CA - Skeena Resources: Snip Ownership Upgrades Investment Thesis

2023-05-07 08:32:06 ET

Summary

- Skeena Resources was one of the worst-performing precious metals stocks last year, declining 49% vs. a 32% decline in the ASA Gold & Precious Metals Limited Fund.

- However, the stock has clawed back a significant portion of its losses this year, up 36% year-to-date, significantly outperforming other developers like Marathon Gold, GoGold Resources, and De Grey Mining.

- I attribute the outperformance to improvement in sentiment sector-wide, Skeena now having full ownership of Snip and two major transactions in four months for other top takeover targets.

- Given that Skeena continues to own one of the highest-grade development projects globally with relatively modest initial capex relative to its production profile, I would expect sharp pullbacks to provide buying opportunities.

It's been a much better start to the year for the Gold Juniors Index ( GDXJ ), which is outperforming the Nasdaq Composite (COMPQ) and the S&P 500 ( SPY ) for a second consecutive year. And while Skeena Resources ( SKE ) investors saw significant negative returns despite the relative outperformance last year for the sector, the stock has seen a meaningful recovery since, up over 30% year-to-date and 80% off its lows. Just as important to the investment thesis for juniors, we're seeing gold majors step up to acquire juniors in full or acquire an interest in their projects. Two examples are the acquisition of half of Windfall by Gold Fields and B2Gold's ( BTG ) acquisition of Sabina Gold, two of my favorite takeover targets heading into 2023.

And while Skeena differs from both projects given that it has lower grades and is a much larger operation based on a 3.0 - 3.7 million tonne per annum throughput rate, it has similarities, including relatively modest upfront capex (~$440 million), industry-leading grades (4.0 grams per tonne gold-equivalent), and it's in a top mining jurisdiction (British Columbia), with a clear trend towards suitors favoring Tier-1 ranked jurisdictions. So, with Skeena now being one of less than ten developers left with arguably world-class projects, its attractiveness is increasing, and it doesn't hurt that the world's largest gold producer might make the Golden Triangle its new home. Let's take a look below:

{kind=link}

All figures are in United States Dollars at an exchange rate of 0.74 USD/CAD unless otherwise stated.

