SLM - SLM Corporation: Discounted Price Gives Way For A Buy Case

2023-08-16 16:22:37 ET

Summary

- SLM Corporation's beaten-down valuation presents an appealing buying opportunity despite potential hurdles like higher interest rates.

- SLM, also known as Sallie Mae, originates and services private education loans in the US, benefiting from the growing student loan debt.

- The company has been buying back shares and delivering solid financial results, making it an attractive investment with a low P/E and solid yield.

Introduction

A beaten-down valuation as uncertainties persists seems to be what characterizes SLM Corporation ( SLM ) right now. The turmoil caused by the regional bank's failures a few months ago seems to have impacted not only that industry but the entire financial sector as a whole. SLM took a big dive and bottomed out back in late March this year. Since then, however, the share price has rebounded very nicely but still sits at a level where I’d be comfortable investing.

Despite some potential hurdles along the way the discount you get with SLM right now is very appealing and sufficient enough to make it a buy. Some of the hurdles for SLM to get over seem to be higher interest rates which are hurting margins and revenue growth. However, the financial position that SLM exist in is highly durable and is ensuring they have many more years of potential growth ahead.

Company Structure

SLM has been in operation ever since 1972 but is more known as Sallie Mae perhaps. Right now the company is facing difficulties as higher interest rates and provisions seem to be hurting margins in the business. Back earlier this year the company experienced a share price decrease which seemed to be caused by a more pessimistic outlook for interest rates but the turmoil that happened in the regional bank's industry seemed to spill over as well.

{kind=link}

Back in July of 2021, SLM made its highest high at around $19 per share. With the solid financials of the company, I think we are eventually heading back there. This assumption is supported by the fact the company has been buying back shares at a decent rate and the last report showcased their potential of delivering sound NII results too.

In terms of what SLM does and focuses on it could be described as a company that originates and services private education loans to both students and families in the United States. SLM helps their clients be able to finance the cost of their education but also aids with retail deposit funds and money market deposit accounts.

Student Debt (Statista)

Student loan debt has been growing rapidly in the US as more and more seek to get a higher education but also the fact that it is becoming more and more expensive to borrow. The price of going to universities in the US has risen which has caused the debt to grow as rapidly as it has done. For SLM this has meant stronger EPS reports over the years. The EPS has been growing by 14.6% in the last 10 years annually. That is quite impressive and investors in the company have seen solid returns as SLM also pays out a decent dividend at a yield of 2.8%.

