SNBR - Sleep Number's Rising Potential: A Bottom In Sight Despite Short-Term Losses

2023-07-24 11:12:38 ET

Summary

- Sleep Number's stock has seen a consistent downward trend over the past two years due to poor profitability, but there are signs of potential future growth.

- The company has suspended share buybacks and prioritized debt repayments in response to declining profitability and increased interest rates.

- Despite substantial debt and declining profitability, the company's stock seems to be undervalued, and a return to pre-Covid19 margins could lead to a significant increase in stock price.

Introduction

Sleep Number's ( SNBR ) stock price has experienced a consistent downward trend over the past 2 years, wiping out all the gains and even exceeding the post-Covid19 boom. The decline appears to be justified, given the company's reported poor profitability during this period. However, there are promising indications of strong catalysts emerging, which could lead to a more favorable return in the future. For investors seeking a slightly higher risk/reward opportunity, Sleep Number might be an appealing option to consider.

Capital Allocation

Sleep Number has demonstrated a consistently aggressive approach to capital allocation over the years, relying on substantial debt while distributing more money than earned, resulting in negative shareholder equity. While this strategy might have been sustainable during prosperous times, it has impeded the process of stabilizing the business and allowing its stock to resume EPS growth. Moreover, the recent increase in interest rates has further strained the company's profitability, which has already taken a hit.

However, in the most recent quarterly report, there are positive signs that the fundamentals are slowly starting to stabilize, as the stock exceeded EPS estimates by $0.21, reporting $0.72 per share. In response to the decline in profitability, the management has chosen to suspend share buybacks and prioritize debt repayments. While this decision is prudent, it is unfortunate that the company is unable to capitalize on its low valuation.

During the latest quarterly earnings call , management conveyed their plan for capital allocation for the rest of the year. The Chief Financial Officer, Chris Krusmark, stated that there will be no share repurchases in the current year. Following up on the capital allocation plan, Dave Schwantes expressed their desire to deleverage the company and return to a 4.0 leverage ratio. This comes as the company expects, a slight loss in Q2 2023.

And we're within that covenant range of 5.0. We're not going to get into giving specifics of exactly where it is but it is expected to go up and then come down throughout the rest of the year and end the year under 4.

Valuation

Valuing this company proves to be quite intricate due to its substantial debt, declining profitability, and negative shareholder equity. Precisely estimating its intrinsic valuation may be difficult, but making a case for higher valuations remains feasible.