Hochschild Pulls Out Of Snip Project

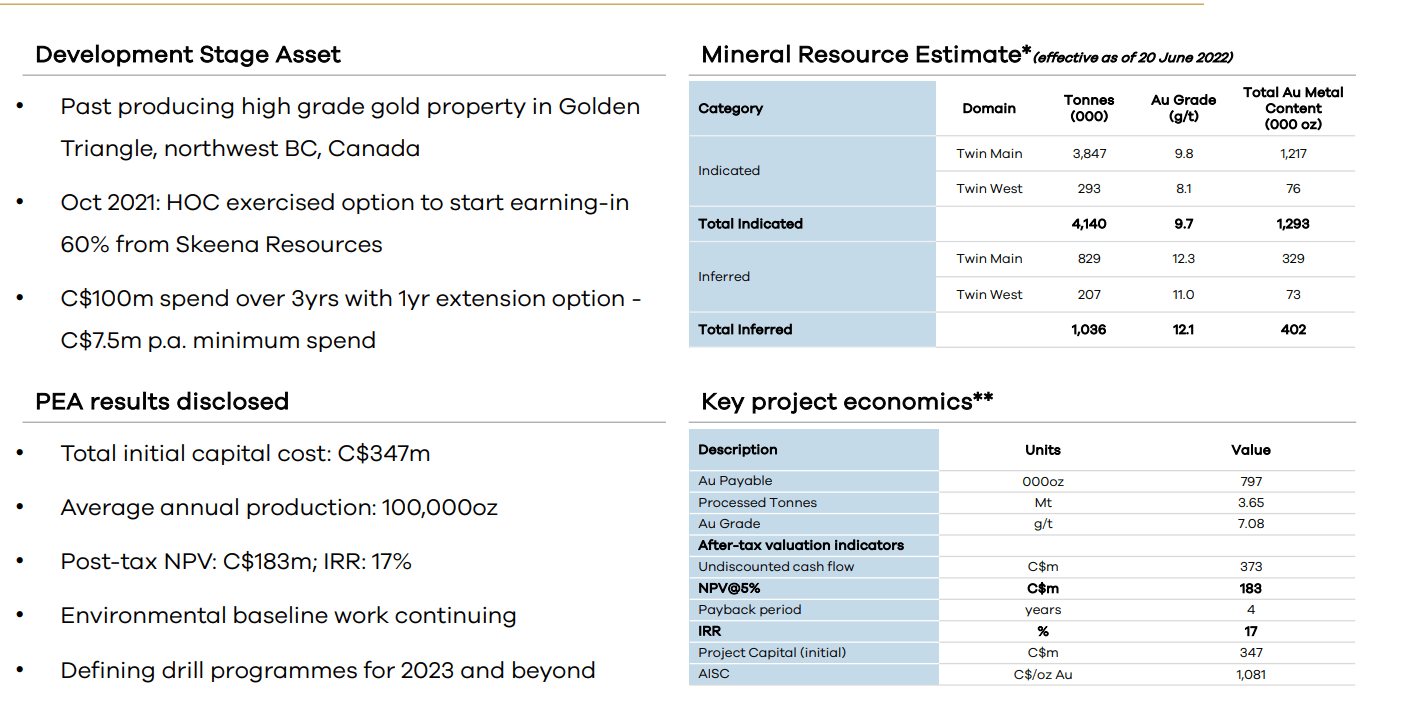

It's been a busy year for Skeena as the company works toward an updated resource estimate at Eskay Creek, project financing by year-end, and an updated Feasibility Study. And when combined with a larger resource base and higher metals prices, this should translate to an increase in the project's NPV. However, one recent development that has received little attention is Hochschild Mining's ( OTCQX:HCHDF ) decision to pull out of the Eskay Creek option agreement, with this being a significant expense to earn 60% of the project for ~$75 million. And while some investors might frown upon Hochschild passing up the opportunity own 60% of Snip, I don't see any reason to be concerned and see this as a positive.

Snip Project - Hochschild Mining (Hochschild Presentation)

{kind=link}

For starters, Snip is a relatively small asset even if it is high grade, with Hochschild proving up ~1.29 million ounces of gold at a grade of 9.7 grams per tonne of gold after spending an additional $11 million on the project in the indicated category. This is a relatively small resource to justify spending another ~$65 million just to earn 60% on, especially given that this is before mine development costs and the costs to build a plant. If this were a case of Hochschild owning 50% of Eskay Creek, pursuing the project may have made more sense. However, from a stand-alone basis, the economics weren't exceptional, with an After-Tax NPV (5%) of just ~$140 million with there likely to be additional toll milling fees to process the material at Eskay Creek.

