SNAP - Snapchat Is Rising But Why? I Urge Caution

2023-12-21 10:55:22 ET

Summary

- Snapchat has rallied hard from the lows, but I question if the rally is justified.

- Investors should be asking why Snapchat is not executing as strongly as peer Meta Platforms.

- Consensus estimates look aggressive, and the stock does not look that cheap even when compared to those estimates.

- Tech stocks are booming, but investors should exercise great caution.

Snap Inc. ( SNAP ) has benefitted from a sudden tech stock rally despite seeing continued financial stress. The company has seen revenue growth slow to a crawl while user growth, while still healthy, has slowed as well. The company has seen its adjusted EBITDA slip to near breakeven and now has a net debt balance sheet. The valuation can work out if the company can meet consensus estimates, but I am of the view that both top and bottom line estimates are too aggressive. I am also of the view that the company is not executing as strongly against TikTok's competitive threats as larger peer Meta Platforms, Inc. ( META ) and thus faces unique existential risk. I reiterate my neutral rating for the stock.

SNAP Stock Price

SNAP is one stock that I would not have guessed would be trading near 52-week highs. The tech sector as a whole has been melting up, perhaps due to hopes for several interest rate cuts next year.

I last covered SNAP in August where I expressed caution given the tough fundamentals and increasingly strained balance sheet. The company has finally reached a net debt position as predicted, but I continue to be concerned that the company is underperforming the results seen at META.

SNAP Stock Key Metrics

In its latest quarter, SNAP generated 5% YoY revenue growth to $1.189 billion, coming ahead of guidance for between $1.07 billion and $1.13 billion. Before celebrating that guidance beat, we must note that in contrast, META delivered 23.7% YoY growth in advertising revenues.

2023 Q3 Presentation

The bright spot for SNAP has historically been growth in average daily active users ('DAUs'), which grew by 12% YoY to 406 million. However, even here there are reasons for concern. Substantially all of the growth came from lower revenue Rest of World users, with North America seeing just 1% YoY growth. META, despite having a larger user base, actually saw North American users grow by 1.9% YoY.

2023 Q3 Presentation

SNAP saw average revenue per user ('ARPU') decline by 6% on a global basis, dragged down by a 4% decline in North America. A lot of that could be explained by the increasing investment in Spotlight, which is the company's answer to TikTok and carries lower monetization rates. It is worth noting that SNAP has seen a solid sequential improvement in ARPU in both North America and Europe.

2023 Q3 Presentation

As stated earlier, SNAP has been investing heavily in Spotlight ads which help it compete with TikTok, but carry a lower rate of monetization. This is evidenced by the deterioration in gross margin which declined by 700 bps YoY.

2023 Q3 Presentation

SNAP saw adjusted EBITDA decline by 45% YoY though it did swing back to positive territory after coming in negative in the second quarter.

2023 Q3 Presentation

The company ended the quarter with $3.6 billion of cash versus $3.7 billion of debt, marking its first quarter with net debt ever as a public company (to my knowledge). The lack of material net cash means that SNAP is not generating material interest income on top of adjusted EBITDA (as is typical among many tech peers) - this in part contributed to the company burning through $61 million in free cash flow in the quarter.

2023 Q3 Presentation

Looking ahead, management gave informal guidance for up to 412 million in DAUs, between $1.32 billion and $1.375 billion in revenue (implying 2% to 6% YoY growth), and adjusted EBITDA between $65 million and $105 million.

On the conference call , management acknowledged inherent uncertainty arising from the Israel-Hamas war. More importantly, management discussed the leaked memo from mid-October in which management had laid out 2024 goals of 20% advertising revenue growth and 475 million users. Management stated that the revenue goal was "really about making more progress in terms of customer success, especially with the lower funnel." The skeptic in me wants to point out the difficulty in counting on a turnaround, though it bears remembering that just a couple of quarters ago META had shown a sudden recovery in its own revenue growth profile. I am doubtful that SNAP will see a recovery to the 20% level, but it should be noted that SNAP was growing faster than META heading into the post-pandemic slowdown.

Is SNAP Stock A Buy, Sell, or Hold?

