CA - Skeena Resources: Buy The Dips

Summary

- Skeena Resources is one of the worst-performing gold developers this year, down 50% year-to-date and more than 60% from its June 2021 highs.

- This significant decline can be attributed to the stock getting ahead of itself from a valuation standpoint, the weakness in metals prices, and uncertainty surrounding high-grade material at Albino Lake.

- Skeena received a negative ruling related to the AWF in November, but I don't see this as material to the story and it's been largely offset by recent drilling success.

- With Skeena trading at a ~60% FY2026 free cash flow yield at conservative metals prices and 0.40x P/NAV despite having a phenomenal project with modest upfront capex, I see the stock as a steal below US$5.20.

Just over three months ago, I wrote an article on Skeena Resources ( SKE ), noting that the recent Feasibility Study [FS] had confirmed Eskay Creek's robust economics and that the stock looked to be offering a buying opportunity after a 60%+ correction. This turned out to be a very poor call, given that the stock immediately fell by 20% after it announced a capital raise with ~5.7 million shares sold at .70. However, this represented only ~7% dilution vs. an avalanche of dilution from other developers. It also resulted in a buy-back of a 0.50% NSR at Eskay Creek. So, with a decent rally in precious metals since then, Skeena has recovered most of its drawdown and trades at a similar level to my September update.

However, while the stock is more than 20% off its lows, it trades at a deep discount to its fair value, sitting at a market cap of just ~$440 million vs. an After-Tax NPV (5%) of ~$1.08 billion at conservative metals prices. Plus, this NPV figure doesn't capture any of the upside on assets/opportunities outside of the current mine plan, including underground potential, its nearby high-grade Snip Project, and an increase in Eskay Creek's mine life from new discoveries made in the past year. So, with Skeena trading at ~0.40x P/NPV with lots of upside for free, I see the stock as a steal below US$5.20.

{kind=link}

Eskay Creek Project (Company Presentation)

All figures are in United States Dollars unless otherwise noted at an exchange ratio of 0.77 CAD/USD.

