SNOW - Snowflake: A Solid Cloud Growth Play For 2024 And Beyond

2024-01-12 05:44:07 ET

Summary

- Snowflake is experiencing significant growth in customer acquisition and revenue, particularly in the lucrative top end of the enterprise market.

- The company generated its highest-ever quarterly revenue in Q3 2023, showing 32% YoY growth.

- Despite a declining net revenue retention rate, Snowflake is expected to deliver double-digit top line growth in FY 2024.

- Snowflake is expected to grow to a $10B annual revenue volume by FY 2029.

Snowflake (SNOW) has emerged as a major force in the market for data cloud services and the company benefits from significant momentum in customer acquisition and related top line growth. Snowflake is growing rapidly and especially has made inroads in the lucrative market for enterprise customers that spend at least $1M on the cloud company's products and services annually. Despite a declining net revenue retention rate, Snowflake still sees very impressive growth rates and the firm is set to deliver double-digit top line growth in FY 2024 as well. Although shares are not cheap based off of revenues, I believe the momentum in the business justifies paying a premium multiplier!

Previous rating

I worked on Snowflake about a year ago -- A Top Buy For Cloud Investors -- in which I mentioned the large addressable market opportunity in the cloud data market as well as an improving free cash flow picture as reasons to buy the firm's shares. Given that Snowflake continues to impress in terms of customer acquisition (especially in the large enterprise account segment) and revenue growth, I believe that the company remains a top bet for investors in the cloud data market going forward.

Snowflake retains solid revenue momentum

Snowflake provides cloud-based data storage and analytics services and the company has seen strong product uptake from its core enterprise customer base during the pandemic as well as after COVID-19. Snowflake generated its highest-ever quarterly revenue volume in the third-quarter as it billed its customers $734M, showing 32% year-over-year growth. The largest block of revenues came from product sales, $698M, while the relatively small revenue block of $36M related to professional revenues. Product revenues are primarily derived from the consumption of compute, storage, and data transfer resources while professional revenues relate to other services rendered such as consulting, technical solution services and platform training.

Snowflake

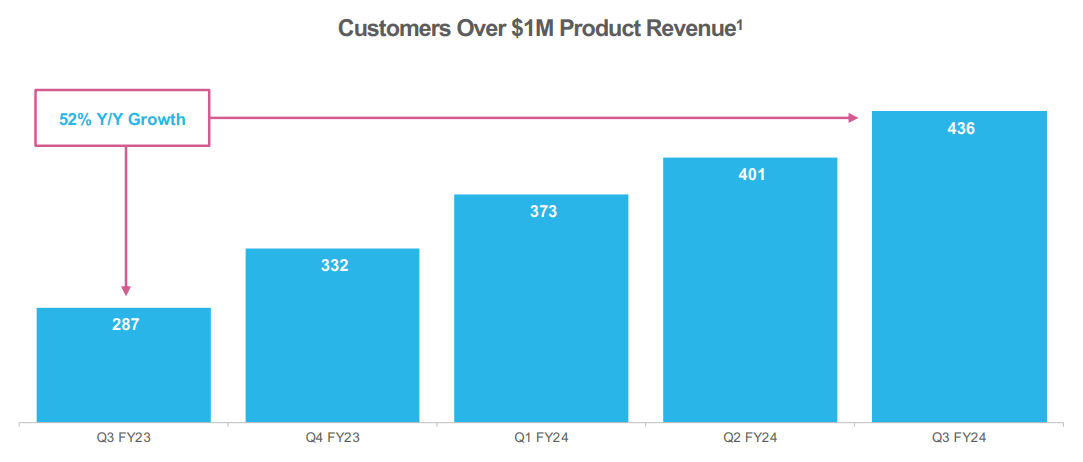

One particular group of clients stands out that is driving Snowflake's revenue growth and this group consists of enterprise customers that spend at least $1M annually on the firm's products and services. As you can see in the chart below, this particularly lucrative customer cohort is growing much faster than Snowflake's total customers (+24 Y/Y growth). In Q3'23, Snowflake's top customers grew at a 52% year-over-year rate, providing crucial support for consolidated revenue growth. These enterprise customers are also becoming more important for Snowflake as a percentage of the total customer count: in Q3'23, Snowflake's top clients accounted for 5% (+25% Y/Y growth) of all customers compared to 4% in the year-earlier period.

{kind=link}

Based off of consensus estimates provided by Seeking Alpha, Snowflake is projected to harness double-digit top line growth in FY 2024 as well as in the years that follow. The consensus revenue expectation for next year is $3.64B, implying a top line growth rate of 30%. Although Snowflake's revenue growth rate is moderating, the cloud-based data company is expected to grow its revenues at an average annual rate of 31% in the next five years.

