SDC - SmileDirectClub Vs. Align Technology - Too Much Risk Versus Not Enough

2023-08-18 15:00:12 ET

Summary

- Smile Direct Club's market cap has fallen from $8.9bn post-IPO, to $221m today, down ~98%.

- The company has been struggling to regain compliance with Nasdaq listing rules, its shares trading at $0.60 at the time of writing.

- Smile Direct's business model, offering cheaper teeth alignment solutions with fewer in-office visits, has not been as successful as Align Technology's more comprehensive approach.

- Align has gone from strength to strength within a market with massive potential, and its shares have delivered fantastic long term gains for shareholders.

- Buying Smile Direct stock would be a rewarding but risky bet on an unlikely turnaround. Buying Align today is to buy at premium price. I'd maintain a watching brief for now.

Investment Overview

SmileDirectClub ( SDC ) completed its Initial Public Offering ("IPO") in September 2019 - five years after the company was founded - raising ~$1.3bn via the issuance of ~58.5m shares priced at ~$23 per share - a higher figure, apparently, than originally planned.

Immediately post-IPO, SmileDirect's business enjoyed a market cap of ~$8.9bn. Fast forward four years, however, and today, the company's market cap has fallen in value to $221m, with shares trading at a value of $0.55 at the time of writing - down 98% since IPO.

By any listed company's standards, this represents exceptionally poor performance. SmileDirect's ambition appears to have been to challenge the market incumbent in the vast and under-penetrated teeth alignment industry - Align Technologies ( ALGN ), but clearly the company has not been successful.

SmileDirect's Delisting Woes

In November 2022, the Nasdaq wrote to SmileDirect informing the company it was no longer in compliance with its listing rules, its share price having traded under $1 for 30 consecutive days. The company was provided an initial compliance period of 180 calendar days, or until May 17, 2023, to regain compliance with the Minimum Bid Requirement.

That did not happen, but Smile instead submitted a turnaround plan to the exchange, which was accepted, meaning the company's shares are - at least for the next few months - no longer in danger of being delisted.

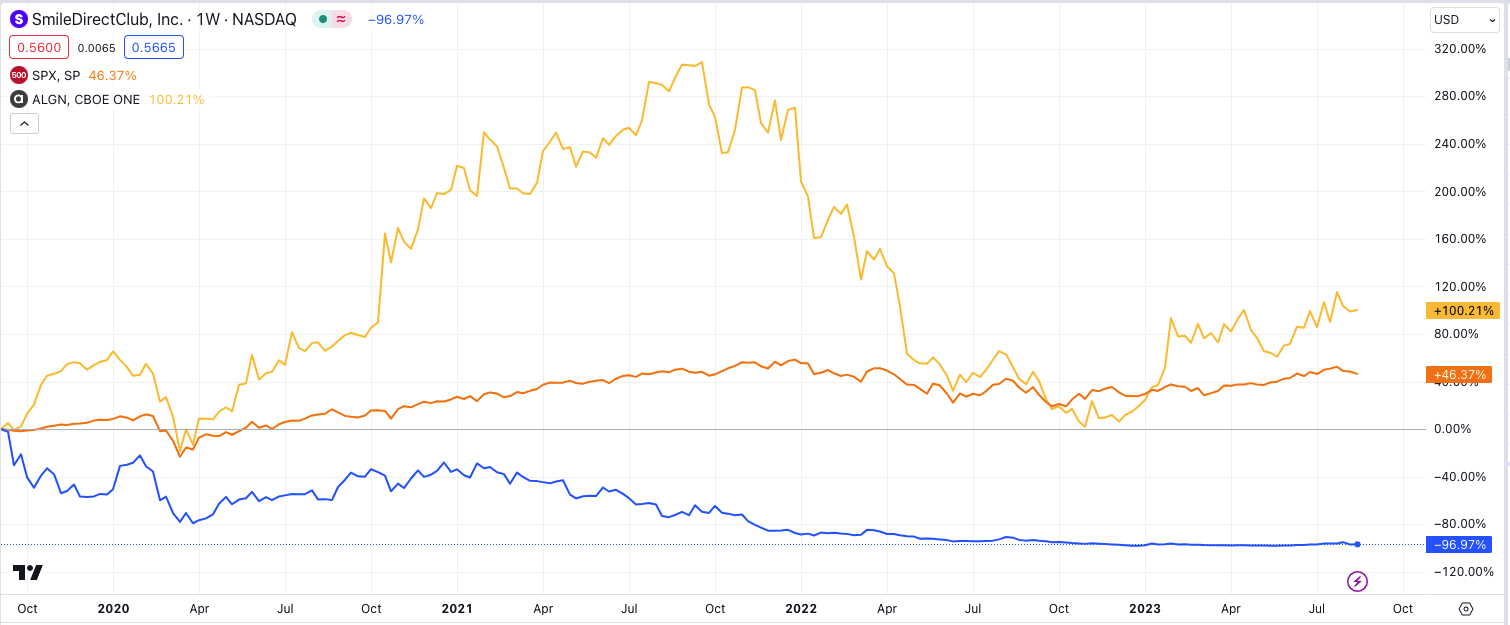

SmileDirect / Align share price performance vs S&P 500 (TradingView)

