CA - Shopify Q3: Strong Growth But No Bargain

2023-11-06 13:52:43 ET

Summary

- Shopify's Q3 earnings beat estimates by a wide margin, and the e-commerce company submitted strong guidance for FY 2023 revenues.

- The recent collaboration between Amazon and Shopify could lead to increased revenue growth for Shopify, especially in the already booming subscription segment.

- Despite positive momentum, Shopify's high valuation and lack of consistent profitability pose risks.

Shopify (SHOP) stock soared last week after the e-commerce company demolished estimates and issued an optimistic forecast for FY 2023 revenue growth. Shopify's strong revenue momentum -- especially in gross merchandise volume and subscriptions -- and robust top-line guidance for the current fiscal year caused shares to soar 22% right after earnings and the momentum has so far been sustained. As much as I like Shopify, its merchant-centric e-commerce business model as well the recent deal with Amazon (AMZN), I believe that shares are now trading again on the expensive side. Shopify's shares are now trading above their 1-year average P/S ratio which implies a slightly unfavorable risk profile!

Previous rating

I previously rated Shopify a strong buy due to the e-commerce company's momentum in Merchant Solutions revenues and potential for gross margin expansion, calling it: A Top Bet On E-Commerce Growth .

Shopify's Q3'23 earnings card was impressive, but I believe investors are potentially getting a bit carried away here in their optimism. Shopify is now highly valued which seems excessive considering that the firm is still struggling with consistent GAAP profitability. The achievement of persistent GAAP profitability going forward would likely be perceived as an inflection point for this growth stock, however.

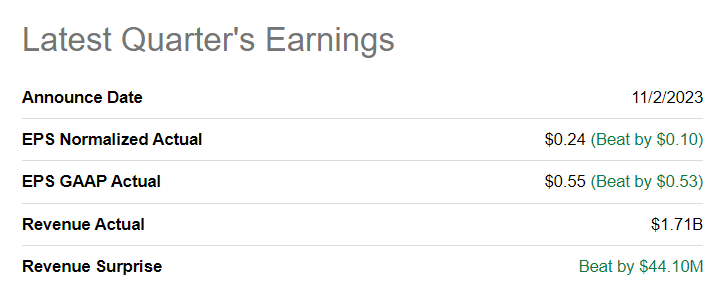

Huge earnings beat

Shopify earned $0.24 per share in adjusted earnings, beating the consensus estimate by a very wide margin of $0.10 per share. Revenues also came in higher (+$44.1M) than expected ($1.71B).

{kind=link}

Strong growth in GMV and revenues, subscription plan price increases driving segment growth

Shopify's gross merchandise volume/GMV -- a key metric for e-commerce companies that measures how many dollars are being spent on an e-commerce platform -- soared 22% in the third quarter to $56.2B. Shopify defines GMV as "the total dollar value of orders facilitated through the Shopify platform" and it is an indicator of platform strength as well as consumer spending trends.

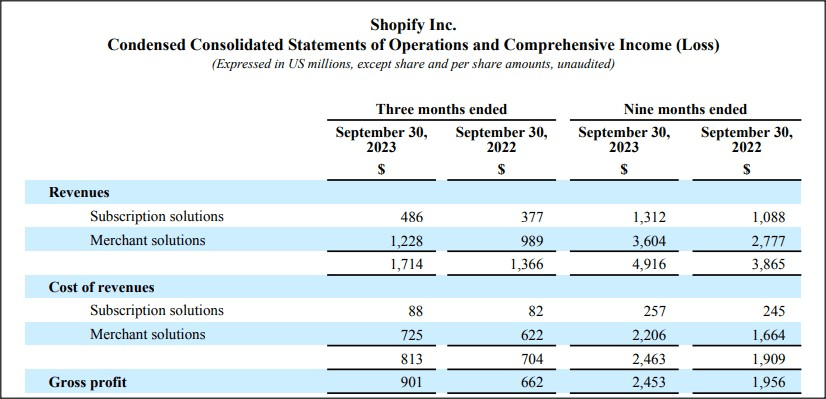

In the second quarter, the company's gross merchandise volume increased 17% to $55.0B, so in terms of GMV, Shopify is seeing an acceleration of its growth. This is due to a growing merchant base but also favorable consumer spending tailwinds as well as moderating inflation. Shopify's total revenues increased a massive 25% year over year to $1.71B due to momentum, especially in the Subscription Solutions business.