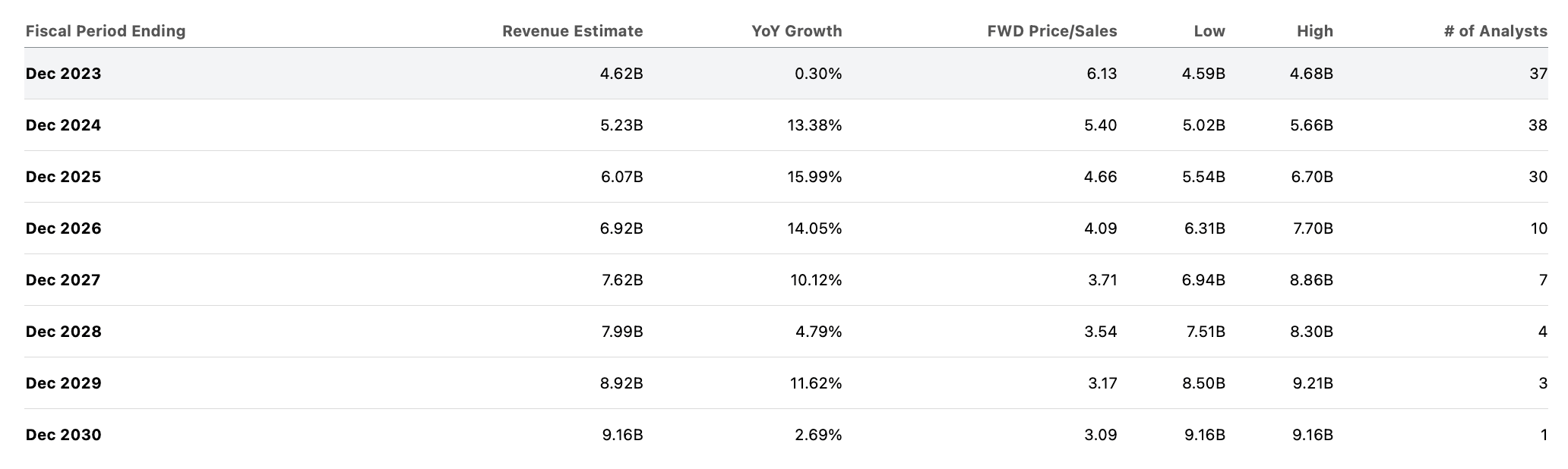

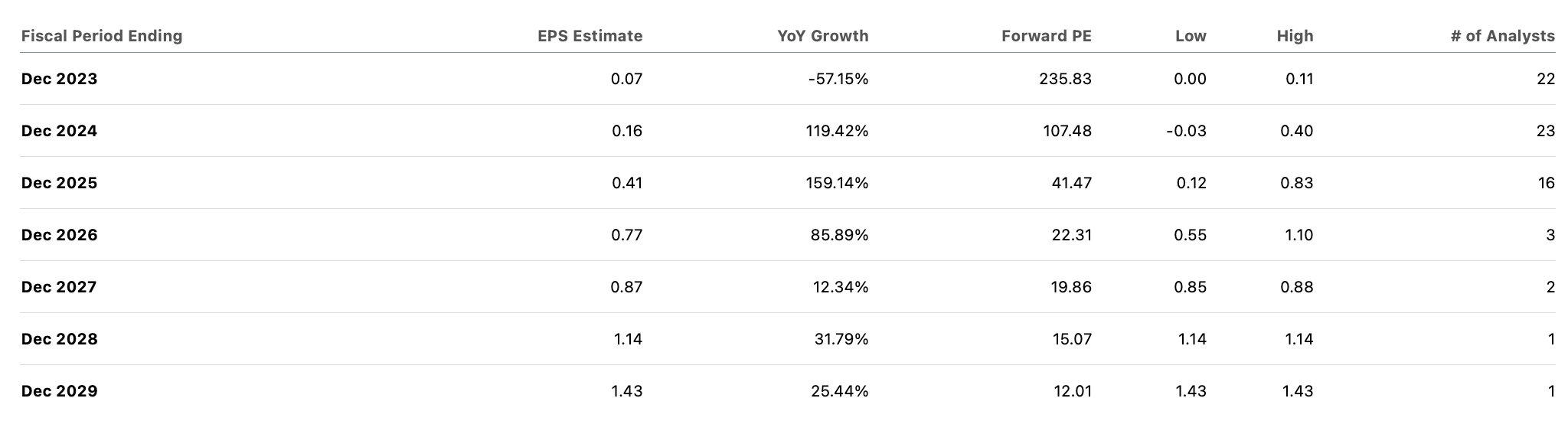

Consensus estimates appear skeptical as well, though they still see the company sustaining double-digit top-line growth for many years.

{kind=link}

Consensus estimates expect the company to eventually achieve 26% net margins by 2029, at which point the stock would be trading at apparently reasonable valuations.

{kind=link}

Let's say that SNAP can achieve consensus estimates, which do not look obviously conservative. Instagram tends to have greater engagement and I have the opinion that SNAP appears to be more at risk from TikTok. Instagram is benefitting from META's artificial intelligence prowess and I view SNAP to have a lot of overlap with TikTok from a usage perspective. After 2029, SNAP might be a low single-digit grower. The stock might deserve a 15x earnings multiple - that implies a stock price of around $21.45 per share, implying a modest upside over the next six years. If we assume a 20x earnings multiple, that upside rises to 9%. Given the net debt balance sheet and strong competitive threats posed by TikTok and META, I find that return proposition to be unsatisfactory. Investors should wait for evidence of an acceleration in revenue growth as well as execution against expanding profit margins before making this leap but even then, the prospective return does not look attractive enough.

Some investors may be investing in SNAP due to the potential for a nationwide ban on TikTok. I find such a ban to be unlikely, especially after Montana's state-wide ban was blocked by a federal judge . Given where the stock stands today, I am of the view that investors are not appreciating the potential downside risk stemming from first the competitive threats which may exacerbate the net debt balance sheet. Given that the company has not yet shown tangible signs that a sustained acceleration in revenue growth is around the corner, this is the kind of stock that I'd feel more comfortable buying at below 3x sales. Assuming 25% long-term net margins, that would equate to 12x long-term earnings, which feels about right given the elevated risks here. I reiterate my neutral rating - investors should not chase the momentum here.

For further details see:

Snapchat Is Rising, But Why? I Urge Caution