SNAP - Snap: Long Road Back

2023-12-29 08:22:51 ET

Summary

- Snap's stock has rebounded in 2023 on the back of improved investor sentiment.

- The company's fundamentals remain poor, though, indicating ongoing issues which increasingly appear to be company-specific.

- While Snap's advertising business is struggling, user growth, Snapchat+, and generative AI are positives.

- Snap's valuation is beginning to look stretched given ongoing struggles within its ad business, limiting near-term upside potential.

Snap's ( SNAP ) stock has rebounded significantly in recent months, supported by a modest improvement in growth. While there are some positive signs for Snap's business, the increase in share price appears to be more related to a general improvement in investor sentiment rather than anything stock-specific. I pointed out earlier in the year that Snap's valuation was too low, and that the stock was likely to rise at some point as a result. Snap will likely need to demonstrate significantly improved growth, along with meaningful progress toward GAAP profitability, if the stock is to maintain its current valuation, though.

Users

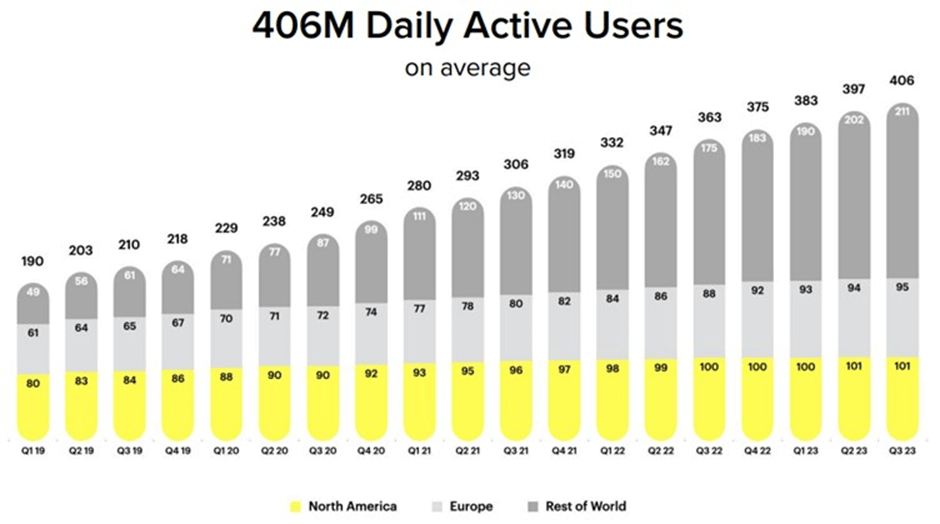

Snap's user base continues to expand at a healthy pace, but most of this growth is coming from international markets, where ARPU is relatively low. This means that the short-term impact of user growth is muted, but ultimately this will support long-term revenue growth. Snap is supporting international user growth through content localization efforts.

Figure 1: Snapchat Daily Active Users (Snap)

{kind=link}

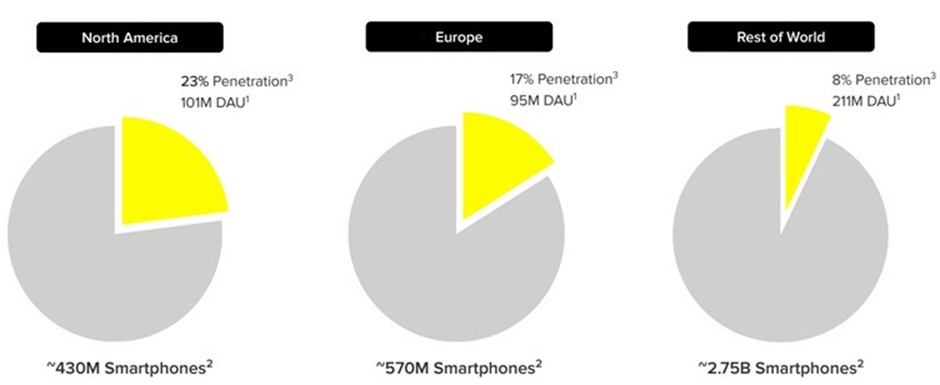

Snap's penetration of smartphone users is still only modest, even in its more mature markets. Relatively stagnant user numbers in the US over an extended period of time suggest that the platform may have already reached saturation, though. Snapchat reaches 90% of the 13- to 24-year-old population in over 25 countries. Near universal adoption amongst younger people, along with a lack of user growth in markets like the US, suggests that churn increases with age. If Snap's users were remaining engaged as they aged, the user base should be expanding as new young people begin using the platform. Despite this, Snapchat has over 750 million monthly active users, providing a significant opportunity if engagement can be increased.