Eskay Creek Project & AWF Ruling

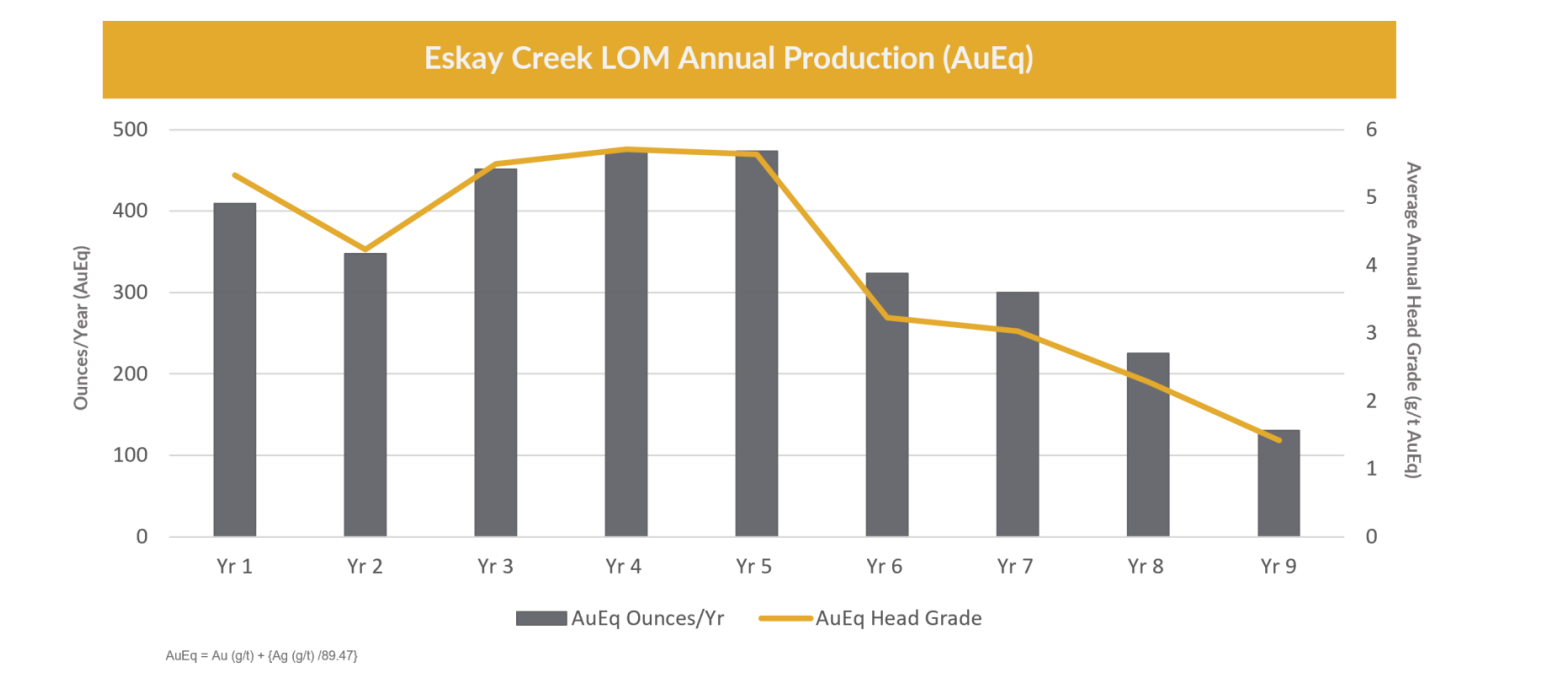

For those unfamiliar with Skeena Resources ("Skeena"), the company is working to bring the ultra-high-grade Eskay Creek Mine in the Golden Triangle of British Columbia back to life. To date, the company has delineated ~5.2 million gold-equivalent ounces [GEOs] in the resource category at an average grade of 3.5 grams per tonne gold-equivalent, and Skeena's recent FS highlighted a project capable of producing ~430,000 GEOs in its first five years at sub $650/oz all-in-sustaining costs [AISC]. Just as importantly, the project is expected to be constructed (assuming permits are granted) with a modest upfront capex of ~$460 million, benefiting from this being a brownfields site with existing tailings.

Comparing these costs to the industry average AISC of $1,270/oz shows Eskay Creek is nothing short of exceptional. However, the real differentiator for Eskay is its scale, with very few 100% owned undeveloped projects not held by majors having a 400,000-ounce production profile in Tier-1 jurisdictions except for De Grey's ( OTCPK:DGMLF ) Mallina, Artemis' ( OTCPK:ARGTF ) Blackwater, and Vista's ( VGZ ) Mt. Todd. This makes Skeena one of a kind in the junior sector, with a planned high-grade open pit with a 9-year mine life and a President (Randy Reichert) with considerable experience at major operating assets like Kupol and Fekola to help bring this into production and optimize the asset.

It's worth noting that while Randy Reichert was a very impressive addition to Skeena, he is surrounded by a very competent and experienced management team across several facets, giving Skeena one of the stronger teams in the junior space to help advance Eskay Creek.

{kind=link}

Eskay Creek Life Of Mine Production Schedule (2022 FS) (Company Presentation)

However, while the release of the FS was undoubtedly a huge positive for investors, it was followed by ~7% share dilution with an unexpected capital raise at unfavorable prices and an adverse ruling on Albino Lake. This ruling means that this waste facility (north of its planned open pits) on Skeena's property that appears to host significant mineralization (average intercept of 13.2 meters at 6.2 grams per tonne gold equivalent) may not be exploitable without a successful appeal. This mineralization was highly attractive given that it appeared to be higher grade than reserves and was deposited into Albino Lake by the previous operator (meaning it didn't need to be mined and would likely have been extracted at sub $300/oz cash costs).

The initial negative ruling was handed down in Q1 2022 by the Chief Gold Commissioner, noting that the individual holding a mineral claim on lands underlying the Albino Waste Facility [AWF] owns all the materials in the AWF. Skeena appealed the decision but received a dismissal of its appeal late last month in the case of Richard Mill versus Skeena. Skeena noted that it intends to appeal this decision, which makes complete sense given that it's a confusing decision, as Skeena's CEO Walter Coles pointed out in his February statement:

“It is incomprehensible to us that the Chief Gold Commissioner of British Columbia would transfer ownership of materials that Skeena and, prior to that, Barrick, have actively managed and environmentally monitored for decades in the Albino Lake Storage Facility to an individual who staked barren mineral claims below the facility. We feel this sets a grave precedent for mineral exploration, development, and environmental liability management in British Columbia. Skeena will utilize all legal avenues to remedy this situation within the BC court system and we have already begun the appeal process.”