{kind=link}

As we can see above, while Align Technology's stock has experienced a fair amount of volatility over the past five years - its share price touching highs of $725 in September 2021, perhaps on the back of growing demand from patients during the lockdown period - it is +97% across the past five years, versus the S&P 500's 45% gain over the same period, and SmileDirect's 97% decline.

Clearly given the two companies have a similar business model, one company's execution has been very strong whilst the other's has been poor. Given the "stay of execution" granted to SmileDirect to keep trading on the Nasdaq, and its plans to turn around the business, however, plus its very low valuation, is there an argument that even small signs of progress could lift the share price back above $1, which would represent an almost 100% return on investment for any investor brave enough to buy today?

In short, it is easier for SmileDirect's share price to spike upward, given the low bar it is starting from, than it is for Align's to do similar given its historically good growth, which has seen Align's market cap valuation grow to over $26.5bn. Does that make SmileDirect an interesting contrarian trade, or would investors be better off backing a business that is already thriving, offering less risk, but also less reward?

SmileDirect and Align Technology - Business Models Compared

In its 2022 10K submission (annual report) SmileDirect breaks down its business model as follows:

Our vertically integrated model enables us to solve critical problems around cost, convenience, and access to care. We offer professional-level service and high-quality clear aligners generally at a cost of $2,050, up to 60% less than traditional orthodontic solutions. We achieve these cost savings while maintaining high quality by removing the overhead cost of multiple in-person doctor visits and managing the entire customer experience, all the way from marketing to aligner manufacturing, fulfillment, treatment by a customer's dentist or orthodontist, and facilitating remote clinical monitoring through completion of treatment, which is facilitated by our proprietary teledentistry platform.

To further democratize access to care, we offer customers the option of paying the entire cost of their treatment upfront or enrolling in our financing program, SmilePay, a convenient monthly payment plan. We also accept insurance and as of December 31, 2022, are in-network with UnitedHealthcare, Aetna, Anthem, Dominion National, Empire Blue Cross and MetLife, among others.

Now, let's compare and contrast this with Align's model, as discussed in its 2022 10-K submission :

Our clear aligners are sold under the Invisalign brand name. Our Invisalign System is intended mainly for the treatment of malocclusions and is designed to help dental professionals achieve the clinical outcomes that they expect and the results patients desire.

To date, over 14 million people worldwide have been treated with our Invisalign System. In order to provide Invisalign treatment to their patients, orthodontists and GPs must initially complete an Invisalign training course. Our iTero intraoral scanner is used by dental professionals and/or labs and service providers for restorative and orthodontic digital procedures as well as Invisalign case submissions.

Our exocad CAD/CAM software products provide restorative dentistry, implantology, guided surgery, and smile design to dental labs and dental practices through fully integrated workflows, paving the way for new, cross-disciplinary dentistry in labs and at chairside.

Align completed its initial public offering all the way back in January 2001, raising $130m by issuing 10m shares priced at $13. Its business model is summarised in the 10K submission as "Connect" - with a physician, "Scan" - to enable doctor diagnosis, "Plan" - the ortho and restorative treatment, "Treat" - take delivery of and use aligners, and finally 'Monitor", with follow-up visits and ongoing patient care.

SmileDirect's offering is essentially a slimmed down version of Invisalign, with a cheaper price point but fewer in-office visits with a physician. Although SmileDirect customers may visit one of SmileDirect's 900+ partner network locations to "begin their journey", they can also complete an initial assessment remotely if they prefer, either with an impression kit, or using a mobile app.

A course of treatment with SmileDirect typically takes 4-6 months, according to Dentaly.org , while a course with Invisalign takes much longer - 12-24 months. Dentaly also suggests that while SmileDirect has a fixed cost of $1,639, or ~$69 per month, Invisalign typically costs $2k - $4k.

That may be more expensive than SmileDirect, but equally, SmileDirect may not be 60% cheaper than Invisalign as management claims, and more importantly, it seems that patients undergoing teeth alignment procedures do not regard price as important a factor as say, quality, or access to a physician.

In a market where people would prefer to pay more for a better service, we can see where SmileDirect seems to have made a fundamental mistake - undercutting rivals on price with a "bare bones" approach was not the right approach to adopt.

