SILV - SilverCrest: An Excellent Way To Play The Silver Bull Market

Summary

- Investors are not buying the recent move in silver, still licking their wounds from the underperformance of miners over the last year.

- SilverCrest Metals is one of the top names in the sector, set to become one of the highest-grade, lowest-cost silver producers in the world.

- SilverCrest is still undervalued given its considerable free cash flow generation potential.

- With a track record of operational excellence, exploration upside, and the wind turning again in favor of precious metals, I see SilverCrest as a buying opportunity at the current $6.5 price.

The precious metals bull market appears to have resumed in strength. Silver, in particular, has risen almost 30% over the last 6 months (despite underperforming gold more recently). I turned bullish on silver at the beginning of September and took the opportunity to load up on dirt-cheap silver miners, like Silvercorp Metals Inc. ( SVM , SVM:CA ) and SilverCrest Metals Inc. ( SILV , SIL:CA ). While Silvercorp has enjoyed a 50% return over the period, SilverCrest has lagged in comparison.

There seems to be a lack of excitement about the stock, which is unjustified considering that SilverCrest has just started commercial production (after completing construction on schedule and on budget), and is set to become one of the world's highest-grade, lowest-cost silver producers. The economics of its Las Chispas project are among the most robust in the sector, with the potential to turn SilverCrest into a veritable cash machine if the company keeps delivering. With a track record of operational excellence, considerable exploration potential, and the wind turning again in favor of precious metals, I see SilverCrest at its current price of around $6.5 as a buying opportunity.

Silver outlook

There is probably still considerable upside on the horizon for both the physical metal and the miners, even after the recent run-up. Of course, nothing goes straight up, and a correction in the silver price is definitely in the cards at the moment (especially considering recent dollar weakness, which I speculate is going to reverse soon). However, the medium- and long-term fundamentals remain extremely robust.

The Fed has proven more hawkish than I expected at the beginning of 2022; however, much of the move in rates appears to be past us, with the terminal rate probably ending up around 5%. By the middle of 2023, the Fed is likely to pause. The market is sensing that the wind of monetary policy is turning and that further rate hikes are unlikely, given the excessive strain they would put on the currently over-indebted financial system. This explains the recent moves in gold and silver.

I discussed in a separate article my long-term expectations about how gold and silver might behave over the next few years. Inflation has likely peaked, but the level to which it is going to relax will be significantly higher than over the last decade. At the same time, nominal interest rates will keep lagging inflation, so real interest rates will be kept in negative territory. This deliberate policy of financial repression is made necessary by the high debt-to-GDP levels of most of the developed world and is extremely supportive for precious metals prices.

From a sentiment point of view, it appears that many gold and silver bugs are still not buying the recent leg up. While based on anecdotal evidence, I believe many investors sold in disgust at the lows last year, and are now waiting on the sidelines for a better entry point (which may not come). I also believe that being contrarian is fundamental to thrive in this sector. Could it be that, this time, the contrarian positioning is actually to be bullish, and the trend is higher? If the recent move is confirmed, could we see a true runaway of the silver price back to $28? What will happen then to the miners?

Not only the wind of monetary policy is turning, but other forces are reversing their effects. Energy prices have decreased, and inflationary pressures are abating, at the same time that the metal is beginning to run again. Margins are going to expand from the razor-thin levels of last year, and the tough year-over-year comparisons with 2021 are also gone. Money will be flowing into the sector. Given how short the list of investable silver producers is, and how small their combined market capitalizations are, prices might gap higher in a matter of weeks.

Under similar circumstances, my approach is typically to buy the highest quality names (before the move becomes obvious). Such names might have less torque than lower-quality names but, if the move does happen, the upside is still considerable, and otherwise, the downside is protected. This brings us back to the topic of SilverCrest.

