CA - Silvercorp: Precious Metals Miners May Become Our New Central Banks

2023-03-28 22:50:09 ET

Summary

- As was the case with the 2008 financial crisis, it is nearly impossible to have a clear understanding currently of the potential for catastrophe engulfing the entire global financial system.

- The next few months might be crucial in the way that the current banking turbulence, and our response to it will shape the future of global finance.

- Silvercorp stock might be one of the most undervalued investment opportunities that can act as a hedge against the possibility of the Western or possibly the global financial system imploding.

- Silvercorp's financial fundamentals are solid, while its outlook is potentially very bright, together with the outlook for silver.

Investment thesis

Silvercorp ( SVM ) together with silver, gold, and other commodities miners may be on the verge of entering a new era in terms of their role in the global economy. What they produce is generally thought of as mostly raw materials that play an increasingly diminished role as an input into the global economy, given the growing trend towards the service economy, which is far less commodities-intensive. We may be seeing the beginning of a change, where precious metals as well as other commodities may begin to play a growing role in providing tangible asset backing for increasingly unstable fiat currency systems around the world. Silvercorp has a proven track record of being a profitable silver producer, and it has a decent history of reserve replacement, which makes it an attractive investment choice if one wants to hedge against the arguably increasingly wobbly pure fiat currency system in place for much of the post-WW2 era. Read my previous coverage on SVM stock here.

Silvercorp proves it can be profitable at mining at current silver price levels

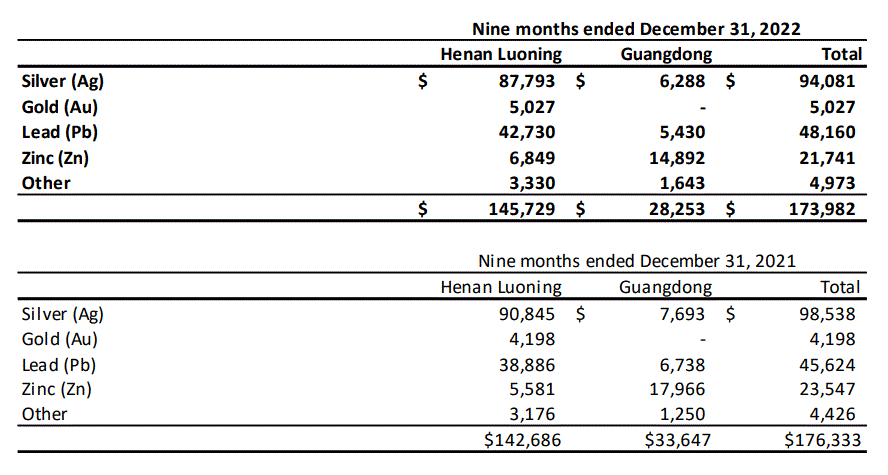

For the first nine months of its fiscal year, ending on the last day of December, Silvercorp realized $174 million dollars in revenue and $18.8 million in net income. Net income is barely half of what it was in the first nine months of fiscal 2021, while revenue remained mostly steady for the same period. It is a reflection of lower silver prices in 2022 compared with 2021.

{kind=link}

As far as the source of income in terms of mined metals, silver does make up more than half of all revenues, making it a true silver investment play. There is a bit of a gold angle to this investment as well, but it is minimal. Lead & Zinc are to some extent a hedge that could potentially counterbalance Silvercorp's status as a precious metals miner.

