SNAP - Snap: Giving Up Gains Is Likely In 2024

2023-12-28 20:47:00 ET

Summary

- Snap's stock has seen a significant rally this year, outperforming the S&P 500.

- Enthusiasm over the company's My AI product has driven some bullishness, but this is likely to be a novelty pop that fades with time.

- The company is seeing sharply decelerating user and revenue growth, particularly in the U.S. where its revenue is most concentrated.

- Snap isn't cheap at ~5.4x FY24 revenue, especially considering declining gross margins.

Amid sharply renewed enthusiasm for growth and tech stocks, Snap ( SNAP ), the disappearing-chat social media company, has been the beneficiary of a sharp year-to-date rally. Investors have latched onto the company's user growth in developing markets, in spite of advertising industry headwinds that have dented revenue to just single-digit growth.

Year to date, share of Snap have jumped nearly 2x, vastly outperforming the S&P 500:

The meteoric rise has been especially concentrated in the past two months, with Snap bouncing from a low below $9. Amid this sharp outperformance, however, we have to ask the question: does Snap's fundamentals protect this outperformance continuing into 2024?

I last wrote a bearish article on Snap in August. While I certainly didn't anticipate the quick fall in interest rate expectations to benefit Snap so loftily, I'm not keen to reverse my position heading into 2024. Since then, Snap has continued to release what I consider to be quite disappointing results.

Risks, in my view, continue to compound for Snap. Among the largest risk for Snap - which the company didn't quite solve in Q3, nor is likely to in the near future - is over concentration in U.S. revenue. That's a problem because the regions in which user growth is occurring is, relative to the U.S., quite under-monetized. And in the U.S, ad rates continue to be pressured - though we'll see if stronger consumer and business confidence, on the back of lower interest rates, will help to reverse this trend in 2024.

Weakening profit margins continue to be another key red flag for the stock - especially in a time where its main social media rival, Meta ( META ), can actually be reasonably valued on a P/E basis. Snap has invested heavily into its infrastructure this year, ostensibly with the goal of improving ad optimization and driving revenue growth - but so far, we've only seen the dampening impact on gross margins, while revenue growth continues to be meager under the burden of a tough macro.

I acknowledge that there is one - and only one - upside risk case for Snap, and that revolves around its AI products. The company has built a generative AI chatbot called "My AI" that has gotten plenty of traction among its existing user base. Increased engagement here can bring on new monetization opportunities and increase ARPU. Per founder and CEO Evan Spiegel's remarks on the Q3 earnings call on early engagement for this new feature:

We continue to leverage AI technology to deliver new products and features to our community. Since launching My AI, more than 200 million people have sent more than 20 billion messages, which we believe makes My AI one of the most used AI chatbots available today. More than 250 million Snapchatters engage with AR experiences on our platform every day on average."

Still, I'm more inclined to believe that the early pop for My AI has more to do with the novelty of the offering, rather than an inclination of its staying power. We also can't ignore the fact that all of Snap's rivals are building their own AI-related features , and I don't believe AI can ensure Snap's long-term relevance in a crowded social media arena.

All in all, I remain bearish on Snap, especially given the stock's valuation has reached moderately rich levels again. At current share prices near $17, Snap trades at a market cap of $28.24 billion. After we net off the $3.61 billion of cash and $3.74 billion of convertible debt on Snap's most recent balance sheet, the company's resulting enterprise value is $28.11 billion.

Meanwhile, for next fiscal year FY24, Wall Street analysts are expecting Snap to generate $5.22 billion in revenue, representing 13% y/y growth - putting the stock's valuation at 5.4x EV/FY24 revenue.

To me, considering the fall to low-teens growth and declining gross margin profile, I find little appeal to investing in Snap at current levels. Steer clear here.