SilverCrest Metals

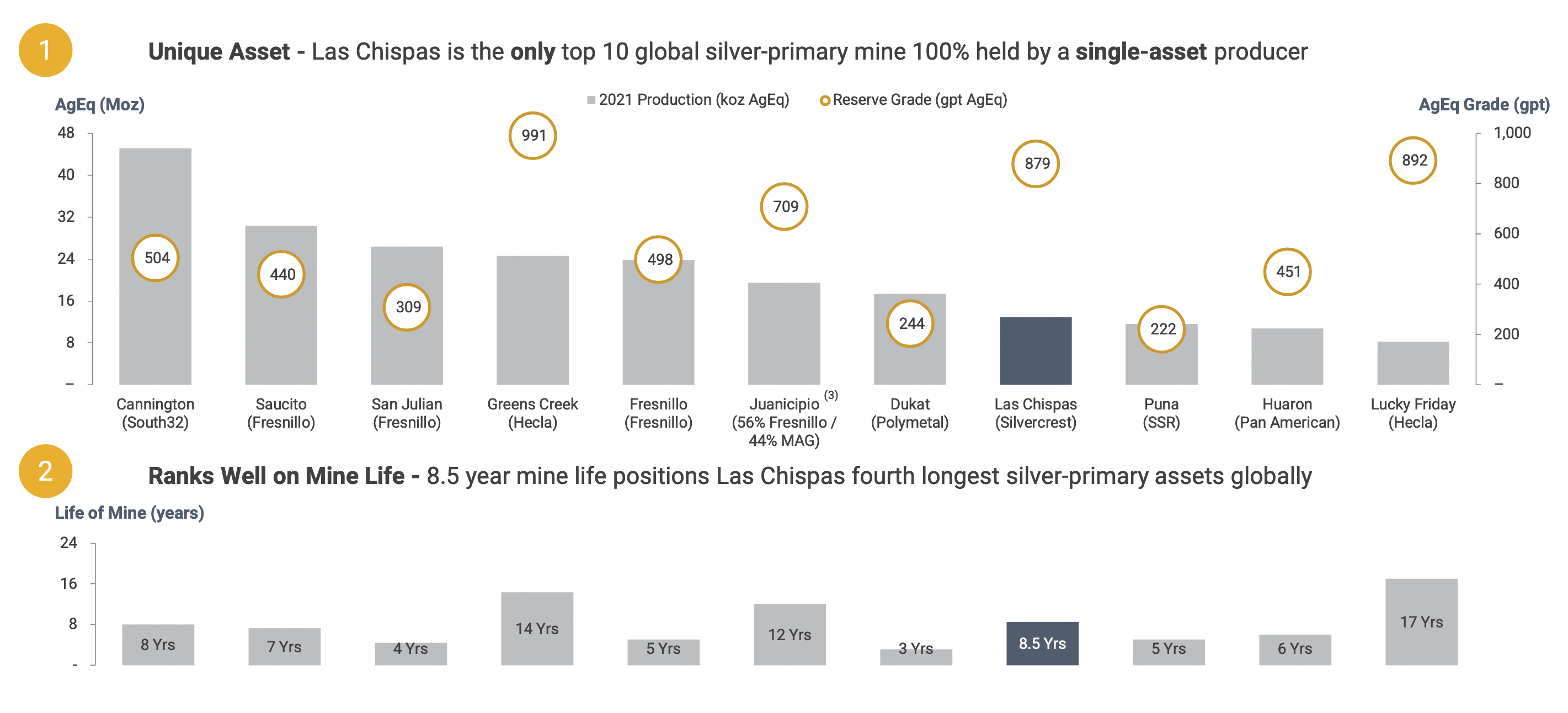

SilverCrest Metals is a junior Canadian single-asset silver producer with operations in Mexico. Its Las Chispas mine is a one-of-a-kind asset. It has the third-highest grade among silver-primary assets in the world, at around 979 g/ton. It also has record-low All-In-Sustaining Costs ((AISC)) of around $6.7 per AgEq ounce. While this estimate is based on the 2021 Feasibility Study, and will undoubtedly be revised upward in the upcoming Updated Technical Report to reflect the recent inflationary pressures, the economics of the project are among the best in the sector, with an estimated payback period of less than one year. Average annual production is expected to be around 6.4 million ounces of silver and 69 thousand ounces of gold (which means, based on current spot prices, that more than half of total revenues are silver-related). The life-of-mine is 8.5 years, making it the fourth longest silver-primary asset in the world. In addition, the exploration potential is significant, especially given the previous successes of the current management team and the geology of the region.

Las Chispas mine vs. comparable projects (Company's Presentation)

{kind=link}

Despite Covid-related logistical challenges and inflationary pressures, the project was brought online in less than 7 years from discovery to production. More remarkably, this was done on time and on budget, a direct result of an experienced management team used to under-promising and overdelivering. Last year was particularly significant for the company. First, pour occurred on June 30, 2022. Subsequent commissioning activities tracked in line with or ahead of the Feasibility Study expectations. Commissioning activities ended on October 30, 2022, which marked the beginning of commercial production .

While the most visible targets have already been achieved, there are still plenty of reasons to be excited about the future. Recent drillings have been consistently successful, especially at the Babi Vista Vein , which are still not taken into account in the Feasibility Study. Plant design throughput is planned to reach its plateau value of 1,250 tpd by the end of 2022. An Updated Technical Report will be released in H1 2023. Besides a revision of reserves and of the mine plan, together with the associated sustaining capital costs, the Updated Technical Report will also contain a revision of the operating costs. Looking ahead, 2023 will be crucial for the company, as it progressively replaces material from the historic stockpiles used during commissioning, with ore material from underground mining. This will give it the opportunity to stress-test its geological models and should turn the company cash flow positive.