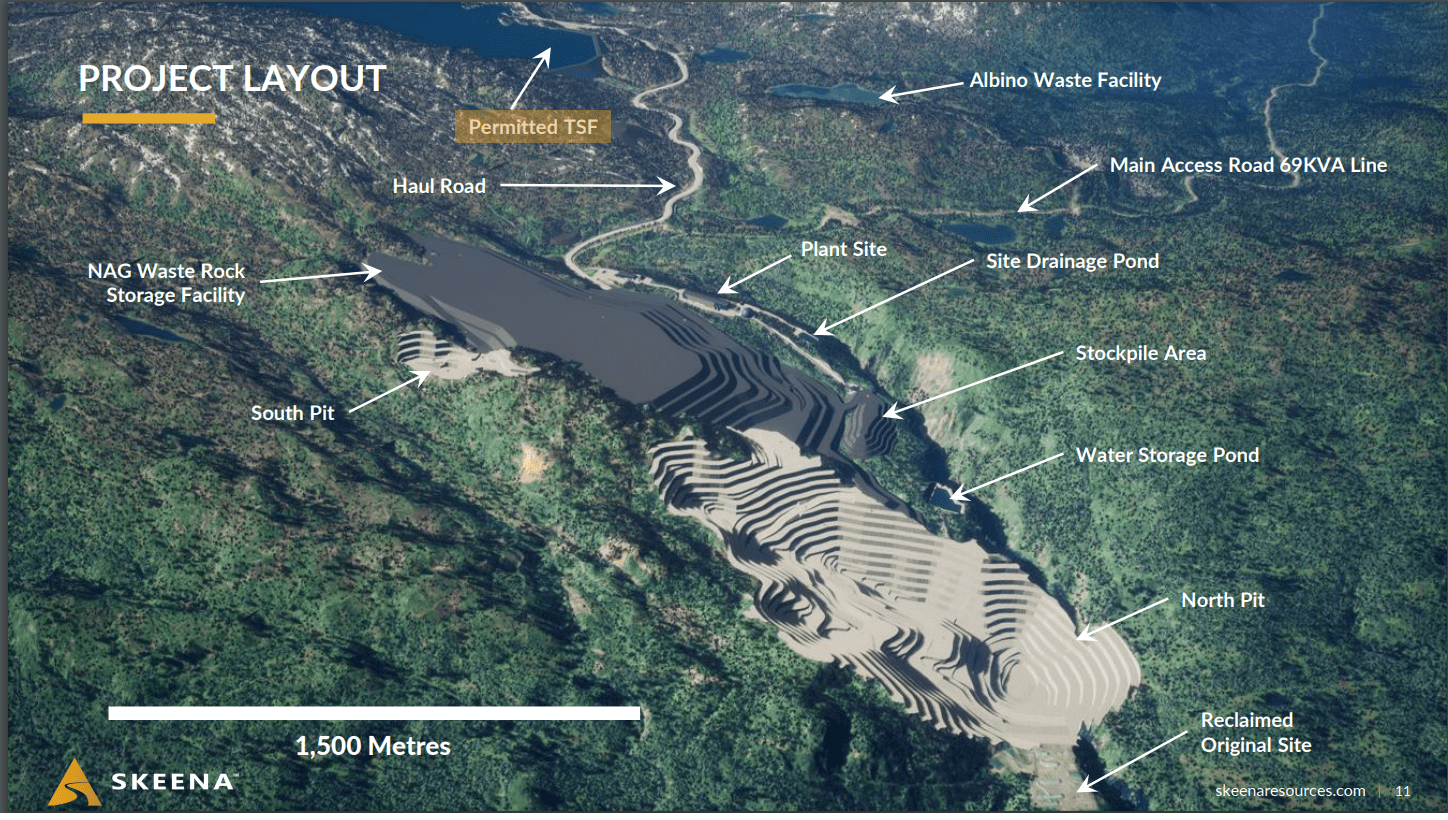

Although this is certainly a negative development and a little bit of a surprise in terms of the appeal decision, it's important to note that the AWF was an upside opportunity for Skeena, and it does not affect the economics of the 2022 FS, the company's resources or reserves, or its planned tailings (Tom MacKay Lake). This is a crucial point because Skeena was already receiving no value for the AWF in its valuation, meaning that this decision should not affect the stock, especially after a violent decline from its highs. Additionally, the benefit of having an existing tailings facility reduces the risk of a capex blowout and upfront capex, so the inability to extract material from the AWF should not be confused with the nearby tailings facility earmarked for Skeena's mine plan.

