ET - Should Investors Move To Cash Right Now?

2023-03-13 10:45:44 ET

Summary

- Markets have been volatile, initially starting 2023 bullishly before tumbling in response to recent Federal Reserve movements and statements.

- Investors would not be unwise to at least ponder transitioning away from stocks and toward cash.

- This could be rewarding, but it also comes with risks of its own.

- For some investors, this transition may make sense, but for others the best move might be to diversify further.

After a very challenging 2022, a year when the S&P 500 pulled back 19.4%, 2023 started out positively. From the start of the year until Feb. 2, the market rose by 9.3% as optimism built around the possibility that interest rates may not need to go as high as anticipated, and as economic and corporate financial data came in stronger than expected. Recent rhetoric from the Federal Reserve, as well as data suggesting the economy might experience something worse than a soft landing, has now resulted in essentially all of those gains being lost. This is obviously painful for investors. While I generally am not a fan of selling stock and holding cash, the extreme volatility seen in the market may lead some investors, justifiably so, to cash in some of the gains they have and wait for the picture to clear up. This is not necessarily an illogical approach to take. But there are some important factors that investors should consider before making such a bold step.

Yes, the picture could worsen

The biggest macroeconomic issue facing not only the US, but also much of the world, is inflation and the measures being taken to bring it to heel. When it comes to the US specifically, inflation is still quite high. In January, for instance, we saw prices come in 6.4% higher than what they were the same time of the 2022 calendar year. The rate for that month represented the third sequential decline seen in inflation. It's also materially lower than the nearly 9.1% that we peeked at in June of last year. Even so, it's well above the 2% rate that the Federal Reserve has been targeting for the long run.

Because the rate of increases in the interest rate was slowing, and because there were other indications that interest rates might not need to rise so high and last for as long as previously anticipated, the market was initially optimistic. But then, on Tuesday, March 7, Federal Reserve Chairman Jerome Powell, in testimony before senators, stated that, “if the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.” This comes just days before inflation data for the month of February, as well as a subsequent decision by the FOMC regarding whether to increase interest rates by only 0.25% or 0.50%, is due to take place.

{kind=link}

St. Louis Fed

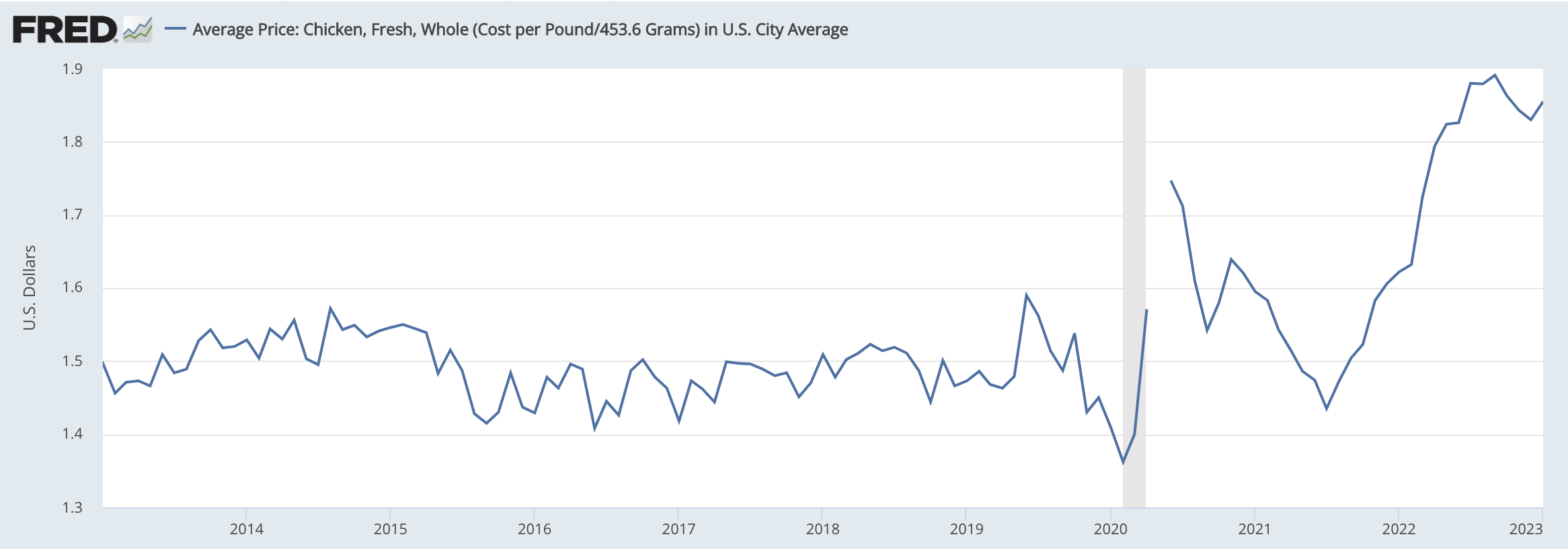

The goal of these interest rate hikes is ultimately to bring inflation down. But it won't be a painless process by any means. In addition to targeting certain spending, as well as investments, the rise in interest rates also is aimed at softening the labor market. With unemployment at multi-decade lows, the argument goes, spending and wages are higher than might otherwise be warranted. In the early days of this inflationary spike, much of the pain was associated with supply chain issues. Along the way, other issues developed. For instance, geopolitical conflict involving Russia and Ukraine has had wide-sweeping consequences across the globe. Energy prices have been most affected. But then there have been other one-off events. Egg prices, for instance, soared 60% in 2022, with a good portion of that rise being driven by a nasty strain of bird flu that resulted in the deaths of 58 million chickens spread across 47 states. Poultry prices, meanwhile, have been showing some improvement, but they were given a big jolt higher in late 2021 in response to a shortage that was, in part, driven by production issues from Tyson Foods ( TSN ).

