SKX - Skechers: Commercial Powerhouse Growing Well

2023-06-22 22:21:42 ET

Summary

- Skechers has grown its revenue at a CAGR of 15%, with its current commercial profile suggesting a continuation is possible.

- Margins are poor relative to peers, but we see scope for improvement with increased direct-to-consumer sales.

- Skechers is trading at a sufficient discount to its peers to imply upside in our view, with a target of 11-24%.

Investment thesis

Our current investment thesis is:

- Skechers is a strong brand with an attractive business model. The company is growing rapidly and its trajectory looks to be continuing.

- Further growth will be driven by improving direct-to-consumer sales, fashion trends leading to increased demand for athleisure, and further international expansion.

- Relative to peers, Skechers is an underperformer, but we believe the valuation adequately reflects this. With strong quarterly sales, we are not overly concerned by the impact of economic conditions.

Company description

Skechers U.S.A., Inc. ( SKX ) is a global footwear company that designs, develops, and distributes a wide range of footwear for men, women, and children. Skechers also provides technical footwear for specific activities such as running, walking, and golf. In addition to footwear, they offer slip-resistant shoes, safety-toe shoes, and lifestyle apparel.

Share price

Skechers' share price has performed extremely well in the last decade, outperforming the market and returning over 500%. This is driven by a consistently strong financial performance, reflecting resilience.

Financial analysis

{kind=link}

Skechers financials (Tikr Terminal)

Presented above is Skechers' financial performance for the last decade.

Revenue & Commercial Factors

Revenue has grown at an impressive rate of 15% since FY12, with 9 financial years of strong growth, one impacted by Covid-19, and the other during weakening economic conditions.

Business model

The Skechers business model is an impressive story of growth, market share gains, and outperformance.

Skechers' objective is to provide comfortable, stylish footwear at affordable prices. The market is filled with performance trainers, such as from Nike ( NKE ), fashion trainers, as well as many affordable options. Very few businesses focus on selling the concept of comfort, likely because of the lucrative younger generation at far more focused on fashion. This has allowed Skechers to differentiate itself and lean into this idea of comfort, describing itself as a "Comfort Technology Company".

Skechers sells its products through both wholesale distributions and direct-to-consumer (Digital and brick-and-mortar ((BAM)) stores).

Retail industry

The retail industry has experienced increased interest in athleisure, which is blurring the boundaries between athletic and casual wear. The driving factor of this is likely changing fashion trends, with an acceleration due to the impact of the pandemic, as consumers seek versatile apparel that can be worn in several settings. Skechers has heavily benefited from this and is entrenching itself within this segment. The company's expansion into clothing is directly into the athleisure segment.

E-commerce was a major shift in the retail industry. Many of the BAM retailers have struggled in part due to the inability to compete on price, with online-only retailers using their asset-light nature as a means of funding customer acquisition. Skechers has grown despite this, primarily due to its value proposition. Consumers are sold on the product, unwilling to consider alternatives. E-commerce has only been a threat because once consumers obtained enhanced choice and better pricing, retailers lost their value proposition.

One of the (many) reasons Retail is considered an unattractive industry is due to changing consumer trends. What was once popular and the next big thing can be left by the wayside just as quickly. In order to mitigate this, businesses are focused on maintaining relevance within the culture they are targeting. In the current social media era, this involves direct-to-consumer marketing through social media and other related services.

Skechers has adapted to the change in the industry well in this regard, partnering with many celebrities (Such as Doja Cat ) and influencers, as well as transitioning many of its new designs toward the typical fashion trends. The approach is interesting as if you look at Skechers' website, it very much reflects the core messaging of the business (Comfort) and its target market. If you go to its social media, however, the business looks like a fashion brand. We perceive this to be smart marketing. Skechers is adjusting its image based on who it is marketing to, a strategy many businesses will not do out of stubbornness of maintaining consistent messaging.

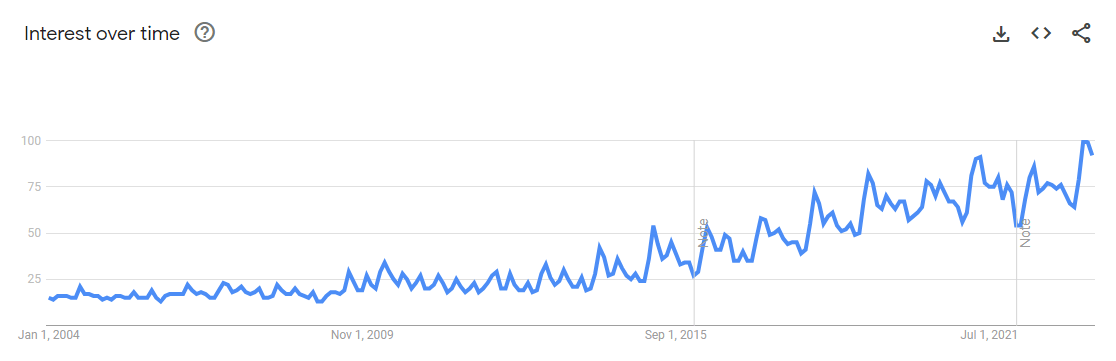

The returns from this are clear. Despite more than tripling its revenue, the company's online interest has only recently peaked (as the below illustrates). This is extremely rare for a mature business, implying the company's current trajectory will continue.