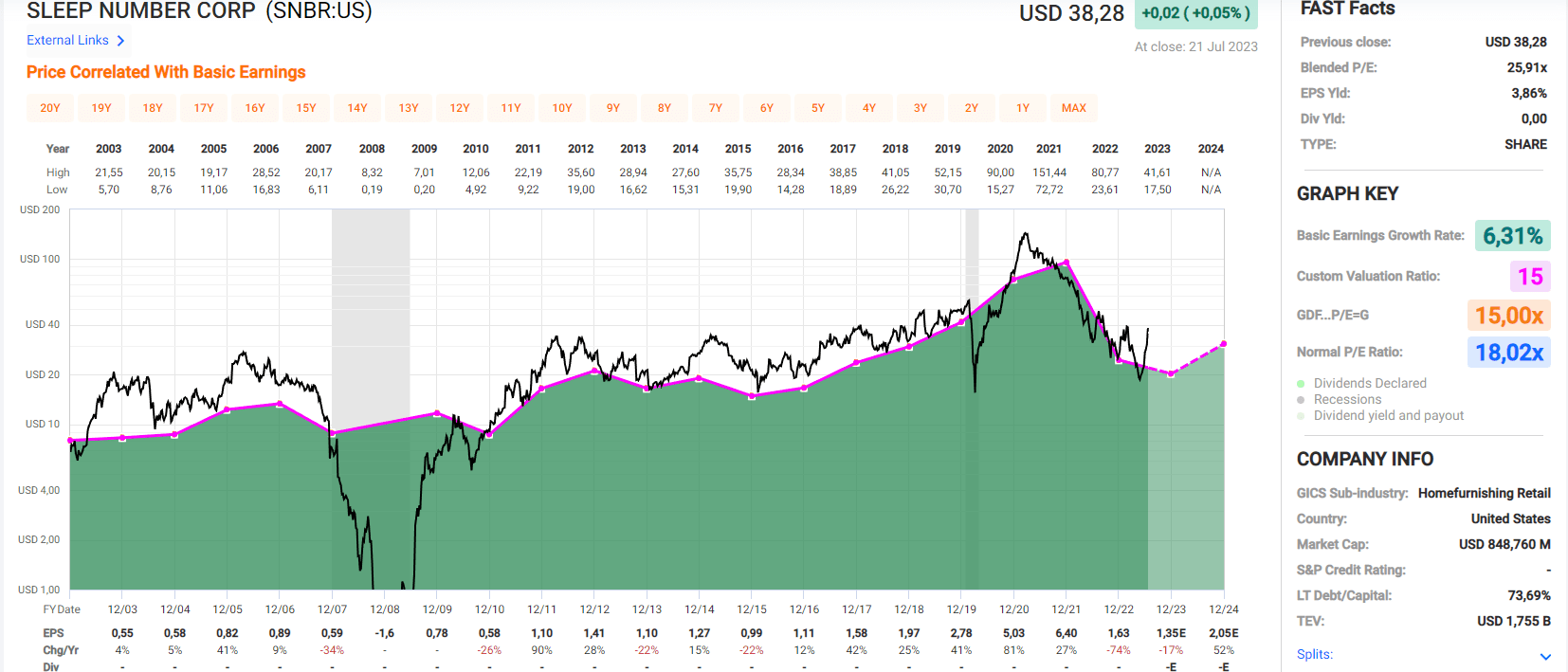

The graph below illustrates the company's earnings (shown by the orange line) with a standard 15 earnings multiple, revealing a clear correlation between earnings and stock price. As earnings declined, the stock price naturally followed suit. The pressing question is when earnings will rebound and by how much.

{kind=link}

Assuming a recovery to pre-Covid19 margins and using current revenues, an estimated price of approximately $63 per share at a 15 P/E ratio appears achievable. This valuation is significantly higher than their 2018 earnings, as revenues have continued to rise while shares were being bought. Even if they fall slightly short of achieving historical margins, purchasing at current valuations still offers a considerable margin of safety.

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company's fundamentals, it can greatly narrow your price target range when investing.

