CA - Shopify's Q3 Earnings Beat The Odds: Is The Stock Still Overpriced Or Worth Every Penny?

2023-11-06 08:30:00 ET

Summary

- Shopify's Q3 2023 financial results beat expectations, with revenue of $1.71B and normalized EPS of $0.24.

- After a painful 2022, Shopify is back to profitable growth and robust cash flow generation.

- Despite strong business performance, Shopify's stock is not an ideal buy due to its premium valuation and downside risk.

Introduction

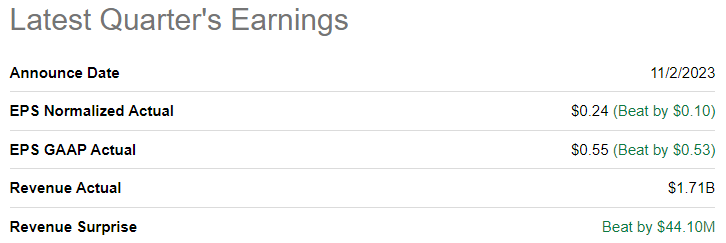

After beating its top and bottom line expectations for Q3 2023 [revenue: $1.71B vs. est. $1.67B, normalized EPS: $0.24 vs. est. $0.14], Shopify Inc. ( SHOP ) stock has jumped up by +22.2% over the last couple of sessions.

{kind=link}

Earlier this year, I rated SHOP stock a "Hold" due to its premium valuation and favored buying Amazon ( AMZN ) as shared in Shopify Vs. Amazon Stock: Heading Into A Potential Recession, Which Is The Better Buy?

With the economy staving off a recession so far, Shopify has delivered robust financial performance throughout 2023 [aided by management's cost-cutting measures], and SHOP stock is now up ~44% from my previous update. While I am kicking myself a little bit for passing on Shopify in early 2023, Amazon's near-identical run-up has eased off the pain.

In today's note, I will provide an update on Shopify's business by analyzing its Q3 2023 financial results. Furthermore, we shall re-examine Shopify's fair value and expected returns to see if SHOP stock is investable at current levels.

Brief Review of Shopify's Q3 2023 Report

As we have discussed in the past, Shopify is a best-of-breed, merchant-focused commerce enablement platform that serves as a centralized operating system for millions of small, medium, and large merchants. Through Shopify, merchants can sell through multiple channels, including direct-to-consumer from the merchant's own website, online marketplaces like Amazon, social media platforms like Facebook ( META ), and even physical stores!

{kind=link}

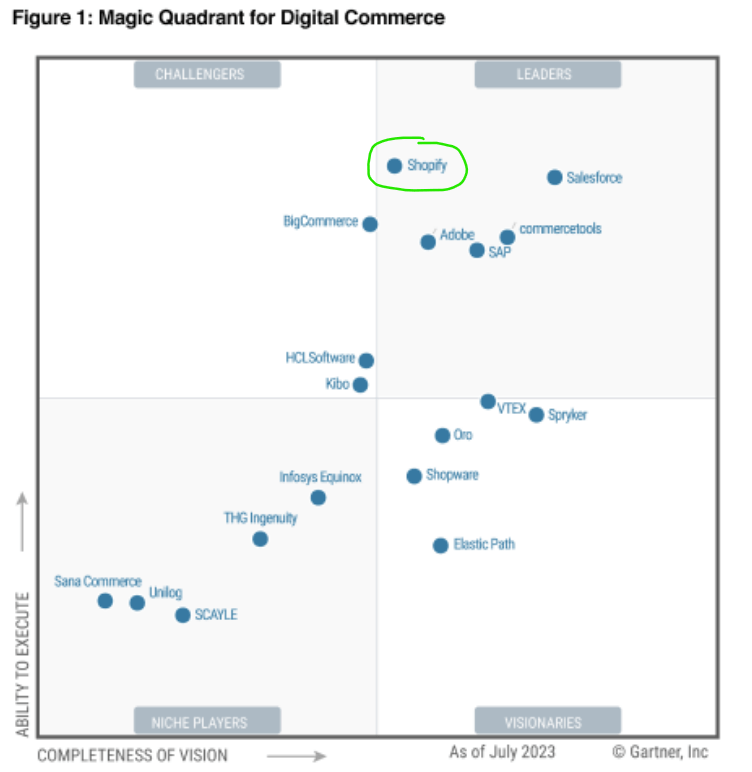

Over the years, Shopify has transformed into an omnichannel commerce enablement platform that allows merchants to sell everywhere their customers like to shop, and it's also a growing presence on the consumer side (through the Shop app). Hence, Shopify being recognized as a "Leader" in Gartner's 2023 Magic Quadrant for Digital Commerce is not at all surprising.