Markets and Financials - SmileDirect versus Align Technology

Neither SmileDirect nor Align have too many concerns around the market opportunity for their products. Align, for example, states in its 2022 10-K that:

Malocclusion is one of the most prevalent clinical dental conditions in the world, affecting approximately 60% to 75% of the global population. We estimate that there are approximately 500 million people globally with malocclusion who could benefit from straightening their teeth

SmileDirect also views the market opportunity as 500m patients, and states in its 2022 10K:

Given that we have captured less than 1% of the total market opportunity, we plan to grow our customer base by continuing to focus our marketing efforts on the approximately 85% of people globally who have malocclusion.

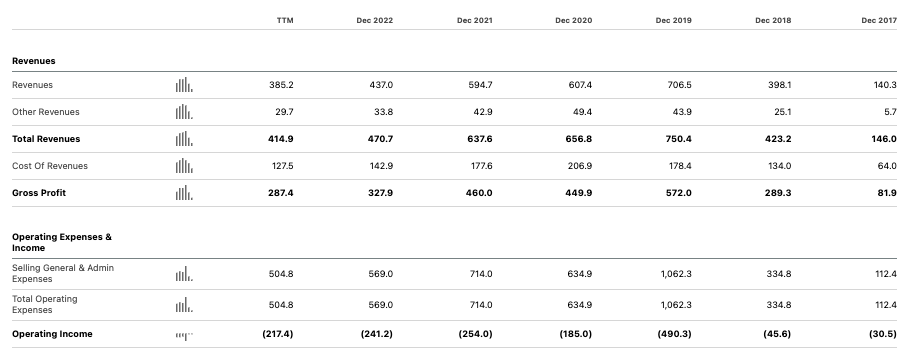

Now, let's take a closer look at historical performance starting with SmileDirect.

{kind=link}

As we can see above, after an exceptionally strong 2019 SmileDirect's revenues have been falling year-on-year, from $707m in 2019, to $437m last year. Meanwhile, operating loss has been substantial - amounting to well over $(1bn) since 2018.

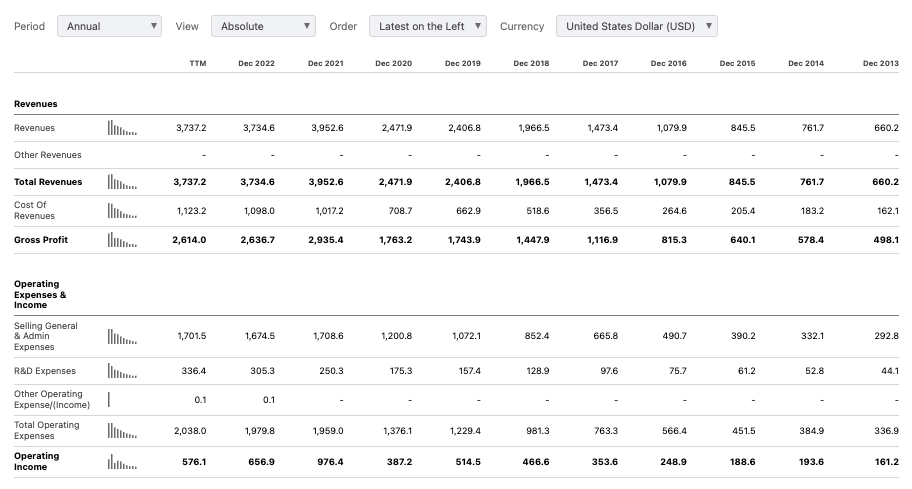

{kind=link}

Conversely, as we can see above, Align has moved from strength to strength, its revenues increasing very nearly fivefold between 2014 and 2022, from $762m, to $3.7bn. Operating income has been positive in every year also, being in excess of $2bn across the past three years - $657m, $976m, and $387m in 2022, 2021, and 2022 respectively.

Align - Recent Performance

In Q2 2023, Align reported revenue growth of 6.3% sequentially, and 3.4% year-over-year, to just over $1bn, while operating income was $171.9m - a margin of 17.2%. The company made 604k clear aligner shipments during the quarter, and reported diluted earnings per share ("EPS") of $2.22. Align additionally reported a near-term cash position of >$1bn, and stated that it has $1bn available for share repurchases.

The company is forecasting for FY23 revenues of $3.97bn-$3.99bn, with a GAAP operating margin just over 17%, and non-GAAP just over 21%. Using the non-GAAP margin, that amounts to operating profit of over $800m, and with planned capital expenditures of ~$200m, plus tax and exceptional items, I would estimate that Align could generate ~$500m net income, for EPS of ~$6.50, and a price to earnings ratio of ~53x.

That figure is a little on the high side, suggesting that although Align is a strong company, it is not valued at any particular discount to its real value. Balanced against that is the fact shares traded over $725 just a couple of years ago - it is tempting to wonder how far a couple of earnings beats in the second half of this year could drive the share price upward.