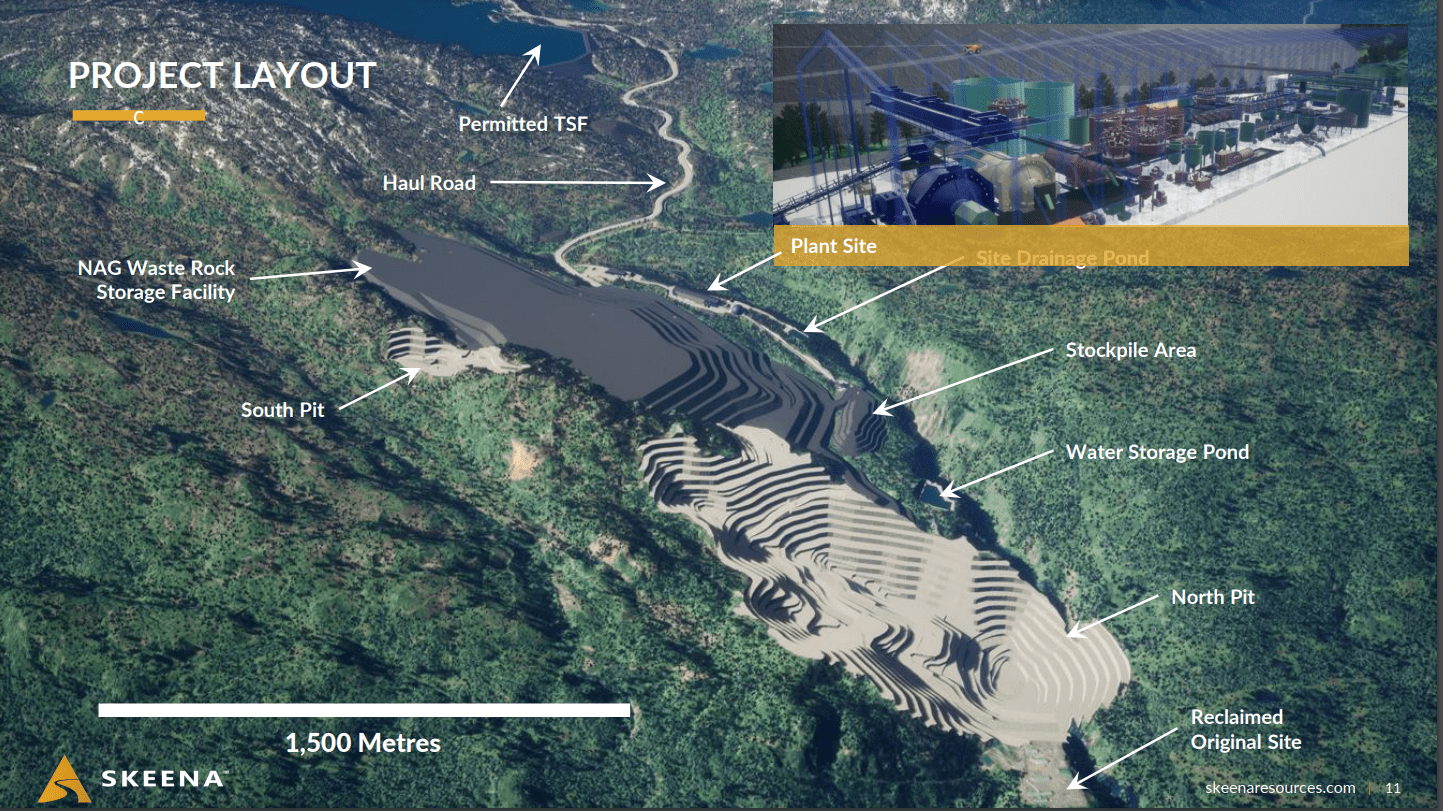

However, for Skeena, this is a very positive development, with the company potentially sitting on a reserve base of 2.5+ million tonnes at an average diluted grade of 7.0+ grams per tonne of gold. This is well above the average grade of Eskay Creek and the project is barely 50 kilometers away, offering the potential to displace some lower-grade Eskay Creek ore with higher-grade Snip material before the end of the decade. Not only does this extend the mine life and bring forward high-grade ounces, providing a further boost to Eskay Creek's NPV if it can be incorporated successfully, in addition to adding new zones to the mine life (21A West, 23 Zone, and potentially Eskay Deeps).

Eskay Creek Planned Project Layout (Company Presentation)