{kind=link}

Eskay Creek Project Layout (Company Presentation)

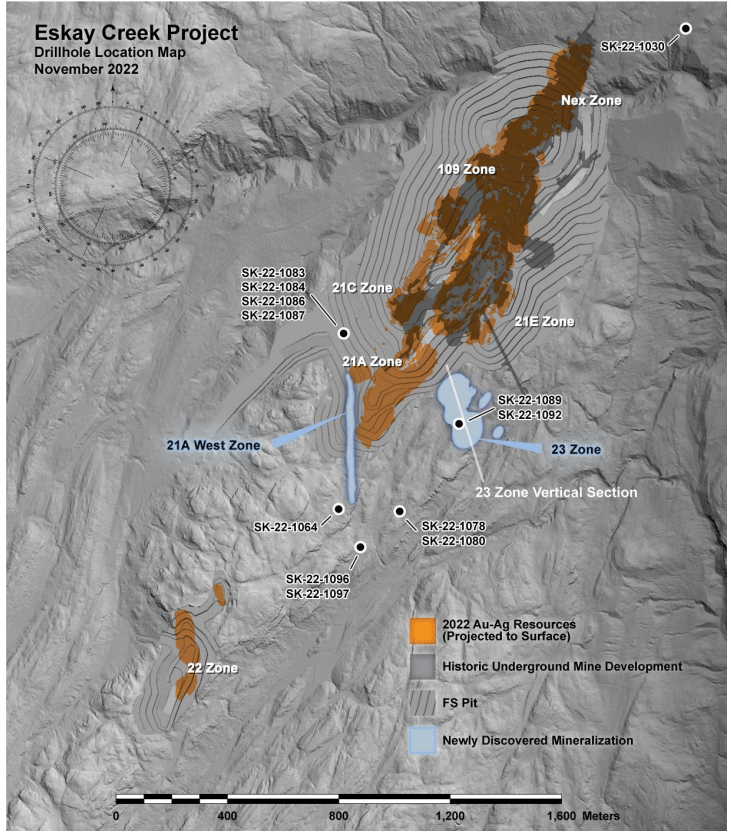

Besides, while this negative ruling (if not overturned) may cost Skeena upwards of 300,000 GEOs at very attractive margins, the company has continued to enjoy exploration success elsewhere on the project in several different zones. The company has delineated the new 23 Zone, it's in the process of adding ounces in the 21A West Zone, it appears to have made a new low-grade discovery east of the 22 Zone, and it hit an impressive 32.19 meters at 4.46 grams per tonne gold-equivalent at 850-meter vertical depths down-dip from the NEX Zone, suggesting that Eskay Creek is just as rich at depth at it is on the surface.

