CA - Sleep Country: A Dirt-Cheap Valuation For This Small-Cap Retailer

Summary

- Sleep Country has suffered a 53% drawdown from its 2021 highs, impacted by a softer-than-expected Q3 report with a clear shift in consumer behavior.

- While this has resulted in some uncertainty near-term and is likely to result is a decline in annual EPS next year, Sleep Country is well positioned to weather any storm.

- In fact, it should emerge stronger than ever with it being likely that it will continue to grow market share, potentially benefit from opportunistic M&A, and retire shares at attractive levels.

- So, with the stock heading down to oversold levels and trading at ~8.0x earnings with a nearly 4.0% dividend yield and potentially a 5.0% yield on cost, I would view any further weakness in the stock as a buying opportunity.

The S&P 500 ( SPY ) is on track for its worst year since 2008, down ~17% year-to-date, and the bulls will have to put up a strong fight to close out the month of December on a positive note. However, while index investors have taken a beating, the Retail Sector ( XRT ) has seen a major hit, down nearly 30% for the year, with some weaker names re-testing their March 2020 lows. In the case of Canadian stock Sleep Country Canada ( ZZZ:CA ), the stock may be well above its March 2020 lows, but it's been decimated, suffering a 53% drawdown from its 2021 highs.

While a decline of this magnitude in Sleep Country's stock might seem justified for a company selling higher-ticket items in a recessionary environment with the reverse wealth effect taking its toll, I would argue that a lot of this negativity is already priced in. In fact, Sleep Country is now trading at just 8x forward earnings estimates and paying a nearly 4.0% dividend yield, plus returning another ~6.0% to shareholders through opportunistic buybacks. So, for patient investors willing to be contrarian, I would view any further weakness in the stock as a buying opportunity.

Cat Sleeping (Author's Photo)

Introduction & Q3 Results

Sleep Country Canada was founded in 1994 with four stores in Vancouver and has since grown to nearly 300 stores with multiple brands. These include its main Sleep Country brand (Dormez-Vous in Quebec) and two recent acquisitions: Endy and Hush. The latter is known for its weighted blankets and is one of Canada's fastest-growing digital retailers, with the acquisition closing late last year. From a revenue standpoint, Sleep Country's revenue is split roughly 80% towards mattresses and 20% towards accessories, and it is Canada's leading specialty sleep retailer with a network of 20 warehouses and growing partnerships with retailers, including Best Buy ( BBY ) and Walmart ( WMT ).

{kind=link}

Sleep Country Offerings (Annual Report)

Overall, the company had a blow-out year in 2021 with strong same-store sales growth and an incremental contribution from Hush (closed in October 2021), reporting record consolidated annual revenue of $920.2 million. This represented 21.4% growth year-over-year. Notably, it also surpassed 520,000 transactions since the acquisition of Endy (2018) with impressive satisfaction scores (4.6/5 stars on Endy.com). From an earnings standpoint, Sleep Country's results were even more impressive, reporting annual EPS of $2.64 (+36%), a new record for the company.

{kind=link}

Sleep Country Brands (Company Report)