SmileDirect - Recent Performance

Meanwhile, SmileDirect drove just $107m of revenue - nearly 10x less than Align, and a ~15% sequential, and 19% annual decrease - in Q2 2023, reporting a net loss of $(54m). The company shipped 46,774 aligners during the quarter, a 22% sequential decrease, and provided guidance for FY23 for $425m-$475m of revenues, adjusted EBITDA of $(40m)-$(10m), and gross margin of 73-76%.

As of June 2023 SmileDirect's current assets stood at $212m, down from $297m in the prior year period, whilst current liabilities were $112m, and long-term debt stood at $863m.

It is hard to take many positives from SmileDirect's Q2 2023 performance, other than the fact that annual losses appear to be narrowing. Even so, with the business not growing, can SmileDirect generate enough cash flow to pay off its debts? The company's forward P/S ratio is an impressive 0.5x, and even the narrowest profit would likely translate to a very competitive PE score that would attract investors who believe the business can be turned around.

Looking Ahead, SmileDirect is hoping that two new developments will make the difference in the second half of 2023 and beyond. As CEO David Katzman commented in the Q2 2023 earnings press release:

"I'm also happy to share that in late May, we launched our innovative AI-powered SmileMaker Platform mobile scanning app for 3D treatment planning in the U.S. Additionally, CarePlus, our premium hybrid in-person and remote aligner product, will be available in all of our U.S. SmileShop locations and select Partner Network offices by the end of August.

Customers at our SmileShops will have the option to select SmileDirectClub's original telehealth-powered Care aligners or choose the premium CarePlus option, which includes access to a local dentist or orthodontist for in-person check-ins, a dedicated 24/7 Concierge customer care team, expedited aligner shipping and the enhanced comfort of scalloped-edge aligners and retainers."

For me, the more interesting development than the 3D scanning app could be the premium Care-Plus option, which gives patients access to a local dentist - after all, it is this more expensive but holistic form of care that has been so successful for Align, while SmileDirect has struggled to attract buyers for its "bare bones", cheaper version.

Concluding Thoughts - Align's Solid Performance And Growth, Or An Outside Bet On SmileDirect Completing Unlikely Turnaround

Align and SmileDirect are the two best-known brands in the teeth straightening market, both inside and outside the US, but their fortunes since listing have been completely contrasting.

A 20-year Nasdaq listing for Align has rewarded shareholders probably beyond their wildest expectations, and even if growth is slowing slightly, and ultimately the $700+ per share highs reached in 2021 were not sustainable, Align's share price is +23% this year.

As discussed above, if the company could show a little extra profitability, or find ways to increase its market penetration by only a few percentage points, its share price could start to experience some rapid upward momentum, although few would argue that Align's shares trade at a significant premium to current performance.

Conversely, it's hard to think of how SmileDirect's period as a listed entity could have gone worse. With debts close to $1bn, a shrinking business, and no profits, it is not hard to see why shares trade well below $1.

Nevertheless, the Nasdaq has seen SmileDirect's plans and concluded they were sufficient for the exchange to agree to continue listing the company's shares, so it is intriguing to speculate about what might happen next. The management team includes three members of the Katzman family, and as such it seems unlikely there will be change at the top, and that every effort will be made to find a way to continue selling its teeth alignment kits.

In my view, however, the deal that would suit all parties the best may be for SmileDirect to sell the business, or for the business to merge with another company looking to gain a Nasdaq listing. It seems surprising both that Align has an apparent monopoly in the teeth alignment market, and that a challenger with the funds and opportunity that SmileDirect seemed to have when listing in 2019, could not make a success out of it, but it may hint at underlying difficulties in the market, as the vast majority of people who could apparently benefit from teeth alignment opt against it, or are unaware of Align or SmileDirect, despite their advertising spends.

To summarise my position - in relation to SmileDirect, the likely next move for the company is to compete a reverse stock split i.e. reduce its share count so that each share trades at a higher price. Such a move would take delisting out of the equation for the time being, but it would be bad news for SmileDirect shareholders, and as such I believe the risk of buying SmileDirect stock today and hoping for the company to find new funding and engineer a turnaround may be slightly too high to warrant a "Buy" call.

Meanwhile, Align continues to grow - albeit perhaps not quite at the rate the market is demanding/expecting, based on the premium share price. With no dividend, Align is a slightly risky stock to hold, that could correct downward if sales fall in a post-pandemic/Business As Usual ("BAU") environment.

I would be interested in the company's stock if the price were to fall below $250, which would value the company at under $20bn, but this may only happen on underwhelming sales performance, which would be linked to slowing growth, the one problem I see at the company. I would want to avoid that type of viscous circle scenario.

For further details see:

SmileDirectClub Vs. Align Technology - Too Much Risk Versus Not Enough