Recent Drilling

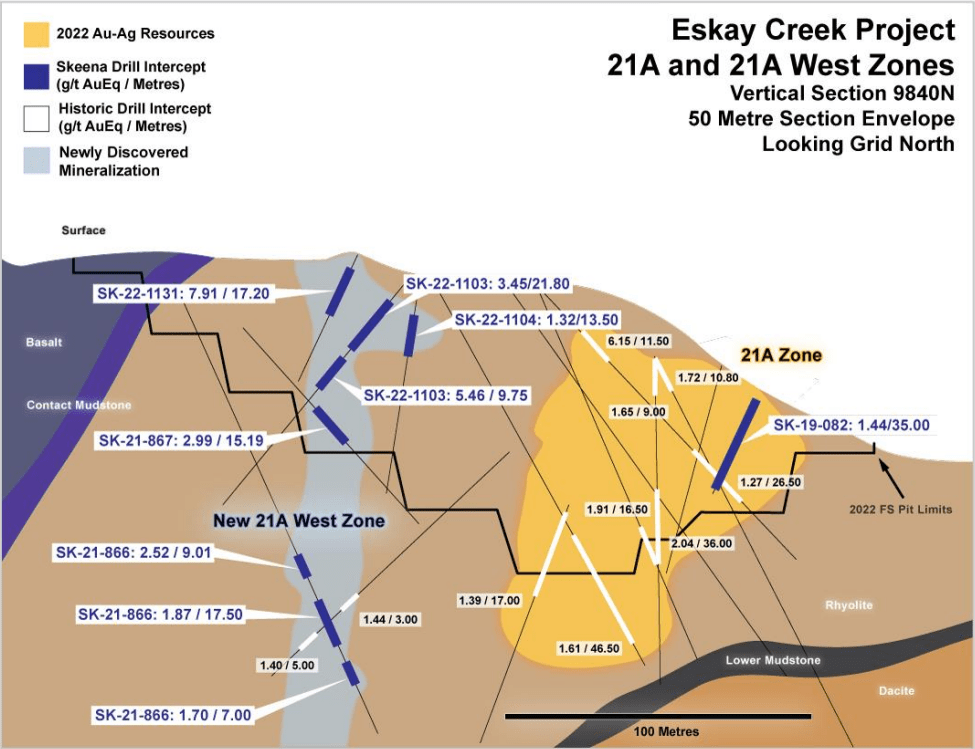

Digging into this year's drilling, there are several key takeaways, with all of them likely to have a positive impact on Skeena's updated Feasibility Study planned for late next year. For starters, the 21A West Zone is shaping up very nicely, with multiple mid-grade and high-grade intercepts outside the planned pit and in areas previously considered waste in the mine plan. Some highlights included drill hole 1122, which hit 24.00 meters at 22.38 grams per tonne of gold-equivalent, roughly 15 meters below highlight hole 1093, reported earlier this year that intersected 12.12 meters of 48.48 grams per tonne of gold-equivalent.

Meanwhile, Skeena also hit 20.60 meters at 5.51 grams per tonne of gold equivalent below the planned pit. Finally, drill hole 1131 was also helpful (17.20 meters at 7.91 grams per tonne gold equivalent), drilled 35 meters south of drill hole 1031, which intersected 50.00 meters at 2.27 grams per tonne of gold equivalent. Based on the lack of historical drilling in this area, the 21A West Zone was considered to be wasted in the recent Feasibility Study. However, with very solid drill intercepts within this area, we should see an improvement in economics in this zone in the updated FS, and it remains open along strike and at depth.

{kind=link}

Eskay Creek - 21A and 21A West Zones (Company News Release)

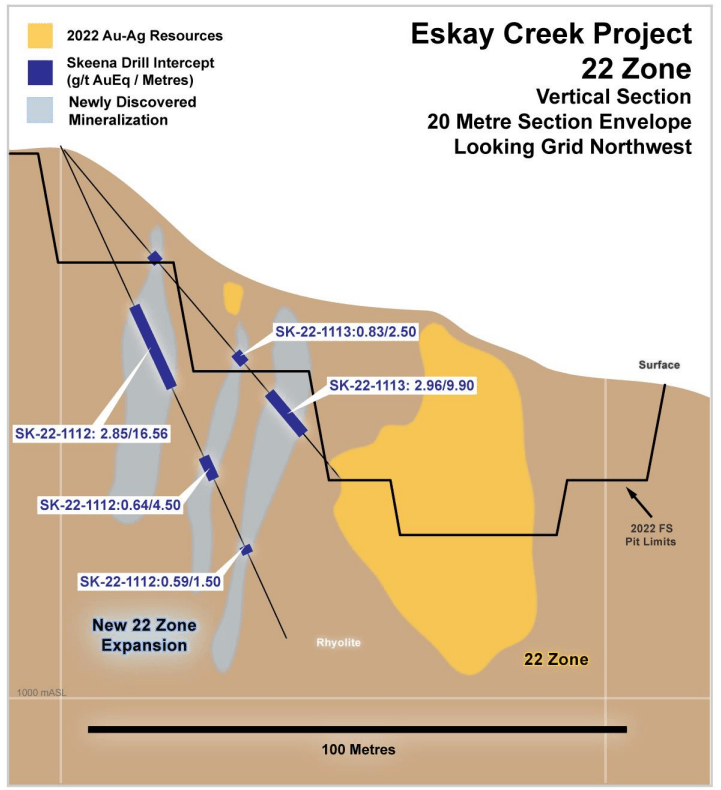

Moving to the 22 Zone, Skeena hit multiple intercepts east of this zone, with hole 1054 (200 meters east of 22 Zone and starting near the surface) intersecting 40.67 meters at 2.15 grams per tonne of gold equivalent. In addition, Skeena released additional holes at the 22 Zone last month, including 16.56 meters at 2.85 grams per tonne of gold equivalent in drill hole 1112 and 9.90 meters at 2.96 grams per tonne of gold equivalent in hole 1113 just outside of the planned pit. These results are very encouraging and could lead to an expansion of this pit to capture this new material if drilling success continues.