Figure 2: Snapchat Penetration by Region (Snap)

{kind=link}

Content

As an app initially focused on image-based chat, Snap has had to reckon with the issue of how to monetize users without impacting the user experience and how to create and access data that is useful for guiding ads.

This is primarily being tackled with content that pulls users toward monetizable surfaces like the map and Stories. Features like Stories are more amenable to advertising and help to provide information on user interests. Additional features also help to increase engagement with the application.

Figure 3: Snapchat Core Features (Snap)

{kind=link}

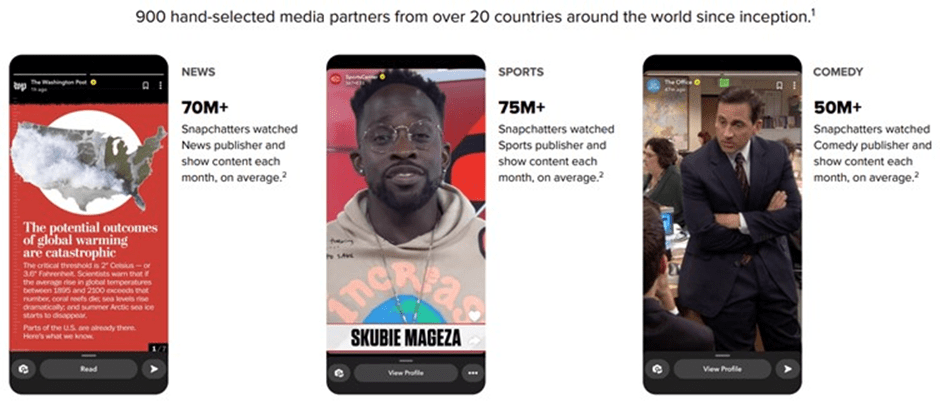

Advertising-friendly surfaces require content, though, which in the case of Stories relies on Media Partners. Content has associated costs, and the incremental impact of this on margins is not really clear. So far, the trend appears to be toward higher margins as this part of the business scales, though.

Figure 4: Snap Media Partners (Snap)

