SKX - Skechers: Direct-To-Consumer Potential Shown In Q3 Growth Story Seems To Continue Well

2024-01-08 05:16:50 ET

Summary

- Skechers sells shoes through franchisee- and third-party owned stores, as well as company-owned stores and ecommerce.

- The company has had an impressive long-term track record of growth that still has room to continue.

- Skechers is shifting its focus from a flexible wholesale strategy into a more solid direct-to-consumer focus, solidifying operations and possibly leaving room for margin expansion.

- The stock currently seems undervalued when considering the promising prospects and historical track record.

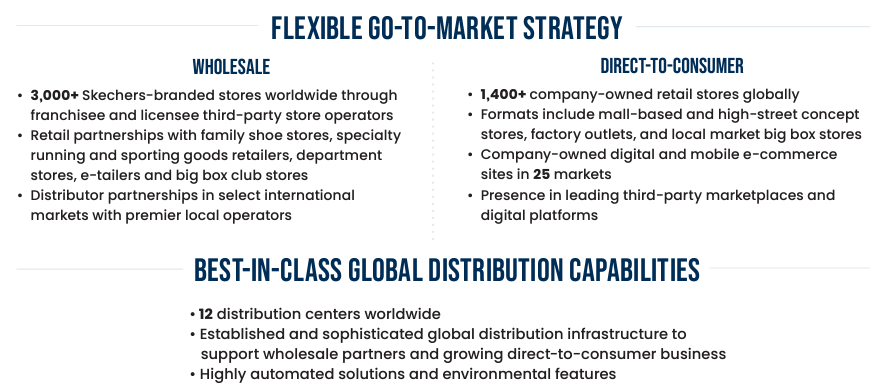

Skechers ( SKX ) sells shoes globally. The company’s offering ranges from casual to athletic sneakers, sandals, and apparel. Skechers currently has quite a large share of its sales in the wholesale segment – in 2022, around 62% of Skechers’ sales came from wholesale, and only 38% from direct-to-customer. Skechers operates around a third of the brand’s stores as company-owned stores, and the rest are through franchisees and licensed third-party owners adding to the wholesale segment. I believe that the wholesale segment positions the company well for growth partly at the cost of margins, and as the company describes, the business model is highly flexible due to the strategy.

{kind=link}

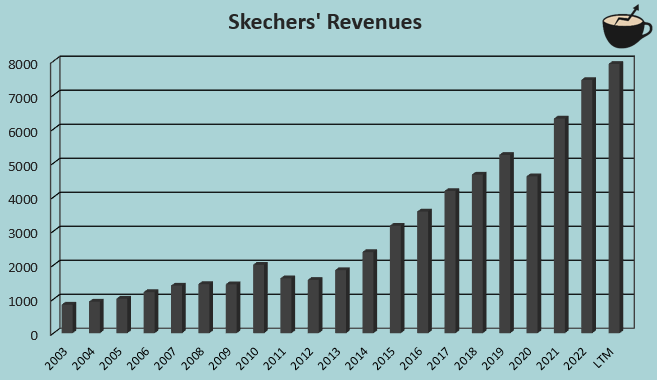

The stock has been an impressive compounder with a ten-year appreciation of 460%, making the CAGR in the period 18.8% - the company’s cash flow reinvestments seem to have paid off well, despite investors not receiving a dividend in the period.

{kind=link}

An Impressive Growth Path

Skechers has had an impressive growth performance. From 2003 to current trailing revenues as of Q3/2023, the company has had a CAGR of 12.0%. The company does have some acquisitions, but they are infrequent and small in size – with $194 million in cash acquisitions in the past decade, the growth can be characterized almost entirely as organic.

{kind=link}

I believe that Skechers should still have a good amount of room to grow its footwear sales. For example, Nike had around $33.1 billion in revenues from footwear in FY2023 according to the company’s annual report , and Adidas’ footwear sales reached 12.4 billion euros in 2022 , or around $13.6 billion in USD with the current currency exchange rate , compared to Skechers’ trailing revenues of $7.9 billion . Still, as the company scales its sales, the room for growth will eventually start to shrink, making achieving growth more difficult for Skechers. As Nike and Adidas are both still growing quite well at their large scale, I don’t think that Skechers is going to have the issue very soon.