{kind=link}

Eskay Creek 22 Zone (Company Presentation)

While the potential expansion of the 22 Zone is positive, the more significant development appears to be the fact that previous operators ignored rhyolite-hosted mineralization near existing zones due to the 15-gram per tonne mill cut-off grade historically. If this is the case, Skeena could continue making new discoveries near existing zones to add ounces at Eskay Creek in areas that weren't considered worth focusing on historically. This could positively impact Eskay Creek's NPV (5%), given that one reason for the lower NPV (5%) despite the exceptional economics is that production dips sharply following Year 5, and the project has a relatively short mine life.

{kind=link}

Eskay Creek - 23 Zone & Project (Company Presentation)

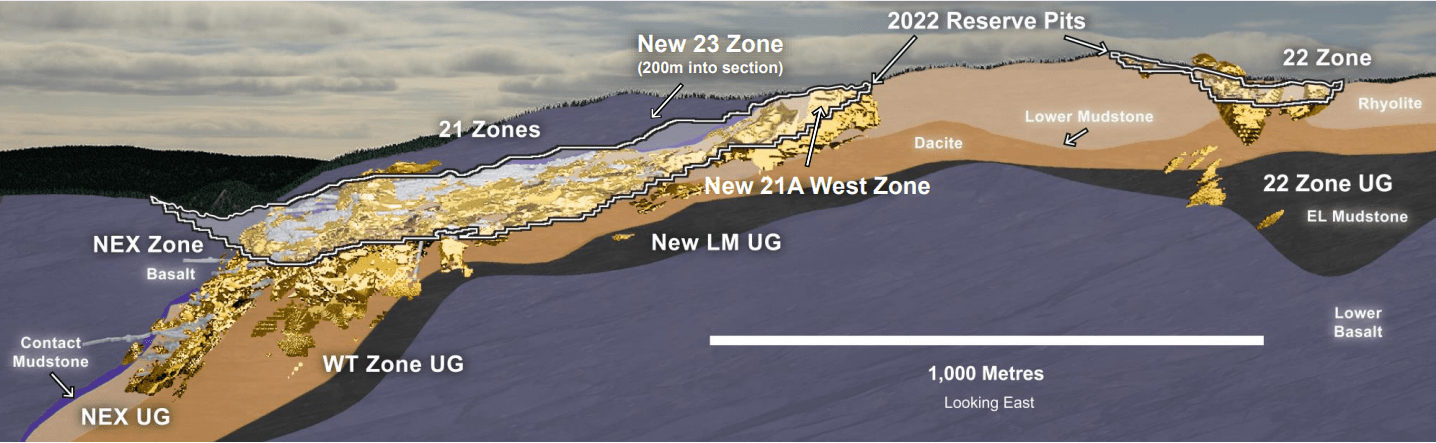

Finally, Skeena discovered the 23 Zone this year (200 meters east of the 21A Zone), which I wasn't overly excited about initially, given that grades were well below the average reserve grade at Eskay Creek. However, with Skeena continuing to expand this zone and the solid continuity experienced to date, the company has noted that the 23 Zone could potentially positively impact its project economics with an improved strip ratio, given its proximity to the Main Pit in the Feasibility Study.