{kind=link}

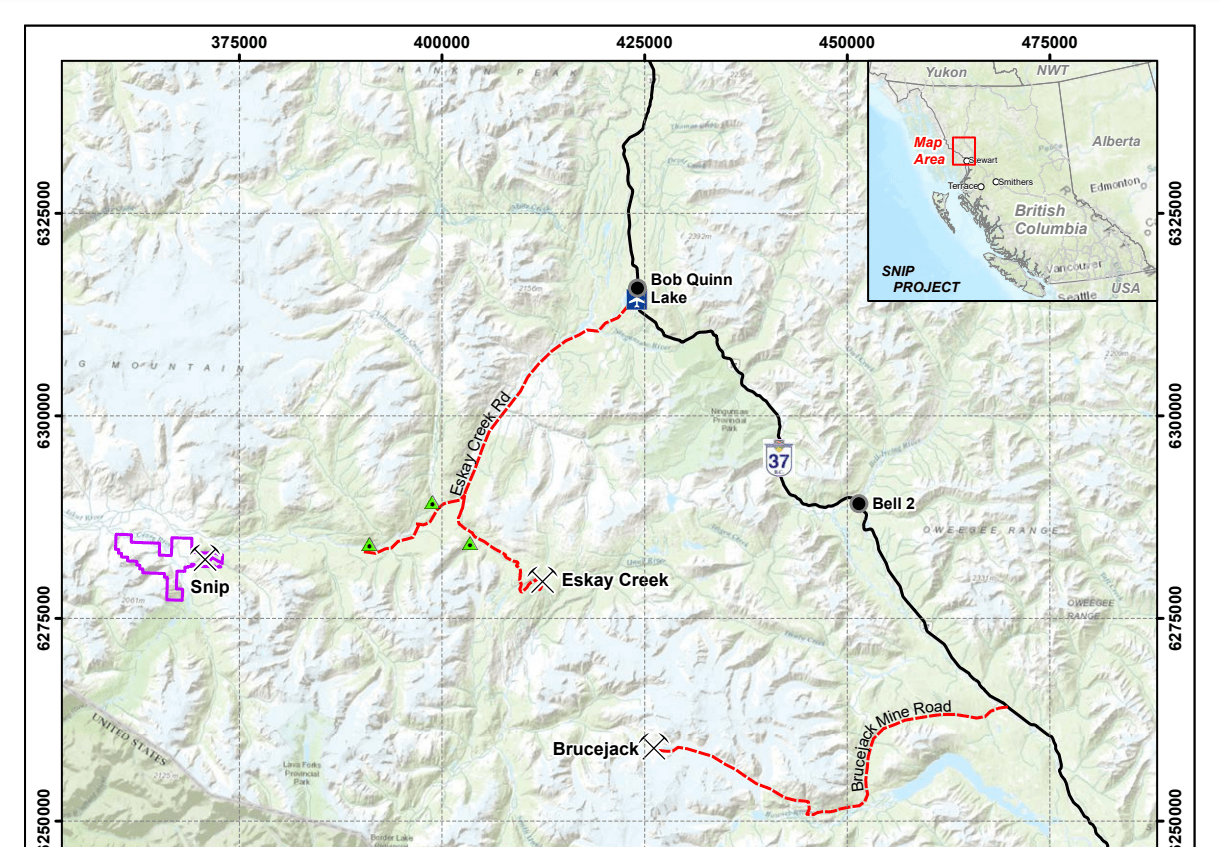

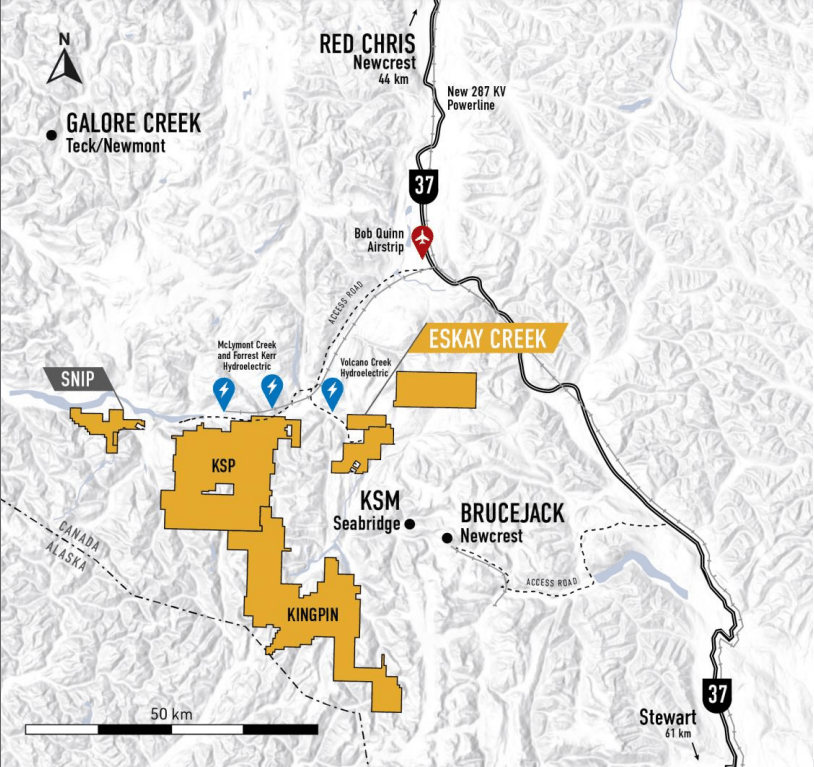

Assuming that Skeena were to haul 1,000 tonnes per day from Snip to Eskay Creek with an average grade of 7.0 grams per tonne of gold and a recovery rate of ~88%, this would translate to an additional 70,000 ounces per annum added to the mine life, pushing peak production well above 500,000 GEOs and average annual GEO production closer to 370,000 GEOs, dependent on grades and the amount of material fed from Snip to Eskay Creek each year. So, this is certainly an upgrade to the investment thesis and I would imagine relatively straight-forward permitting with this being a small footprint mine at a past-producing asset in a jurisdiction with multiple mines already in production, including Brucejack and Red Chris owned by Newcrest ( OTCPK:NCMGF ).