{kind=link}

St. Louis Fed

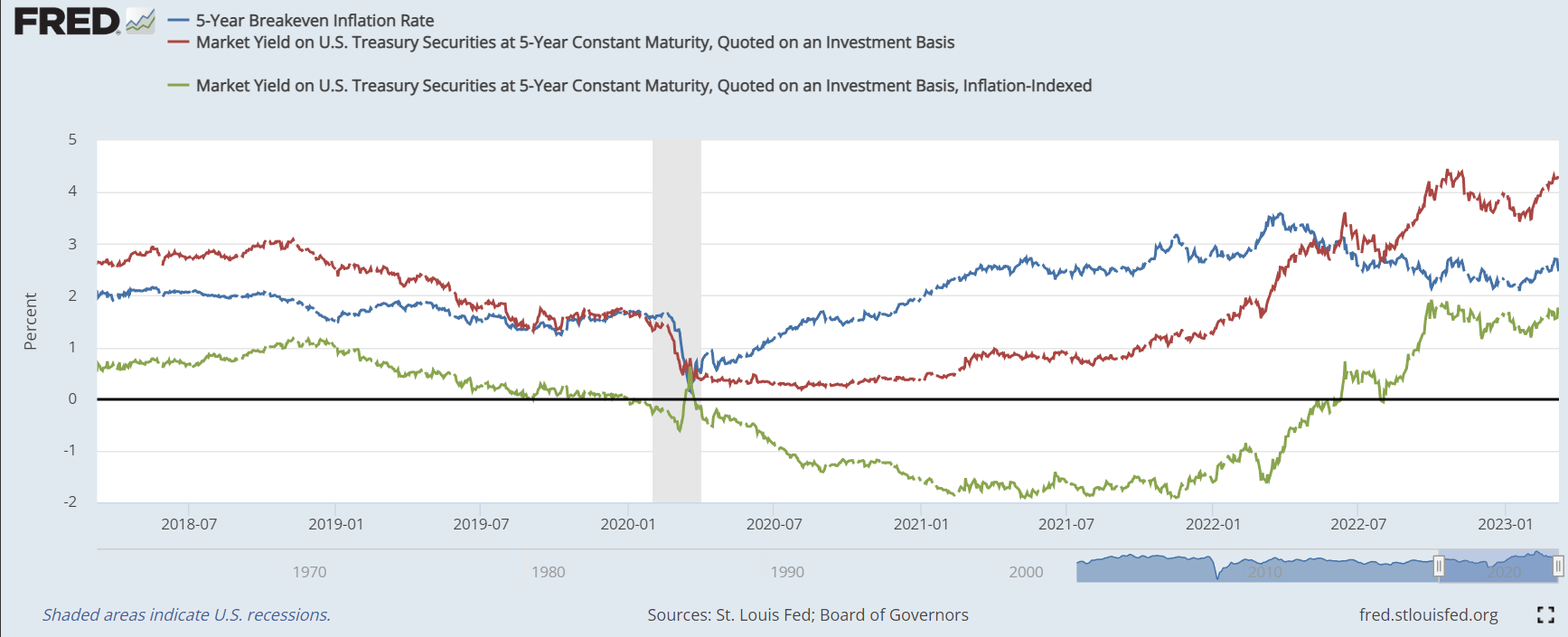

Some of these issues will sort themselves out. But because of the potential pain associated with letting the picture continue, the Federal Reserve is doing all it can to bring inflation down and they are doing it in large part through interest rate increases. One article that I read that was written by fellow Seeking Alpha contributor Colorado Wealth Management Fund made a very interesting point. In discussing yields, he noted that the Federal Reserve is willingly establishing higher interest rates than what the market is even demanding. You can see this in the chart below.

