CA - Shopify: It's Just Math Decade Of Underperformance Ahead

2024-01-18 06:59:36 ET

Summary

- Shopify's stock has delivered stunning returns over the past year.

- The company has shown accelerating top-line growth alongside dramatic boosts in profitability.

- While all fundamental indicators are pointing in the right direction, I question the stock's valuation.

- Consensus estimates look very aggressive, and I explain why the stock is priced for perfection.

I don't short stocks solely on the basis of overvaluation, but Shopify (SHOP) has seen its stock rise to deniably lofty levels. The company is seeing a perfect storm of tailwinds between a macro recovery as well as improved operational efficiencies. Management appears to be more focused on profitability than ever, guiding for even more free cash flow growth over the coming year. SHOP has seen its stock soar alongside a melt-up in the tech sector, but I question whether the sharp upward move is justified. I critically analyze consensus estimates and explain why the valuation is aggressive based on those estimates. I continue to view SHOP stock as being dangerous at current levels - I reiterate my avoid rating.

SHOP Stock Price

When growth almost disappeared following aggressive pandemic growth, SHOP saw its stock among the most beaten-down names, as investor sentiment swung from extreme optimism to extreme pessimism. The stock has been one of the biggest winners over the past year.

I last covered SHOP in September where I explained why the company's Buy With Prime partnership with Amazon (AMZN) was a reason to sell, not buy the stock (though I stuck with my neutral rating). The stock is up since then, but I expect this rally to run out of steam.

SHOP Stock Key Metrics

In its most recent quarter, SHOP delivered 22% YoY growth in GMV as the company continues to lap easy comparables. The company had shown just 11% YoY growth in GMV in the third quarter of 2022.

2023 Q3 Presentation

SHOP was able to generate stronger revenue growth at 25% YoY, coming at the high end of guidance for "low 20's" growth. Revenue growth exceeded GMV growth due to the company's pricing change implemented at the beginning of 2023.

2023 Q3 Presentation

SHOP saw gross margins expand 410 bps to 52.6% as the company benefited from the sale of its lower margin logistics business.

2023 Q3 Presentation

Combine that gross margin expansion with increased operational efficiencies and SHOP was able to generate $122 million of operating income, representing a 7% operating margin - in the prior year, SHOP had lost $346 million in operating income. SHOP was able to generate $276 million of free cash flow in the quarter, up from negative $148 million in the prior year. While I may have disagreements about the extent of this tech stock rally, the initial recovery makes a lot of sense given the dramatic transformation in profitability seen at SHOP and others.

SHOP ended the quarter with $4.9 billion of cash and marketable securities or $4 billion in net cash after accounting for the convertible notes.

Looking ahead, management has guided for high-teens revenue growth in the fourth quarter. The company had generated 26% YoY growth in the prior year so it would not have the benefit of an easier comp. Consensus estimates call for $2.07 billion in revenue, implying high teens YoY growth.

2023 Q3 Presentation

Management continues to expect gross margins to expand up to 400 bps in the fourth quarter, again due to the sale of the logistics business.

On the conference call , management noted that they have now delivered four consecutive quarters of positive free cash flow, with the third quarter generating more FCF than the prior three quarters combined. One of the bearish points amidst the 2022 tech stock crash was the inability to generate profits - SHOP (and others) have clearly debunked such fears. Despite the strong momentum, management declined to offer either a long term growth outlook or profitability framework at their 2023 Investor Day .

Is SHOP Stock A Buy, Sell, or Hold?

In short, SHOP represents a pure-play investment in the growth of e-commerce. For everything that is not Amazon, SHOP offers a comprehensive end-to-end solution to empower e-commerce operations. While growth has slowed post-pandemic, e-commerce remains an unstoppable growth story and penetration continues to increase over time.

{kind=link}

As the largest and most well-known e-commerce platform outside of AMZN, SHOP has historically garnered a premium valuation and that remains the case today. SHOP found its stock trading at 120x this year's earnings.