Recent Developments

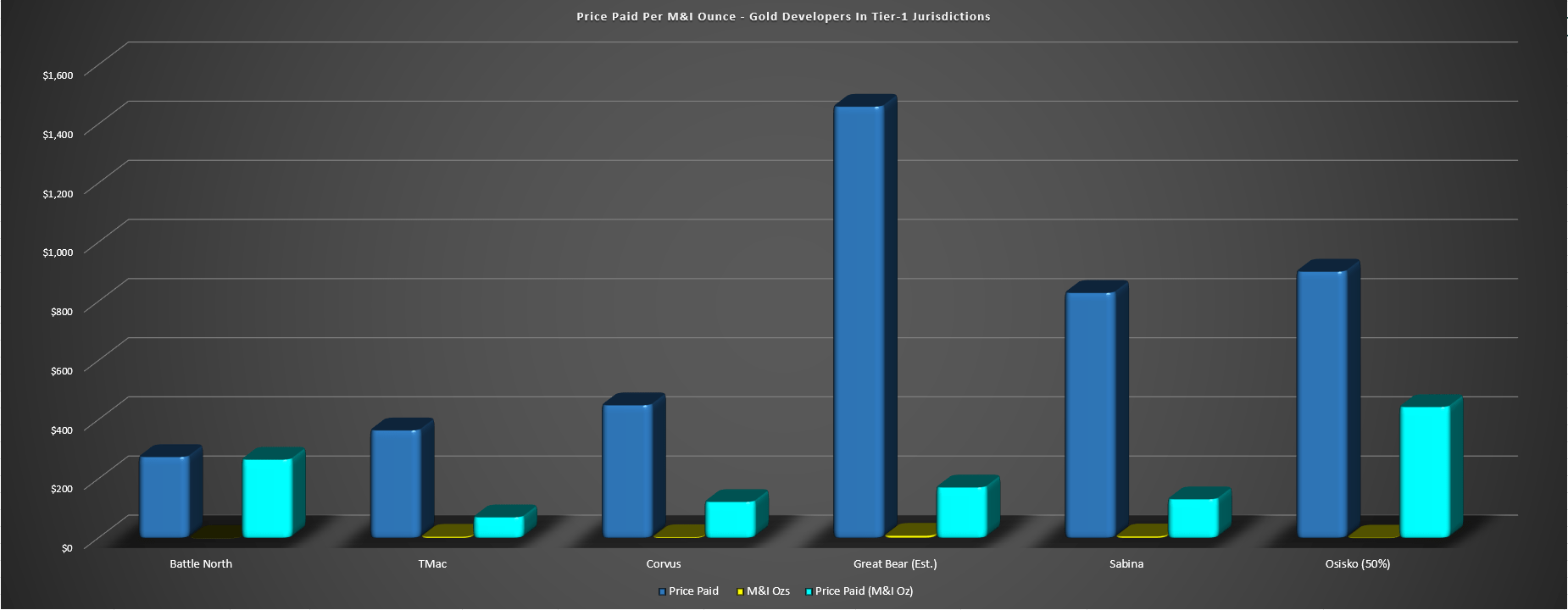

Digging into recent developments, we've now seen three major acquisitions over the past 18 months, with Kinross ( KGC ) acquiring Great Bear, B2Gold ( BTG ) acquiring Sabina, and Gold Fields ( GFI ) stepping in to acquire half of Osisko Mining's Windfall Project. In addition, Newmont ( NEM ) looks like it will be moving into the Golden Triangle to own two massive gold and gold-copper projects if its acquisition of Newcrest is successful. This could place more eyes on Skeena given that it has similar scale to Brucejack but at lower costs given that it's a high-grade open-pit operation vs. a high-grade underground operation with a very nuggety nature.

Price Paid Per M&I Ounce - Tier-1 Jurisdiction Gold Developers (Company Filings, Author's Chart)

{kind=link}

Overall, I see these developments as quite positive for Skeena and juniors in general, assuming those juniors have solid projects in safe jurisdictions. And with Skeena potentially beefing up Eskay Creek with the ability to spike grades if it hauls material from Snip and with it having a larger land package following last year's acquisition, one could argue it has a target on its back as intermediate producers and majors scour the sector for the best remaining undeveloped projects. Finally, given the price paid in recent acquisitions of well over $100.00/oz for M&I resources, it's clear that Skeena is undervalued, especially if it can continue growing its already large M&I resource base (~6.4 million GEOs with Snip per Hochschild's most recent resource estimate).