{kind=link}

St. Louis Fed and Colorado Wealth Management Fund

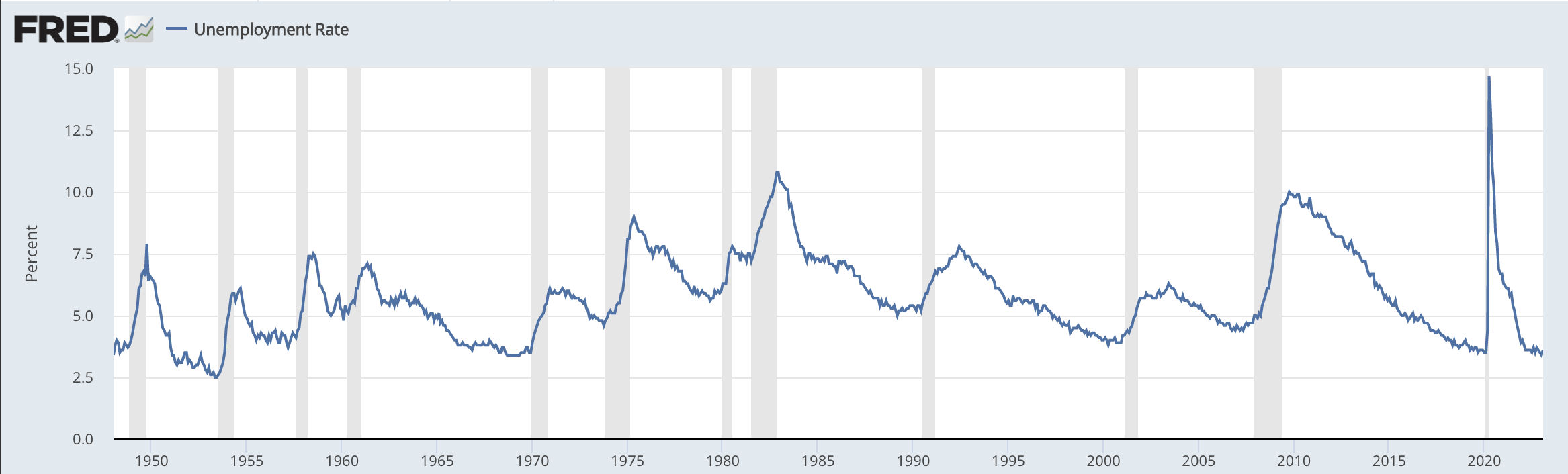

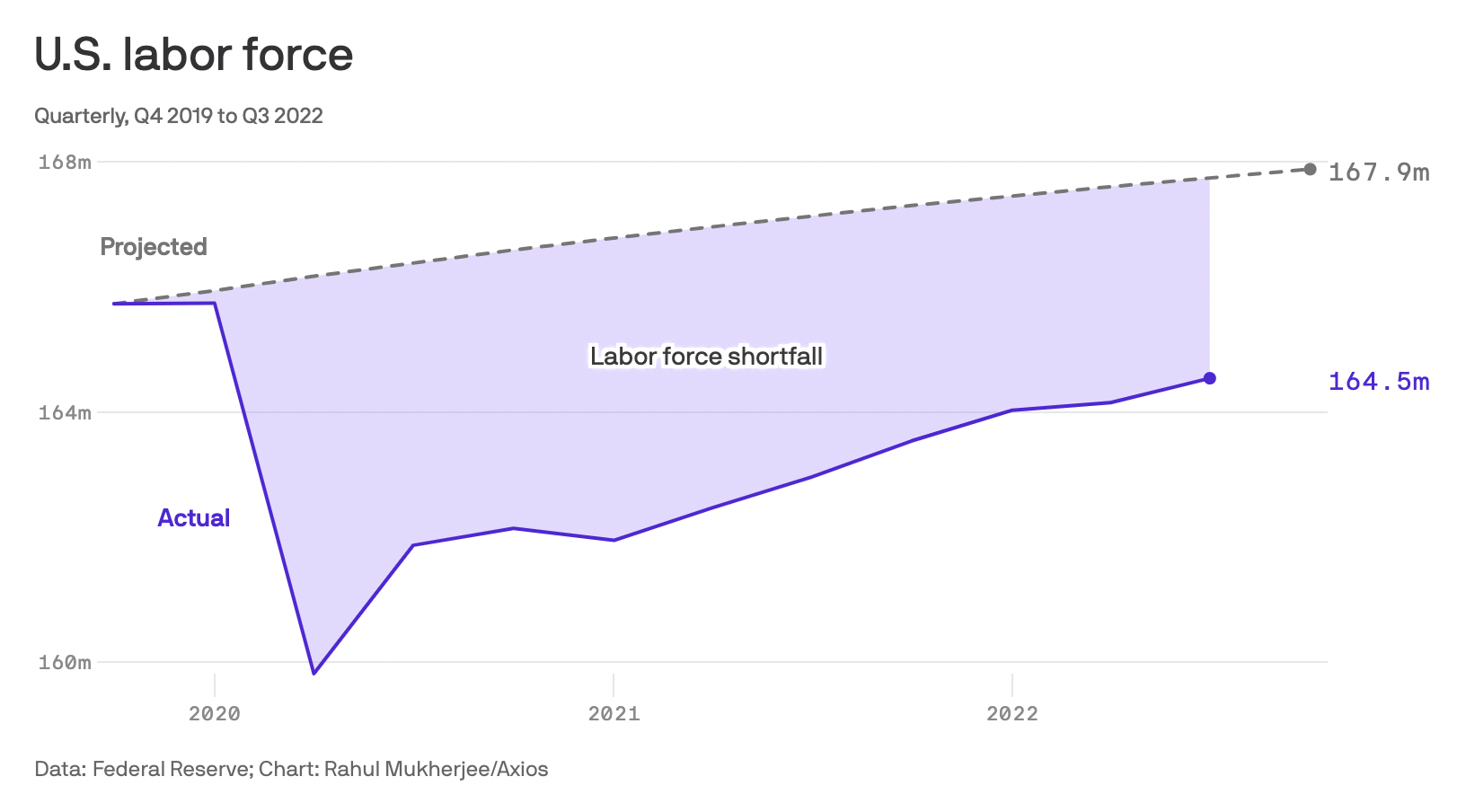

All of that excess is a testament to the effort being made to combat inflationary pressures. But unfortunately, the end result might be a tremendous amount of pain on its own. One estimate suggested that the Federal Reserve’s job might not be done until the US loses as many as 2 million jobs. It's true that we have a tight labor market. Part of this is because of the COVID-19 pandemic. According to an estimate provided by Powell in November of last year, around 400,000 individuals who would have been in the labor force are no longer with us because they died in the pandemic.