Great Direct-to-Consumer Performance

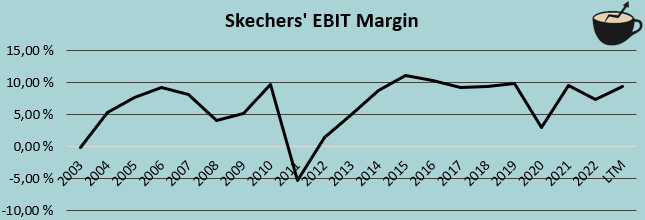

Skechers has had a very good performance recently even in the currently turbulent macroeconomic situation. In Q3, the company’s revenues grew by 7.8% year-over-year, and the company’s EBIT margin scaled by 3.6 percentage points year-over-year from 6.9% to 10.5%.

It seems that Skechers is solidifying the company’s self-owned store operations – the company’s performance has shifted from a flexible franchisee -model more into a well-performing company-owned store model. In the third quarter, the company’s wholesale revenues decreased by 1%, and direct-to-consumer sales grew by 24% driving the great performance. According to the Q3 earnings call , Skechers opened 72 new company-owned stores in Q3, in line with the company’s long-term growth plan through growing direct-to-consumer sales. In terms of geographical areas, direct-to-consumer sales in EMEA had an impressive growth of 61%, compared to APAC’s growth of 24% and the Americas’ growth of 17%. The new store openings and well-performing geographical areas further underline Skechers’ room to grow in select verticals.

In the Q3 earnings call, the improving channel mix was mentioned as a factor in Skechers’ impressive gross margin growth. The attribution seems reasonable, as company-owned stores capture a greater share of the value chain. While more capital intensive, growing company-owned stores could prove to be valuable for investors, as they seem to increase Skechers’ margins and solidify the operations. On an overall medium- to long-term basis, Skechers’ EBIT margin has mostly been near 10% from 2014 to Q3/2023 excluding the pandemic’s and cost inflation’s effects in 2020 and 2022, but could in my opinion scale if the channel mix continues to improve.

{kind=link}

Stock Compounding Should Continue

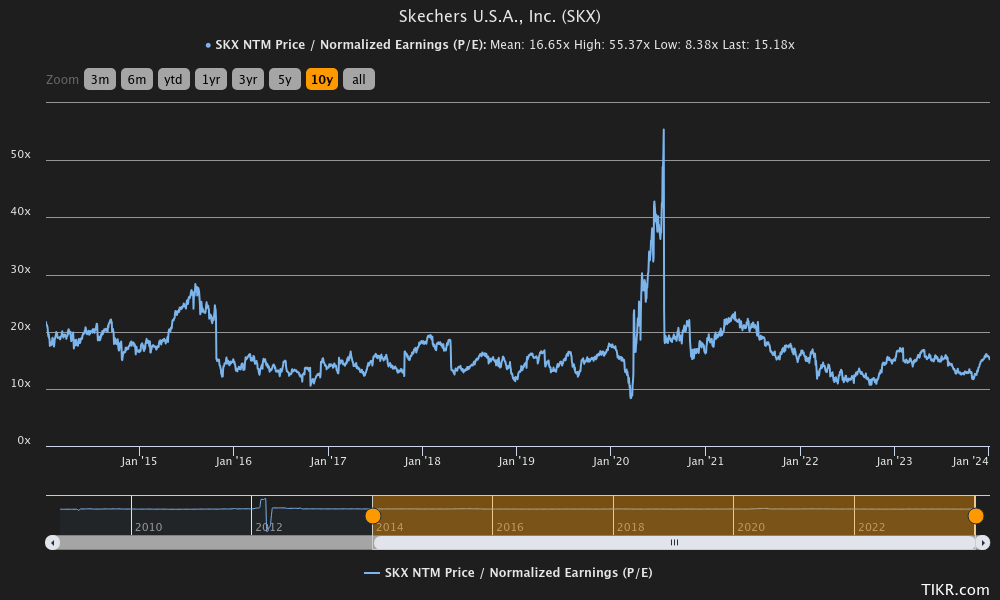

Skechers is currently priced near its long-term average on a forward P/E basis. Currently, the stock trades at a forward multiple of 15.2, a bit below the ten-year average of 16.7 but within the overall historical range.

