SKX - Skechers: A Good Time To Start A Position

2023-07-18 08:17:03 ET

Summary

- Skechers has potential to expand its direct-to-consumer segment and continue strength in the Wholesale segment, making it a good long-term investment.

- The company's financials are solid, despite slight hiccups in FY22, and it is expected to see positive trends in the future.

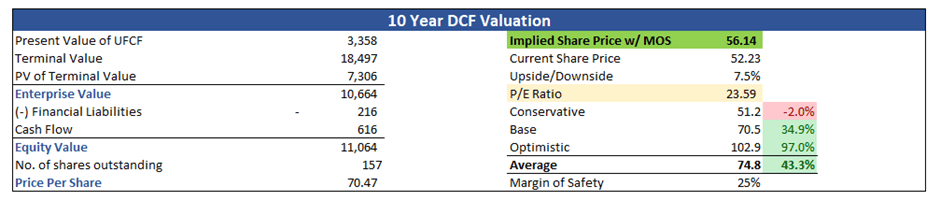

- Skechers' intrinsic value is $56.14 a share, implying an under-valuation currently, and further expansions into Europe will help revenue growth.

Investment Thesis

I wanted to take a look at one of my favorite shoe companies, Skechers (SKX), to see what kind of an outlook it has in store, look through its historic financials, and give my target price based on reasonable assumptions. I believe that the company has a lot of potential to expand its direct-to-consumer segment, along with continuing strength in the Wholesale segment, Skechers is a good buy right now for investors who are looking for a long-term position to add to their portfolio.

Outlook

The problem with quarterly reporting is that everyone is so focused on the short term. When I saw that the company went down slightly on their softer guidance for Q2, I thought that was an overreaction, to say the least, and could be an opportunity for a long position. I had to dig deeper into the company itself to see what kind of potential it has. The company reported decent sales quarter after quarter and the most recent report looked very good to me, with gross margins expanding on the wholesale and DTC segments. The only bad thing that I saw, and everyone else, was the decline in the domestic wholesale segment, which I think is just a short-term hurdle and will come back to growth very soon.

Wholesale

This segment is still the top revenue generator for the company and will probably be for another few years. To grow this segment, the company will have to rely on other shoe stores to stock their Skechers shoes. The global footwear market is expected to grow to $312B by '28 from $234.5B just last year, representing 3.9% CAGR, which is still fine, however, this segment is not going to experience a very massive growth rate for Skechers in my opinion.

Direct To Consumer

A lot of companies are starting to focus on their brand stores that will avoid the middleman selling their products. The wholesale segment is great to have still because it is a good way of reaching a lot more of an audience, however, gross margins suffer because the company has to sell the distributor the shoes at a lower price. The DTC segment naturally will come with higher gross margins, for example, the Wholesale segment in the latest quarter achieved 39.6%, while the DTC segment came in at 66%.

So, of course, the management is going to focus a lot more on the DTC segment going forward and build out their empire through their own branded stores and e-commerce channels. Digitization is one of the better ways to achieve higher margins in the long run and if the company is going to focus most of its energy on this segment, it will achieve higher margins going forward. Of course, in the beginning, operating margins might suffer a little but over time, it is a win for the company. A recent survey found that Skechers is becoming very popular among people and took second place right after Nike, which tells me that people are preferring the combination of comfort, style, and a cheaper price tag than the other well-established companies in the industry, especially the older generation that is fueling the popularity in the brand. The company is aiming to open 125- 140 stores worldwide to continue pushing the DTC segment further.

I believe that the slowdown in the domestic market will start to pick up much sooner than anyone thinks, while international markets will continue to see robust growth for years to come, especially now that China is out of the zero Covid situation and people are back shopping in person, coupled with much lower inflation than we saw previously, the shoes will become much more accessible against competitors like Nike ( NKE ).