{kind=link}

St. Louis Fed and Axios

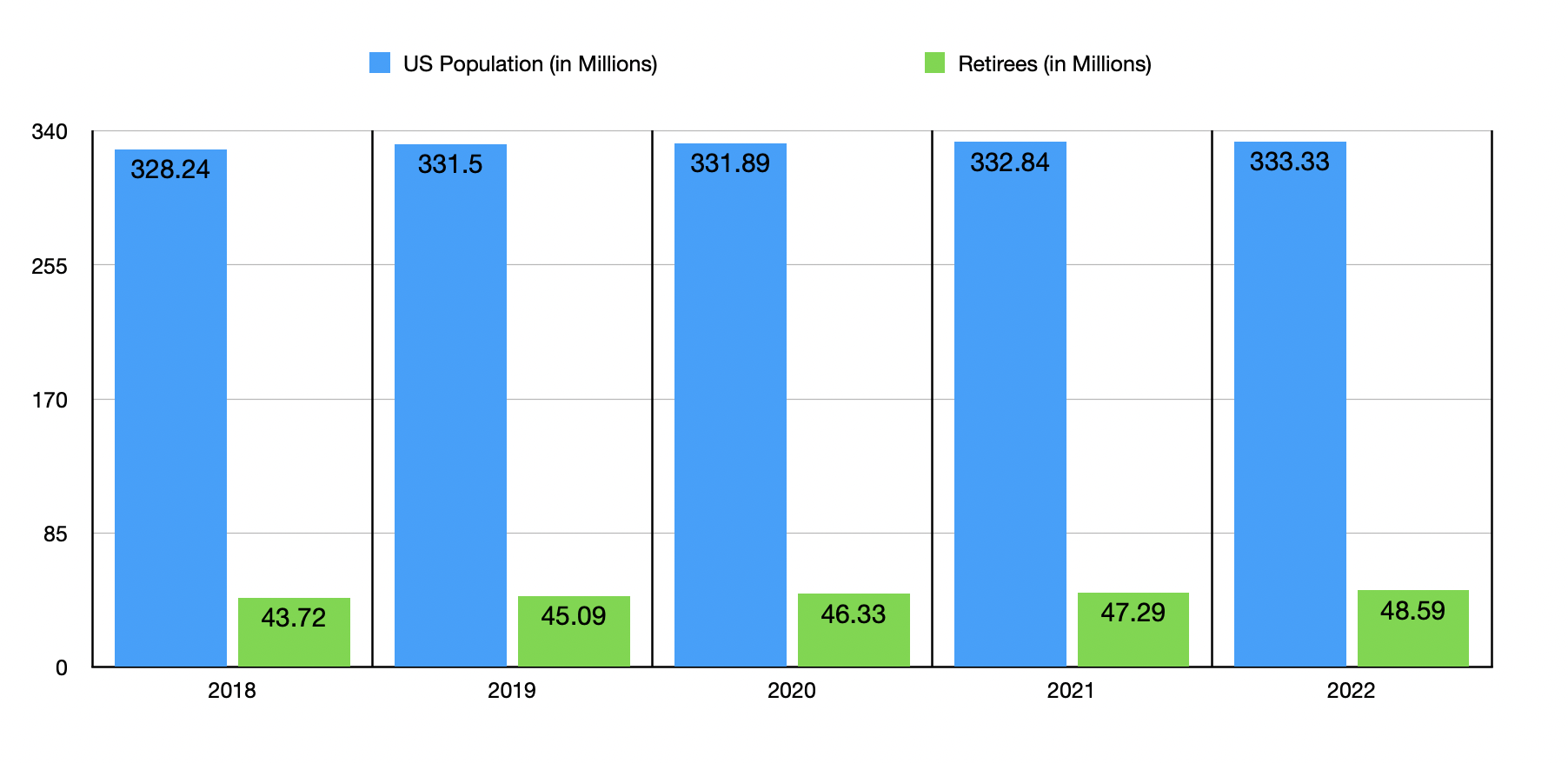

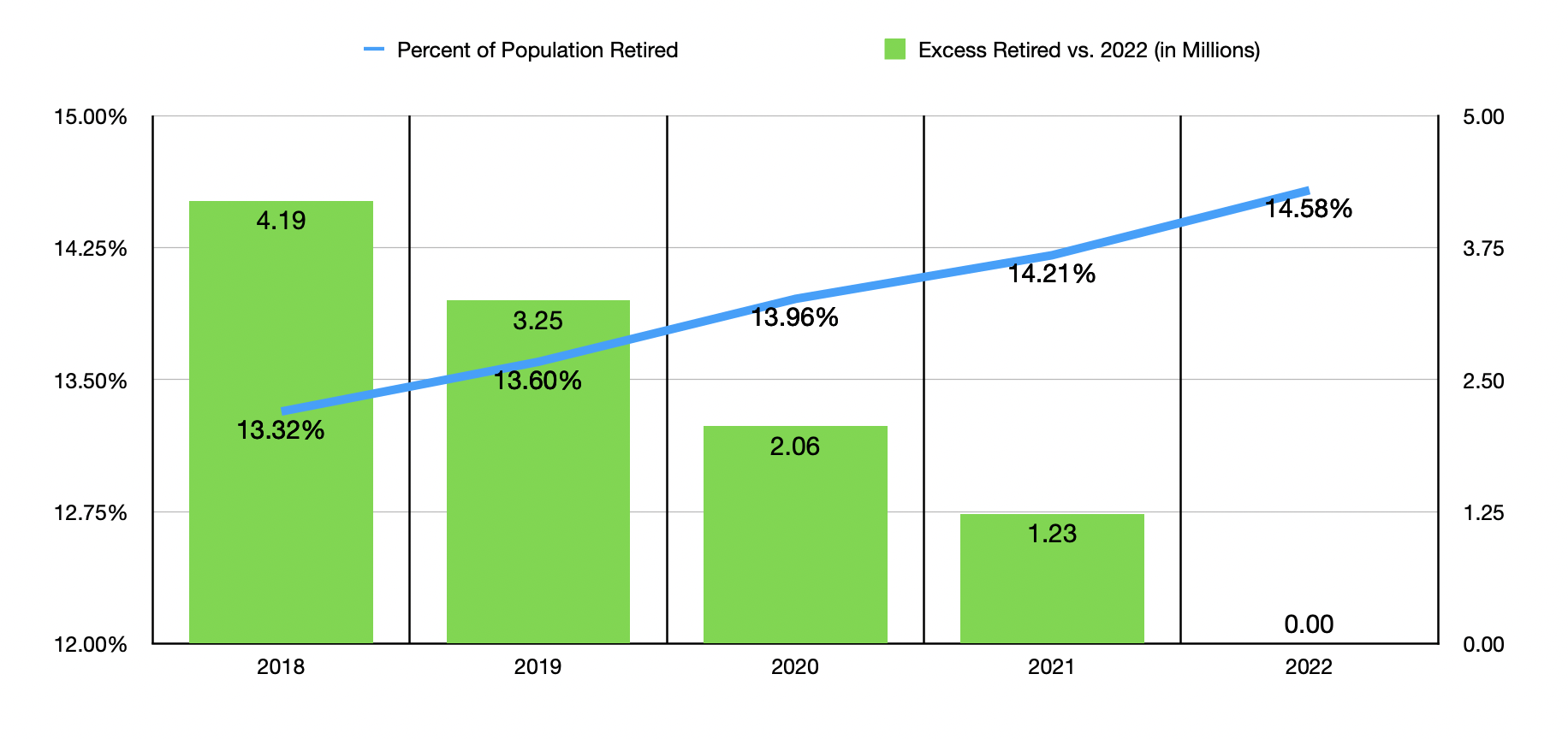

There seems to be a flurry of other issues as well. A paradigm shift occurred because of the pandemic related to remote work that empowered employees to demand a change in how work is done. In addition, a slew of retirees is impacting the picture. In 2022 , there were 48.59 million individuals receiving Social Security retirement benefits. That number is up from 43.72 million in 2018. It's true that the population of the country continues to rise also. So we need to look at this on a percentage basis. Doing this, we see that the percent of Americans who are receiving Social Security retirement benefits has grown from 13.32% to 14.58%. Though this may seem like a small contributor, consider that if we take the difference in percentages from the final year before the pandemic, 2019, and apply that to the population of the US today, it means 3.25 million fewer people in retirement than what we have today.

{kind=link}

Author - Statista

{kind=link}

Author - Multpl

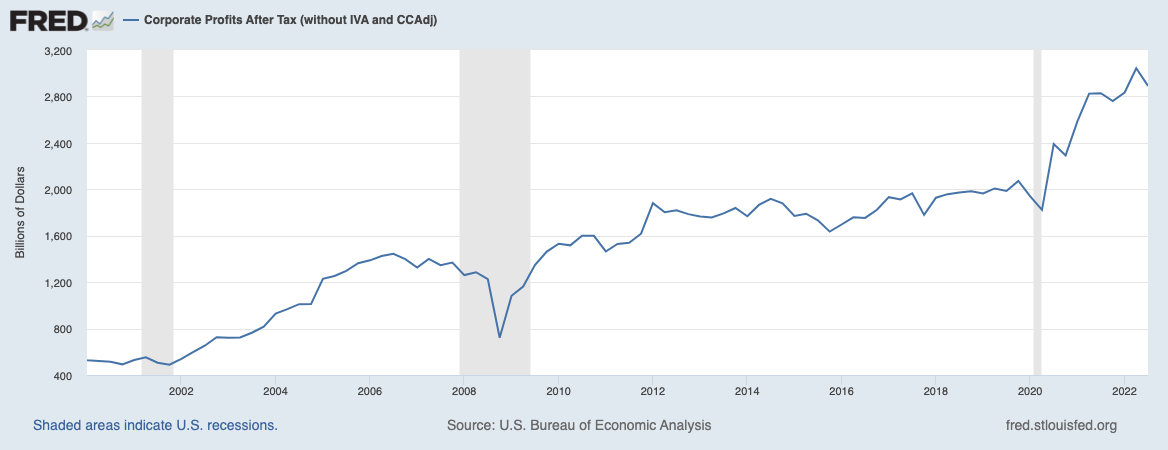

The arduous road that the Federal Reserve seems intent on is all aimed at weakening consumption and weakening investment to the point where the labor force sees a pullback. Some might add to this that a weakening in wages would also be helpful in softening inflationary pressures. With enough effort imposed by the Federal Reserve, this will likely come to pass. However, it does miss the fact that there seems to be another major contributor to inflation there's not being addressed. This is that corporations are, quite frankly, price-gouging customers. This is not true of every business, and there are some industries that are being harmed significantly by current economic conditions. As a whole, the fact that corporate profits are more or less at all-time highs is rather telling.

{kind=link}

St. Louis Fed

This is not to say that the Federal Reserve doesn't want to address that side of the issue. If they had the authority to do so, they likely would. But at the end of the day, they can only do what is legally within their power. Being able to step in and stop the price gouging would likely be an easier way to reduce inflationary pressures. It would almost certainly result in less pain in the long run. But the fact that the Federal Reserve is prevented from doing this should give investors even more cause to wonder whether or not now is the time to cash out and wait for the pain to subside.

Does cashing out make sense?

Cashing out and keeping that cash on reserve for a potential bottom can be incredibly rewarding. As I mentioned already, any investor who would have sold out at the peak this year would have been up about 9.2% compared to being virtually flat from the start of the year. Another lesson in the benefits of moving to cash can be seen when looking at the market's return last year. With the S&P 500 down 19.4% during that time, it would absolutely have been better to cash out at the start of the year unless you picked some excellent stocks that ultimately went on to perform well. Though there aren't any guarantees when it comes to the market, and timing is more art than science, the most recent signals from the Federal Reserve and the economy more broadly due suggest that we could see additional downside from here before we see upside.

Obviously, you can cherry pick other time periods in history where selling your holdings and waiting for the pain to die down would have been profitable. On the other hand, investors should be cautious about market timing in general.

