CA - Simon Property Group Stock: Buy The Dip Hand-Over-Fist

2023-04-11 04:30:56 ET

Summary

- SPG stock has pulled back by ~17% over the past few months due to a combination of recession fears and a tougher refinancing environment.

- We believe that the pullback is an attractive opportunity.

- We share three reasons why the stock is a Strong Buy on the dip as well as one big risk to keep an eye on.

Simon Property Group ( SPG ) stock has pulled back by ~17% over the past few months due to a combination of recession fears and a tougher refinancing environment:

In this article, we share three reasons why SPG is a strong buy on the dip and also look at the big risk to keep an eye on:

#1. Flight To Quality

SPG owns a diverse portfolio of properties, including enclosed malls (100M sq. ft.), Premium Outlet Centers (30M sq. ft.), The Mills (20M sq. ft.), and the Taubman Realty Group. Other than Brookfield ( BN ) ( BAM ) and to a lesser extent Macerich ( MAC ), there is no other U.S. mall landlord that can come close to SPG's asset scale and quality.

Moreover, its assets are overwhelmingly considered to be "Class A" and therefore enjoy close proximity to more dense and affluent population centers. This results in much greater demand for shop space in its centers by tenants given the access SPG's assets provide to substantial consumer purchasing power. Moreover, its scale enables it to develop close relationships with tenants and consumers alike (via loyalty programs and name brand recognition). As a result, SPG's pricing power is much greater, and its property redevelopment and value-add prospects are much greater relative to landlords of lower quality assets and/or smaller real estate empires. This produces a virtuous cycle, leading to strong rent growth over time and a very sustainable business model through economic cycles.

These competitive advantages are becoming even more pronounced today. First of all, lingering impacts from the coronavirus crisis are driving retail tenants towards malls and shopping centers with dominant positions in their local trade areas, as they prioritize profitability. According to Robb Paltz from Moody's Investor Service, tenants are likely to continue avoiding speculative malls with low traffic volume and margins. Thus, the "flight to quality" is anticipated to continue within the retail REIT sector with a focus on population and income demographics supporting the mall as well as the mall's adaptation to experiential tenants. These are both areas where SPG excels.

Moreover, now with the economy teetering on the brink of a recession, tenants are most interested in operating in the most economically vibrant shopping centers as they are the best positioned to continue generating sufficient revenue during a recession in order to remain profitable. Moreover, given that SPG's assets have among the very best anchors, it is the least likely to see its properties enter a death spiral due to a major anchor going bankrupt and having to vacate its stores.

Last, but not least, SPG's strong balance sheet gives it the financial firepower it needs to reinvest in its properties and keep them economically viable during a severe economic downturn. This leads us to our next point...

#2. SPG's Balance Sheet Is Second To None

SPG's A- credit rating from S&P with a stable outlook - one of the very strongest in the entire REIT sector and the best among all mall landlords - demonstrates just how strong its balance sheet is.

It has substantial wiggle room relative to its senior unsecured debt covenants as well, with a debt to total assets ratio of just 42% (well below its 65% covenant limit), total secured debt to total assets of just 19% (well below its covenant limit of 50%), a fixed charge coverage ratio of 4.8x (well above its covenant floor of 1.5x), and total unencumbered assets to unsecured debt of 248% (well above its covenant floor of 125%).

On top of that, its unsecured interest coverage ratio is a very conservative 5.8x and its FFO payout ratio is a mere 58% (giving it plenty of retained cash flow to fund capital expenditures). Moreover, while its weighted average interest rate has risen significantly over the past year due to rising rates, it still remains quite low at just 3.43%, while its weighted average term to maturity on its debt of 6.7 years implies that its debt maturities are well-laddered.

Even more important is the fact that only 10.8% of its debt is variable rate and its weighted average term to maturity on its fixed rate debt is 7.1 years. It also has a relatively small amount of debt maturing in 2023 with some of its highest yielding debt coming due this year as well. As a result, even if interest rates should remain higher for longer, SPG is well-positioned to weather these headwinds.

As of the end of 2022, SPG has ~$7.8 billion in total liquidity, including $1.3 billion in cash on hand, giving it plenty of flexibility to invest opportunistically across its real estate portfolio and even inject cash into its struggling tenants in exchange for equity (as it has done in the past with tremendous success) in order to sustain its occupancy numbers in the short-term while also generating outsized long-term returns for shareholders.

In summary, it is hard to think of a retail REIT whose balance sheet is better positioned to weather a recession than SPG's.

#3. SPG Stock Is Meaningfully Undervalued

Last, but not least, SPG's valuation looks quite attractive right now. It is currently trading at a 20% discount to consensus analyst estimates of NAV per share, a 15.81x EV/EBITDA ratio (which is well below its 10-year average of 17.6x), a 10.12x P/AFFO ratio (which is well below its 10-year average of 15.81x), a 9.19x P/FFO ratio (which is well below its 10-year average of 14.17x), and a 6.67% dividend yield (which is well above its 10-year average of 4.77%).