Potential Risks

I also think that DTC can be a double-edged sword. Sure, the gross margins are going to be much better than the wholesale route, however, opening up all the extra stores, hiring people, and other operating expenses will add up in the future and may bring lower net margins in the end than just going the wholesale route. The company is focused on gross margins and that is why I believe the strategy of focusing on DTC is the priority for them because they are looking for that high number on the gross margins, which is almost double that of the wholesale segment. If the company is not able to minimize operating expenses in the long run, the profit margins from the DTC segment will be much lower than the wholesale and the company may have to start closing down its own stores in favor of wholesale distribution.

A potential long-term risk could also come from future lawsuits like the one we saw with Nike a couple of years back with regard to patent infringement. Nike said Skechers "ripped off" their designs on some of the shoes. This was ultimately settled in 2021 and no details are known as to what happened afterwards. If this sort of thing repeats and Skechers loses, that could be a huge hit to the company's reputation and sales.

Financials

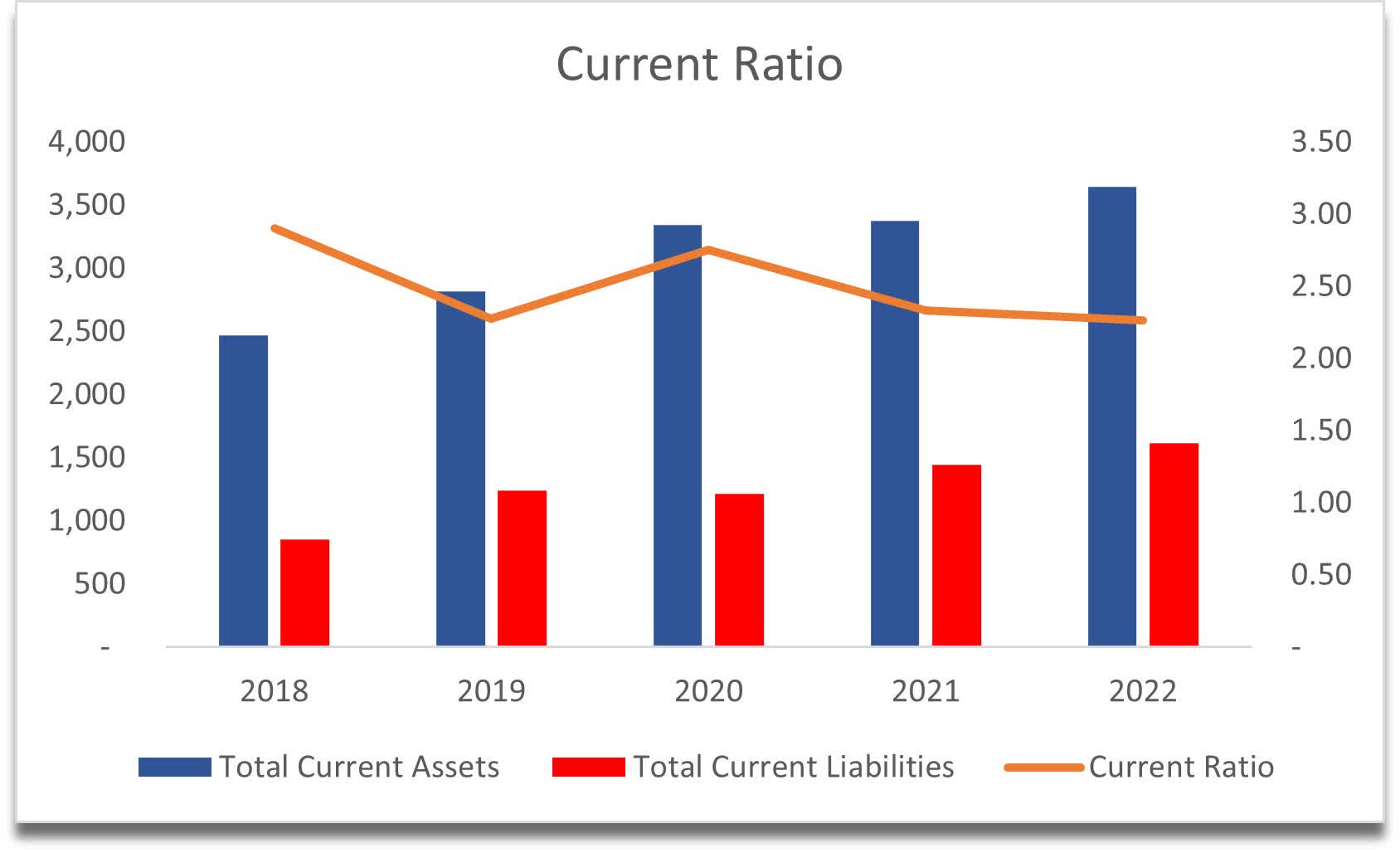

Skechers as of Q1 '23 had $760m in cash and around $90m in short-term investments against around $230m in long-term debt. EBIT in the same period was $522m, which easily covers any interest expense it would have. The company's current ratio has been very healthy over the years, and it stood at 2.2 as of FY22, which tells me that the company has no liquidity and insolvency issues. It would be able to pay off its short-term obligations twice over if it had to, all at once.