{kind=link}

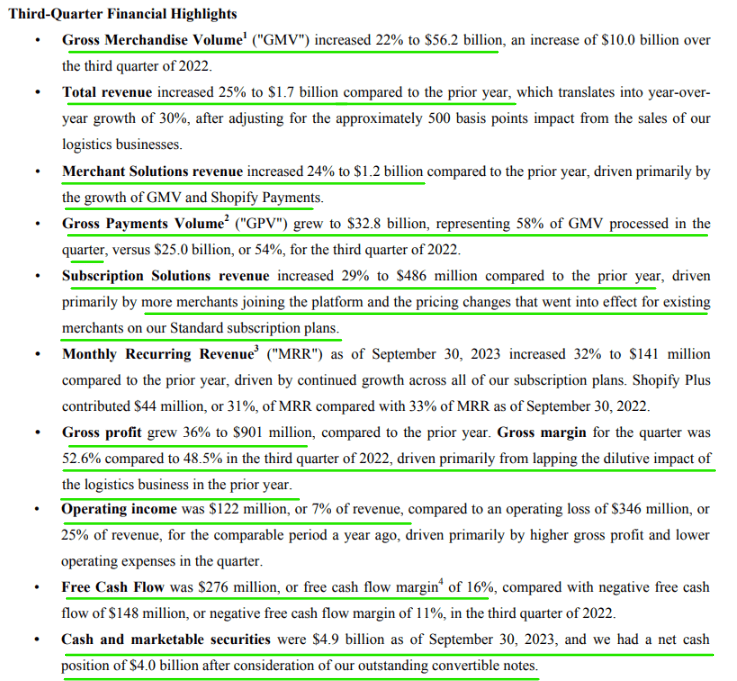

Driven by the strength of its robust ecosystem, Shopify delivered a solid double beat last week for Q3 2023. In the quarter gone by, SHOP's GMV rose 22% y/y to $56.2B on the back of strong new merchant additions and healthy sales growth at existing merchants [amid continued consumer resilience].

Interestingly, Shopify's revenues outpaced GMV growth, rising +25% y/y to $1.7B, powered by higher subscription prices and improved product attach rates. With Shopify's subscription price increases from earlier this year taking full effect in Q3, "Subscription Solutions" segment revenue jumped +29% y/y to $486M. In the "Merchant Solutions" segment, Shopify recorded revenues of $1.2B (up 24% y/y) with strength in GMV and Shopify Payments (GPV: $32.8B, 58% of Q3 2023 GMV [vs. 54% of Q3 2022 GMV]) getting partially offset by Shopify's exit from the logistics business via sale to Flexport . Adjusting for the 500 bps headwind to growth from the sale of its logistics business, Shopify's revenue would have been up 30% y/y in Q3 2023.

{kind=link}

Even in this challenging macroeconomic environment, Shopify was able to raise subscription prices on its Standard plan by 33% with little to no churn, exemplifying the supreme value proposition of its ecosystem. During the earnings call, Shopify's leadership expressed confidence in the price-value ratio of Shopify's platform still being skewed toward value [i.e., more pricing power exists] and name-checked Shopify Plus and Shopify Audiences as monetization opportunities.

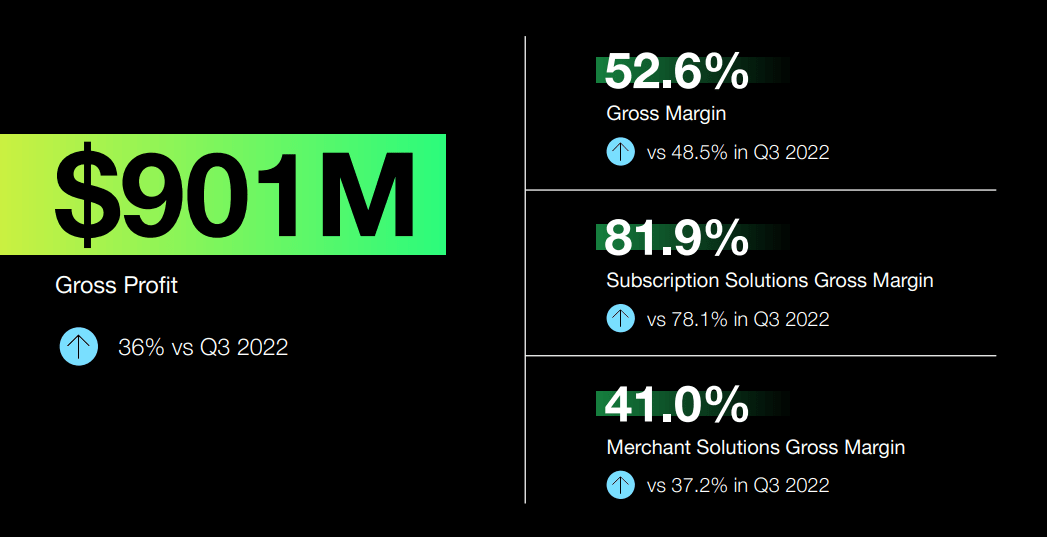

In addition to delivering healthy top-line growth, Shopify is rapidly improving its margin profile driven by management's cost-cutting measures and prudent exit from the logistics business . In Q3, Shopify's gross profit rose to $901M (up +36% y/y) as its gross margin expanded to 52.6%.