{kind=link}

Advertising

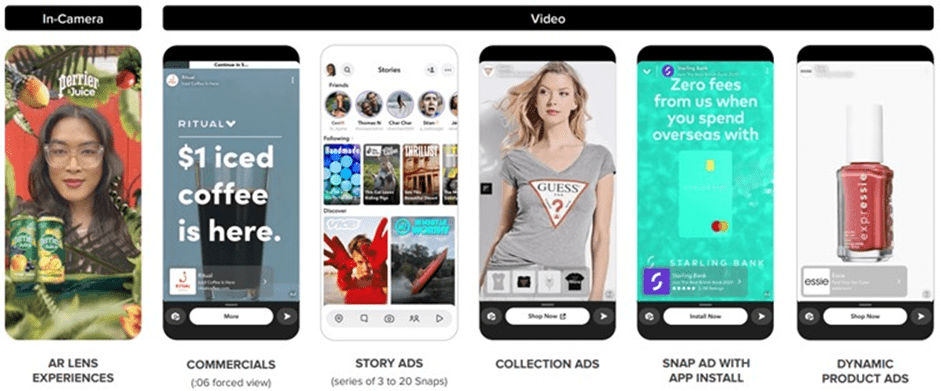

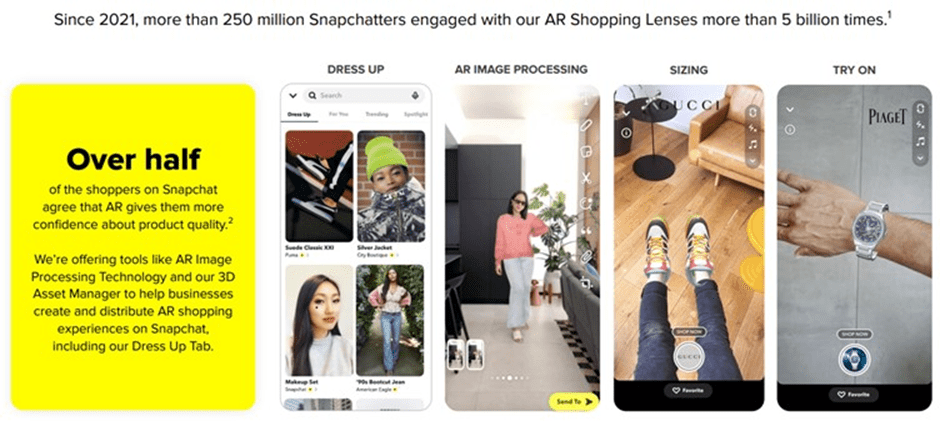

Many of Snap's surfaces are still under-monetized and offer advertisers unique capabilities. It will likely take time for advertisers to fully realize the potential of products like AR Lens Experiences, though. Recent experience suggests that advertisers continue to view Snap as a more experimental and expendable channel. Until Snap can improve targeting and attribution, its ad business is likely to remain depressed.

Figure 5: Snap Advertising Solutions (Snap)

{kind=link}

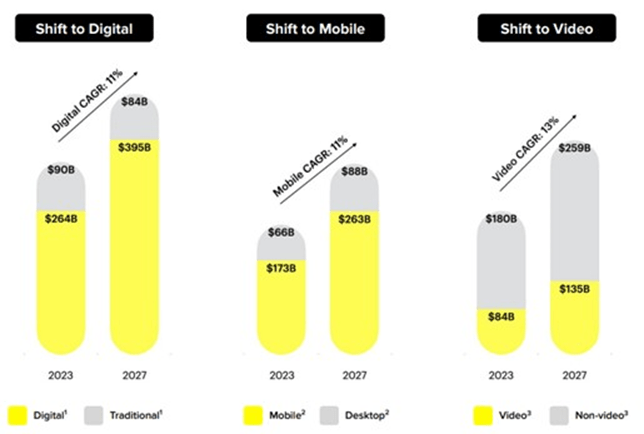

Snap's business is benefitting from secular advertising trends, even if this hasn't been apparent over the past few years. Provided Snap can overcome its current issues, this should see the company return to solid growth.

Figure 6: Advertising Industry Trends (Snap)

{kind=link}

Snap's struggles are not that surprising, given reduced access to user data on the back of privacy initiatives and Snap's lack of first-party data. The rise of features like Stories and My AI should help to provide Snap with more user data, though.

Snap has also partnered with Microsoft ( MSFT ) on sponsored links within My AI . Microsoft's Ads for Chat API connects users with partners related to the conversation occurring within My AI.

At the extreme, My AI could become a search destination for younger users. I don't see these types of offerings as a serious threat to Google ( GOOG ) though, and the economics of an LLM-powered search product are still not clear.

Generative AI

My AI is an AI-enabled chatbot which potentially helps to increase user engagement with Snapchat, generates user data that is relevant for advertisers, and provides another surface that can be monetized through either subscription or advertising.

In excess of 200 million Snapchatters have sent over 20 billion messages to My AI. Despite early traction, Snap has stated that My AI isn't a daily use product yet as it still has shortcomings (access to real-time information, etc.). Snap's main focus at the moment is on improving response quality.

Users reportedly display commercial intent, though, and Snap has taken steps to integrate that into its models to improve content and advertising. Snap has also begun testing sponsored links within My AI, which connect users with advertisers.

Snap also recently introduced Dreams, a Generative AI feature which provides users with personalized images based on selfies. Dreams is free to try, but users can pay if they want more access. This type of functionality could make generative AI a driver of Snapchat+ but it is not clear how many users will be willing to pay. In addition, innovation is likely to drive the cost of generative AI toward zero over time. As a result, value creation is only likely to come if generative AI can be embedded into Snapchat in unique ways.

Snapchat+

Snapchat+ is supporting Snap's growth and diversifying the company's revenue. Snapchat+ now has over 5 million subscribers , with revenue up more than 250% YoY in the third quarter. Snapchat+ should now be providing something like 200 million USD of high-margin revenue annually. This means that Snapchat+ is an important contributor to growth at the moment, and highlights the weakness in Snap's advertising business.

Figure 7: Snapchat+ Functionality (Snap)

AR

On average, more than 250 million Snapchatters engage with AR experiences on Snap's platform daily. AR helps to keep users engaged and provides advertisers with a differentiated product. Snap is investing a large amount in AR development, though, and the benefits of this appear questionable.