{kind=link}

Author

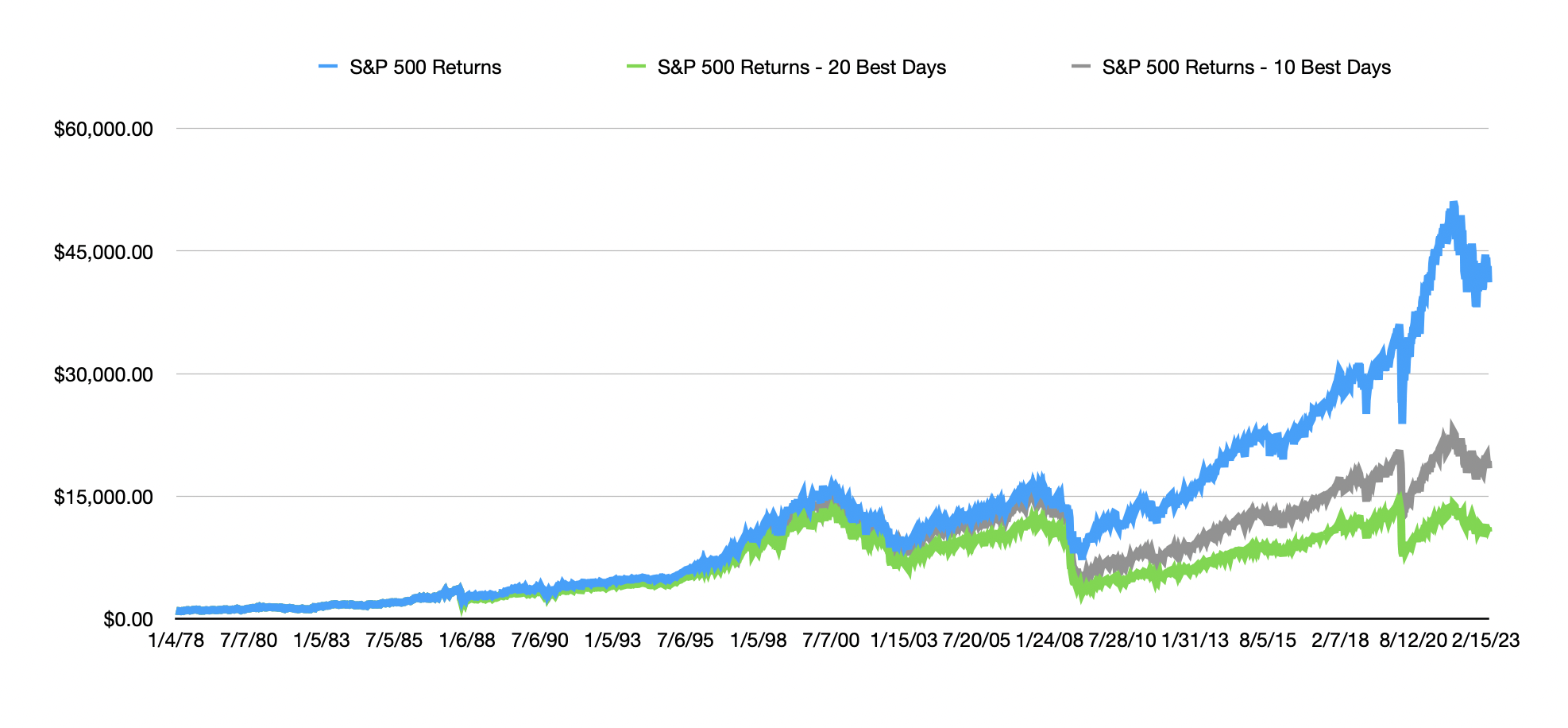

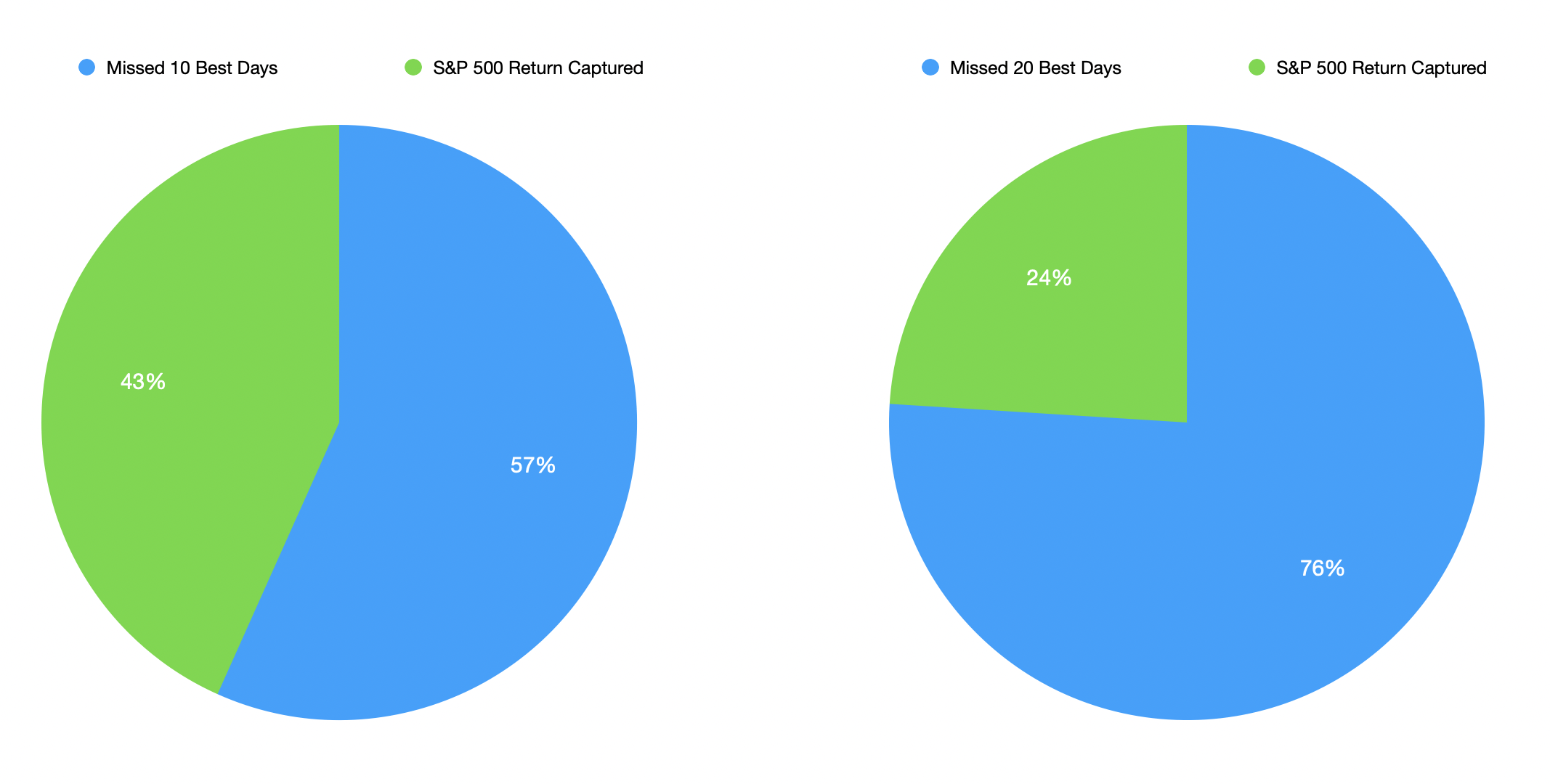

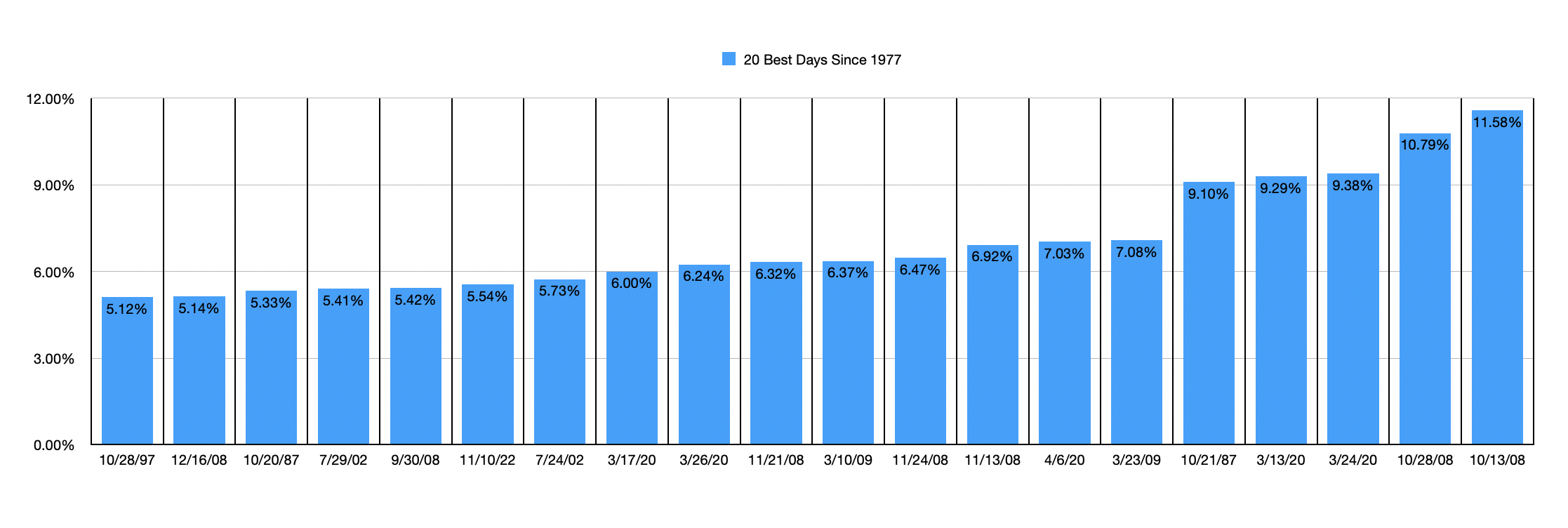

In one analysis I performed, I looked at the total return of the S&P 500 from Jan. 1, 1978, through March 10 of this year. $1,000 invested in the S&P 500 would have turned into $41,159.56 without factoring in anything like taxes, fees, etc... It's also a nominal return, not an inflation-adjusted return. During that time, 11,393 trading days went by. But if you had timed the market and missed out on only the 10 best days, your $1,000 would have turned into only $17,403.62. In this case, you would have missed 56.7% of your upside by missing only a small number of days. Missing the top 20 days would have resulted in your $1,000 turning into only $10,644. In this case, 76% of the upside you would have enjoyed from just holding your stock would have been missed.

