VZ - SK Telecom: Looking Beyond The Traditional Business Model

- 5G is reversing the declining ARPU trend. But intense competition and the lack of killer apps hinder 5G from significantly increasing ARPU.

- Telcos, including SKT, look beyond the traditional business model to ramp up their growth trajectory. While it is too early to judge, the numbers are showing good signs so far.

- SKT produces higher EBITDA margins than its competitors and generates consistent free cash flows. However, from a valuation perspective, KT seems a better choice.

Investment Thesis

Although 5G started to reverse the declining ARPU trend, intense competition and the lack of killer apps will hinder it from significantly impacting ARPU. Like other telcos, SK Telecom Co., Ltd looks beyond the traditional business model to ramp up its growth trajectory, and the numbers show a glimpse of promise. Lastly, SK Telecom operates at higher EBITDA margins than its competitors, generates consistent free cash flows, and has low debt. But KT Corporation’s EV/EBITDA is much lower than SKT’s.

Ownership Structure

SK Telecom Co., Ltd ( SKM ) is a Korean wireless telecommunication service provider whose operations go back to 1984. SK Inc., the ultimate controlling entity, owns 30% of SK Telecom (we will call it SKT from here on).

SKT's Ownership Structure (Company)

{kind=link}

In 2021, SKT completed the horizontal spinoff of SK Square, which engages in semiconductor and ICT businesses. As additional information, SK Square is now the major shareholder of SK Hynix following the spinoff, replacing SKT.

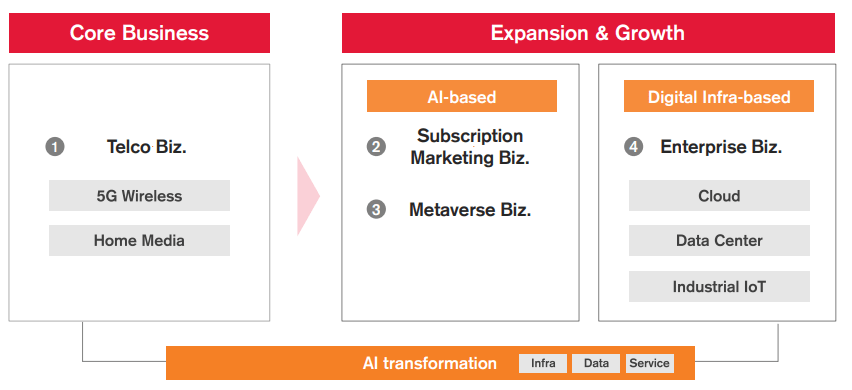

SK Telecom 2.0

As their growth is stalling, telcos are looking beyond the traditional business model to reignite their growth trajectory, including SKT. SKT redefined itself as an aspiring AI-based service company–the so-called SK Telecom 2.0. As a result, SKT divides its business into five groups: Mobile & Fixed, which remains a core business, and four segments with high growth potential: Media, Enterprise, AIVERSE, and Connected Intelligence.

SK Telecom 2.0 (Company) Strategies (Company) SKT's Growth Trajectory (Company)

{kind=link}

{kind=link}

Industry Analysis: 5G To Reverse Declining ARPU

SKT directly competes with KT Corporation (NYSE: KT ) and LG U+. KT is the biggest operator in terms of revenue. But SKT leads in the mobile service market.

The industry is highly regulated by the Korea Communications Commission and the Ministry of Science and ICT ((MSIT)). Previously, SKT, as the dominant network service provider, was required to obtain approval from the MSIT regarding its rates and terms of services. The MSIT could order changes if those rates were “significantly unreasonable or against public policy.” After the Telecommunications Business Act amendment, the MSIT can object to rates or terms submitted by SKT within fifteen days.

Moreover, the MSIT can take proactive measures to promote competition. For example, by passing regulatory criteria, any company can become a network service provider without a separate license requirement. Furthermore, in April last year, the MSIT allowed ten MVNOs to offer more affordable 5G mobile data plans after the ICT ministry granted MVNOs the flexibility to independently design their 5G data plans, according to the Yonhap news agency.

The emergence of MVNOs is a double-edged sword, in our view. On the other hand, MVNOs, which lease bandwidth capacity from MNOs, can help drive MNOs' revenues. On the other hand, MVNOs offer lower rates than MNOs, intensifying competition and thus impacting profitability. For example, Figure 5 shows that SKT leads in the wireless subscribers' market share. But it was not until recent years that the share started to deteriorate. Nevertheless, after separating MNO and MVNO subscribers, we found that LG U+ showed incredible growth thanks to expanding MVNO subscriber base.

MNO + MVNO Market Share (Companies, Vektor Research) MVNO Subs Market Share (Companies, Vektor Research)

To gain a clearer picture of the industry, we divided the time frame into three periods: the emergence of 4G LTE (2010-2014), industry stagnation (2014-2018), and the 5G age (2018-present). During the first period, the wireless industry’s aggregate wireless service revenue grew 3% annually thanks to the emergence of 4G LTE technology in 2011. In the subsequent years (2014-2018), however, the growth rate declined by 0.6% per year. Finally, as we enter the 5G era, the revenue growth started to pick up once again (~2% per year).

