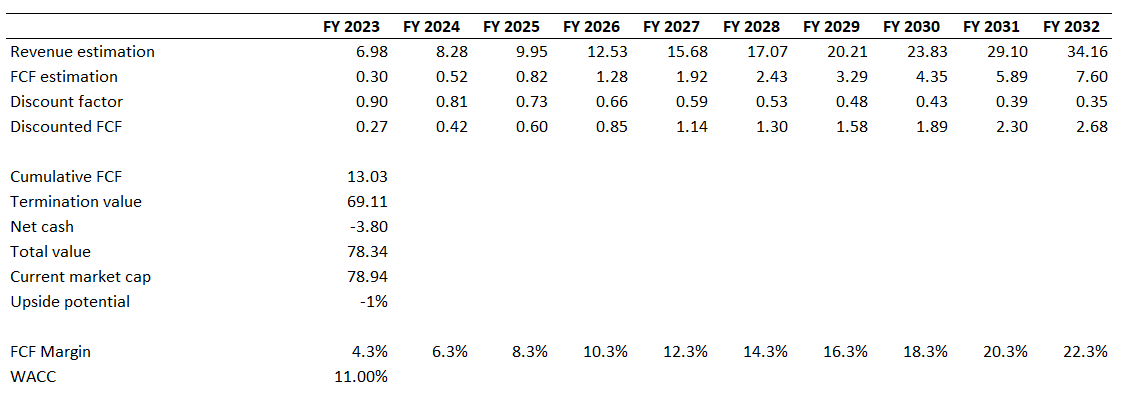

To get more conviction, I have to simulate a discounted cash flow [DCF] model. I use an elevated 11% WACC, which is higher than my initial model by one percentage point. The reason why I am more cautious is because of the Fed's recent hawkish rhetoric suggesting rates to stay higher for longer. I use a TTM FCF ex-SBC margin of 4.3% and expect a two percentage point yearly expansion over the long term. I use revenue consensus estimates for the next decade, projecting a 19% CAGR.

{kind=link}

According to my DCF simulation, the stock is fairly valued. The business's fair value is about 78$ billion, which is almost identical to the current market cap. That said, I can conclude that the stock is fairly valued now with almost no upside potential. I would also like to underline that most of the underlying assumptions are optimistic since it is a big challenge to sustain a 19% revenue CAGR over the decade, and a two percentage points yearly FCF expansion is also an extraordinary target.

Risks to my cautious thesis

The most obvious risk to my cautious thesis is the sudden change in the monetary policy. Interest rates affect the valuation of growth companies a lot because of the discounting of future cash flows. The higher the discount rate, the lower the present value of future cash flows. That said, if a rapid pivot in the Fed's rhetoric occurs, this might be a powerful catalyst for all growth stocks, especially for high-quality businesses like Shopify.

Investor's sentiment and hot headlines significantly affect stock prices in the short term as well. Such news is difficult to forecast, but stock prices can move up by double-digits in one day if the market considers this news as very beneficial for the company. This also brings a high level of uncertainty for my cautious thesis.

Bottom line

To conclude, SHOP is still a "Hold". While the company demonstrated a stellar previous quarter, my valuation analysis suggests that the vast optimism is already priced in. I like the management's firm commitment to innovation and have high conviction that the company is well-positioned to absorb massive secular tailwinds. But over the near term, I expect the company's growth profile to shrink as tight monetary policy will weigh on consumer spending as interest rates stay higher for longer.

For further details see:

Shopify: I Am Still Cautious Despite Stellar Quarter