{kind=link}

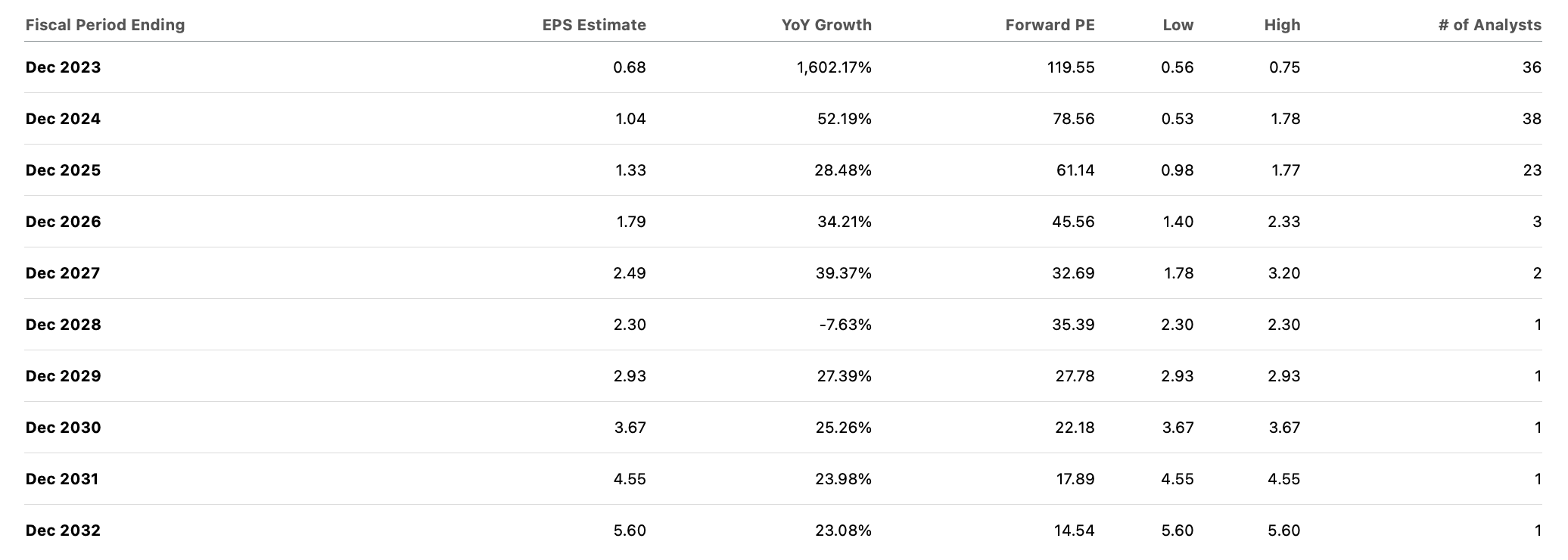

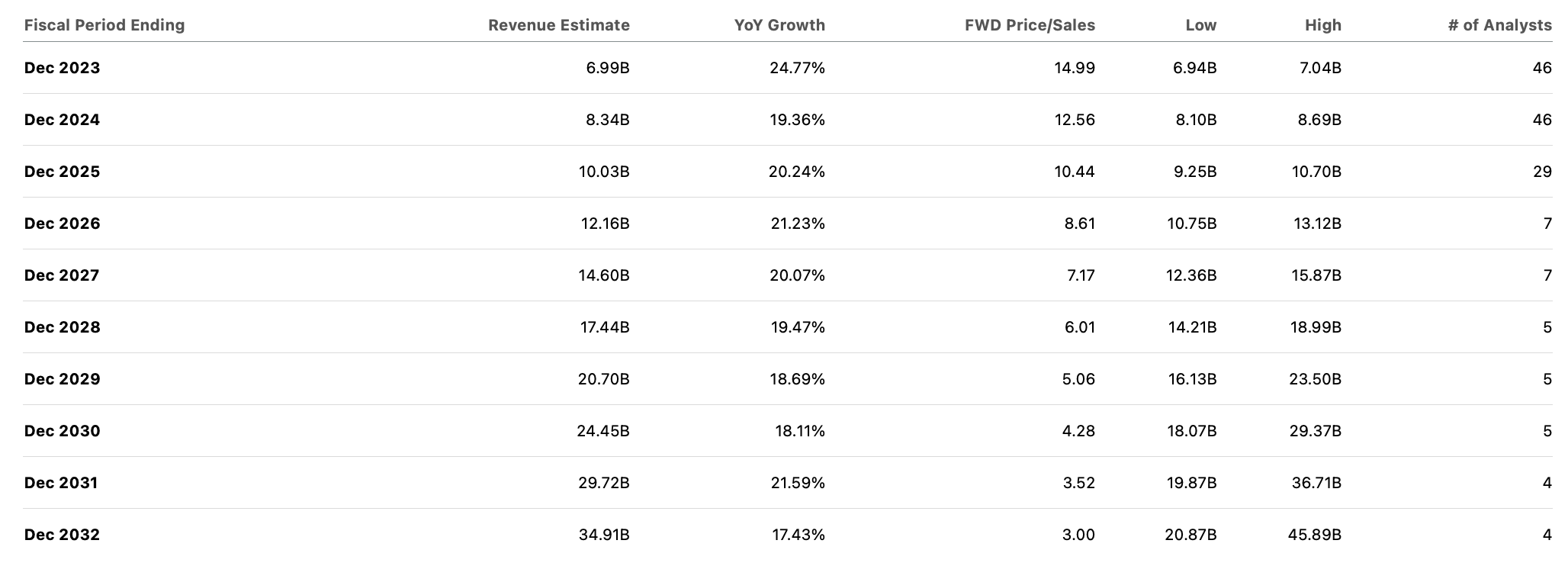

Consensus estimates call for SHOP to sustain nearly 20% top-line growth for nearly the next decade.

{kind=link}

Those consensus estimates look aggressive when one factors in the likelihood that GMV growth should decelerate from here due to the law of large numbers. But perhaps there is one important detail to understand in the bull thesis. Unlike the estimated 15% take rate charged by AMZN, SHOP in general charges around 2.9% . AMZN has (more than) justified their high take rate through their sales funnel and irreplaceable logistics network. Over time, SHOP may be able to increase their take rate, perhaps through the build-out of their Shop App, which would be a similar e-commerce marketplace platform.

2023 Q3 Presentation

Take rate expansion can have a dramatic impact on the bottom-line. Consider that even inclusive of the company's profitability gains, operating profits still made up just 7% of revenue.

2023 Q3 Release

If SHOP were to be able to increase their average take rate to 5%, that may imply a roughly 60% increase in revenues, which might lead to around a 5x increase in operating profits.

Coming back to consensus estimates, I could see SHOP generating around 13-15% top-line growth from GMV growth over the next many years (though that might even prove aggressively high). Perhaps the remaining 5-7% gap from consensus can be made up from take rate expansion. 9 years of 6% annual take rate expansion would have SHOP ending up with a take rate around 69% higher than now, or around 5%. I am of the view that consensus estimates are full if not outright aggressive given that they appear to be pricing in a very rapid increase in take rates.