Aggregate Wireless Service Revenue Growth (Companies, Vektor Research)

We believe that the share price reflects the trend. SKT’s share price bottomed out in mid-2012 before it reached its highest in late 2014. Since then, the share price had stalled, and it picked up again as we entered the 5G era.

SKT and KT Share Price (Yahoo Finance)

Why did this happen? The mobile & fixed industry drivers are subscriber base growth and ARPU. First, smartphones began to gain traction in the last decade's first half, primarily supported by 4G LTE technology in 2011. Since then, the penetration rate began to stagnate (see Figure 9).

Second, telco ARPU declined because of the rising popularity of OTT services overshadowing many operators' services, such as voice calls. Moreover, competition from MVNOs lowered prices.

Penetration Rate (Company, the Ministry of Interior and Safety) ARPU (in KRW) (Companies)

But in the third period, revenue growth started to pick up, albeit only slightly. Although 5G was introduced in 2019, such technology did not immediately lift ARPU. In the early days of 5G, SKT encouraged widespread adoption by offering discounted data plans ranging from US$49 per month to US$66 per month with a data cap and from US$78 per month to US$110 per month with unlimited data. Other operators also introduced promotions.

Aggressive rollout results in high 5G adoption: over a third of aggregate wireless subscribers were 5G users in 1Q22. GSMA estimates that 5G will represent 73% of mobile connections by 2025. And the trend is likely to continue. For example, SKT plans to offer more affordable plans as low as KRW40,000 per month (~US$30.6 per month).

To make matters more appealing, people are moving to premium plans. For instance, SKT reported a 0.6% annual increase in ARPU from 1Q21 to 1Q22, trailing KT that recorded 3.7% (Y/Y) gain. By contrast, LG U+, posted an ARPU decline of 4.2% (Y/Y).

5G Subs as a % of Wireless Subs (Companies)

Although 5G has not yet significantly impacted operators because of the lack of the so-called killer apps, it has started reversing the declining ARPU trend. Therefore, who holds the upper hand in the 5G competitive landscape?

No Significant Competitive Advantage

Spectrum holdings are crucial for operators to gain a competitive advantage. In the US, for example, T-Mobile US (NASDAQ: TMUS ) managed to drive its subscriber growth by deploying its extensive mid-band spectrum early.

But it was not the case in the Korean telecom industry. In June 2018, SKT and KT acquired 100 MHz in the 3.5 GHz band, while LG U+ won 80 MHz. Last month, the ICT ministry announced that LG U+ secured additional 20 MHz of spectrum in the 3.4-3.42 GHz band despite complaints from its competitors. Moreover, each of the three operators also obtained 800 MHz in the 28 GHz band.

Research by OpenSignal suggests that SKT led the pack in 5G availability and 5G download speeds, while RootMetrics, which measured performance by city, found that LG U+ won in some areas. Yet, despite the difference in methodologies, the result might prove our hypothesis: the difference in performance between all three operators is not that much, indicating no significant competitive advantage. Yet, this was not the case in the US.

5G Availability by OpenSignal (OpenSignal) 5G Availability by RootMetrics (RootMetrics) 5G Download Speeds by OpenSignal (Mbps) (OpenSignal) 5G Median Download Speeds by RootMetrics (Mbps) (RootMetrics)

All in all, we believe that operators have no significant competitive advantage in the mobile market. Indeed, an aggressive 5G rollout and more people moving to premium plans will likely continue to reverse the declining ARPU trend. But it is unlikely to drive operators’ revenue growth to a large extent partly because of competitive pressures and the lack of killer apps. GSMA also estimates that developed APAC mobile revenue growth to grow 2.9% in 2022 before slowing down to 1% in 2025.

Growth Story: Leveraging 5G to Go Beyond the Traditional Business Model

As growth in the mobile market is stalling, telcos look beyond a traditional business model to help drive their growth trajectory and are making moves. For example, early this year, KT acquired a stake in Shinhan Financial Group amounting to KRW437.5 billion to “promote digital platform technology based future growth DX business cooperation.” Moreover, KT decided to integrate its OTT platforms with CJ ENM.

When asked regarding M&A plans, SKT CEO Young Sang Ryu said that the company plans to acquire technology companies that focus on AI and metaverse. Furthermore, SKT invested KRW10 billion in CMES, an AI robot-based logistics business, as a part of its Connected Intelligence business. In addition, SKT signed a memorandum of understanding with Equinix (NASDAQ: EQIX ) to “to expand the quantum business including ‘QKD as a Service ((QaaS))’ in both Korean and overseas markets.”

As we advance, SKT expects media, enterprise, and AIVERSE to grow 30% per year until 2025, contributing more than a third of SKT’s revenue.