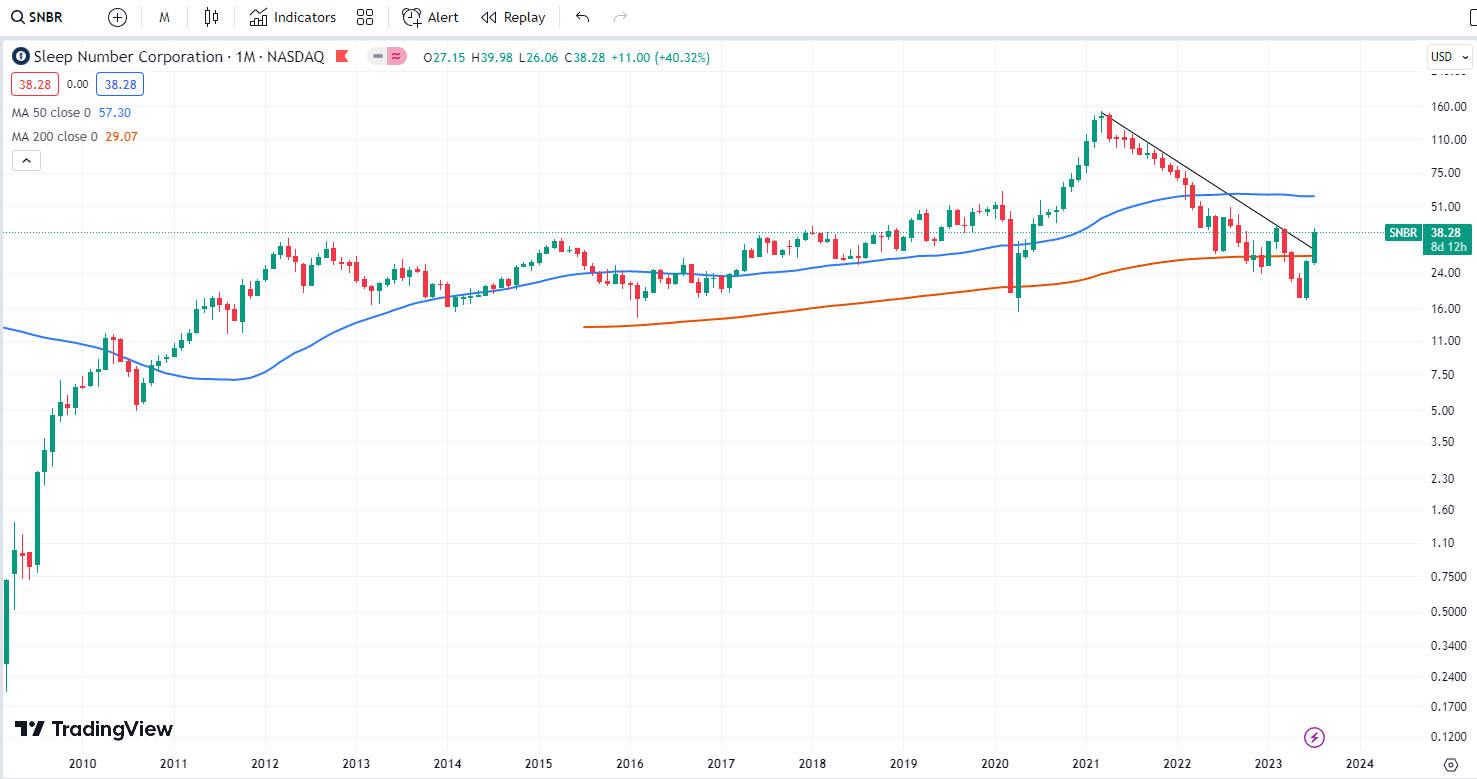

The stock seems to be undervalued when considering its position relative to both its 50- and 200-month moving averages. For a growing company, being below the 50-month moving average often serves as a reliable indicator for intrinsic valuation, especially when it aligns with the fundamentals, as is the case here.

A potential return to the 50-month moving average would place the stock at around $58, which closely matches the estimated value of $63 based on fundamental analysis. Considering the circumstances, it is unlikely that the stock would drop below its 200-month moving average again, as margins are expected to stabilize in the future.

