TXG - Singular Genomics: Betting On Expanding Genomics Systems Market

Summary

- Singular Genomics Systems is a unique opportunity to invest in a commercially-viable startup at the forefront of a rapidly expanding field.

- The company has adequate funding to maintain its current level of commercialization and sales activity for a few years.

- Capital gains could hit triple-digit rates if management is successful in implementing its goals, but getting there will be a long, arduous process.

Investment Thesis

Since launching its first product, BeadLab, in 2002, Illumina ( ILMN ) shares have returned 13,500% return at their peak in late 2021. Singular Genomics ( OMIC ) could be the perfect stock for investors regretting losing out on the gene sequencing boom of the early 2000s.

Although the industry has been around for quite some time, many of its applications and end markets are just beginning to emerge, underpinning its potential upside in the coming years. Since the FDA approved Luxturna, the first gene therapy in 2018, a dozen gene therapies have entered the market, and hundreds of others are under development. We also see rapid growth in molecular diagnostic tests, driven by advancements in sequencing and broader adoption from professional guideline-setting bodies and key opinion leaders. For example, Exact Sciences ( EXAS ), the molecular diagnostic company behind the much-marketed "ColoGuard," and one of the handfuls of participants of OMIC's Early Access Program "EAP," has a 5-year annual revenue growth average of 70%.

There is also a need for more product diversity in the market, created by the shortcomings of ILMN's product portfolio. It has become clear that no single company can cover this market's use cases, either from a technological perspective or a pricing strategy. Below is one of many research abstracts expressing this sentiment, comparing some of the few devices on the market, including ILMN's HiSeq 4000, 10x Genomics ( TXG ), BGI Genomics' ( 300676. SZ ) MGISEQ, PacBio's ( PACB ) Sequel, and Oxford Nanopore's ( ONTTF ) PromethION and MinION.

Among short-read instruments, HiSeq 4000 and X10 provided the most consistent, highest genome coverage, while BGI/MGISEQ provided the lowest sequencing error rates. The long-read instrument PacBio CCS had the highest reference-based mapping rate and lowest non-mapping rate. The two long-read platforms PacBio CCS and PromethION/MinION, showed the best sequence mapping in repeat-rich areas and across homopolymers. NovaSeq 6000, using 2 × 250-bp read chemistry, was the most robust instrument for capturing known insertion/deletion events. Nature, 2021

The script above, similar to many others, clearly notes that no device is perfect for all uses, and as the industry grows, the need for different technologies will become deeper. Thus, although OMIC is a late entrant in a competitive space, we see strong potential in its genetic sequencing technology and platform.

Revenue Trends

After a rocky start in scaling production, OMIC reported its first product shipment in Q4 2022, realizing $700,000 from three G4 sequencing instruments, in addition to two devices whose revenue is yet to be recognized. Production delays plagued the company in 2022 as it tried to ramp up production to meet demand from early adopters and partners (pre-orders commenced in Q4 2021.) Nevertheless, as with many of its peers, scaling up the chemistry of its instruments away from lab-setting into mass production was met by many challenges impacting consistency, a common problem in the biotech sector.

The preliminary revenue announcement gives more visibility on OMIC's pricing strategy, which shows that, on average, investors should expect a selling price of $230,000 per instrument, in addition to recurring sales from consumables, including kits, reagents, and cell flows needed to operate the device. In a previous article, I showed that, on average, ILMN realizes $140,000 per device in consumables each year, and PacBio also generates a similar amount.