{kind=link}

And the numbers look promising. For instance, SKT’s 1Q22 data center revenue grew 35% (Y/Y), and the cloud business increased by a whopping 229% (Y/Y) after the Gasan and Siksa data centers were opened in July last year. As it stands, the company is developing other data centers in the Seoul metropolitan area with the size of 80MW (scheduled to operate in 2026), as mentioned during the 1Q22 earnings call . Moreover, SKT said it would build four data center buildings by 2024 and 12 more by 2029.

Data Center and Cloud Revenues (in KRW Billion) (Companies) SKT's Data Center Ambition (Company)

{kind=link}

AIVERSE includes subscriptions and the metaverse business. In September last year, SKT unveiled T Universe, a subscription-based service that bundles third-party services, claiming to have generated a GMV of KRW350 billion in 2021. By leveraging AI and digital transformation, SKT seeks to offer an “advanced online-offline subscription commerce platform” that specifically caters to customers’ needs in the future. SKT aims to reach 36 million T Universe subscribers by 2025, with an annual GMV of KRW8 trillion.

SKT’s metaverse service, ifland, showed incredible growth in monthly active user ((MAU)), which stood at 1.35 million compared with only 280 thousand less than a year before. The management believes that the AIVERSE business will generate KRW2 trillion by 2025, up from KRW200 billion in 2021. Moreover, AIVERSE does not require massive Capex, while offering massive potential growth. While it is too early to say whether such ambition will materialize, numbers are showing good signs.

Financial Analysis

Figure 19 shows that SKT has declined 16% since the beginning of the year.

Share Price Change (Yahoo Finance)

Figure 20 shows that SKT and KT’s revenue growth picked up in the last few quarters. Please note that SKT’s quarterly revenues in 2021 excluded the spin-off business. Thus, we see declines in revenue. In reality, SKT’s revenue grew 4% (Y/Y) in 2021, just as KT did in the period.

Revenue Growth (Y/Y) (Companies)

Yet, SKT has produced EBITDA margins higher than its competitors. After the horizon spin-off, SKT’s EBITDA margins were up from 29%-30% to 31%-32%.

EBITDA Margin (Companies)

Moreover, balance sheet-wise, SKT and KT are on the safe side, although the former had an edge.

Net Debt to EBITDA (x) (Companies, Vektor Research)

SKT’s ROAE was around 7% after the spin-off. With a three-year average of ~6%, SKT’s ROAE is far trailing other incumbents in their respective industries, such as Verizon (NYSE: VZ ) at 28% and Telkom Indonesia (NYSE: TLK ) at 21%.

ROAE (%) (Companies, Vektor Research)

SKT has been paying dividends consistently, as the company is a cash-generating business, recording consistent free cash flows in the last ten years. When asked about SKT’s dividend policy, the CEO said that the company would maintain dividends juts like before the spin-off. In the future, it will be based on EBITDA and Capex.

FCF (KRW Billion) (Companies, Vektor Research)

SKT is trading at a forward EV/EBITDA of 4x (Seeking Alpha comparison ), indicating that it much cheaper than many of its peers. KT, though, is trading at a more attractive multiple than SKT.

Valuations Comparison (Seeking Alpha)

{kind=link}

Overall, SKT produced higher EBITDA margins and a more consistent cash-generating business than KT. We assume that SKT and KT's balance sheets position is on the safe side, and their 3-year average ROAE ratios are similar at ~6% (KT slightly has an edge on this one). However, from a valuation perspective, KT seems a better option since its EV/EBITDA is about 40% lower than SKT.

Investment Risks

Intense Competition from MVNOs and Lack of Killer Apps. MVNOs are putting pressure on MNOs, lowering profitability. The lack of killer apps will hinder MNOs' effort to ramp up 5G adoption and significantly improve ARPU while also spending massive Capex on the network build-out.

Lower-than-expected growth from growth businesses. The growth businesses, such as data centers and metaverse services, are showing promising results. But we think it is too early to tell whether they will live up to their expectations. Failure for the expectations to materialize will jeopardize SKT's growth story.

Conclusion

While the rising popularity of 5G should offset the declining ARPU, the lack of killer apps might not significantly drive ARPU growth. Therefore, like other telecoms, SKT looks beyond the traditional business model. And the advanced 5G development and high adoption in Korea support telcos' growth businesses. For example, SKT is developing its data center business, a subscription-based business, and a metaverse service, which would probably not possible without advanced 5G development. While it remains unknown whether these businesses will live up to the expectations, the numbers show a glimpse of promises.

Although SKT produced higher EBITDA margins and is a more consistent cash flow generator, KT's multiples are much lower than SKT's. Suppose you are looking for defensive stocks with stable dividends. In that case, VZ is probably something you want to look at due to its proven dividend track record, high ROAE, and reasonable valuations (not a recommendation).

Yet, if you are looking for diversification, SKT and KT are possible options, and it might be worth observing how their growth stories will unfold. For now, we assign a HOLD view on SKT. If you have any thoughts, please do not hesitate to comment below.

For further details see:

SK Telecom: Looking Beyond The Traditional Business Model