{kind=link}

Snap's AR expertise is also being leveraged through the cross-platform Camera Kit SDK. Camera Kit enables partners to build custom AR experiences for their applications. This could grow into a meaningful revenue stream in time.

Financial Analysis

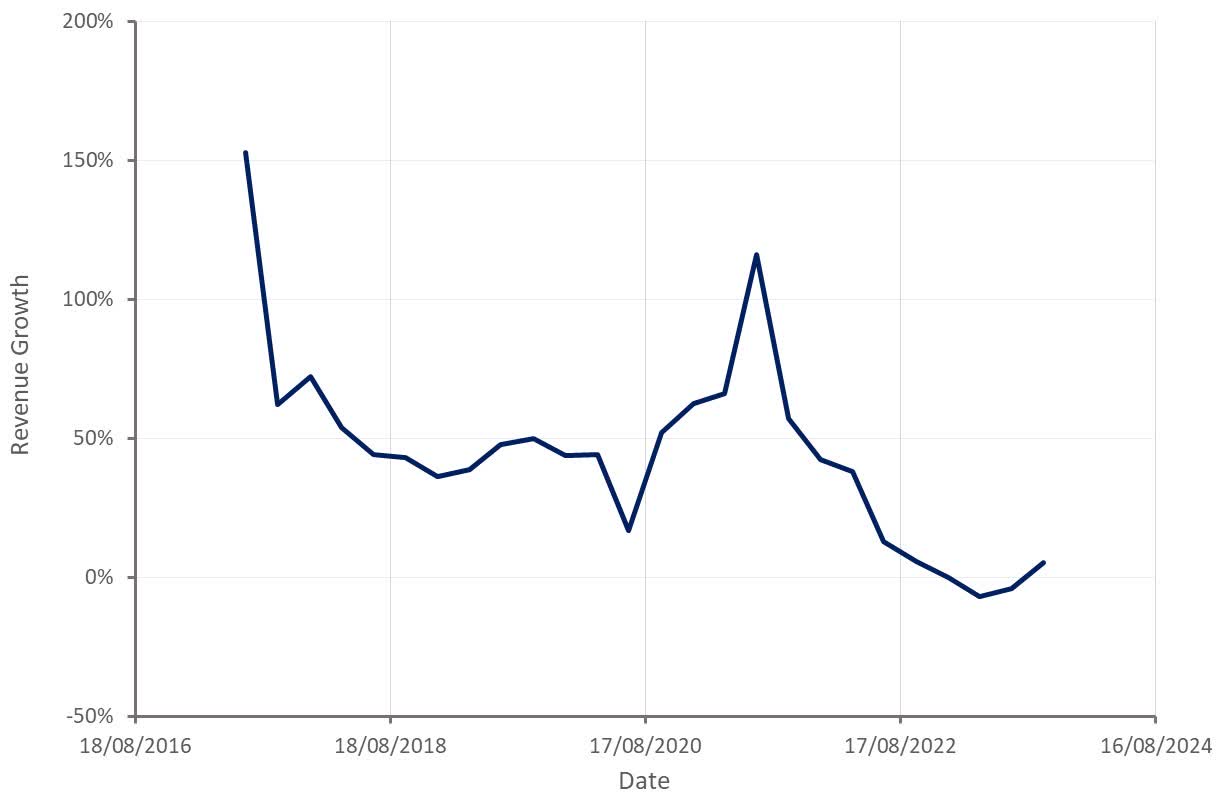

Snap's revenue increased 5% YoY in the third quarter to 1,189 million USD. While growth is improving, this is in large part the result of easier comparable periods. This should be considered disappointing given general improvements in digital advertising and how successfully Meta ( META ) has adjusted to the current operating environment.

While Snap believes its direct response advertising business is progressing, it remains cautious about the macro environment. As a result of rising geopolitical tensions and observed pauses in customer spending, Snap did not issue formal guidance for Q4. Internally, the company is forecasting 1,320-1,375 million USD in revenue, though, representing a 2-6% revenue growth rate. This guidance is particularly soft given that it is coming against a much easier comparable period.

The blow of this weak guidance has likely been softened by another leaked memo, which provides far rosier projections for 2024. Snap reportedly expects more than 475 million DAUs in 2024 and revenue growth in excess of 20%, both far in excess of consensus analyst expectations. Snap has confirmed the numbers but referred to them as internal stretch goals. Snap has a history of leaking internal goals and later falling well short of those goals, so I would not place much weight on these figures.