Merchant Solution revenues increased 24% year over year to $1,228M compared to a 29% increase in Subscription revenues, resulting in a related segment top line of $486M. In the past, Merchant Solutions was the fastest growing business segment for Shopify and it still generates a 2.5x higher revenue volume than the Subscription business. Subscription revenues soared due to the increase in monthly subscription plan prices in the second quarter as well as a growing number of online merchants using Shopify's online store plans.

{kind=link}

Platform pricing strength translates into FCF margin expansion

Price changes and subscription revenue tailwinds had another important effect on Shopify's financial scorecard: they improved Shopify's free cash flow margins significantly. Shopify generated $276M in free cash flow on revenues of $1.71B which calculates to a free cash flow margin of 16%. This FCF margin expansion has been driven by top-line growth, especially in the subscription business, as well as a decline in operating expenses. In the second quarter, Shopify earned $97 in free cash flow, implying a margin of 6%. In other words, price increases, cost-savings (including lay-offs), and subscription momentum have driven a 10 PP Q/Q increase in Shopify's free cash flow margin.

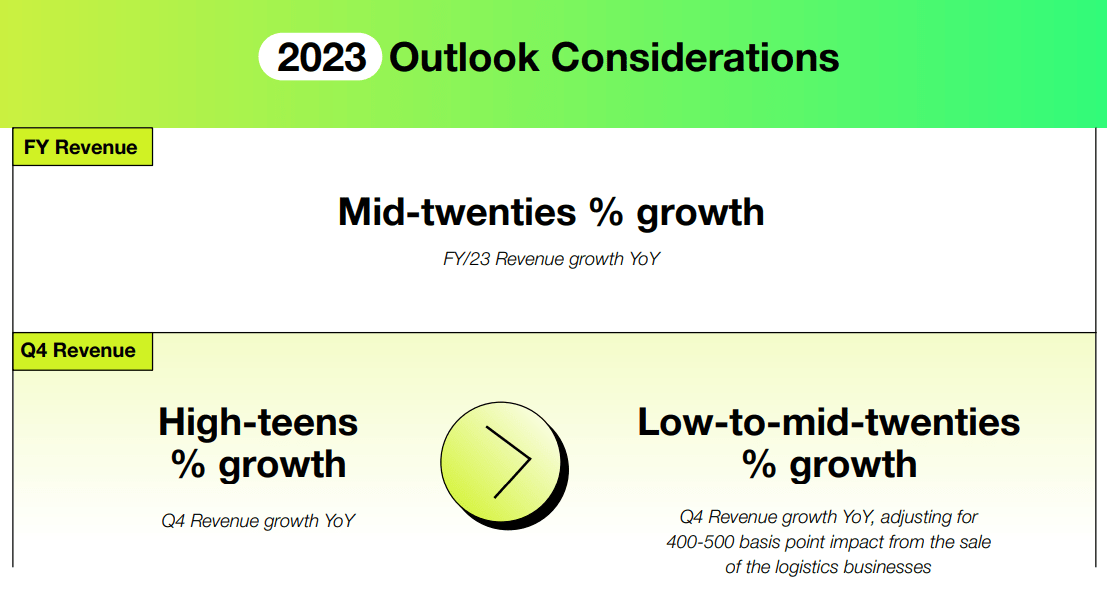

Strong outlook for Q4'23, FY 2023

Shopify expects revenue growth in the mid-twenties percentage in FY 2023, driven by high-teens percentage growth in the fourth quarter. Due to the inclusion of the holiday period, the fourth quarter is typically strong financial quarter for e-commerce companies, including Shopify.