{kind=link}

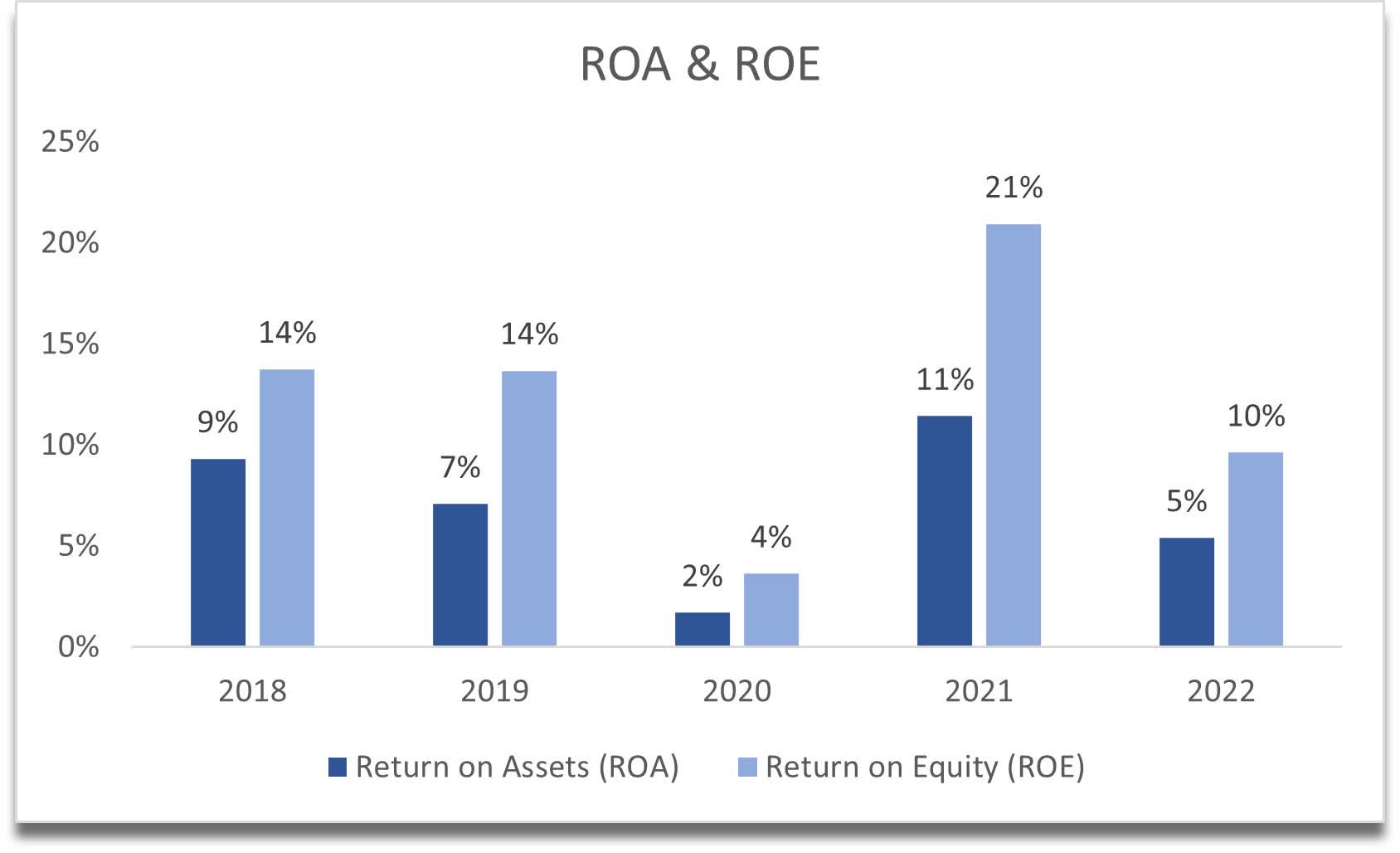

I am a little more worried about the efficiency and profitability metrics that the company achieved at the end of FY22. ROA and ROE, although right at my minimums of 5% for ROA and 10% for ROE, have come down from the previous year's highs. This tells us that the company still is somewhat efficient at utilizing its assets and shareholder capital, but something happened in '22 that has affected the returns quite a bit.