{kind=link}

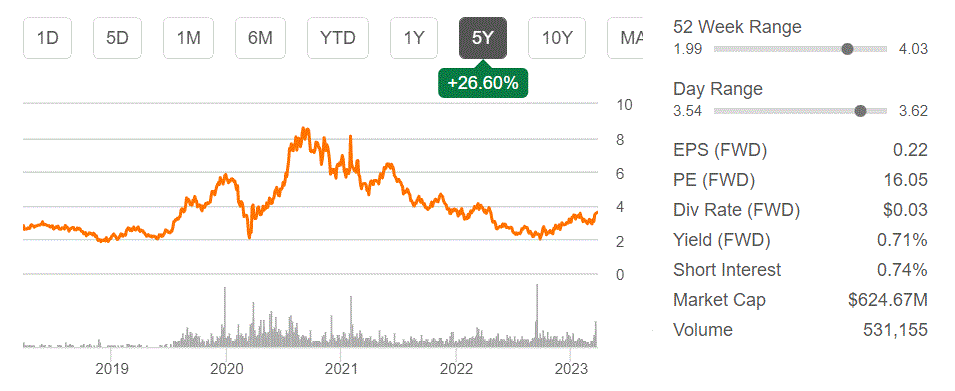

With a forward P/E of 16, it looks to be on the expensive side as a miner in general and about where one would expect it to be in comparison with other precious metals miners like Barrick ( GOLD ) for instance, which currently trades at a forward P/E ratio of about 22. Based on the trajectory of the financial results we are seeing, with net earnings down compared with the previous year, as well as a valuation that is arguably already where one would expect it to be, there is only one investment thesis that provides for a buying argument and that is the expectation that silver prices are set to enter a sustained bull market in the near future.

The global financial system is unraveling and the main Western central banks seem to be near a checkmate situation

Another Zoltan, a Zoltan Pozsar , with far more pedigree in the world of global finance than yours truly, has been floating the idea of commodities-backed currencies gradually taking over from the USD-dominated global FX system. I happen to agree with him, not just because we share a great name, but because I fail to see any other way out of the global financial predicament we find ourselves in.

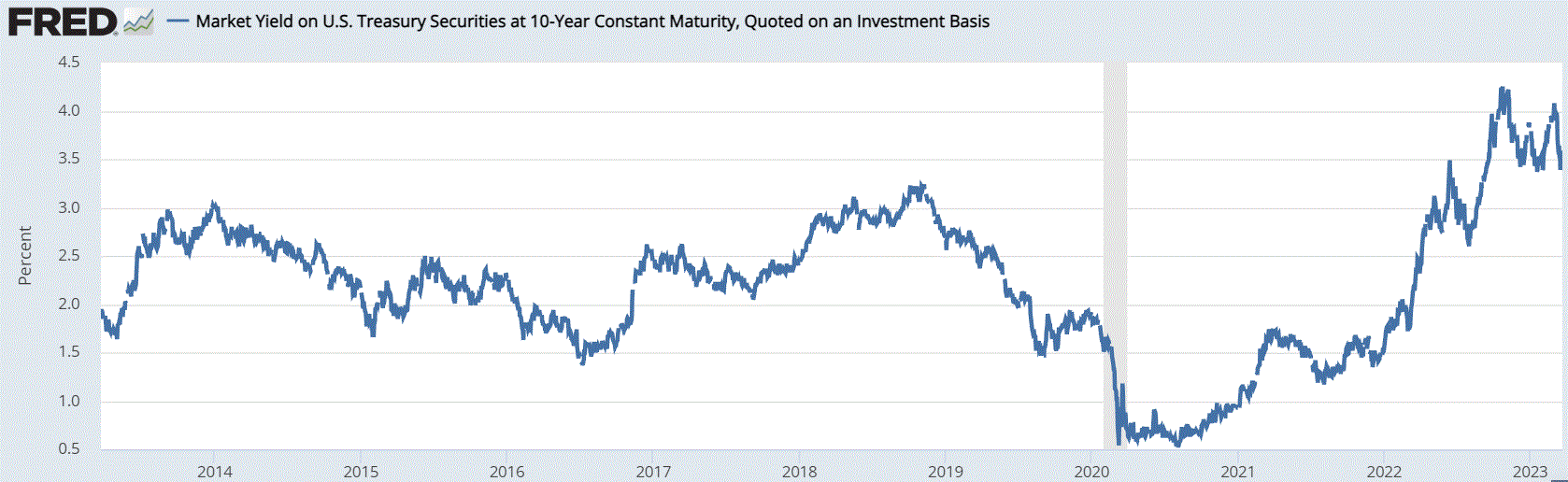

The SVB failure exposed a severe problem with the current efforts to fight inflation, after over a decade of very low-interest rates filled balance sheets with low-yielding debt, ranging from government bonds to mortgages and car loans.