Valuation

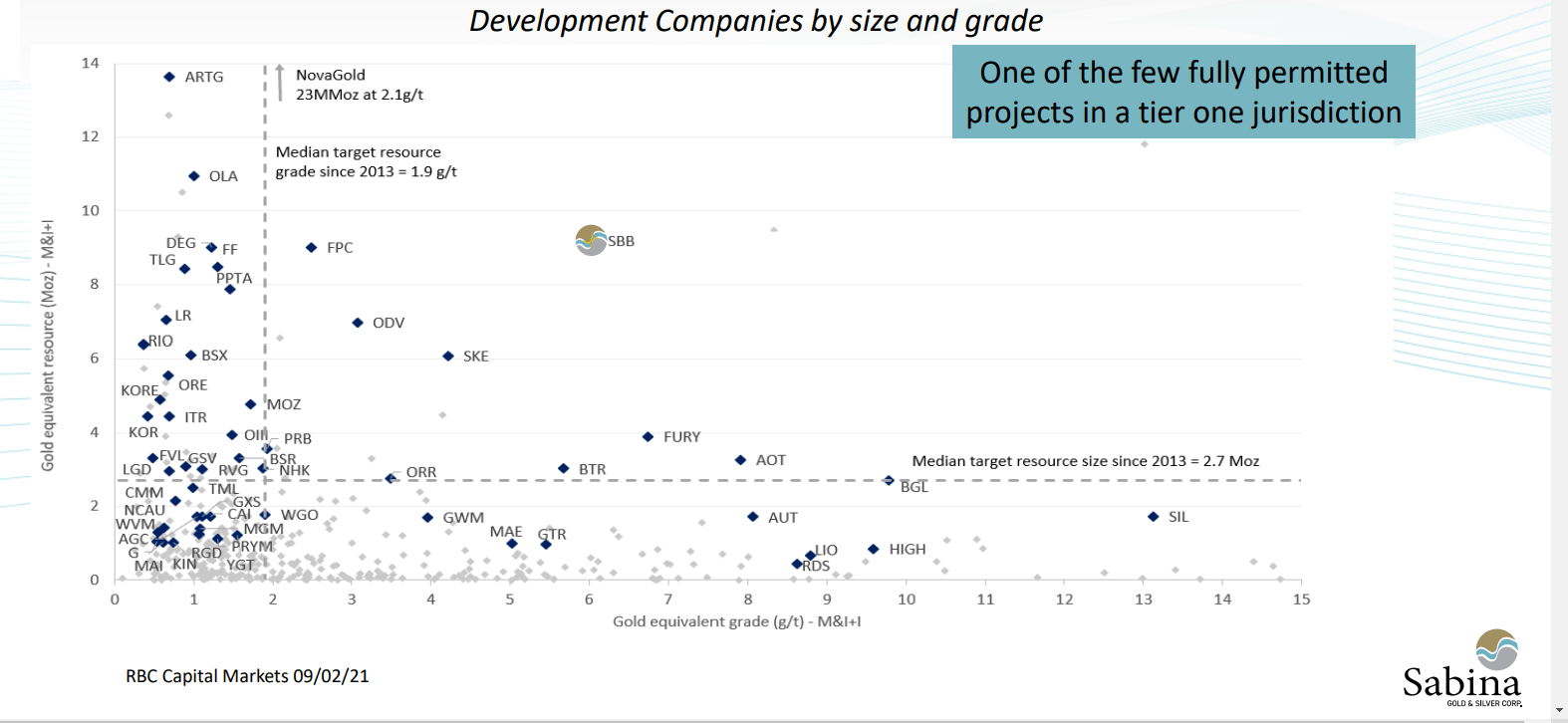

Based on ~85 million fully diluted shares and a share price of US$7.25, Skeena trades at a market cap of ~$612 million, a very reasonable valuation for a company sitting on a global measured & indicated resource base of ~6.4 million GEOs that looks like it could ultimately grow to 7.0+ million GEOs even without Albino Lake (21A West Zone, 23 Zone, 22 Zone Expansion). This translates to a valuation of just ~$95.60 per gold-equivalent ounce even before any resource expansion, below that of Sabina Gold & Silver which B2Gold recently acquired for a price of ~$132.00/oz on M&I resources.

Development Companies by Size & Grade (Pre-Sabina Acquisition) (Sabina Gold Presentation)

{kind=link}

That said, Sabina was fully funded for construction with significant underground development already complete, it had a permitted project, and deserved a significant premium given that it was a district play with the company having an 80-kilometer gold belt in Nunavut with an iron formation triple the size of Goose (main deposit) 50 kilometers north at George. This suggests that B2Gold likely scooped up what will ultimately be at least 8.5 million M&I ounces of gold for ~$830 million, resulting in a price paid of closer to ~$100.00/oz on future M&I resources. Based on this comparison and under the assumption that Skeena is likely to increase resources, the stock continues to look undervalued even after its recent rally.