{kind=link}

Author

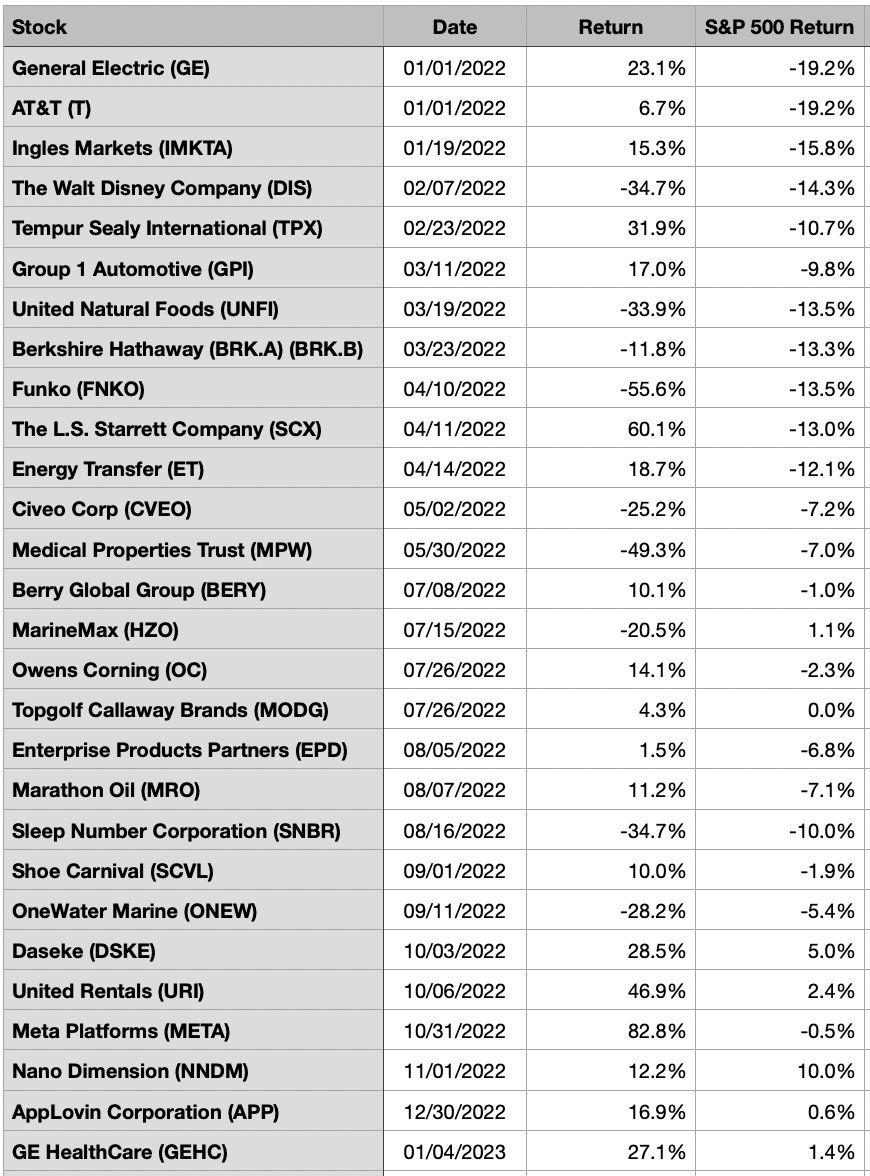

One alternative to this is to concentrate your portfolio by buying into some of the highest-quality, value-oriented companies that you can find. In this case, you might experience some temporary pain. But in the long run, the upside could be material. As an experiment, I looked at all of the companies that I performed an analysis of starting from January of 2022 through today. I looked at the 28 different firms that I assigned a "strong buy" rating to and measured the upside or downside of each one from the latter of A) the start of 2022 and B) when I first rated the company a "strong buy."

{kind=link}

Author

As of this writing, 19 of those 28 holdings generated positive returns, with 20 of those holdings beating the market. Of the holdings that generated market-beating returns, the average return calculated in excess of what the market saw was 27.3%. This doesn't mean that there weren't some losers in the group. The eight companies that underperformed the market had an average downside that was worse than the market by 27.9%. If you had taken the same amount of money for each of the 28 holdings and applied it to them when I announced each company a "strong buy," the end result would have been upside of about 5.2% compared to the 6.9% drop seen by the S&P 500 over the same window of time. The overall delta in favor of my picks was 12.1%. Not bad considering how difficult the market has been. This also illustrates the importance of diversification. Picking the eight holdings that performed worst would have been awfully painful and it would have been better to have just invested in the market instead.

{kind=link}

Author

Am I saying to definitely avoid switching over to cash? Absolutely not. Statistically speaking, over a long enough period of time, it's not a strategy that makes sense for the average investor. But every person has their own unique circumstances. Those who have enough saved up for retirement (or close to enough saved up for it) and who are due to retire in the next few years might be well advised to remove some risk from the market. Individuals who have large expenses coming up and who were investing in order to cover those expenses might also be advised to consider a move toward safety. Examples might be college, the purchase of a home, the purchase of a business, or more. If most or all of your excess capital is invested in stocks and you lack at least three to six months' worth of living expenses that's already stored in cash, you would be wise to take some out of the market. A middle ground to consider would also be bonds/treasuries that you intend to hold to maturity. Of course, yield-to-maturity matters here since you would ideally like to at least capture what inflation is, plus additional upside to account for the risk of said investments.

Takeaway

At this point in time, I understand why investors might be uncertain. The way I see it, we probably are bound for some additional pain in the months ahead. If the Federal Reserve does move forward with significant interest rate hikes with the hopes of breaking the labor market and weakening consumer demand and investment further, the amount of pain that will probably need to be inflicted will be felt across the economy. What makes such a great amount of pain needed is the fact that the labor side of things really isn't even the main problem, nor is it easily fixed. There are real structural reasons why the labor market is tight. We do still have a number of factors, such as geopolitical concerns regarding Russia and Ukraine, as well as one-off events like the avian flu, that are causing inflation as well. Add on top of this the price-gouging from corporations that the Federal Reserve really can't do anything about, but Congress and the Biden Administration could, and it's clear that the Federal Reserve is being forced to solve a multifaceted problem by only targeting a couple of its facets.

In response to this, investors would not necessarily be making a bad decision by putting some cash to the side. In the past couple of weeks, I have been tempted to do so, but I have resisted that urge up to now. A meaningful pullback in the market could then lead to a golden opportunity for investors to benefit from. But at the same time, this comes with risks of its own. As I demonstrated, missing even a handful of some of the strongest returns over a span of 45 years can lead to significantly reduced upside in the long run. For those who feel like market timing is not an ideal solution, picking a diverse portfolio of high-quality companies that are value oriented may actually be the best path in the long run. For now, that's the path I am walking. But that could change based on what additional developments arise.

For further details see:

Should Investors Move To Cash Right Now?