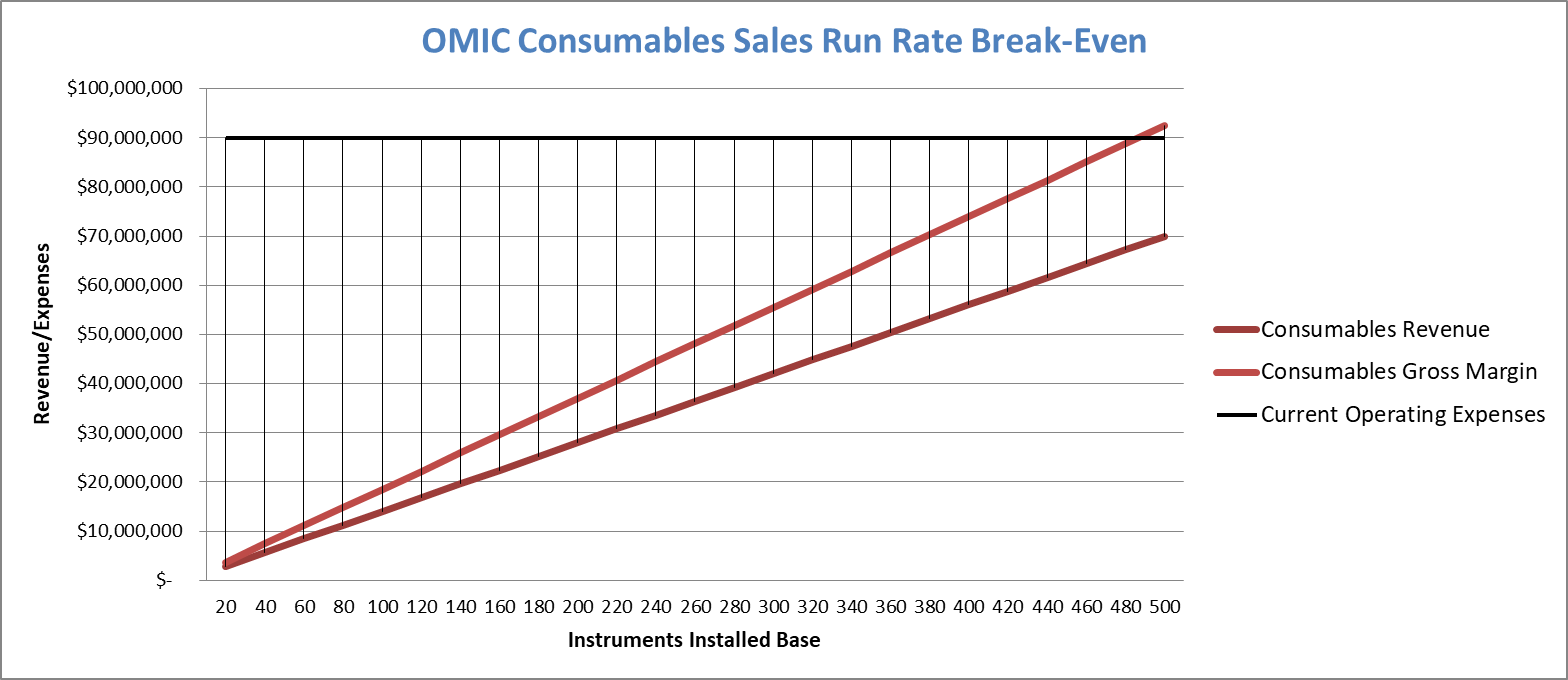

How much should we expect in gross margins? Initially, OMIC's margins will be very low, or even negative, given its small scale, barely enough to cover overhead costs. However, in the long term, its margins will revert to industry averages shown below.

Assuming the OMIC realizes a 60% gross margin, it needs 500 devices installed to reach consumables sales run-rate break-even. Thus, we are still at the beginning of the road, and one shouldn't ignore the challenges related to first-product launches.

There is always a learning curve, as OMIC's CEO realized when attempting to scale up the production of G4. In the short run, investors should expect five devices shipped per quarter, according to management guidance. Thus, it is critical to follow the company's progress in ramping up manufacturing capacity.

Operations

During its lifetime, OMIC raised $450 million and delivered a product to the market using approximately $190 million, demonstrating an efficient use of cash. The company is now in its third year of operations and has reached another inflection point as it looks to expand its customer base and product offerings. To that end, OMIC is investing in new sales personnel to increase its reach into new markets and improve the capabilities of its existing sales force to grow sales and penetrate deeper into the market.