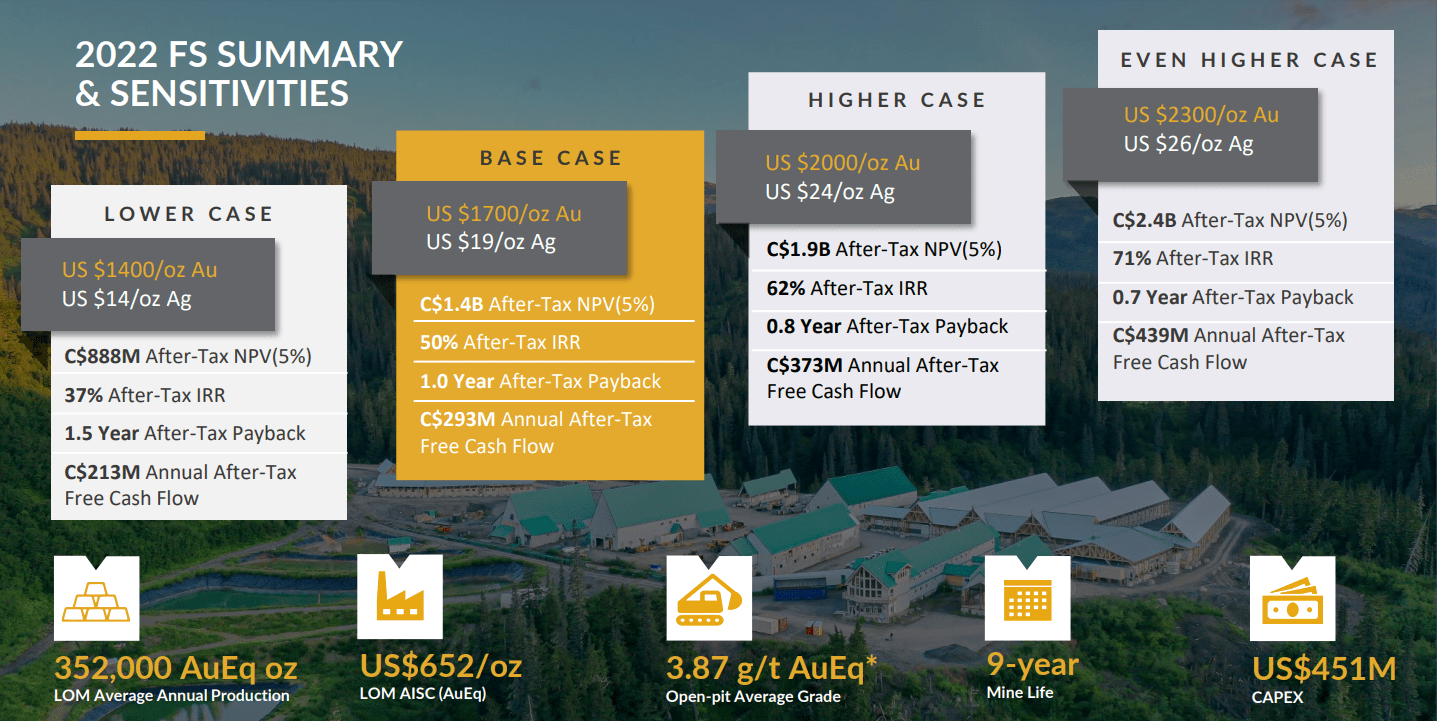

keena - FS Summary & Gold Price Sensitivity (Company Presentation)

{kind=link}

As shown above, Skeena is significantly undervalued at current prices, with an estimated After-Tax NPV of ~$1.40 billion at a 5% discount rate using metals prices closer to spot at $2,000/oz gold and $24.00/oz silver. However, I would argue that it's always best to bake in some additional conservatism for projects that won't begin construction for at least another year in an inflationary environment and won't begin operations for at least three years. And if we use more conservative assumptions for mining/milling costs and initial capex, the estimated After-Tax NPV (5%) of ~$1.40 billion looks rich.

Initial capex has been estimated at $438 million (C$592 million) to build Eskay Creek, but I think a safer estimate is $490 million given that while we may have seen peak inflation, I think it's more realistic to assume continued pressure on labor costs due to the shortage of skilled labor, especially in prolific mining jurisdictions.

While this still points to a significant upside to fair value given that Skeena still trades at barely half of its estimated After-Tax NPV (5%) under more conservative assumptions on a fully diluted basis, I would argue that the discount rate being used for developers is far too low given the current cost of capital, the current risk-free rate, and that pre-permitted and pre-financing gold developers are much riskier than gold producers. This is because in the latter case, the asset is in production, there's a low likelihood of major surprises from a grade or metallurgy standpoint due to quarterly production figures being available, and permits have already been granted to provide visibility into future production. Hence, I think a more conservative discount rate to use for gold developers like Skeena is 8.0%.