Q3 download

Let's now go through Snap's latest quarterly results in greater detail. The company's latest user trends, which arguably are the metric that drives the business the most, is shown in the snapshot below:

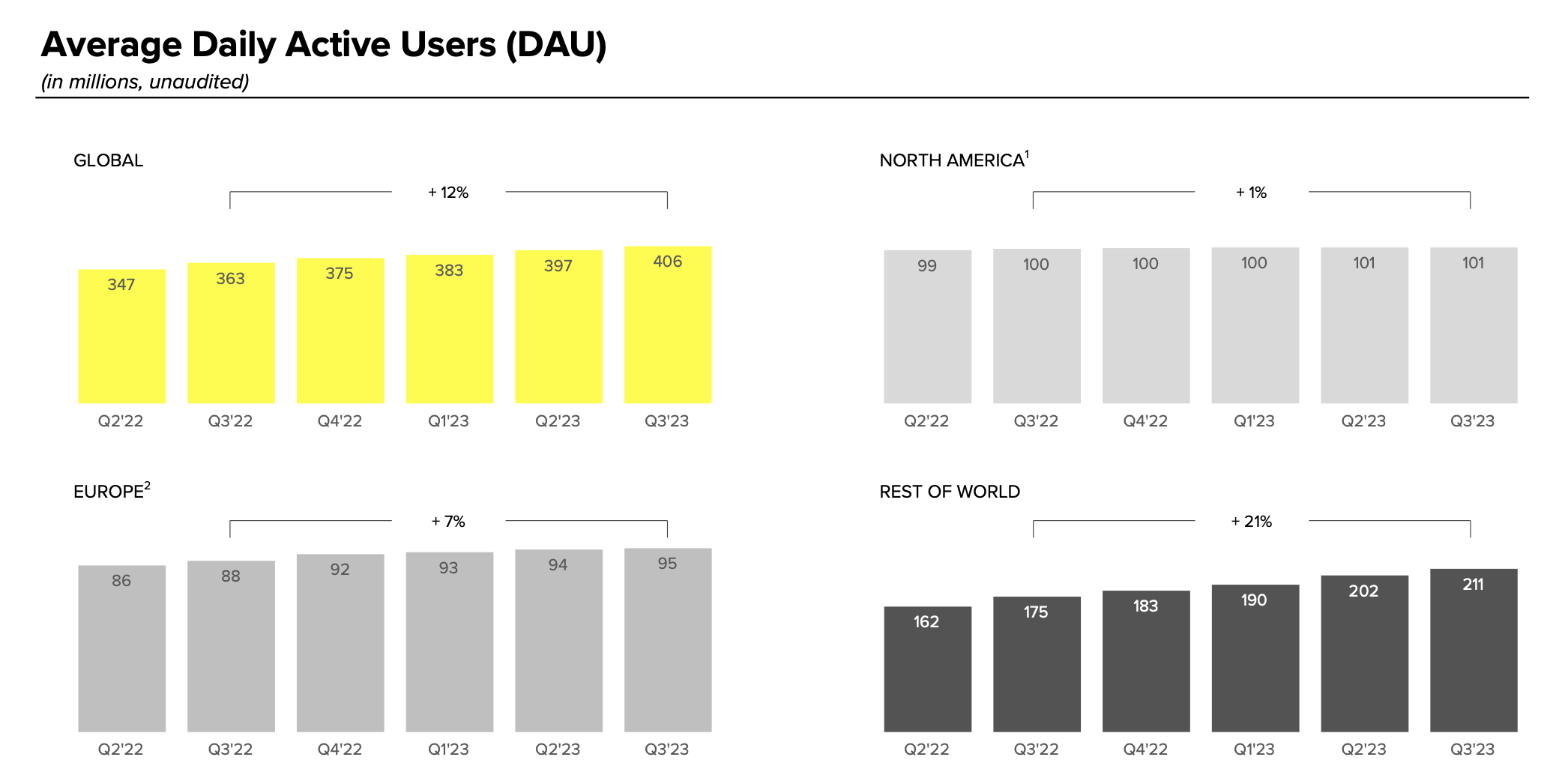

Snap DAU trends (Snap Q3 earnings deck)

{kind=link}

DAUs grew 12% y/y and added 9 million net-new users from Q2. Two observations here: first, net-new user growth slowed down dramatically from Q2, where the company had added 14 million net-new users; second, Snap is continuing to forecast slower DAU growth going forward, with Q4 anticipated to end at 410-412 million DAUs. The top end of that range implies only 6 million net-new adds.