{kind=link}

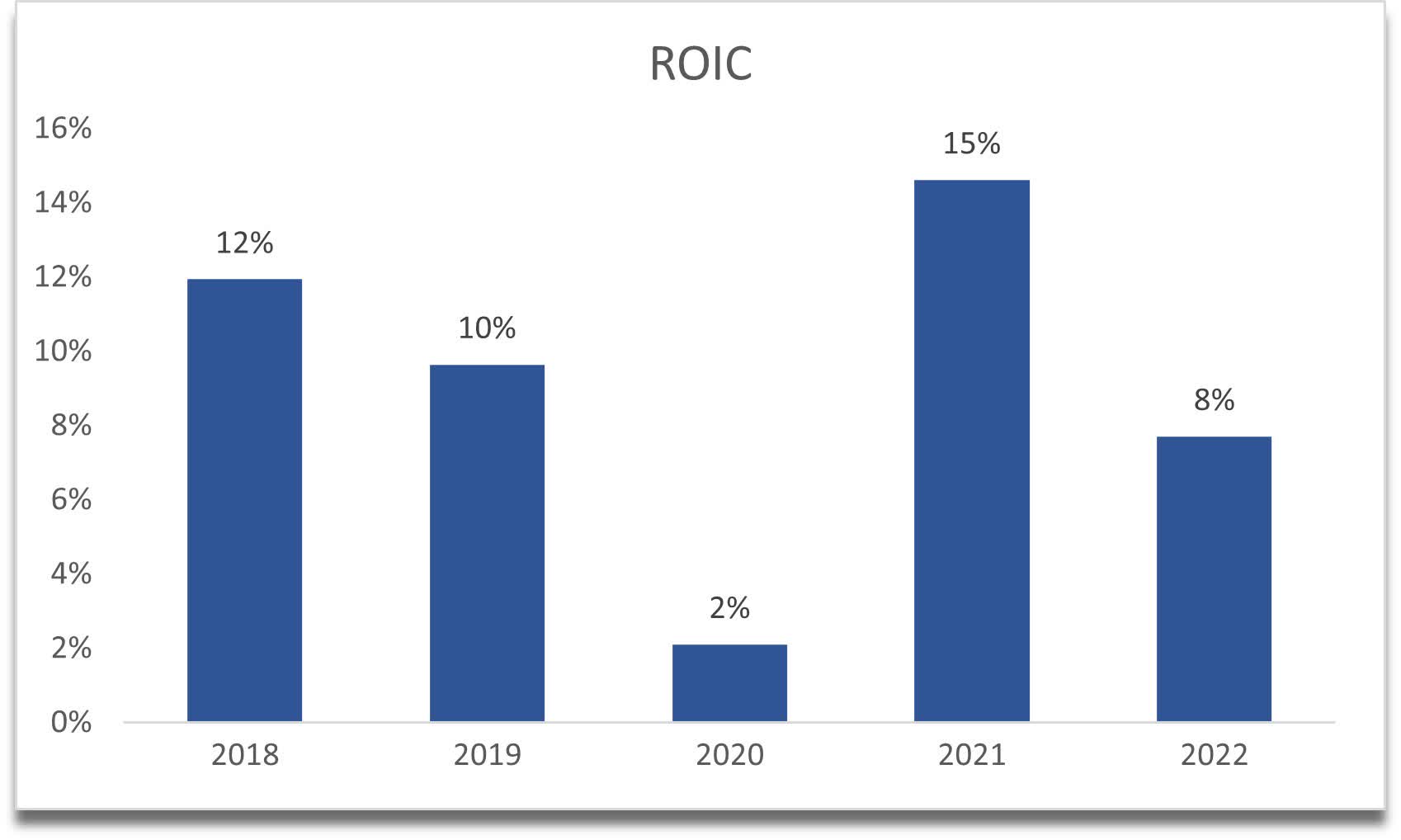

A very similar scenario to the company's return on invested capital or ROIC. It has come down from FY21, which tells us that Skechers lost a bit of the competitive advantage and some of its moat in one year. I would like to see the number come back above 10% ideally in the future.