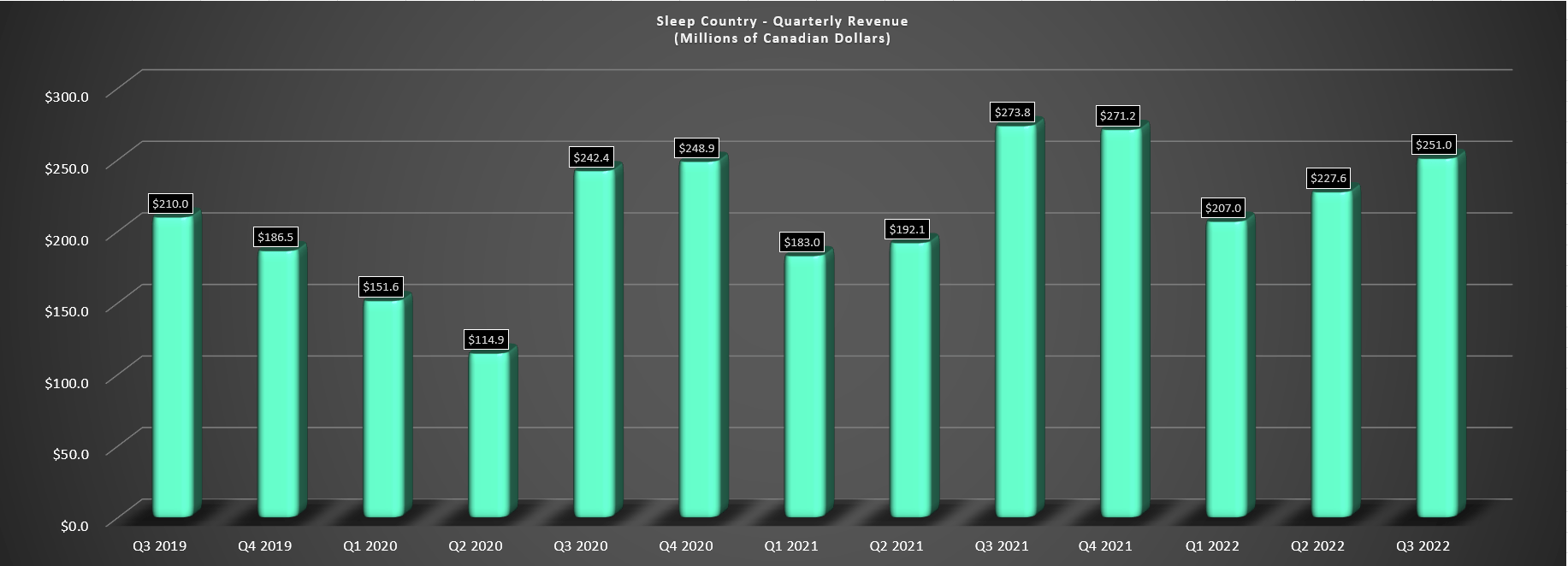

Unfortunately, while 2022 started strong with 13.1% revenue growth and 18.4% revenue growth, respectively, we saw a meaningful slowdown in Q3, with revenue coming in at just $251.0 million, down 8.3% year-over-year. Sleep Country's CEO, Stewart Schaefer, noted that consumer spending changed rapidly as the quarter progressed and also relayed the unfavorable outlook that the negative consumer confidence and macro headwinds are likely to continue to impact the business in Q4 of this year. While this is undoubtedly disappointing, and the stock found itself down over 5% on the news (November 7th), it managed to claw back to nearly flat for the day, and the stock has been trying to build a bottom since the report.

{kind=link}

Sleep Country - Quarterly Revenue (Company Filings, Author's Chart)

It's easy to be pessimistic about the Q3 results with a clear deceleration in revenue growth, but there are some important points worth unpacking. For starters, while revenue was down sharply, the company was lapping tough comps from Q3 2021, with this being the best quarter in the company's history. This was partially due to pent-up demand from Q2 2021 that was shifted into Q3 2021 as stores were closed for 33% of operating days in Q2 2021 and re-opened in June. The result was that revenue that would have otherwise contributed to June 2021 sales moved into the following quarter, creating new insurmountable comps.

This unusual boost in sales due to timing combined with the headwinds from the reverse wealth effect (lower stock prices, housing prices, and crypto prices), it's not surprising that the company could not successfully lap these Q3 2021 sales with positive growth. Still, the company's three-year sales growth rate remains firmly in positive territory despite the challenging macro backdrop, with revenue up ~20% vs. Q3 2019. In addition, gross margins remained strong, coming in at 38.5%, a 100 basis point increase from the year-ago period. This is a significant deviation from most retailers that have seen a sharp decline in sales and margins, leading to a substantial give-back from an earnings standpoint, like Abercrombie ( ANF ).

{kind=link}

Sleep Country's solid margin performance was driven by an increase in its average unit selling prices offset by higher product and delivery/transport expenses, and operating EBITDA margins are sitting at 24.1% year-to-date, sitting 120 basis points ahead of year-ago levels and continue to sit at multi-year highs, well above the ~18.6% three-year average pre-COVID-19. Most importantly, though, the company continues to stick to its strategic plan despite the slowdown and will open five stores this year (~2% growth), has opened a pop-up experiential store for Hush at Yorkdale (Toronto), and has expanded its partnership with Walmart, bringing the total number of shop-in-stores to 17, up from 10 previously.