{kind=link}

With operating expenses declining by 23% y/y to $779M in Q3 (primarily due to lower headcount [compensation]), Shopify flipped to a positive operating income of $122M (7% of revenue) versus an operating loss of -$346M from a year ago period.

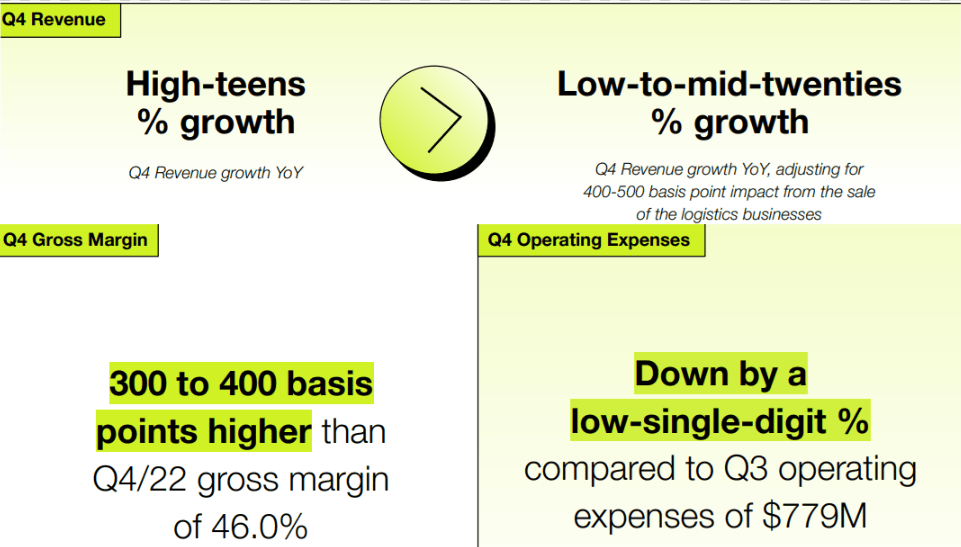

After an excruciating year in 2022, Shopify has returned to profitable growth, and in its new shape, Shopify is now looking like a cash printing machine. In Q3 2023, Shopify generated $276M in free cash flow (16% FCF margin). And these positive business trends are projected to continue in Q4 2023, with the free cash flow margin set to grow to the high teens.

{kind=link}

{kind=link}

While Shopify's management has found some much-needed cost religion, the innovation engine at Shopify is still running at a breakneck pace, with offerings like Shop Pay, Shopify Markets & Markets Pro [cross-border selling solution - powered by Global-e Online ( GLBE )], and Shopify's new one-page checkout set to keep driving healthy growth at the company.

As of Q3 2023, Shopify had a net cash position of $4B on its balance sheet, which is enough firepower to survive any economic downturn that may be headed our way in the upcoming year or two.

Now, as a business Shopify is firing on all cylinders; growing revenues at a healthy clip whilst expanding margins!

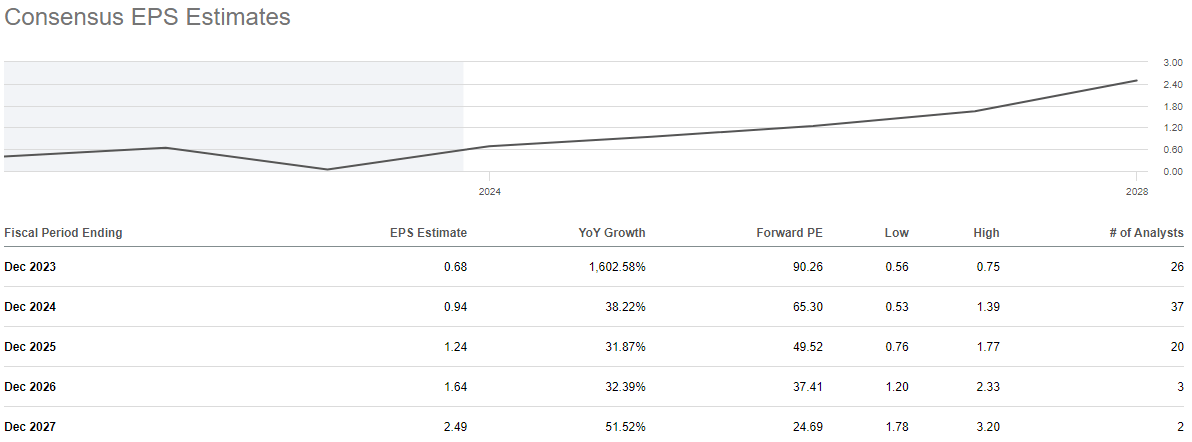

However, is this enough to justify a forward P/E ratio of ~90x?