Despite the recent bull run in silver and silver equities, the company's valuation remains cheap. SilverCrest has a market capitalization of around $980 million, cash and cash equivalents of $88.6 million and a debt balance of around $90 million (as of the end of Q3 2022). The comfortable cash position means that further capital expenses can be funded internally and do not require any shareholder dilution. Assuming cash costs of around 10$/AgEq ounce (to reflect the higher operating costs and include also interest and administrative expenses), Las Chispas should produce around $175 million in FCF per year, based on current silver spot prices. This is equivalent to an EV/FCF ratio of around 5.6x, definitely not an expensive valuation considering the quality of the team, the exploration upside and the margin of safety.

I would argue that low-cost producers like SilverCrest deserve a significant premium in the current market conditions. Volatility in the metal price and inflationary pressures can literally crush the margins of most silver producers. SilverCrest has the advantage that its low costs will allow it to remain profitable even under challenging conditions. Meanwhile, it has the possibility to grow organically its production profile thanks to its exploration program, giving it optionality in a silver bull market.

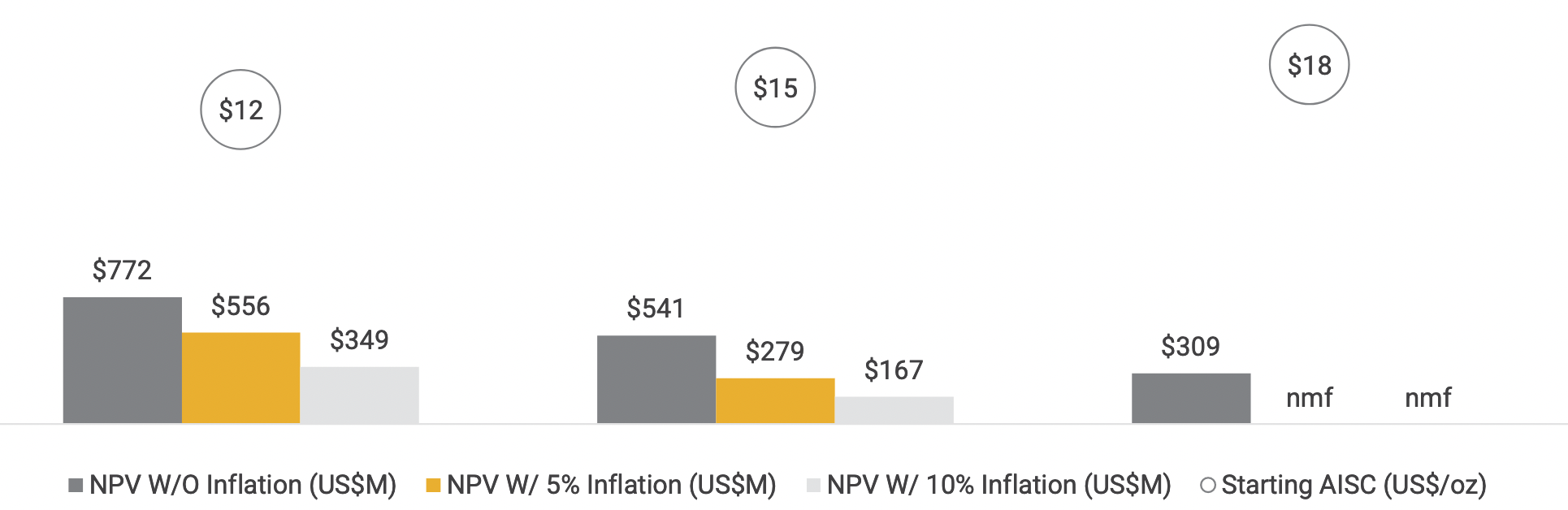

The following example perfectly exemplifies how a higher inflation environment leads to a more dramatic margin compression for higher-cost producers than for lower-cost producers. It considers three identical assets, with annual production of 10 million ounces and a 10-year life-of-mine, but with different cash costs of, respectively, $12, $15, and $18 per ounce. The silver price is assumed to be fixed at $22 per ounce. If inflation averages 10%, the NPV of the lowest-cost asset is reduced by 55% (compared to a scenario with no inflation), but it is reduced by almost 70% for the second asset, while the third asset becomes uneconomic!

Why lower-cost producers deserve a premium in a high-inflation environment (Company's Presentation)

{kind=link}

Conclusions

Precious metals are at a crucial crossroad. While a correction in the short term is possible and actually healthy, I believe that the trend will continue higher, both because monetary-policy-related headwinds are weakening and because sentiment is still far from ebullient about the sector. My strategy at the moment involves buying high-quality, forgotten junior producers. In this regard, SilverCrest is one of the best names to invest in for silver exposure. Despite being a single-asset producer, SilverCrest Metals Inc. arguably deserves a premium, because of its high-margin operations, especially given the current environment of higher inflation and inflation volatility.

For further details see:

SilverCrest: An Excellent Way To Play The Silver Bull Market