Perhaps by 2032, SHOP can sustain around 13% top-line growth. With 2032 estimates calling for a 21% net margin, I do not anticipate much margin expansion from there (recall that SHOP has outsourced much of its operations with the most significant being from its sale of its logistics business). If SHOP can garner a 2x price to earnings growth ratio ('PEG ratio') in 2032, then the stock might trade at around 26x earnings, implying a stock price of around $145 per share. That implies around 6.6% annualized returns over the next 9 years (or perhaps around 8% to 9% inclusive of earnings yield). Given the aggressiveness of the estimates and valuation, I find such return potential to be inadequate.

Some investors might suggest that SHOP deserves higher valuations than 26x 2032e earnings. I'd take the opposite side of the argument. SHOP's sale of its logistics business has clearly improved profit margins but I am now hard pressed to believe that SHOP can avoid ceding market share to AMZN over time, especially as AMZN continues to increase the availability of its lightning-fast shipping speeds. At best, AMZN's increasing dominance may add pressure to the company's ability to hit consensus estimates. The fact that SHOP has partnered with Amazon Pay does not mean that the Amazon threat has disappeared - I view this to be more like how Google Search has disrupted the likes of Expedia ( EXPE ) and others through taking a large cut of processed volumes. SHOP might always appeal to smaller and medium sized businesses which might not sell the type of volume that benefits from AMZN's logistics network, but I am skeptical that the company can hit consensus estimates if it is restricted to these markets.

Given that SHOP is trading at valuations that offer only modest rewards against aggressive estimates, I must reiterate my "avoid" rating as this is the kind of stock that might underperform in the event that things do not go perfectly.

For further details see:

Shopify: It's Just Math, Decade Of Underperformance Ahead