This forecast, more than anything, implies saturation for Snap as the product gets long in the tooth and faces competition from Instagram, TikTok, and other social media applications. And saturation is almost certainly the case in North America, where user growth was flat sequentially at 101 million DAUs and up just 1% y/y.

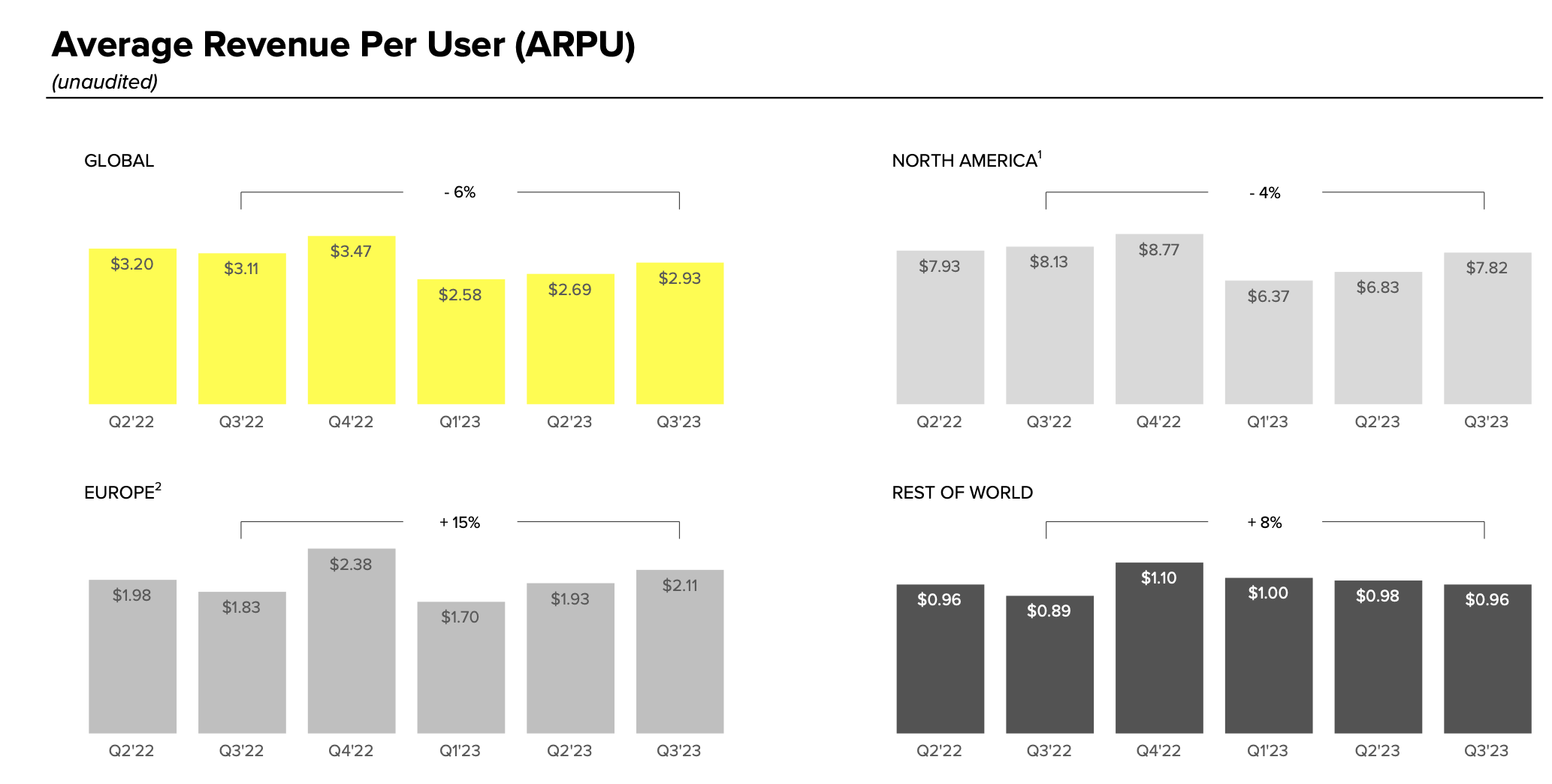

Meanwhile, revenue remains concentrated in North America, which generated $789 million in revenue for the quarter (-3% y/y) and constituted 66% of Snap's overall $1.19 billion in revenue, up 5% y/y. Revenue is lagging behind DAU growth as ARPUs continue to drag from a y/y basis, as shown in the chart below:

Snap ARPU trends (Snap Q3 earnings deck)

{kind=link}

Poorer advertising demand in North America, where ARPU is down -4% y/y, as well as an unfavorable mix shift in users to the "Rest of World" segment where ARPUs are roughly one-eighth of a North American user, have brought global ARPU down -6% y/y. Again, this is in spite of deep investments that the company has made in infrastructure spending to improve its ad targeting platform.

Perhaps even more concerning: Snap is expecting top-line deceleration to follow DAU deceleration as well in Q4. Its guidance range calls for 2-6% y/y revenue growth in Q4, with the company citing limited ad market visibility as the core driver. Asked about this deceleration on the Q&A portion of the Q3 earnings call, CFO Derek Andersen noted as follows:

I think on the brand side in particular, coming off of the progress that we saw in Q3 with those new brand products seeing really good uptake, you're right, as we move into Q4, Q4 is a little bit different as a quarter. Historically, we've seen a little bit larger share of the revenue coming from brand products in Q4. And then two, the Q4 business being a little bit more back-end weighted than other quarters historically as well. So, both of those things sort of impacting visibility. And brand having grown at a slower rate in Q3 and being a larger share of the business in Q4 sort of brings a little bit of a mix shift headwind.

And then last, the point that you raised very specifically, which is what we've seen since the onset of the war in the Middle East is we have had a number of primarily brand-oriented campaigns pause spending in the early period after the onset of the war there in the Middle East. I will say that we have seen a lot of those campaigns resume spending. And the impact to our daily run rate has reduced significantly as a result of that. But we also have seen a very small amount of incremental campaign pauses triple in more recently.

And so, one of the things that we've tried to do here when we're thinking about giving forward-looking information for Q4 is number one, be transparent about what we've seen quarter-to-date on that side. And then, I think when we look back historically, for example, to what we all experienced at the onset of the war in Ukraine and the impact that that had on folks' business and the operating environment, I think we've realized that war is fundamentally unpredictable. And as a result, it would be imprudent to provide a formal guide in that kind of an environment."