{kind=link}

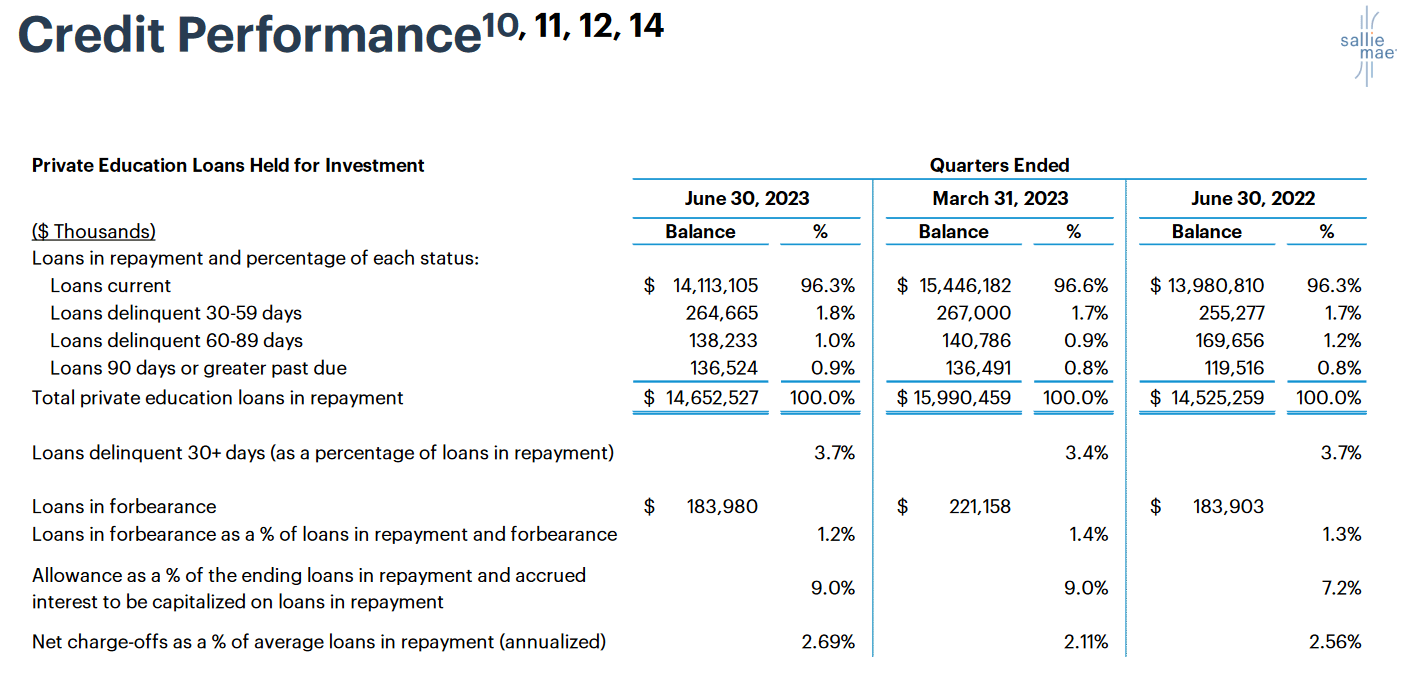

Looking closer at the credit performance of SLM we can see that the loans delinquent are rising on a QoQ basis by a fair bit, reaching 3.7% as opposed to 3.4% back in the first quarter of 2023. This doesn't bode that well for SLM as it means less NII is coming in. Where I do become concerned is that the overall debt in the US has a delinquency rate of 2.23% , well below what SLM is experiencing. What should be said though is that students often have far lower incomes than most people and a higher delinquency rate should be expected. Going into the next few quarters watching the impact this has on earnings will be important. It doesn’t seem though that there is such a large amount of delinquent debt past 90 days, only 0.9%. The company still sits very solid at an ROE of 22.3% which is ensuring they can maintain the dividend and buy back shares.

Earnings Transcript

From the last earnings call by the company, we got some good insights as to how the operations are for the business. The CEO Jonathan Witter said the following:

-

“We were able to put the proceeds from this successful loan sale and the corresponding capital release to work in the second quarter, repurchasing just over 16 million shares of our common stock. We have reduced the shares outstanding since January 1st of 2023 by 7% and by 48% since January of 2020”.

As highlighted previously, SLM is doing a great job in terms of buying back shares, and they are doing it when the price is not that expensive in my opinion. Looking at the progress since January 2020, SLM has reduced the outstanding shares by 48%. Doing that in just a little over 3 years is outstanding and a true testament to what investors might be able to get from an investment here.