Figure 9: Snap Revenue Growth (Created by author using data from Snap)

{kind=link}

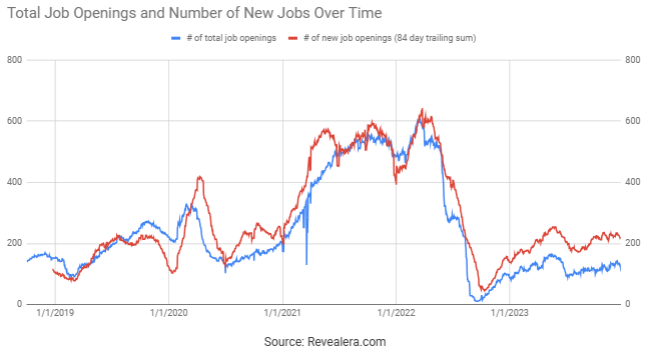

Job opening data suggests that while Snap's business has stabilized, growth doesn't appear to be accelerating. This stands in stark contrast to companies like Meta and Pinterest ( PINS ), who continue to increase hiring rates.

Figure 10: Snap Job Openings (Revealera.com)

{kind=link}

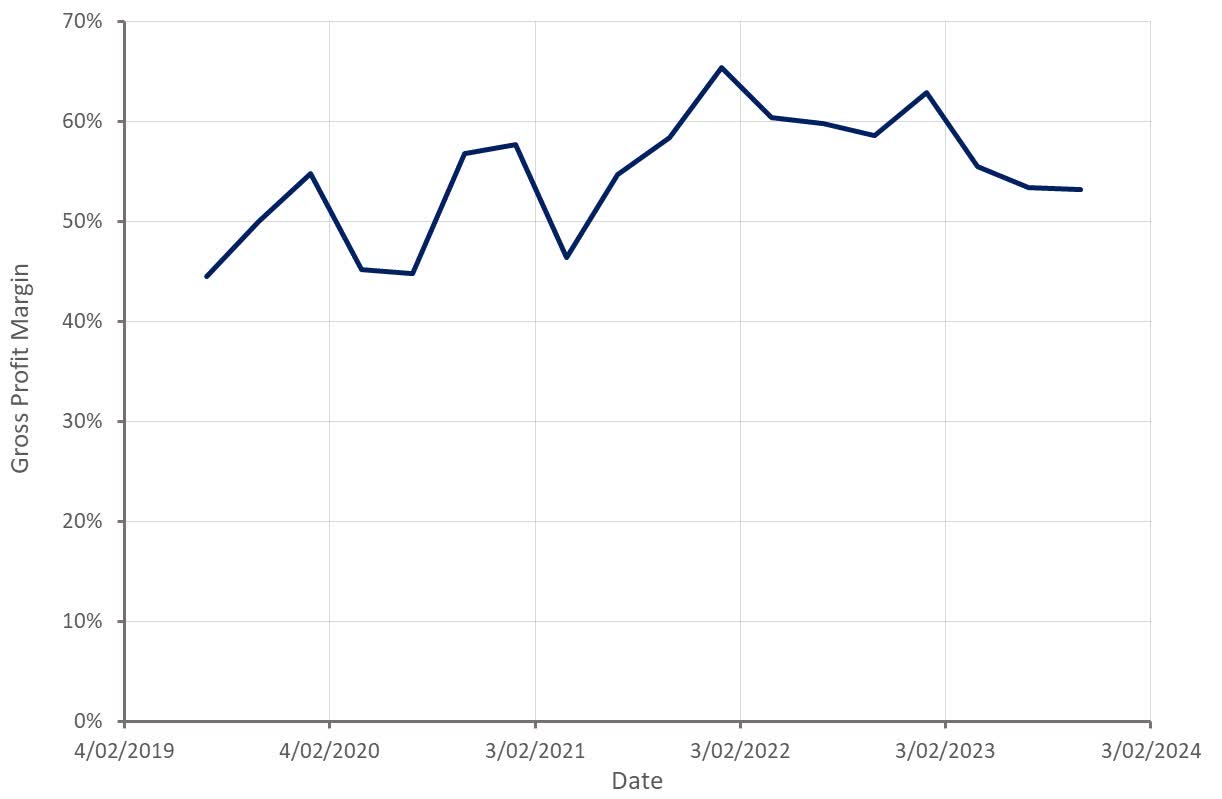

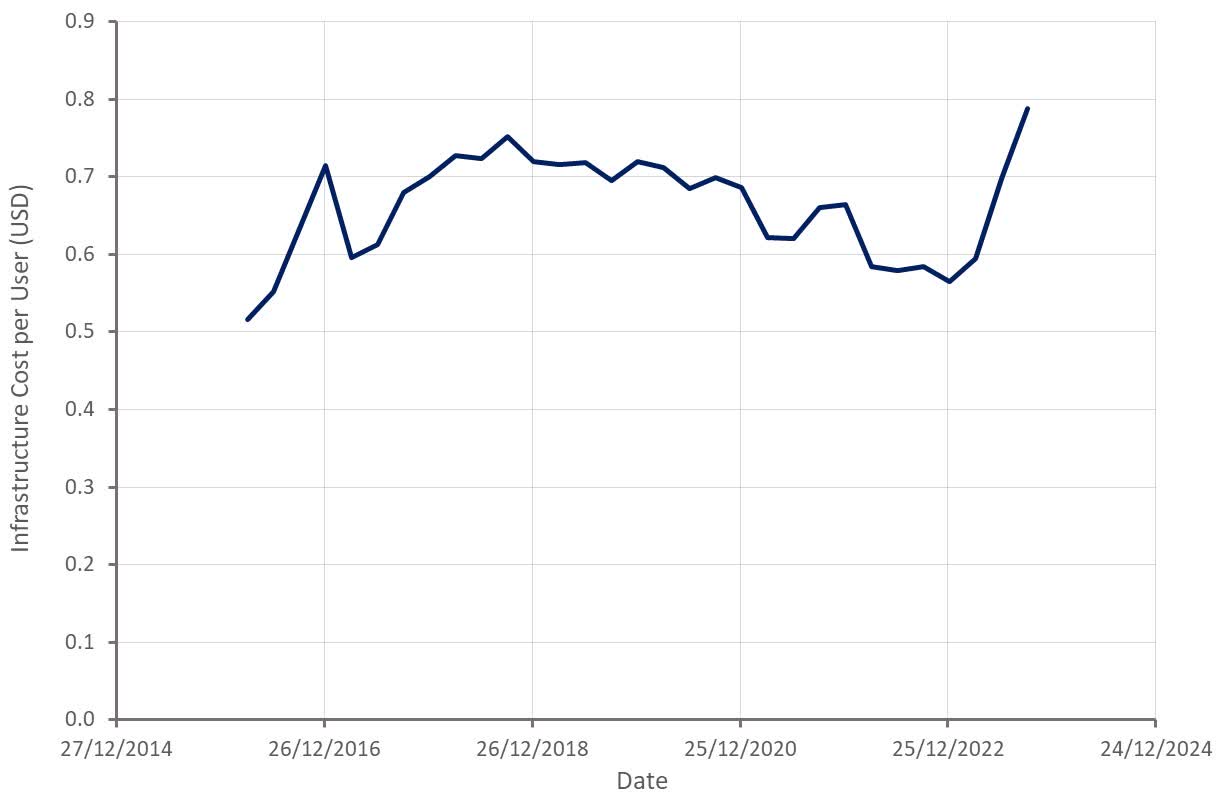

Snap's gross profit margin remains under pressure, which in large part is the result of rising infrastructure costs. This is particularly concerning given how quickly infrastructure costs are rising.

Figure 11: Snap Gross Profit Margin (Created by author using data from Snap) Figure 12: Snap Infrastructure Costs (Created by author using data from Snap)