To summarize, we have seen very encouraging results at three zones (21A, 23, and 22), and the underground opportunity provides a nice upside to the story, where grades have been very impressive in past drilling (5.99 meters at 12.27 grams per tonne of gold equivalent and 2.21 meters of 314.07 grams per tonne of gold equivalent) in Lower Mudstones. Let's take a look at the valuation:

Valuation

Based on ~85 million fully diluted shares and a share price of US$5.20, Skeena trades at a market cap of $437 million and an enterprise value of $416 million. This figure is a massive discount to its After-Tax NPV (5%) of ~$1.08 billion for Eskay Creek in its most recent FS, which is based on what I would argue to be conservative metals prices ($1,700/oz gold, $19.00/oz silver) considering this mine would operate from 2026-2034 assuming it is green-lighted. Using what I believe to be a fair multiple of 0.75x P/NPV to reflect Eskay Creek's robust economics and scale and Tier-1 jurisdiction, offset by weaker sentiment in the sector that has led to depressed multiples for many developers, I see a fair value for the stock of $810 million [US$9.50].

However, this valuation doesn't do Skeena nearly enough justice, in my view, given that there is considerable upside not captured in the 2022 FS. This upside includes the following:

- 40% interest in Snip (a high-grade underground project in BC) if Hochschild ( OTCQX:HCHDF ) spends $77 million before 2025 on the project (or 100% if Hochschild doesn't complete the required spending).

- An increase in ounces and an improved strip ratio in some areas of the mine plan, plus the potential to add new zones into the mine plan to extend its mine life.

- Further near-mine and regional upside at a property that is proving up mineralization wherever Skeena moves its drill rigs.

- Underground potential at Eskay Creek, with a current underground resource of ~280,000 GEOs (4.3 grams per tonne gold-equivalent) which excludes the new discovery down-dip of the NEX Zone.

{kind=link}

Skeena Eskay Creek Project & Underground Potential (Company Presentation)

I would argue that it's conservative to ascribe $300 million in incremental value to Skeena for these assets/opportunities. If we add this $300 million to its fair value of $810 million [0.75x P/NPV multiple on 2022 FS], this translates to a fair value for Skeena of ~$1.11 billion or US$11.95 per share (assuming 93 million shares fully diluted with one capital raise in 2023). Measuring from a current share price of US$5.20 translates to a 121% upside from current levels to its 18-month target price. This makes Skeena one of the most undervalued gold developers despite having one of the most robust projects with a very modest environmental footprint (low GHG emissions) in a Tier-1 jurisdiction. Hence, I see this recent pullback below US$5.20 as a gift.