Positioning vs. Peers & Outlook

While it's easy to be negative on Sleep Country after softer Q3 results, and the Canadian housing market undoubtedly came into this slowdown at much frothier levels than the United States (translating to a higher risk of a pullback in consumer spending), Sleep Country is in a unique position. This is because it is the leader by a wide margin in Canada in the sleep category and has gobbled up the potential future competition with its acquisitions of Endy and Hush over the past few years. Additionally, the company has invested in start-up company Sleepout (25% ownership for $500,000), with this company offering portable blackout curtains, giving Sleep Country another low-risk entry into what could be a budding growth story in sleep accessories.

{kind=link}

This commanding position with a huge lead over the competition suggests it should have the pricing power to raise prices strategically in some areas while keeping prices low in what it deems as products that are more sensitive to price increases. Additionally, while Sleep Country's mattresses, pillows, sheets, and other accessories are not a staple, a trend toward healthier living is a tailwind for the industry. Plus, even if these are discretionary purchases, its products are functional and critical to one's health. In fact, the cumulative effects of sleep loss and sleep disorders can have multiple negative consequences, including increased risk of hypertension, diabetes, obesity, and depression.

Given this positioning as a leader in providing sleep products with a growing retail presence and a vast distribution network to ensure it is quicker and more efficient than the competition regarding delivery, a critical component of customer satisfaction. This superior positioning was strengthened by the announcement that it would be opening two new storage hubs in Calgary, Alberta, and Belleville, Ontario, supporting its plans for continued aggressive growth. Finally, when it comes to the medium-term outlook due to the weaker economic environment, the company's commentary was positive and was as follows:

"Believe it or not, we prefer the pause than the trading down because in past recessions, if we're going there or slowdowns, it's a purchase that is put off. It's not the restaurant business or the fashion industry in terms of clothing where you miss a season; they push it off. So, if a customer trades down from a $1,500 bed to a $1,000 bed and they’ve now exited the market for the next eight to 10 years, that concerns us. So, even though it's painful when things slow down a little bit, we have not seen trading down."

- Sleep Country, Q3 Conference Call

This dip in foot traffic vs. trading down is very positive news for Sleep Country, as explained above, given that mattresses are typically multi-year purchases, and a trade-down can significantly impact sales as they are waiting years to see that customer visit again for a high-ticket purchase. So, while the slowdown is negative, I would be surprised to see a shift to trading down, especially with the increased awareness of sleep as a critical component of health vs. past recessions. To summarize, this slowdown and a slight pullback in earnings next year will pass, and Sleep Country will likely emerge stronger than ever, just as many large restaurant brands have due to their weaker competition being forced to spend less on marketing or potentially close underperforming stores.