When you combine those attractive looking numbers with the fact that occupancy for its malls and outlets at the end of 2022 was a very robust 94.9% (up 150 basis points year-over-year and up 40 basis points sequentially), domestic property NOI growth was 5.8% year-over-year for Q4 and 4.8% for all of 2022, including ABR per foot growth of 2.3% year-over-year, it looks very cheap.

The Big Risk To Keep In Mind

Recession concerns have been on the rise due to several data points indicating that a recession is increasingly likely. For example, recent data showed a 29% decline in global personal-computer shipments from a year ago. Geopolitical concerns are also on the radar, with China's military saying it is "ready to fight" after completing large-scale combat exercises around Taiwan.

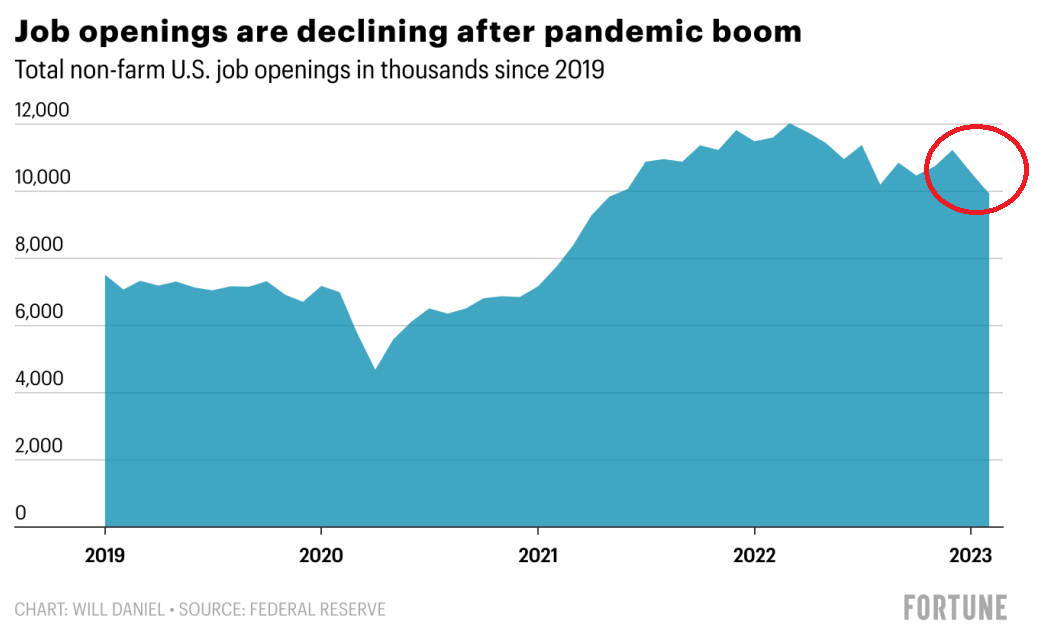

Furthermore, U.S. Jobs data indicates that the jobs market is cooling significantly. This could mean that a spike in unemployment and a sharp decline in consumer purchasing power could be right around the corner:

{kind=link}

When you combine these broader macroeconomic headwinds with the recent regional banking ( KRE ) crisis, the outlook for commercial real estate ( VNQ ) is looking increasingly dicey. This is because interest rates remain elevated and bank lending standards are clearly tightening even as the economy is showing real signs of slowing, particularly in commercial real estate. Between the rise of e-commerce and the work from home trend, office and retail real estate are facing increasing disruption at the same time that businesses are tightening their belts and trimming their payrolls (thereby declining the need for office space) and consumer demand appears to be set for a decline. As a result, it is not surprising that SPG's stock price has taken a hit.

If we fall into a deep recession or even depression (which is considered the likely scenario in the catastrophic scenario that China attacks Taiwan) and interest rates are forced to remain higher for longer due to stubbornly high inflation, SPG will likely take a significant hit to FFO per share and its assessed NAV per share will likely have to be written down substantially as well. In such a scenario, SPG will not look so cheap after all.

Investor Takeaway

While SPG is definitely not a guaranteed win and we would not even label it a low-risk investment given its economic sensitivity, we do believe that the risk-reward is strong asymmetric in favor of longs at current prices.

Between likely repricing of shares back closer to historical valuation multiples in the coming years alongside the attractive current dividend and probably continued per share FFO growth, the path to double digit total returns is quite clear. Meanwhile, even if a severe recession hits and hurts SPG's total return generation, the company is very unlikely to suffer permanent impairment (barring a severe depression) given its very strong balance sheet and high-quality portfolio. As a result, we rate SPG a Strong Buy at present and believe the current pullback in the stock price presents an attractive buying opportunity.

For further details see:

Simon Property Group Stock: Buy The Dip Hand-Over-Fist