{kind=link}

{kind=link}

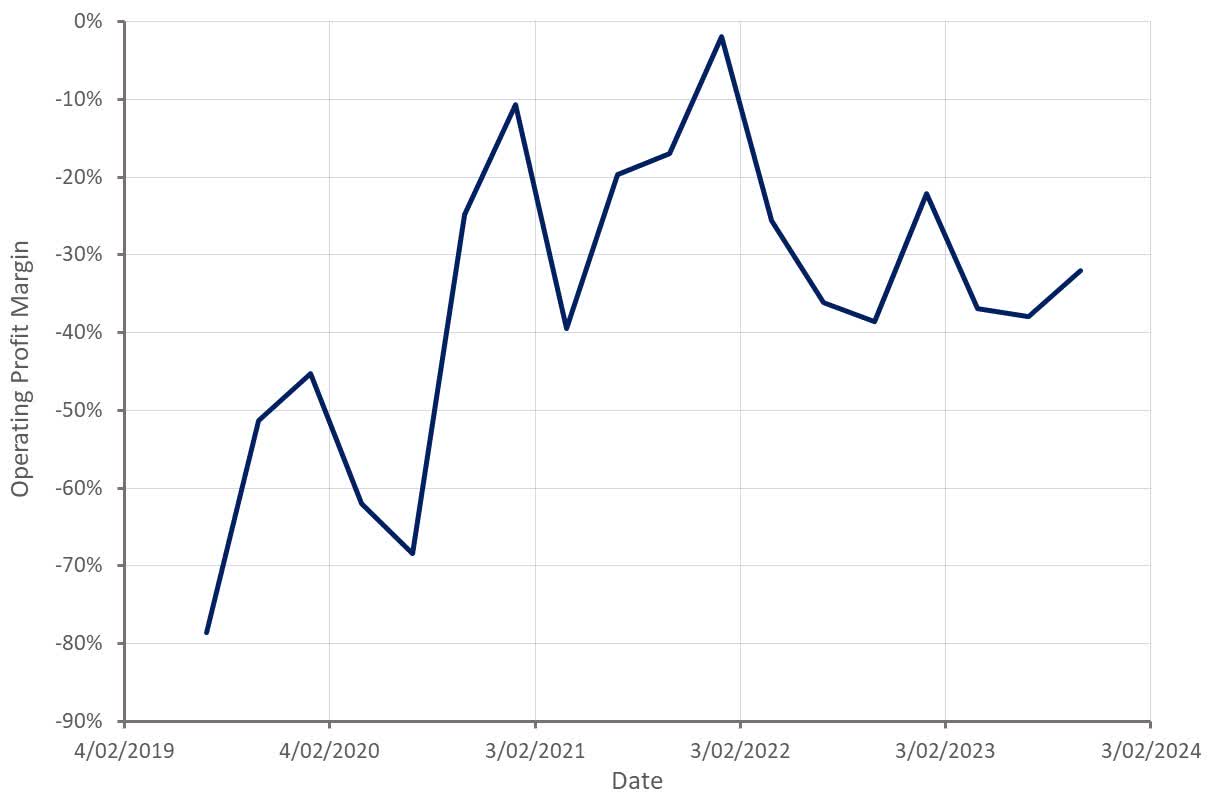

Snap has been highlighting the impact of cost control measures on its adjusted EBITDA profitability, but from a GAAP perspective, the company continues to struggle.