{kind=link}

Because interest rates have risen so fast in the past two years or so, old debt that is still waiting to mature that was issued between 2009-2021 is losing its base value. In other words, $1 million in US 10-year bonds issued in 2020 may have a yearly yield of just .5%, while freshly issued 10-year bonds today may yield about 3.5%. Because of this, if an institution has such assets on the books, it may lose about 20% of the basis value if it had to liquidate into the current market. As a result that $1 million in assets on their books becomes $800k.

{kind=link}

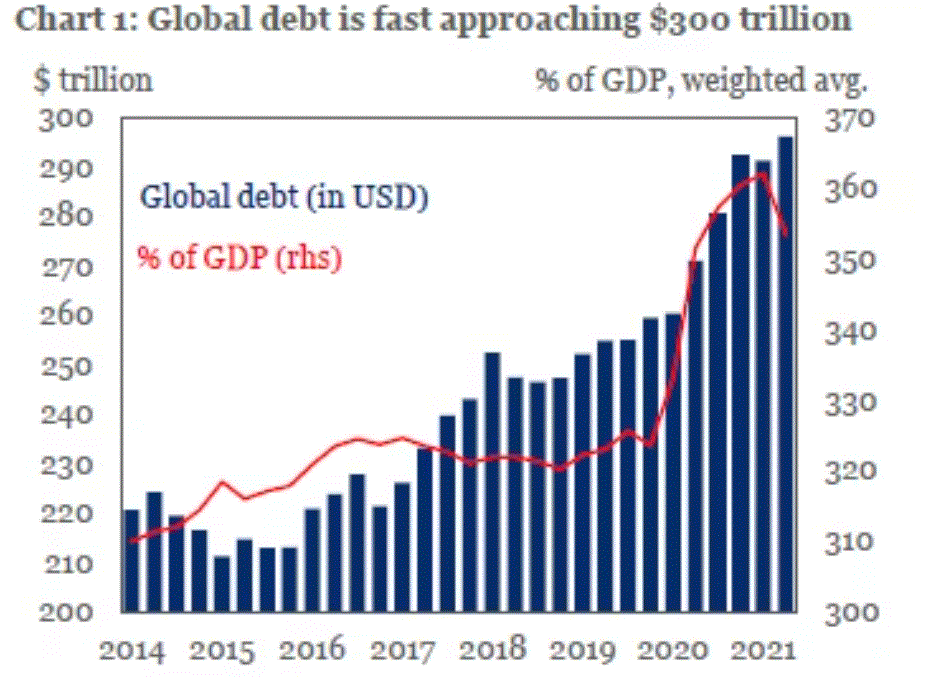

Taking the small-scale example and applying it to total global debt and assuming a similar 20% or so decline in the real market value of the debt that is currently on the books of global financial institutions as well as other entities, we are looking at tens of trillions of dollars in potential losses if everyone were to be forced to liquidate their debt assets.

This problem is set to last for many more years to come until most of the debt issued between 2009 and 2021 reaches maturity and gets replaced by newly issued debt at the current higher interest rates. If at any point between now and the time when we will flush the old low-yielding debt out of the system, there is a crisis that will lead to a debt-liquidation frenzy in order to cover losses or in order to raise cash for any other reason, the global financial system could potentially collapse.

There is a partial market consensus building in regard to the growing banking volatility we are seeing acting as an impediment to the efforts of central banks to rein in inflation. The problem with that market assumption is that some of the inflationary pressures are not dissipating, even though the global economic slowdown we are seeing is traditionally seen as a deflationary mechanism. One of the main problems seems to be geopolitical. Growing trade frictions with China, the world's factory is inflationary, since it disrupts the coordinated global flow of manufactured goods, including intermediary goods that are needed across the world in order to produce finished goods. The other is the continued economic war on Russia, the world's largest net exporter of commodities, ranging from food & fertilizers to oil, gas, and palladium. The confrontation with Russia comes at a time when there seems to be an already occurring global commodities bull market, that is independent of the Russia effect.

As long as these frictions will continue, inflationary pressures on the global economic system will persist. This in turn leaves central banks in a bind. They can either fight inflation and hurt financial institutions in the process, or they can choose to save the banks, while inflationary pressures will likely take on a life of their own at some point and cause potentially unforeseen problems not only for banks but for the economy. It is not an enviable position for the stewards of monetary policy.