Earnings Trend

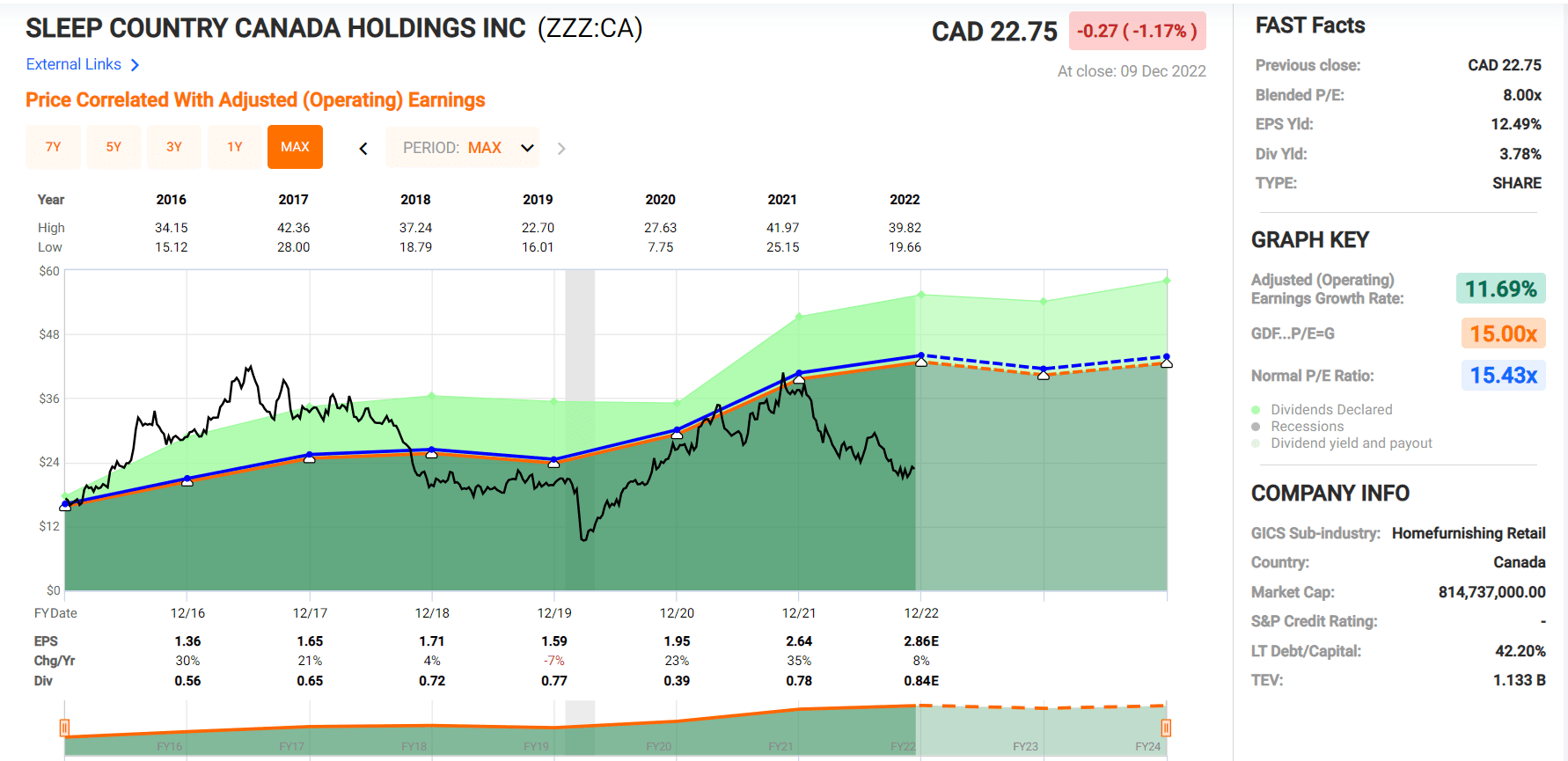

If we look at Sleep Country's earnings trend below, we can see that it's enjoyed a ~16.6% compound annual EPS growth rate since FY2015, despite wading through a global pandemic. However, based on FY2022-FY2024 estimates, this growth rate is expected to slow materially. This isn't surprising given that consumer confidence has taken a hit and mattresses/accessories are a discretionary category even if they are clearly functional and key to one's health due to the importance of consistently productive sleeping patterns.

{kind=link}

Sleep Country - Earnings Trend (Company Filings, Author's Chart, FactSet)

As shown in the chart above, Sleep Country is expected to report growth in annual EPS this year ($2.86 vs. $2.64), but annual EPS is expected to dip next year to $2.71 and only make a slightly higher high in FY2024 with estimates of $2.85. Assuming Sleep Country only meets these estimates, this would result in a 490 basis point decline in its compound annual EPS growth rate vs. FY2015 levels (11.7% vs. 16.6%). Often, a slowdown in a company's earnings growth rate of this magnitude can lead to multiple compression for a stock, so this material deceleration is not ideal.

Based on this earnings trend alone, one might conclude that Sleep Country is not an ideal buy-the-dip candidate, with just ~12% growth in annual EPS expected from FY2021 to FY2024 and the Canadian economy in a position for a hard landing. However, a recessionary environment and the reverse wealth effect certainly aren't ideal for Sleep Country's business; the company could actually benefit from a prolonged slowdown with the potential to add A-rated properties, scoop up market share as competitors may be forced to spend less on marketing, and potentially also open opportunistic M&A. As former Intel ( INTC ) CEO Andy Groves stated:

"Bad companies are destroyed by crises; good companies survive them; great companies are improved by them".