{kind=link}

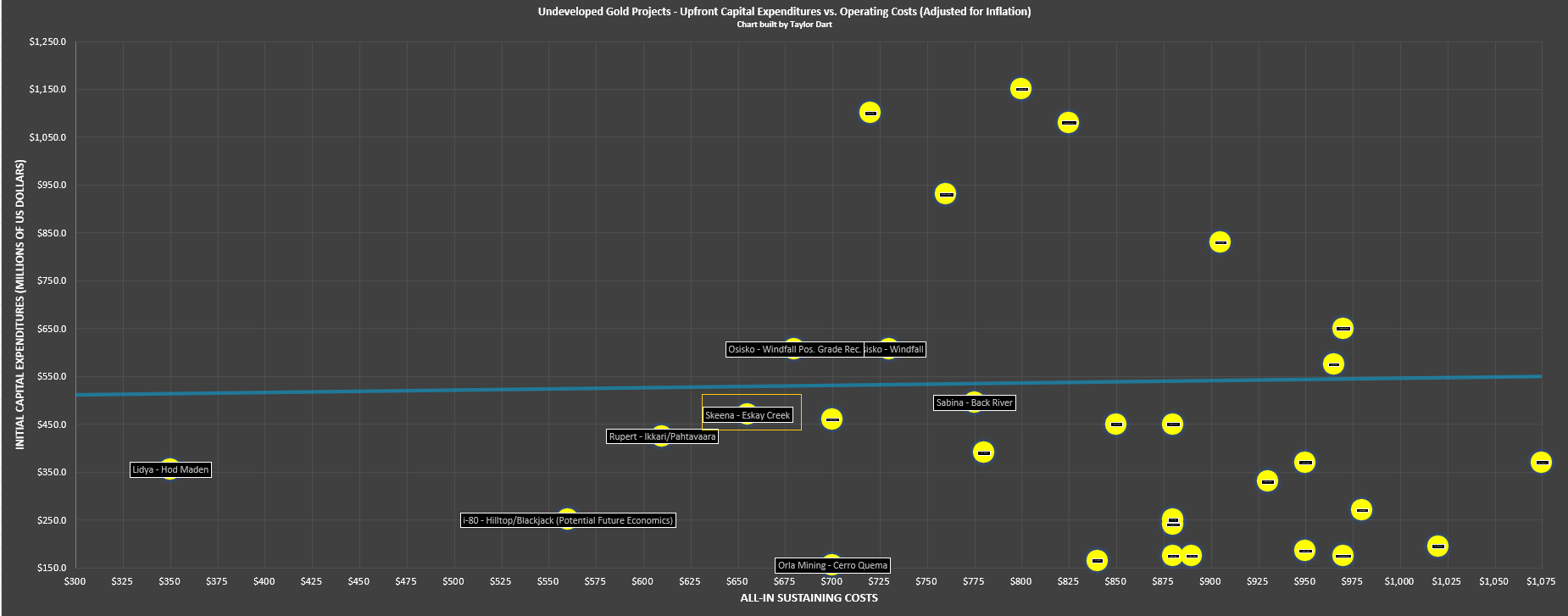

Undeveloped Gold Projects - Upfront Costs & Operating Costs vs. Eskay Creek (Company Filings, Author's Chart & Estimates)

Summary

While several gold producers have enjoyed sharp rallies off their lows, Skeena Resources has hardly participated in the recovery, impacted by an unfortunately timed capital raise and more negative news for the Albino Waste Facility. However, this has largely been offset by continued exploration success at several zones, which should augment already exceptional economics at Eskay Creek in the updated H2-2023 Feasibility Study. Notably, this underperformance has led to Skeena becoming more attractively valued from a relative standpoint vs. peers.

{kind=link}

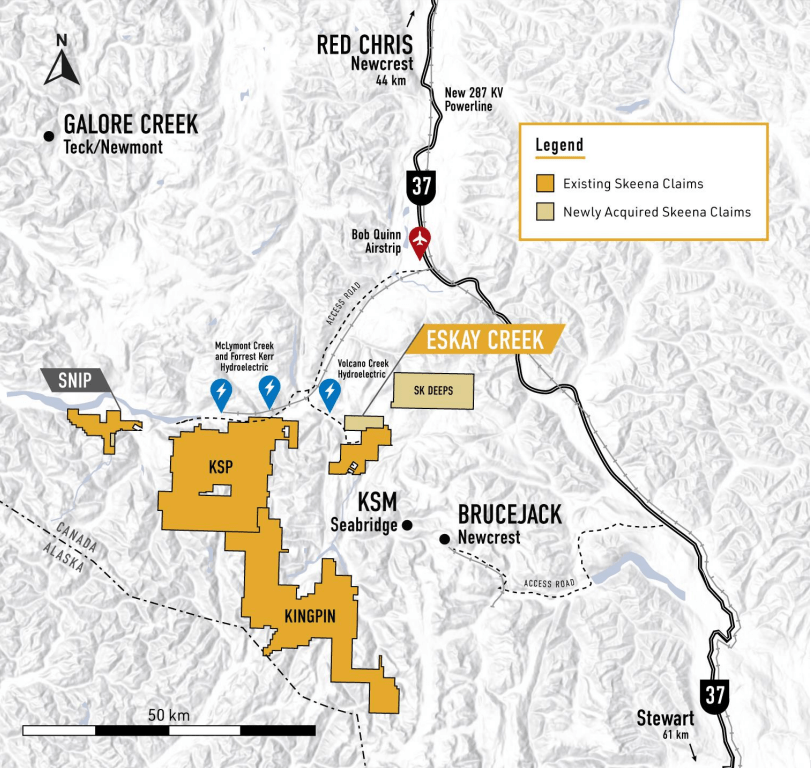

Eskay Creek Property, New Claims & Nearby Projects (Company Presentation)

In fact, Skeena trades at a ~60% FY2026 free cash flow [FCF] yield vs. an appropriate 10% FCF yield if it were to graduate to producer status. In addition, it trades at a fraction of the price paid for Pretium's Brucejack, a mine with a similar production profile but inferior margins to Eskay Creek's estimated AISC. Given this significant undervaluation from a cash flow and P/NPV standpoint, I would not be surprised by a takeover offer from a major producer, but there's considerable upside even if Skeena receives its permits and goes it alone. Given these two avenues for a re-rating, I remain long Skeena and will increase my position if we see further weakness.

For further details see:

Skeena Resources: Buy The Dips