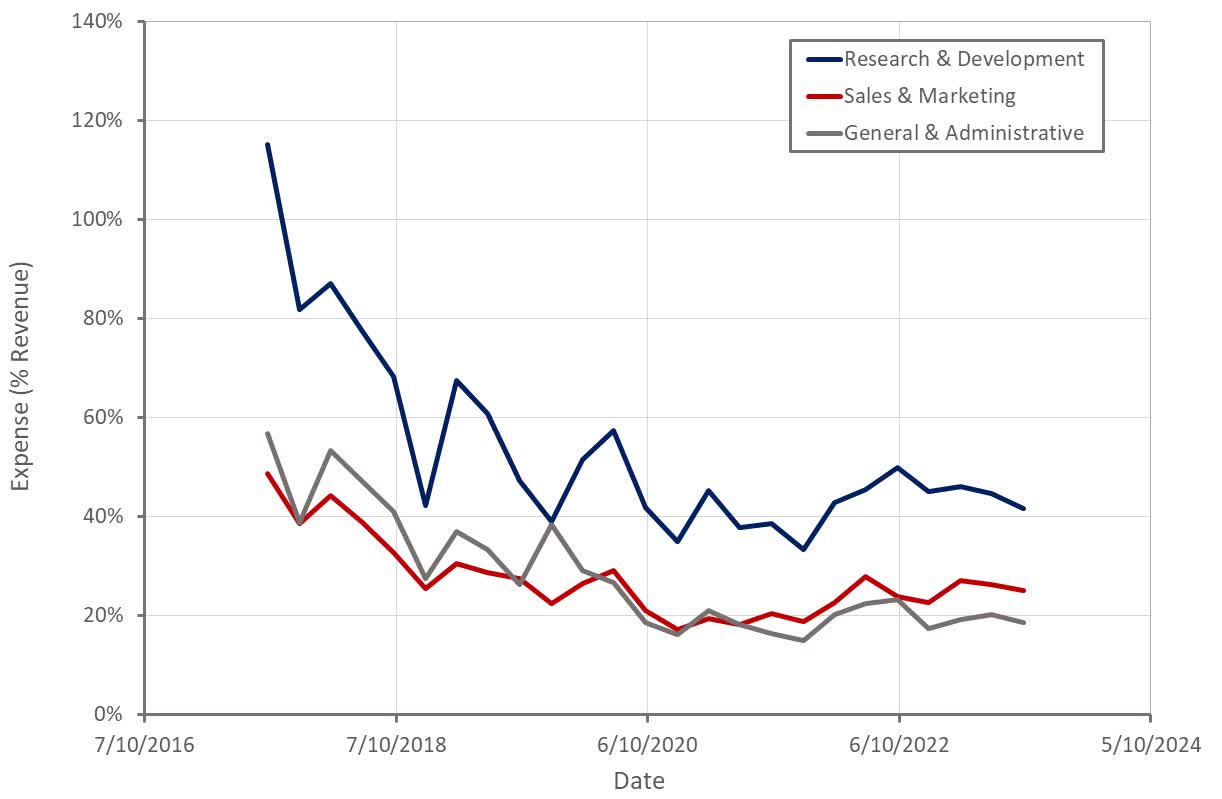

Losses remain large for a company of Snap's size, which is largely a strategic decision. Snap continues to make large investments in R&D, developing capabilities in areas like AR, hardware, and AI. An investment in Snap is to a large extent a bet that R&D will pay off in the future. I view much of this spending as unfocused and without clear strategic intent, though.

Figure 13: Snap Operating Expenses (Created by author using data from Snap) Figure 14: Snap Operating Profit Margin (Created by author using data from Snap)

{kind=link}

{kind=link}

Conclusion

I made the case earlier in the year that Snap's stock was probably near the bottom, based on its valuation and improving digital advertising market fundamentals. This has proven to be the case, although this appears to be more the result of a broad-based improvement in investor sentiment rather than anything Snap-specific.

Snap's advertising business continues to struggle, and the company's margins are being pressured by investments in areas like AI and AR. On a positive note, user growth remains solid and Snapchat+ is becoming a meaningful contributor.

I tend to think that Snap's stock will do ok from current levels over the long run, given the strength of its user base and its differentiated platform. Snap's valuation is beginning to look stretched given the company's ongoing struggles, though. As a result, the next 12 months could prove tough as Snap still needs to improve its adtech stack and any recovery in digital advertising is likely to be modest.

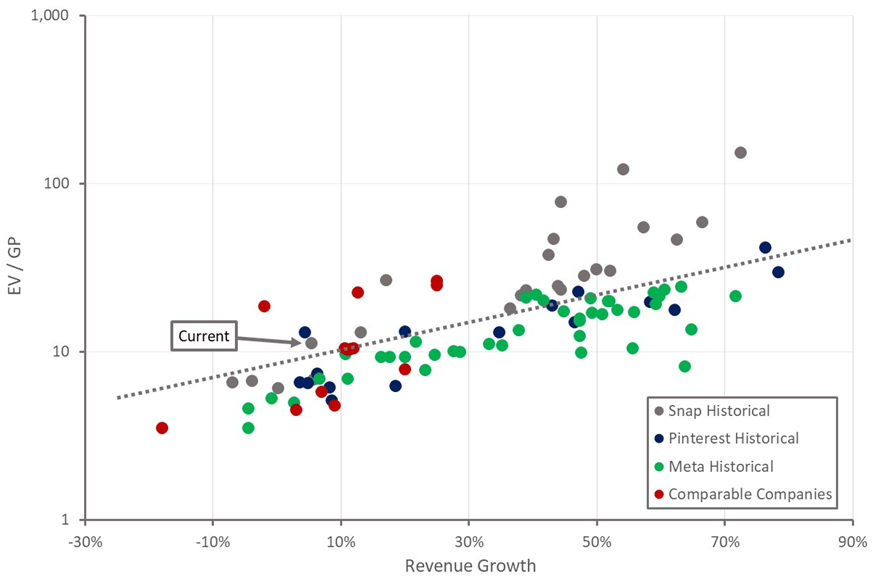

Figure 15: Snap Relative Valuation (Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Snap: Long Road Back