SGH - SMART Global Earnings: Too Mixed For Me (Rating Downgrade)

2023-04-05 03:32:53 ET

Summary

- SMART Global's crown jewel, its IPS segment, easily outperformed my expectations.

- However, the remainder of the business is a problem.

- Given that investors can't cherry-pick the segments they want, I don't believe that paying up 7x EPS for the whole business makes sense.

Investment Thesis

SMART Global ( SGH ) was in the process of diversifying its focus away from its legacy memory business towards the more interesting and rapidly growing Intelligent Platform Solutions ("IPS") unit.

And while this coveted segment delivered a solid set of results , significantly accelerating its growth trajectory from the previous quarter, fiscal Q1 2023, the rest of the business continues to be a laggard.

Unless the whole business starts to grow, investors will increasingly question its bottom-line profitability and whether there's enough value to be added to the stock.

To summarise, I'm moving my buy rating to the sidelines.

Story Stocks Sours?

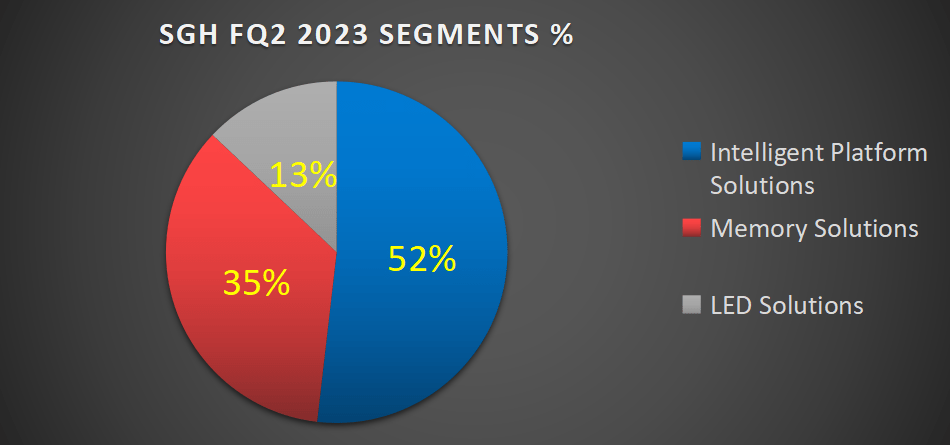

SGH's Intelligent Platform Solutions segment was meant to be the crown jewel that would allow SGH to grow its AI and machine learning opportunity. SGH's IPS business unit delivers tailored high-performance computing manufacturing.

{kind=link}

Let me cut to the chase, in my prior bullish article I made the case that SGH's IPS segment could grow at "30% CAGR over fiscal 2023". After all, the acquisition of Stratus Technologies, which was added to the IPS segment in August 2022, allowed it to post a massive amount of revenue growth at 78% y/y in fiscal Q1 2023.

This time around IPS was up a massive 170% y/y including Stratus. Admittedly, the IPS segment was always expected to be lumpy, but I'm not sure that this level of bumpiness was expected. Excluding the Stratus acquisition, this segment was up 107% y/y, clearly beating my previous estimate of 30% CAGR for fiscal 2023.

But what about the business as a whole?