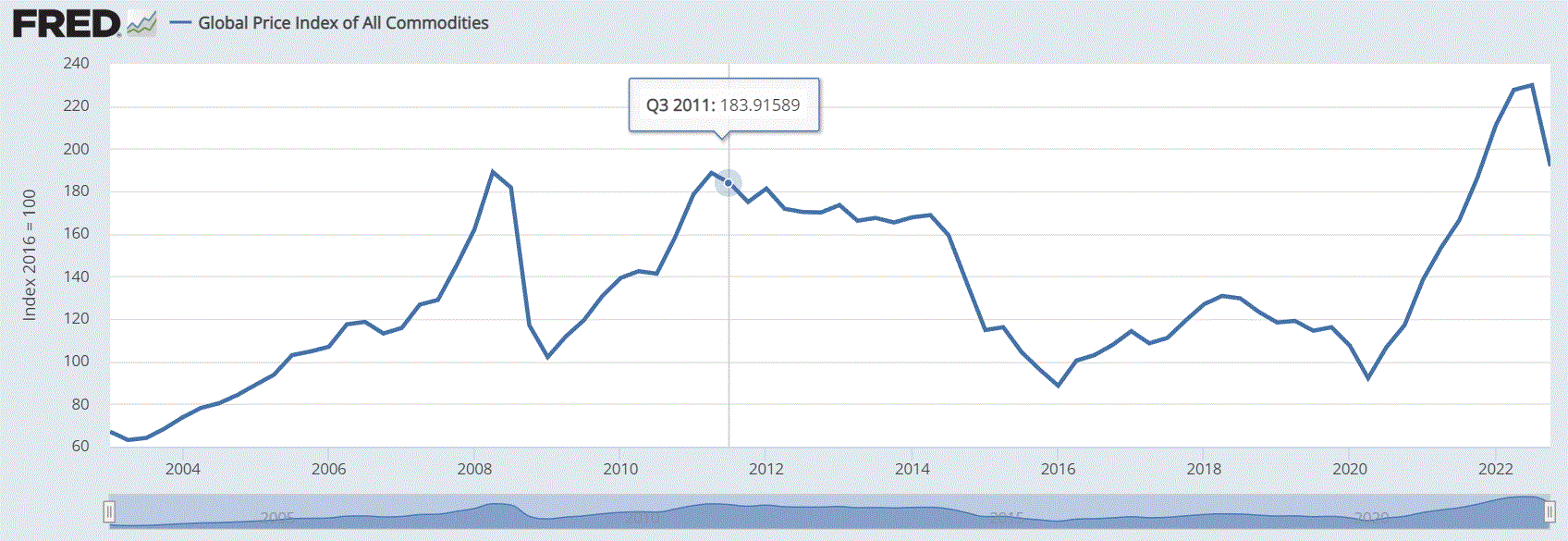

It should be noted that even though we are set to experience perhaps the fourth or fifth-worst year in terms of global economic growth so far this century, global commodities prices are still holding up pretty well.

{kind=link}

Even though the global average price of all commodities is coming down, as of the last quarter of last year we were still at a higher price point than we were during the two previous price spikes shown on the chart. This is an important factor that we need to be mindful of because it is arguably a sign of inflationary pressures stemming from foundational inputs in the economy. It makes it very hard to try to control inflation, without crashing the economy in order to relieve commodities demand. And given how well commodities prices are holding up, despite the economic deceleration we have seen in many major economies, it seems that it will take a significant reduction in demand in order to break the current commodities bull market. In the absence of far more extracted supplies flooding the market, any recessionary-induced break in the current commodities bull market will likely only last as long as the recession will.

Silver has the potential to become a fiat currency backstop asset

One of the under-reported stories of last year has been the effect that Russia's decision to start demanding ruble payments for some of its natural gas exports has had on its efforts to stabilize the ruble in the face of the economic and financial blitzkrieg that the Western World inflicted on Russia last year. In effect, the ruble gained commodity-backing to some extent. Buyers of natural gas from Russia were obliged to start buying rubles in order to be able to purchase gas, thus enhancing external ruble demand. The lesson will probably not be lost on most other net commodities exporters going forward. Mexico for instance could use silver exports much the same way as Russia used gas to provide some backing to the peso if it were to be under significant market pressure.