{kind=link}

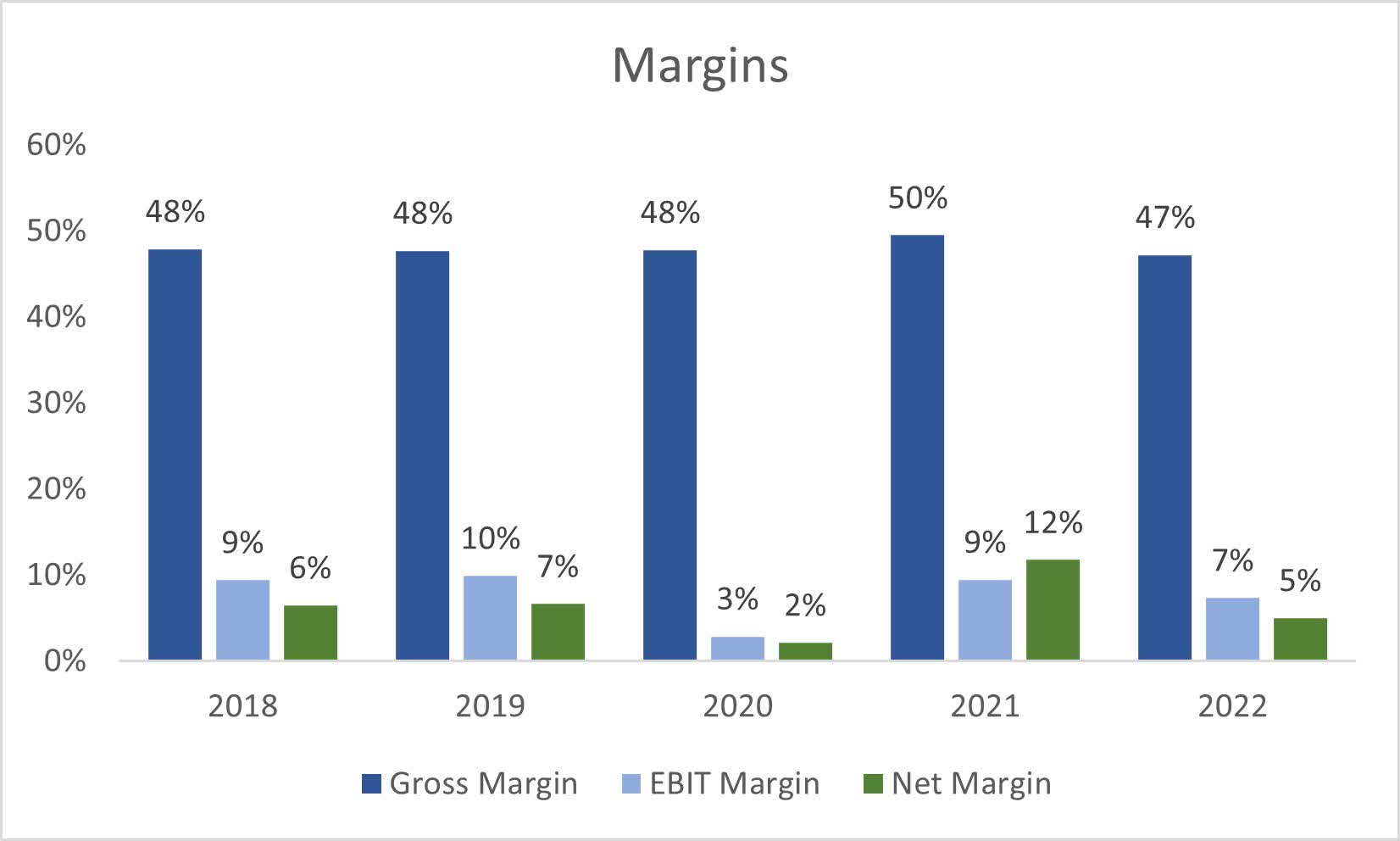

In terms of margins, these also have come down slightly from FY21, however, during the latest quarter report, we saw that the company gained 360bps in gross margins already, so I'm confident that the company is going to increase the above metrics this year if it manages to find some more cost-cutting measures.

{kind=link}

Overall, very solid financials, with slight hiccups in FY22 but we are already seeing some positive trends in the first quarter of '23, so I don't expect these to continue to trend downward for long unless something bad happens.

Valuation

I like to approach my valuation calculations with a little more conservatism, so for my base case revenue growth, I went with around 7.7% CAGR over the next decade. In the last decade, the company grew revenues at around 18% CAGR, so I think my assumption is quite conservative.

For the optimistic case, I went with 11.5%, while for the conservative case, I went with 5.7% so I can get a range of possible outcomes, which are all very likely to happen.

In terms of margins, I went with a slight improvement over time of around 400bps or 4% on gross margins and 200bps on operating margins from the margins the company attained in FY22. We already know that in Q1 23 the company improved margins by 360bps, so an improvement of 400bps over the next decade is very achievable. These improvements will bring net margins to around 12% by '23, which is about where the company was at the end of FY21.

On top of these assumptions, I'll add a 25% margin of safety to be even more conservative. With that said, the company's intrinsic value is $56.14 a share, implying an under-valuation currently.

{kind=link}

Closing Comments

I like the company at this price, and I do believe that Skechers will continue to perform well in the future in terms of gaining market share from other footwear companies because of their design, comfortability, and affordability. The shoes are very high quality and last a long time and are very affordable. That is what attracted me to the shoes in the first place.

Once the demand comes back in the domestic market, the company will perform above analysts' estimates. It is not a bad time to open a position right now and wait for the reward in the future.

Further expansions into Europe with the acquisition of Sports Connection will help revenue growth and the company will start to dominate the footwear industry as long as it doesn't drop the ball and the momentum continues.

For further details see:

Skechers: A Good Time To Start A Position