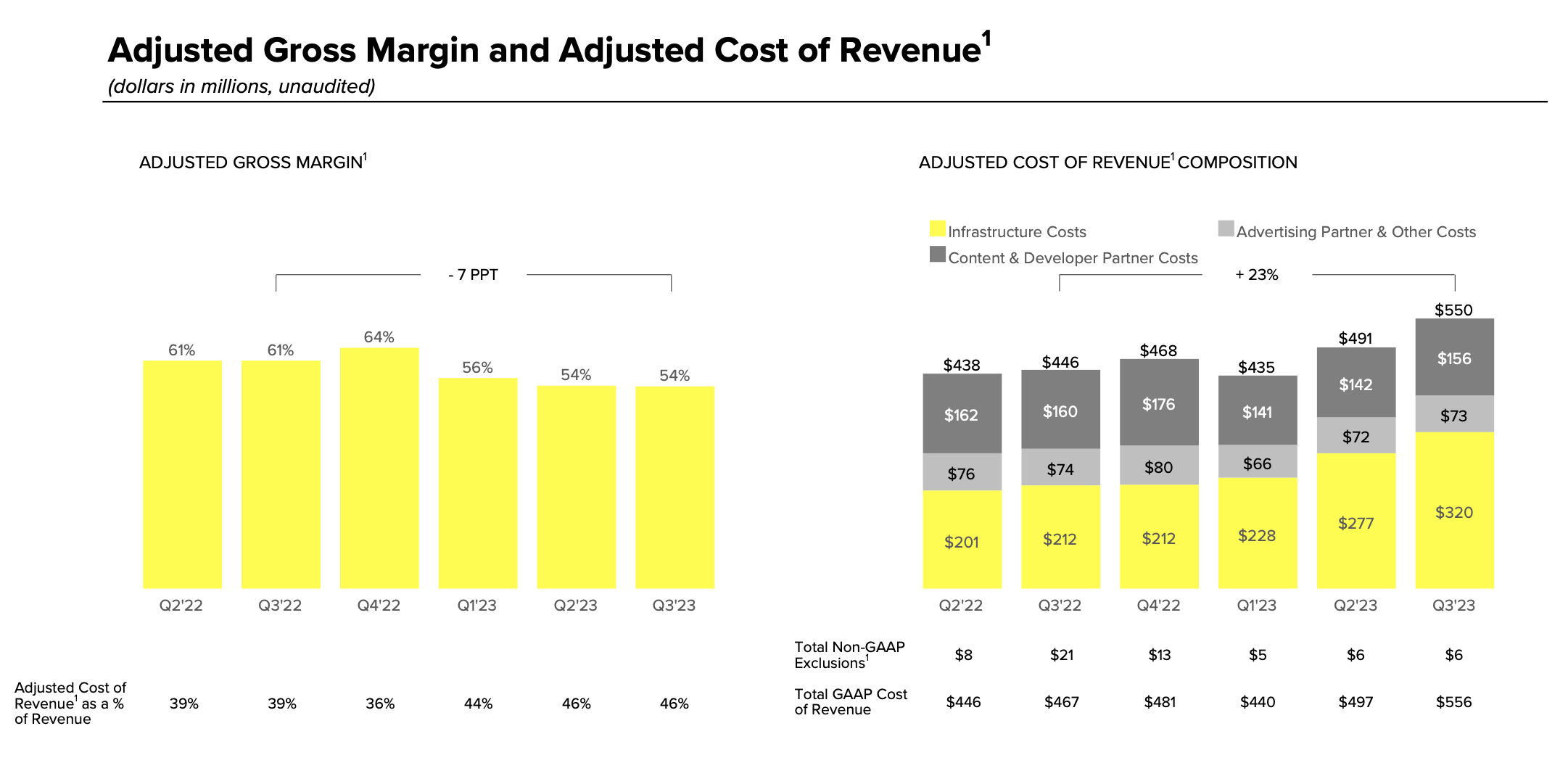

Adding insult to injury, as a result of the incremental spend that has not yet materialized into revenue acceleration either in Q3 or Q4, Snap's gross margins fell seven points y/y to 54%, largely driven by infrastructure spend (represented by the yellow bars on the right-hand side of the slide below):

Snap gross margins (Snap Q3 earnings deck)