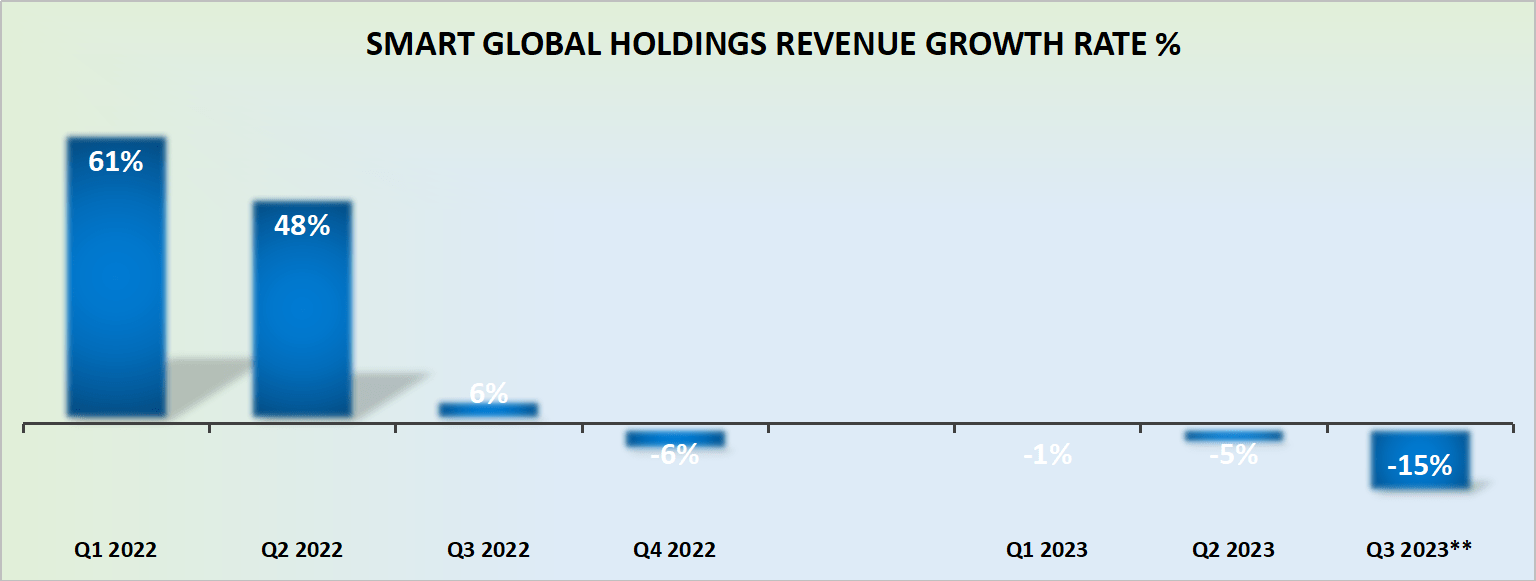

Revenue Growth Rates Fizzling Out

{kind=link}

The problem here is that investors are having to buy the whole business. Yes, the IPS segment, but the Memory Solution business too, which was down 42% y/y in the fiscal Q2 2023.

The high end of SGH's guidance points to fiscal Q3 2023 coming in at negative 15% y/y. This is significantly worse than what analysts were expecting. Consequently, this brings into question the likelihood that SGH will indeed positively impress against these expectations.

SA Premium

Analyzing SGH's Profitability Prospects

Looking ahead to fiscal Q3 2022, SGH's bottom line is expected to come in around $0.40, plus or minus $0.10. This compares with $0.44 in the prior year's quarter.

Put more simply, the midpoint of its guidance would leave SGH's bottom line moderating relative to the prior year.

So, we have a business that's clearly not growing and profitability that doesn't appear to be moving in the right direction. What would give an investor the tenacity to buy the stock? Perhaps its valuation? Let's address this next.

SGH Stock Valuation - 7x EPS

On a non-GAAP basis, where we pretend management works for free basis, the stock is on a path to report about $2.45 of EPS. This leaves the stock at under 7x this year's EPS. Surely, that's a cheap valuation?

The problem with investing is that cheap can often become a lot cheaper. What investors want to back are companies that next year are fairly sure to be more profitable than this year.

And I'm not convinced that's going to be the case here. There's only so far a company can cut back on its Memory Solutions business to extract cash flows. It will get to a point where all the surplus costs will have been taken out of the business. Including costs that are needed to invest in the future growth of the business.

The Bottom Line

I had huge hopes for SGH's IPS segment. And that clearly did deliver way above my expectations. What I didn't count on was SGH's Memory Solution business shrinking so dramatically over such a short period of time.

While I recognize that SGH has ample cash on its balance sheet, it also has a fair amount of debt too. More specifically, SGH's balance sheet carries around $435 million of net debt. This is not a thesis breaker, particularly given that SGH clearly makes solid free cash flows. But given that the business isn't really delivering much topline growth, at some point, that will start to produce suboptimal cash flows, and then, all of a sudden, that leveraged balance sheet starts to become a problem.

For further details see:

SMART Global Earnings: Too Mixed For Me (Rating Downgrade)