{kind=link}

Skechers (Google Trends)

Direct-to-consumer is a key opportunity in our view. With such a strong online presence currently, it makes complete sense that Skechers should drive sales to its own outlets, cutting out the middleman, and improving returns. Historically, retail outlets were the gatekeepers to accessing consumers, but with e-commerce and social media, this is no longer the case. Skechers looks positioned perfectly to exploit this.

Another opportunity for Skechers is global expansion. The business is already operating across several continents but is not embedded to the extent it is in the US.

Economic & External Consideration

Current economic conditions represent a key near-term risk to Skechers. Inflationary pressure and elevated rates are negatively impacting consumers, contributing to softening consumer spending as finances are protected. Footwear is not a necessity for consumers, especially at Skechers' price point, which means many may defer spending where possible.

Skechers looks to be bucking this theory, with the most recent quarterly sales up 10% YoY. Further, DTC sales are up 24.5%, an impressive level, implying the strategy of bringing consumers in-house is working incredibly well. Further, sales in China are already on an upward trajectory, as the impact of Covid finally begins to subside. Based on these results and the assumption that growth in China will continue, we expect a strong result in FY23.

Margins

Skechers currently has a GPM of 48%, EBITDA-M of 10%, and a NIM of 10%. Margins have generally improved over the last decade, although faced some erosion in recent years.

The general upward improvement is driven by scale economies, allowing the business to extract greater marginal value. This has been diminished somewhat by the current inflationary pressure, resulting in greater operating costs.

Our view is that margin improvement should continue as inflationary pressure subside and increased DTC selling will contribute to margin improvement. This said, the ability to win margins will not be easy due to the level of competition.

Balance sheet

Inventory turnover has reached a 4 year higher, in a year when many have experienced a decline. This reflects strong inventory management, although could imply an expectation of slower demand. This said, the company's CCC has gradually increased in the last few years, contributing to a decline in FCF generation.

Skechers is conservatively financed, with an ND/EBITDA ratio of 0.8x (This is primarily property leases). This conservatism provides Skechers the flexibility to raise debt if required.

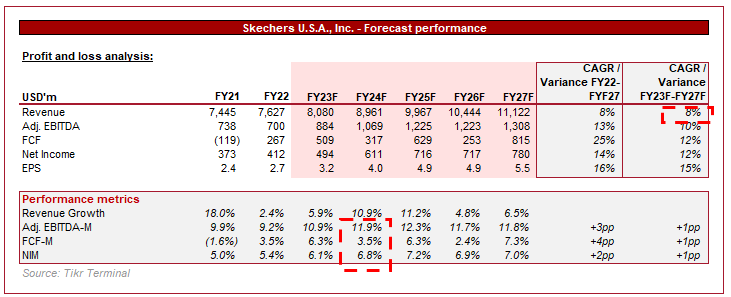

Outlook

{kind=link}

Outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting continued strong growth, driven by a continuation of the company's current strategy. In conjunction with this, margins are forecast to improve quickly, implying an impressive response to inflation subsiding.

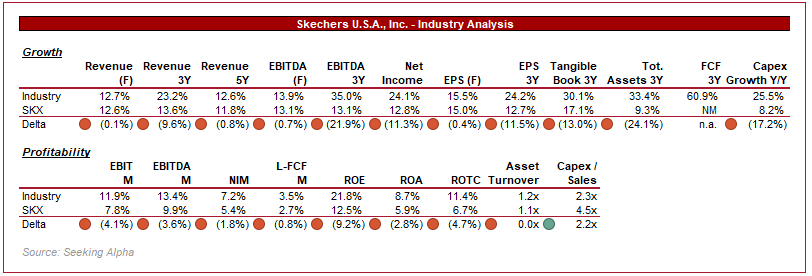

Peer analysis

{kind=link}

Footwear industry (Tikr Terminal)

In order to assess Skechers' relative performance, we have compared the business to a cohort of footwear businesses. Skechers underperforms the group on both growth and margins.

From a growth perspective, Skechers performs well on an absolute basis but is slightly below the average. This is due to 3 specific businesses lifting the average, Crocs ( CROX ), On holding ( ONON ), and Rocky ( RCKY ).

Profitability is more concerning, with a noticeable difference from the average. Of the 8 businesses, only 2 have an EBITDA-M below Skechers (one of which is 0.6% below).

Given the relative underperformance, we believe Skechers should be trading at a discount to the peer group.

Valuation

Skechers valuation (Tikr Terminal)

In order to value Skechers, we have utilized the valuations of the peer group discussed previously. Given the margin delta and slower growth, we have applied a 25% discount to the peer group's average valuation. We believe this adequately accounts for the weaker performance, especially on an NTM basis, when margins are forecast to improve.

Based on this valuation, we imply an upside of 11-24%. A reversion to the LTM historical average multiple implies an upside of 8% and analysts see a similar upside of 14%.

Key risks with our thesis

The risks to our current thesis are:

- A slowdown in growth, especially in the DTC segment, as we are pricing in healthy growth in FY24.

- Continued margin deterioration, even marginally, given the difficulty retailers face in winning margins back.

Final thoughts

Skechers operates an impressive business model. The company has generated a strong customer base which continues to grow in size. Skechers has pivoted well to changing trends and thus far, remains on its strong growth trajectory.

The upside will be driven by a continued transition to DTC sales, the athleisure trend supporting apparel growth, and international expansion. We cannot stress enough that a successful DTC strategy will unlock several percentage points in margin improvement.

Although the valuation does not imply large upside, we believe this stock warrants a buy rating given the resilience it has shown thus far in the face of weaker economic conditions.

For further details see:

Skechers: Commercial Powerhouse Growing Well