-

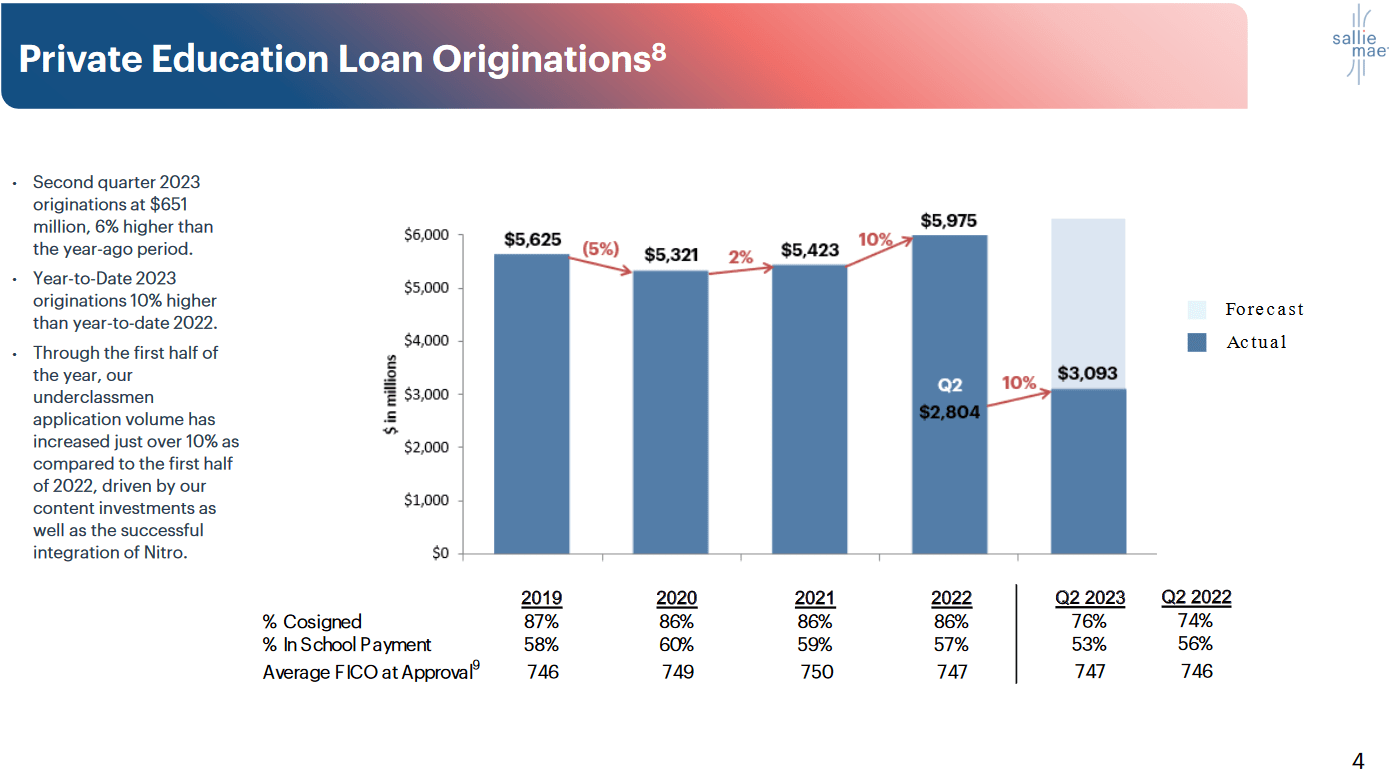

“Private education loan originations for the second quarter of 2023 were $651 million, which is up 6% over the second quarter of 2022. Our originations for the first half of the year are slightly ahead of our forecast for 2023. We are also seeing strong underclass application growth. Through the first half of the year, our underclass application volume has increased approximately 11% as compared to the first half of 2022, driven by our investments in technology and content”.

In terms of loan growth for the company seeing the private education loan originations increasing like this is great. Some variance seems reasonable between the quarters, but as long as YoY growth is achieved, I am very pleased.

Valuation & Comparison

GGM Model (Author)

Viewing the GGM model above here, I think it becomes clear the SLM has a sound risk/reward profile right now. The company is trading a fair bit below my target prices as I seek a 10% annual return and a dividend growth of 8% in the long run. That seems reasonable as the company has a history of doing large increases and then staying there for some years. I think that with the low p/e and solid yield, SLM is a buy for me.

Risk Associated

Among the potential risks that come to the forefront in a climate of elevated interest rates is the looming specter of defaults. As interest rates climb, borrowers might find themselves facing a more challenging environment to meet their debt obligations. This, in turn, raises the potential for an uptick in defaults, as borrowers struggle to navigate the financial strains associated with increased borrowing costs.

{kind=link}

As we have already seen a rise in delinquencies on student debt, it seems possible that it may stay at this elevated level for some time until we see a decline in the interest rates. That doesn't seem to until sometime in 2024 though.

Investor Takeaway

The student loan market is difficult to navigate, however, I think that SLM has done a great job so far and the ROE sits at 22.3% TTM. This is ensuring that they can continue paying the dividend and reward investors in the company. Watching the development of the debt delinquencies in the coming quarters will be important, but long-term SLM remains appealing and a buy rating will be given to it.

For further details see:

SLM Corporation: Discounted Price Gives Way For A Buy Case