Let's run Shopify through TQI's Valuation Model to see if SHOP stock is overvalued or worth every penny.

SHOP's Fair Value And Expected Return

Despite suffering a painful post-pandemic normalization, Shopify is still growing at a healthy clip and is projected to keep growing revenues (and earnings) rapidly for many more years to come.

{kind=link}

{kind=link}

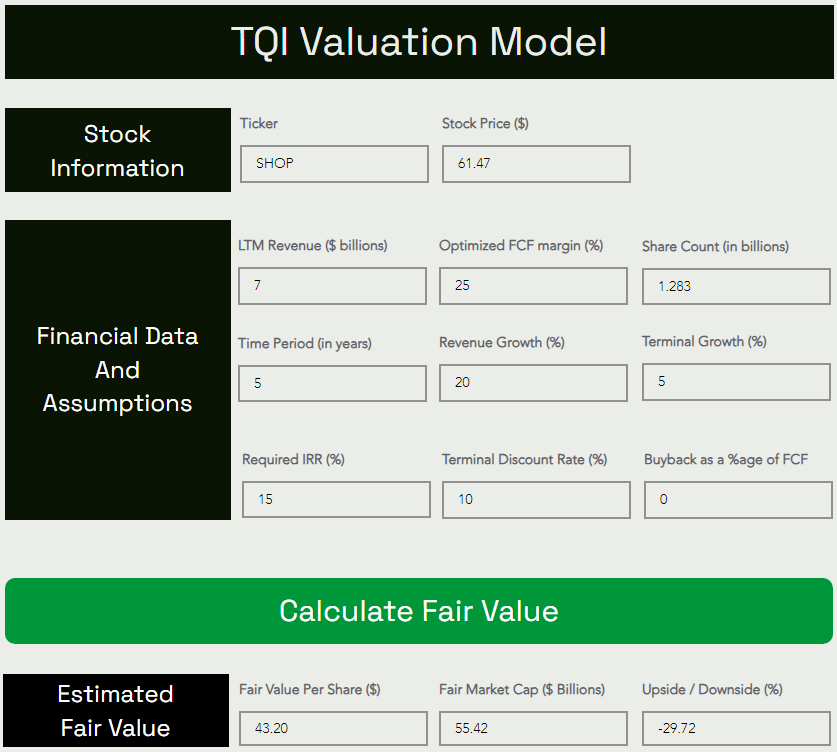

On the back of Shopify getting rid of its own fulfillment network (logistics business) and several cost reductions, the e-commerce giant is showcasing robust margin expansion and operating leverage. Over the long run, I think Shopify will comfortably generate free cash flow margins of ~25-30%, but for my model, I am sticking with an optimized FCF margin assumption of 25% to instill a margin of safety. All the remaining assumptions are pretty straightforward, but let me know if you have any questions in the comments section below.

Here's my updated valuation for Shopify:

{kind=link}

{kind=link}

According to TQI's Valuation Model, Shopify is worth $55B (or $43.20 per share), which means the stock has a downside of ~30% to its fair value. With SHOP's 5-year expected CAGR returns of ~6.66% falling well short of my investment hurdle rate of 15%, Shopify is not an ideal buy at this time.

Concluding Thoughts

At my investing group, we own a 2.1% position in SHOP within our Moonshot-Growth strategy. Shopify's merchant-focused commerce enablement platform is best-in-class, and its moat is getting stronger with each passing quarter.

While I am thoroughly impressed with Shopify's stronger-than-expected Q3 results, the risk/reward for SHOP stock is unattractive at this time due to its premium valuation. Ahead of a potential recession, paying a 30-40% premium for any business is not a wise decision, even for a high-quality company like Shopify. Hence, I suggest staying on the sidelines on SHOP until the risk/reward improves significantly via a price or time correction. If Shopify's 5-year expected CAGR climbs back above 15%, I would happily add more shares to our long position.

Key Takeaway: I rate SHOP "Neutral/Hold" at $61.5 per share.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

For further details see:

Shopify's Q3 Earnings Beat The Odds: Is The Stock Still Overpriced Or Worth Every Penny?