And, as we have seen from Sleep Country's track record of accretive M&A to date, an economic crisis like we could be in store for certainly wouldn't be the end of the world, especially with Sleep Country coming into this slowdown with a solid balance sheet, allowing it to continue retiring shares at depressed levels. In fact, Sleep Country is on track to repurchase over 2.25 million shares in 2022 alone, representing more than 6.0% of its outstanding shares, making this one of the most aggressive NCIBs executed by companies trading on the Canadian Stock Exchange this year.

{kind=link}

Perhaps the most important point worth highlighting is that whether one believes we're likely to see a prolonged pullback in consumer demand or a softer landing, Sleep Country has already seen a significant contraction in its multiple, which has taken this risk off the table. In fact, Sleep Country is trading at its cheapest levels in years, with the only time it's been more undervalued being the March 2020 lows when it briefly traded down to ~5x trailing earnings. In this case, the company doesn't have all of its stores closed as it announced in mid-March 2020 , yet it's trading at less than 8x FY2022 earnings estimates ($2.86).

Valuation

Looking at the chart below, we can see that Sleep Country has historically traded at 15.4x earnings and closer to 13.0x earnings over the past five years. Even if we use what I believe to be a brutally conservative multiple of 10.8x earnings (30% discount to its historical multiple of 15.4) to adjust for the challenging landscape and assume a 3% miss on current FY2023 earnings estimates ($2.63 vs. $2.73), this would result in a fair value of $28.40. If we measure from the current share price of $22.60, this translates to a 26% upside from current levels.

{kind=link}

Sleep Country - Historical Earnings Multiple (FASTGraphs.com)

Understandably, a 26% upside might not interest investors all that much, and this is fair given that many more liquid large-cap names have also corrected sharply and are offering significant upside to fair value. However, it's important to note that Sleep Country could return another 10% to shareholders next year alone from dividends and share buybacks. In addition, while it may only be paying a ~3.8% yield currently, which might not seem all that alluring, this company could offer a forward yield of nearly 5.0% for those investors willing to be patient. This is because the company would still have a very modest payout ratio even at $1.06 annualized (a 24% increase from current levels). And this modest payout ratio is relative to what will likely be a trough for earnings.

So, after adding in upside from dividends and share buybacks, the total return potential here looks to be ~36% to its 1-year target price, but this assumes a miss on earnings and assumes that the stock continues to trade at a significant discount to its historical multiple. So, even under very conservative assumptions, I see Sleep Country as very attractively valued as it sits below $22.60 per share.

Technical Picture

Moving to the technical picture, we can see that Sleep Country has strong support at C$21.00 and no strong resistance until C$31.85. This translates to a reward/risk ratio of 5.80 to 1.0, with $1.60 in potential downside to support and $9.25 in potential upside to resistance. Generally, I want a minimum 5.0 to 1.0 reward/risk ratio to justify entering new positions in small-cap stocks. As the expected support/resistance range suggests, Sleep Country easily meets this criterion despite rallying 10% off its lows since Q3 earnings. Given this attractive setup, I have started a new position in the stock at C$21.25 and added to my position under C$20.00.

{kind=link}

ZZZ.TSX - Weekly Chart (TC2000.com)

Summary

Sleep Country investors have enjoyed a ~7.4% compound annual growth rate in dividends since FY2015 and a phenomenal annual EPS growth rate of ~16.6% in the same period. Not surprisingly, this resulted in strong share-price performance since its public debut in 2015 (~200% return). Unfortunately (for investors), this outstanding execution has made it difficult to buy the stock at an attractive multiple. However, for investors that missed the March 2020 correction, which was certainly a trickier period to invest in retail names due to store closures, we are now seeing a rare opportunity to buy the dip in this steady growth story with a commanding position vs. peers in the sleep category.

This is evidenced by the fact that Sleep Country now trades at roughly half its average earnings multiple since inception and could potentially offer a Canadian-bank-like yield for those that are patient, with room to grow its dividend to C$1.12+ by year-end 2025 (~5.0% yield). Just as importantly, I see Sleep Country as an attractive way to diversify one's portfolio with a lack of consistent growth stories in the Retail Sector on the TSX trading at attractive valuations (double-digit free cash flow yields). Hence, I see the stock as offering a rare mix of growth and value at current levels, and I would view any further weakness in the stock as a buying opportunity.

For further details see:

Sleep Country: A Dirt-Cheap Valuation For This Small-Cap Retailer