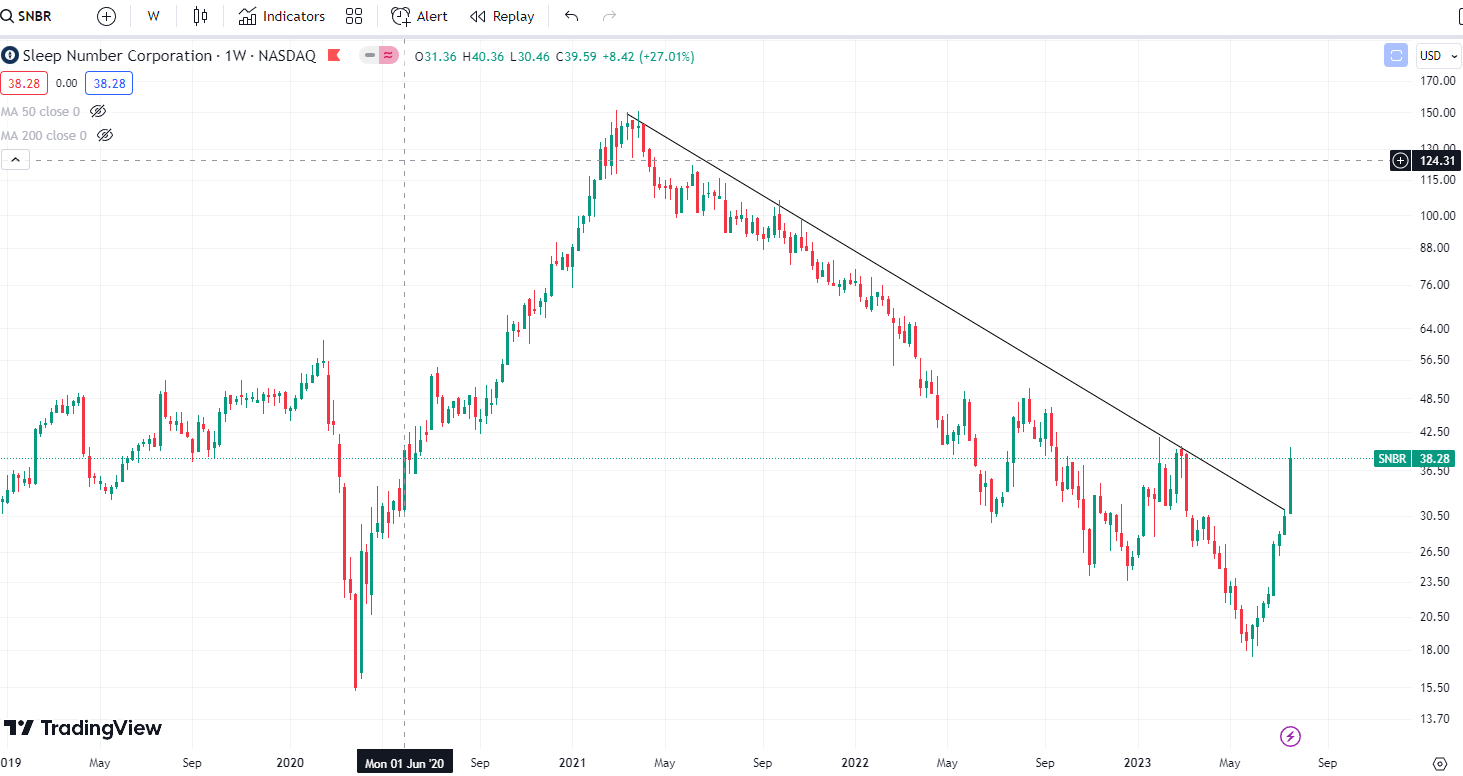

Furthermore, it is worth noting that a bullish breakout has recently taken place, suggesting further positive momentum for the stock.

{kind=link}

Recently, there has been a significant development in the form of a breakout from the falling resistance line. This breakout comes on the heels of an investment upgrade from Wedbush analyst Seth Basham . It is highly probable that this breakout will act as a catalyst for the formation of a bottom.

Furthermore, this breakout aligns with the findings of a fundamental analysis, which suggests that the worst period for the company is likely over. The analysis indicates that there is a normalization of margins on the near horizon.

{kind=link}

Final Thoughts

Even with a remarkable 100% surge in the past two months, I remain optimistic about the untapped potential of Sleep Number. The duration it takes for the stock to reclaim its previous valuations hinges on how quickly the company can stabilize its margins. The encouraging news is that the availability of chips has improved, opening the door to the possibility of higher margins in the future. Management's reaffirmation of this long-term belief during the recent quarterly earnings call is a positive sign, although they did caution about expecting a loss in the upcoming quarter.

Apart from the potential for improving profitability by acting as a catalyst, a significant breakthrough occurred when the stock broke through a downward resistance line that persisted for two years. While a retest of this resistance line remains a possibility, I am convinced that if one believes in the company's ability to enhance margins, now might be the opportune time to consider adding it to their watchlist.

For further details see:

Sleep Number's Rising Potential: A Bottom In Sight Despite Short-Term Losses