{kind=link}

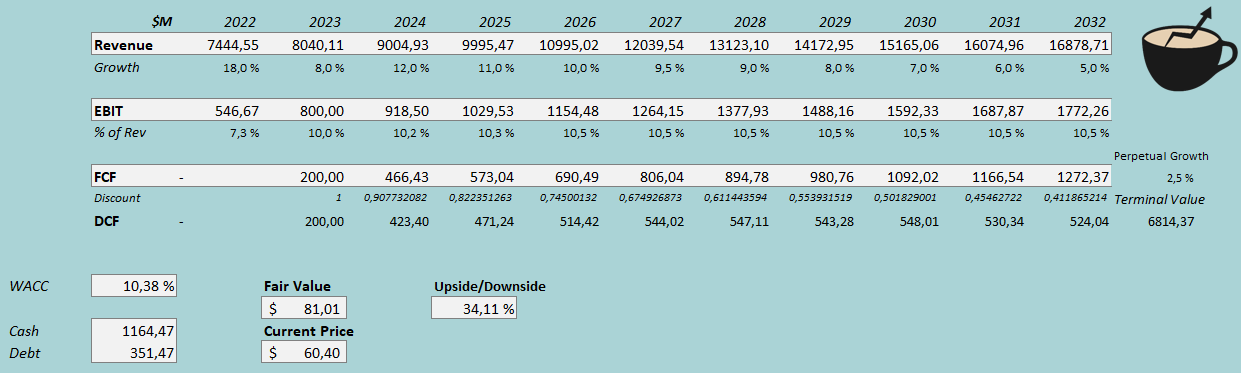

The P/E seems to be quite low when considering Skechers’ solid growth. To further demonstrate the valuation, I constructed a discounted cash flow model. In the DCF model estimates, I factor a continuing growth story. After a solid 2023 growth of 8%, I estimate the growth to accelerate with an estimate of 12% for 2024. Afterwards, I estimate the growth to slow down in steps into a perpetual growth of 2.5%, representing a CAGR of 8.5% from 2022 to 2032.

As for the EBIT margin, I estimate quite a stable performance. I estimate the margin to scale slightly from a 2023 estimate of 10.0% into 10.5% in 2026 and forward. The scaling represents a growing portion of direct-to-consumer sales, and otherwise quite a stable cost performance. Skechers’ growth takes up capital, making the cash flow conversion worse initially with the growth. The cash flow conversion improves in the DCF model as Skecher’s growth slows down.

With the mentioned estimates along with a cost of capital of 10.38%, the DCF model estimates Skechers’ fair value at $81.01, around 34% above the stock price at the time of writing. The estimated fair value represents a fair forward P/E of 20.4 with analysts’ estimates.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Although Skechers has some debt on the company’s balance sheet , the company doesn’t have interest expenses – it seems that the company capitalizes its interest expenses. As such, the costs of debt are already accounted for in the estimated cash flows, and the debt doesn’t bear costs in the CAPM; I estimate the cost to be free in the cost of capital, and a low long-term debt-to-equity of 3%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.05% . The equity risk premium of 4.60 % is Professor Aswath Damodaran’s latest estimate for the United States, made on the 5 th of January. Yahoo Finance estimates Skechers’ beta at a figure of 1.39 . Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 10.69% and a WACC of 10.38%.

Takeaway

Skechers’ growth story seems to still continue well. The company is also transitioning its focus from a flexible wholesale strategy into a company-owned store strategy, potentially improving the margins with time. My DCF model also estimates the stock to still have an undervaluation despite a very good price rally in recent years – I believe that the long-term stock rally still has room to continue. For the time being, I have a buy rating for the stock.

For further details see:

Skechers: Direct-To-Consumer Potential Shown In Q3, Growth Story Seems To Continue Well