Countries that do not have the resources to become net exporters of crucial commodities can opt to stockpile commodities as a way to back their currencies with something that is tangible and it is in demand. In this regard, silver stands out as a potentially very attractive long-term investment choice for state actors. It is a precious metal, which can be easily stored and transported. At the same time, it has growing industrial applications demand going in its favor as a means of amplifying its scarcity. As I pointed out in an article I wrote some years ago, which still tends to receive periodic flare-ups of reader interest, there is arguably not enough silver on this planet to facilitate a world that would hypothetically be powered exclusively by solar energy.

Considering all the other industrial applications for silver that are pushing demand higher, in my personal view silver has a distinct long-term advantage over gold, due to its dual-use aspects. Gold tends to have a long-term price floor in the form of marginal mining costs. Silver has that, as well as a secondary price floor due to its growing use in a variety of important industrial applications. Lower silver prices should in theory stimulate the growing adoption of silver used in a number of industries, thus providing an extra layer of price stability for the long term. It may be an aspect that may make silver a winner as a tangible asset used to back fiat currencies around the world.

Investment implications

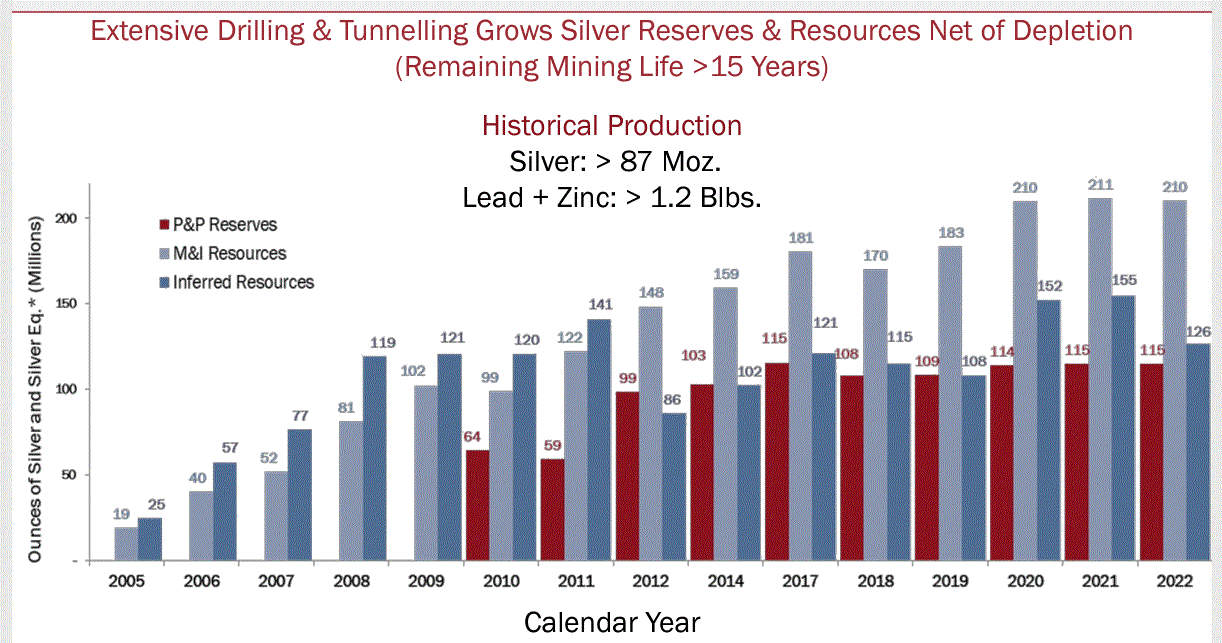

Silvercorp stock has a lot of potential within the wider global economic and geopolitical context we see evolving before us this decade. It is producing silver and other minerals at a profit, while its reserve situation has been evolving in a positive direction in past years.

{kind=link}

With the company fundamentals looking solid, it makes for a good long-term potential investment play if one holds to the view that our global financial system is increasingly in trouble and becoming more unstable. I own a relatively small stake in SVM stock, as part of my overall portfolio. I intend to use any significant pullbacks from current price levels to add to my position unless new information will come along in the meantime that will change my mind.

For further details see:

Silvercorp: Precious Metals Miners May Become Our New Central Banks