{kind=link}

Shopify's outlook is supported by a surprisingly strong U.S. economy which is favorably affecting consumers' willingness to spend money, not only on Shopify merchant websites, but on e-commerce in general. Amazon also submitted strong guidance for the fourth quarter which assumes up to 12% top-line growth year over year and $160.0B and $167.0B. Both forecasts imply optimistic expectations for the holiday period. Easing inflation is a big help as well and slowing price growth implies that pressure is coming off of the consumer... creating potential tailwinds for consumer spending in Q4'23.

Recent Shopify/Amazon deal, catalyst for subscription growth, improving platform appeal for merchants

Amazon and Shopify, two e-commerce companies that tend to compete against each other, recently struck a stunning collaboration deal that will allow Shopify's U.S. merchants that use Amazon's fulfillment services to offer Prime benefits (such as free and fast shipping) to customers that shop on their websites. This deal was announced in August.

By doing this, Amazon allows third-party sellers outside of the Amazon platform to offer Prime benefits for the first time ever which will give Shopify merchants a considerable competitive advantage. The inclusion of Buy with Prime allows non-Amazon sellers to benefit from the trusted Amazon label which can be expected to lead to higher transaction and order volumes. According to Amazon, the inclusion of the Buy with Prime sticker leads to an increase in store conversions of 25% on average .

The deal makes the Shopify platform significantly more attractive... for merchants. Growth in merchants as well as higher average subscription plan prices will be key to Shopify's top-line growth going forward. The Amazon-Shopify deal should therefore be a boost to subscription revenue growth going forward.

The deal also offers merchants a competitive advantage compared to other online sellers which in itself may boost the Shopify platform appeal. As a result, I would not be surprised to see that Shopify raised its plan prices yet again in the near future.

Shopify's valuation vs. BigCommerce

Shopify is currently expected to grow its revenues by 25% this year and 19% next year, based off on consensus estimates provided by Seeking Alpha, and I would not be surprised if analysts were to raise their revenue expectations as a result of Shopify's FY 2023 outlook.

Shopify, however, has gotten a little bit expensive with shares now trading for 9.4X sales. A rival in the space, BigCommerce ( BIGC ) is trading at 2.1X revenues, but the firm is projected to grow at much lower rates than Shopify. BigCommerce is expected to generate 10% and 13% annual revenue growth this year and next year. BigCommerce is also not as big and has a smaller revenue base than Shopify. In other words, Shopify, from a commercial point of view, is much more established and already reports, as discussed, positive free cash flow.

I believe Shopify deserves to trade at a premium given its large size and strong market position, especially in the retail market. Since shares trade above the 1-year average P/S ratio, I believe SHOP is likely already (more than) fairly valued. I would consider buying Shopify in a range of $45-50, which is where SHOP traded before the well-received Q3'23 earnings release. Such a price range implies a 7.0-7.8X revenue multiplier which is more in line with Shopify's historical P/S ratio of 8.0X. I prefer to buy high-growth stocks like SHOP generally if they are trading at small (10%) discounts to their historical P/S ratios.

Risks with Shopify

Shopify generated $718M in net income in the third quarter, but the e-commerce company is not consistently profitable as the GAAP loss in the first nine months of FY 2023 was $525M. Achieving consistent GAAP profitability would likely be a positive catalyst for shares of Shopify since the company has prioritized growth over profitability in the past. However, if the company failed to achieve consistent GAAP profitability, I would consider this to be a headwind for Shopify as the timeline gets pushed out and investors would have to deal with a higher degree of uncertainty. What would get me to change my mind about Shopify is if it's GMV and top-line growth decelerated.

Final thoughts

Shopify had a strong Q3'23 that resulted in 5 PP sequential GMV growth Q/Q and a boost in subscription revenue growth due to price increases and merchant growth. Shopify submitted an upbeat guidance with FY 2023 top-line growth expected to be ~25% as the firm banks on a strong holiday season. Shopify is executing well overall and I like the business model, but I am retreating from my previous buy recommendation as shares of Shopify seem highly valued on a revenue basis!

For further details see:

Shopify Q3: Strong Growth, But No Bargain