{kind=link}

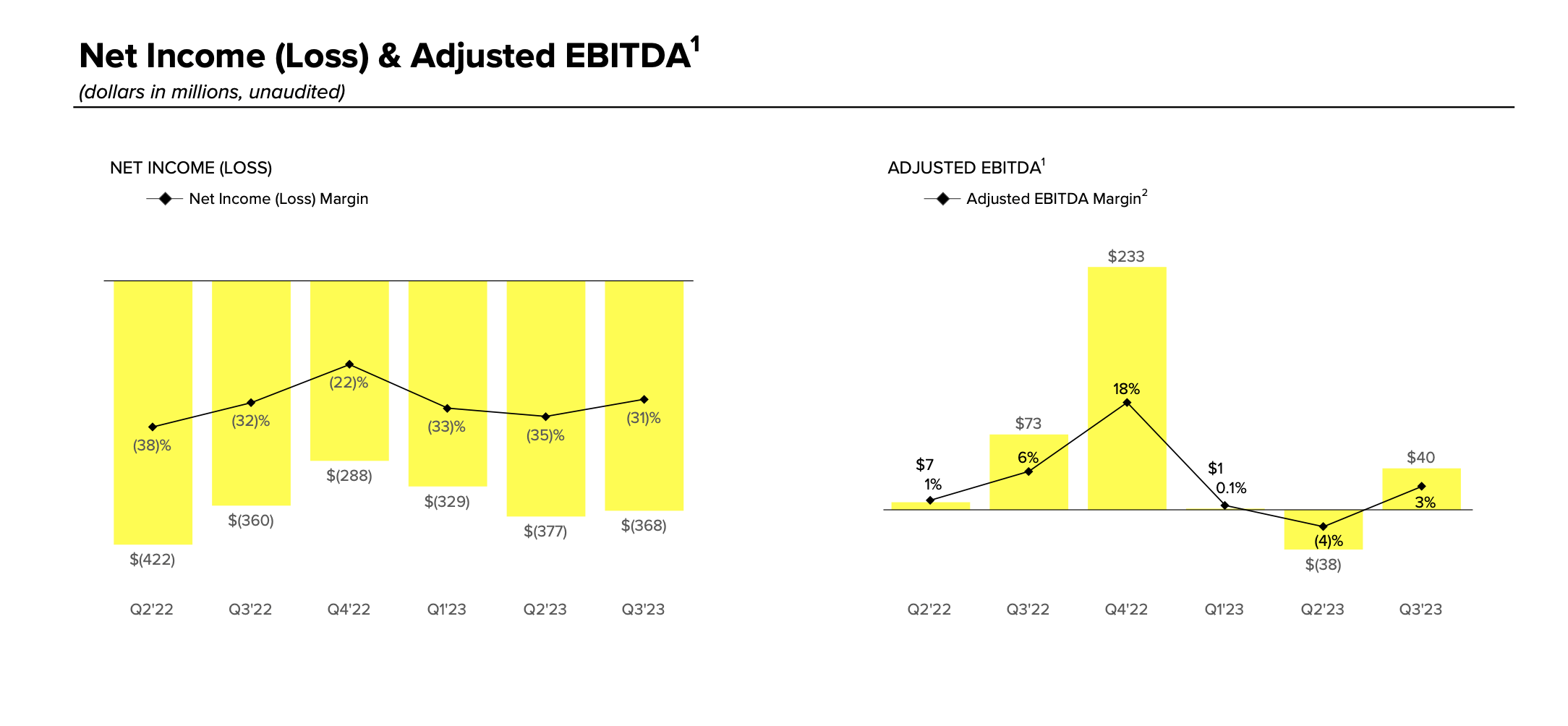

Adjusted EBITDA also cut in nearly half relative to the prior Q3, as adjusted EBITDA margin slipped to 3% - three points worse than 6% in the prior year.

Snap profitability (Snap Q3 earnings deck)

{kind=link}

Key takeaways

Ongoing deceleration in both user and revenue growth, top-line concentration in the slowest-growing region in terms of DAUs, deteriorating gross margins and EBITDA, and a heavily competitive social media field - it's difficult to point to any good reasons to stay invested in Snap. Sell off any gains that you have here and invest elsewhere.

For further details see:

Snap: Giving Up Gains Is Likely In 2024