After factoring in some grade upside from eight years of mining at 1,000 tonnes per day from Snip being fed to the Eskay Creek Plant (2029-2036), an additional three years of open-pit mining at Eskay Creek (albeit at lower grades) with lower-grade reserves added at new zones and more conservative mining costs/milling costs (plus higher mining/transport costs at Snip), the estimated After-Tax NPV at an 8% discount rate comes in at ~$930 million. This After-Tax NPV (8%) figure is based on a $1,900/oz price for gold and a $25.30/oz price for silver, well above the three-year average price for both metals but slightly below spot levels.

Snip Project Location (Snip Technical Report)

{kind=link}

Based on what I believe to be a fair multiple of 1.0x P/NAV at this 8% discount rate (given that Skeena has a world-class project in a safe jurisdiction), I see a fair value for Skeena of ~$930 million, or US$10.80 per share on a fully diluted basis. And while this more conservative estimate of fair value points to a 48% upside from current levels, I am looking for a minimum 50% discount to fair value to justify starting new positions in sub $1.0 billion market cap names in the developer space. After applying this discount to Skeena, the ideal buy point comes in at US$5.45 or lower, where I initially highlighted the stock as attractive earlier this year.

Skeena Article - December 2022 (Seeking Alpha Premium)

{kind=link}

The other risk worth considering is that Skeena has not yet financed Eskay Creek and while I would expect any financing to be a mix of primarily debt and limited equity given the rapid payback, I don't think it's unreasonable to assume a minimum of $150 million in equity, which would translate to ~19 million shares at a share price of US$8.00. This could put pressure on the stock depending on the price where capital is raised given that this would translate to ~22% share dilution, even if the project would be more de-risked with financing in place. So, while I continue to Skeena as one of the best developers sector-wide and a top takeover target, especially with Osisko Mining ( OTCPK:OBNNF ) no longer available to majors, I don't see this as a low-risk buying opportunity.

Takeover Potential?

This view that Skeena is no longer in a low-risk buy zone does not factor in what a suitor may pay in a takeover scenario, and with the world's largest gold producer set to move into the Golden Triangle next year, this is certainly an asset that Newmont could inspect closer if the Newcrest deal goes through. That said, both Newcrest and Newmont have relatively heavy capex schedules between Red Chris Block Cave, Lihir Phase 14A/Seepage Barrier, Cadia PC1-2, Havieron, Ahafo North, Tanami Phase 2, and potentially Yanacocha Sulfides. So, unless Newmont does some portfolio rationalization following the deal, I'd be surprised if it made another acquisition, even if Eskay Creek is a top-10 undeveloped gold project globally.

Eskay Creek Location & Infrastructure (Company Presentation)

{kind=link}

However, there are still several other companies that would love to get their hands on a project with sub $800/oz all-in sustaining costs, especially after three years of margin compression has put a severe dent in the average gold producers' profitability even after factoring in a $1,900/oz plus gold price. So, if one is of the view that Skeena will inevitably be acquired at a premium, my fair value estimate is likely far too conservative. That said, I prefer to make conservative assumptions when assessing fair value and if a stock is still significantly undervalued, I will gladly invest. And in Skeena's case, I think there are more attractive opportunities elsewhere following Skeena's 80% move off its lows.

Summary

Skeena has had a solid year thus far it securing full ownership of Snip with an additional ~$11 million of work compliments of Hochschild after the company pulled out of the project and continued near-mine exploration success. And with gold prices rising and large gold producers generating meaningful free cash flow despite the impact of inflationary pressures on their cost profiles, one could argue that we could see a couple more takeovers this year which should continue to place a bid under juniors as investors speculate on which name is next to be acquired.

That said, while the rising gold price and recent transactions in the sector are positive, Skeena is now up over 85% from its Q3 2022 lows and much of the easy money has been made here. This doesn't mean that the stock can't go higher and there continues to be value left here, especially if gold prices remain above $1,950/oz. However, I prefer to buy when stocks are hated, and it's hard to argue that sentiment is nearly as favorable for starting new positions when several miners are up over 80% from their Q3 2022 lows. Hence, if the strength in Skeena's share price persists, I would view any rallies above US$8.55 before July as an opportunity to book some profits.

For further details see:

Skeena Resources: Snip Ownership Upgrades Investment Thesis