At this point, OMIC spends $90 million annually on operating expenses, divided equally between R&D and Administrative costs. As a small company, investors can quickly see the direct relation between R&D and revenue growth. The company's development efforts culminated in the rollout of G4 and will soon see a ramp-up in PX sales. However, the gene sequencing industry is highly competitive. After OMIC finds its scale, I believe that this correlation between R&D and growth will become weaker. At some point, product upgrades will become necessary to maintain a technological edge and market share, rather than generate growth. This is one of the negative characteristics of the industry that OMIC has to contend with.

Balance Sheet

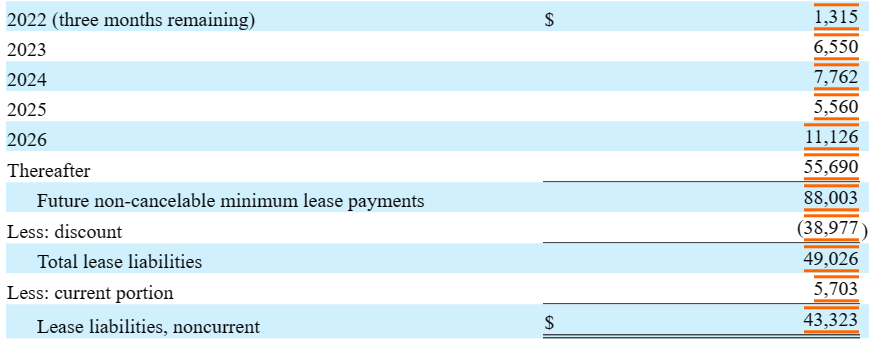

The latest data from OMIC's quarterly report dated September 2022 shows $345 million in total assets, 76% ($264 million) of which is cash and cash equivalents. The company's liabilities total $68 million, mostly consisting of leases payable under noncancelable operating contracts (such as office leases), payable over the next years, with the bulk due after 2026. Below is OMIC's lease obligation schedule.

OMIC Operating Lease Liabilities. Figures in 000s $ (Singular Genomics Q3 22' Report)

{kind=link}

Interest-bearing debt stands at $10 million, a small amount compared to the company's cash balance, and interest payments are fully covered by interest income derived from interest from the company's financial assets, mainly consisting of US government short-term bills.

{kind=link}

Cash burn increased as the company ramped up marketing and selling expenses related to the G4 rollout and the R&D expense related to the PX Spacial analysis system. The current cash burn run rate now stands at $90 million - $100 million, giving OMIC a cash runway of approximately two years, give or take, before it runs out of cash. Filings with the Securities and Exchange Commission "SEC" show that the company registered a $250 million self-registration offering in preparation to raise additional capital to push on its commercialization agenda.

Summary

I am bullish about OMIC's prospects in the short to medium term, but there are several headwinds that the company will have to overcome in order to scale its business and achieve long-term growth successfully. This includes establishing interest in its products on a scale enough to generate necessary literature around its products, a critical component in generating market adoption. Second, the company needs to continue building a scalable and reliable manufacturing process.

After a rough start, we are seeing early signs of progress manifested in the newly announced product shipment. Nonetheless, the company experienced multiple operational setbacks, including its discussions with Columbia University regarding the "Diligence Obligation Clause," which I believe is related to the delay in bringing the product into the market.

From a valuation perspective, the company is significantly undervalued relative to its peers, trading below its net cash balance. This valuation gap is due to several factors, including low visibility into the company's future revenues, high R&D spending, which is expected to detract from near-term profitability, and operational challenges that continue to weigh on the company's operations despite recent positive developments. Still, among "Third-Generation Sequencing" companies, most of which are also unprofitable and facing similar challenges, it is the most undervalued, offering an attractive speculative trade thesis if the company can execute its growth plans in a timely manner.

For further details see:

Singular Genomics: Betting On Expanding Genomics Systems Market