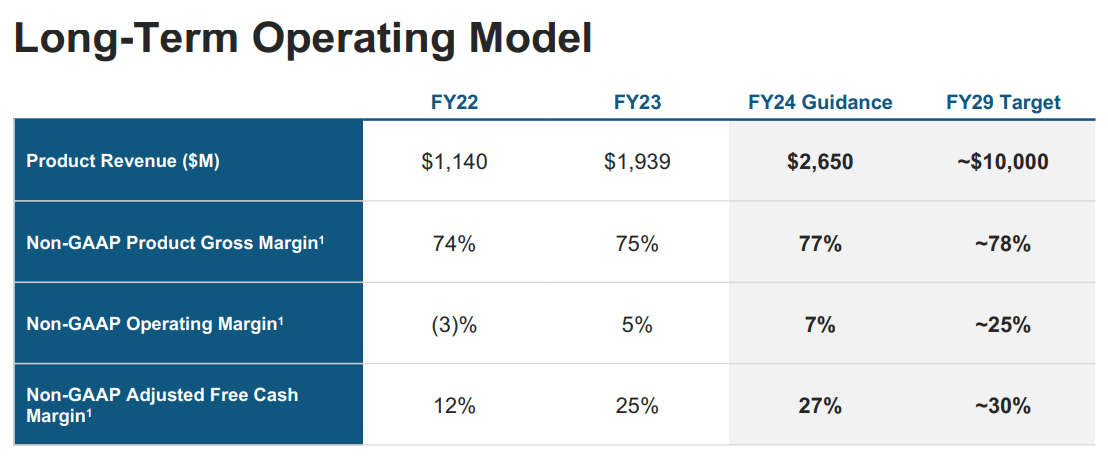

This reconciles with the company's operating model with projects revenues of approximately $10B by FY 2029 and a free cash flow margin, adjusted, of approximately 30%.

{kind=link}

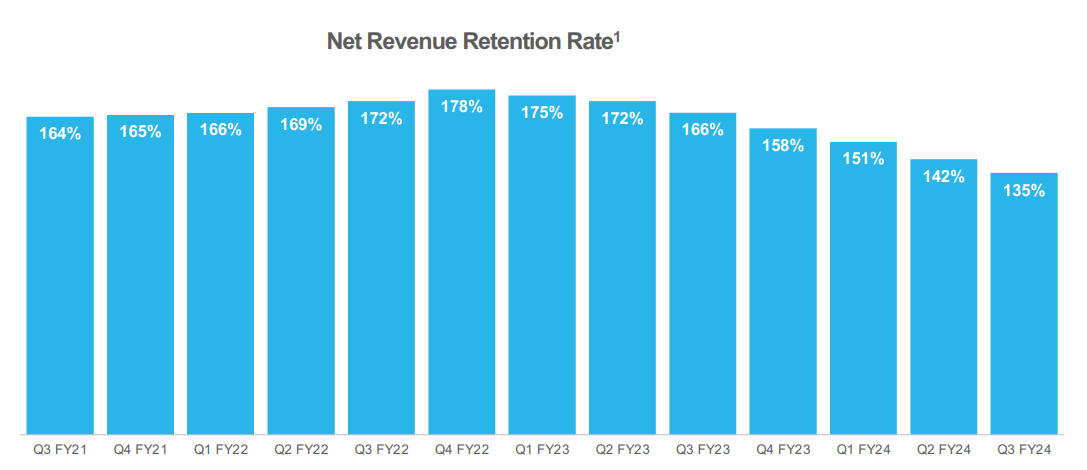

Snowflake's net retention rate trend and monetization success

Software companies measure their monetization success through a metric called net revenue retention rate/NRRR. This rate is known sometimes by other names such as dollar-based net retention rate or similar terms, but they all measure the same thing: the retention rate expresses how successful a company is growing its revenues organically from the same customer pool from one reporting period to the next. This figure is influenced by a company's ability to upsell customers to new products and services and is usually expressed as a percentage.

Snowflake's net revenue retention rate declined seven quarters in a row, but despite the decline was still a solid 135% in Q3'23. The down-trend in the retention rate does put a bit of a stain on the Snowflake thesis, but I believe the other factors discussed here still make the firm an attractive buy for investors that look for exposure to the rapidly-growing cloud-computing market. The net revenue retention rate of 135% implies that the firm's customers are still boosting their spending quite drastically. To me, the trend in the NRRR only becomes a real problem if it dropped below 100% because then Snowflake would not be able to generate organic revenue growth.

{kind=link}

Snowflake's valuation

As I mentioned previously, Snowflake is projected to generate revenues of $3.64B in FY 2025 which implies a price-to-revenue ratio of 17.8X. This is not a cheap revenue multiplier factor, but none of the cloud companies really are cheap. If we look at revenue multipliers of other cloud-based software companies like Cloudflare ( NET ), Datadog ( DDOG ) or MongoDB ( MDB ) we can see that investors pay a premium multiple for pretty much all of them... and the reason for this is the exceptionally strong growth curve these companies are on. Snowflake is the most expensive cloud-based companies in the industry group below, but shares are trading significantly below the 1-year average P/S ratio of 30.0X. If Snowflake returned to a 30.0X revenue multiplier, shares would have 68% upside potential. Personally, I see a 20X P/S ratio as not unrealistic given the current rate of top line growth which could give the software company a fair value around 12%. Again, the fair value is a dynamic number and may rise and fall together with changes in the revenue trajectory.

Snowflake's risk profile

As a fast-growing and highly-valued cloud-based software company, Snowflake is vulnerable to a growth slowdown in customer accounts and product revenues which could weigh more heavily on the company's valuation factor going forward. What I also see as a risk down the road is that the company's net revenue retention rate could drop towards 100% which would indicate more urgent short term organic revenue growth challenges.

Closing thoughts

Snowflake, despite its high valuation factor, is still a very well-run cloud-based software company with considerable momentum in customer growth, especially as it relates to the top end of the enterprise market, which in my opinion supports the valuation. The company has made considerable inroads in the lucrative enterprise segment and Snowflake is expected to grow its top line at an average annual rate in excess of 30% and move towards a $10B annual revenue volume by FY 2029. I believe the risk profile is still very much favorable and I continue to see Snowflake as a buy, despite downward pressure on its net revenue retention rate!

For further details see:

Snowflake: A Solid Cloud Growth Play For 2024 And Beyond