SNOW - Snowflake: Despite Easing Headwinds Recovery Will Take Time

2023-11-24 09:21:02 ET

Summary

- While consumption headwinds are easing, it will take time for Snowflake's business to recover.

- The impact of AI on Snowflake's business is uncertain and may take time to materialize, potentially setting investors up for near-term disappointment.

- Snowflake's high valuation poses a downside risk if growth fails to stabilize in the coming quarters.

While optimization is still a problem for Snowflake Inc. ( SNOW ), consumption headwinds appear to be easing. A return to more normal consumption growth and the introduction of new products should support growth going forward, but it will take time for Snowflake's business to bounce back. While AI is expected to be a large positive, it is not clear how much Snowflake will benefit in the near term, or when the impact will be seen. Snowflake's valuation remains high, creating downside risk if growth fails to stabilize in the coming quarters.

Market

The macro environment remains difficult, but Snowflake has suggested that sentiment is improving. There is also evidence that customer optimization efforts are beginning to ease, which should help support consumption growth going forward. Caution is still warranted as Snowflake's operating environment appears to be stabilizing rather than improving.

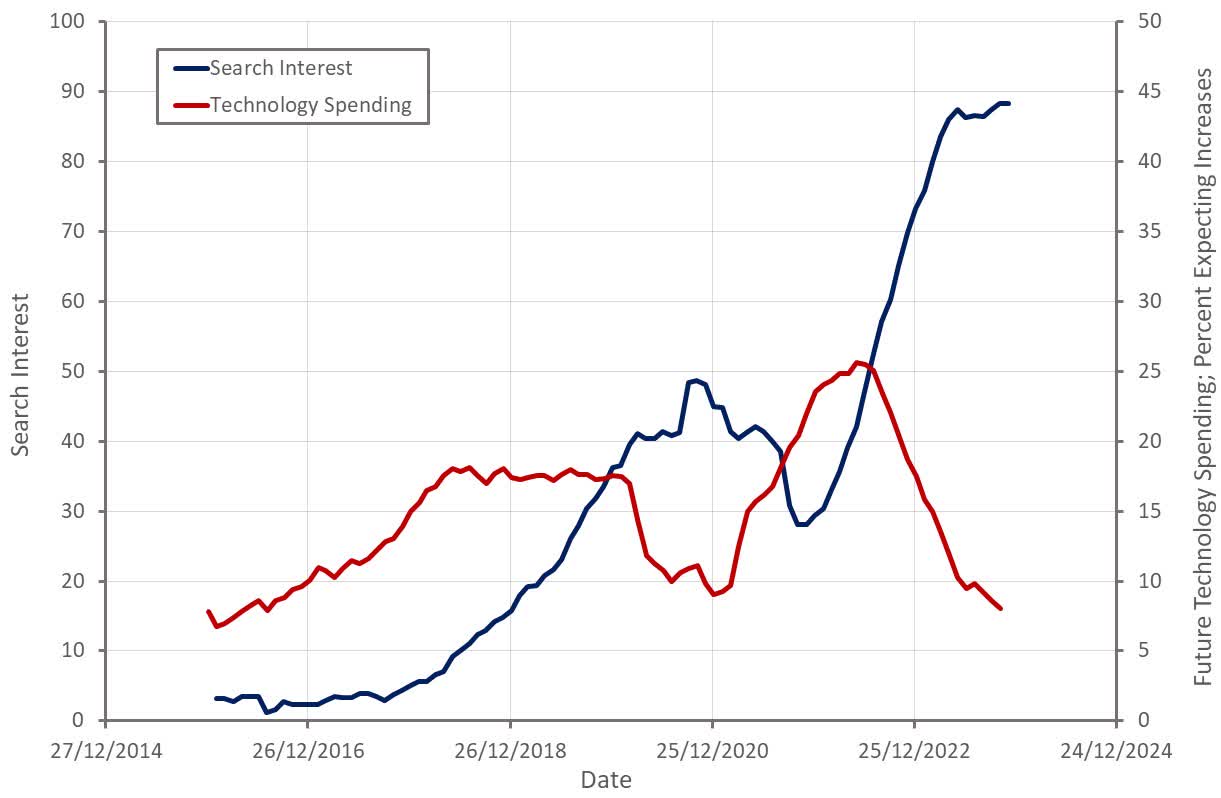

Figure 1: "Snowflake Pricing" Search Interest (Source: Created by author using data from Google Trends and The Federal Reserve)

{kind=link}

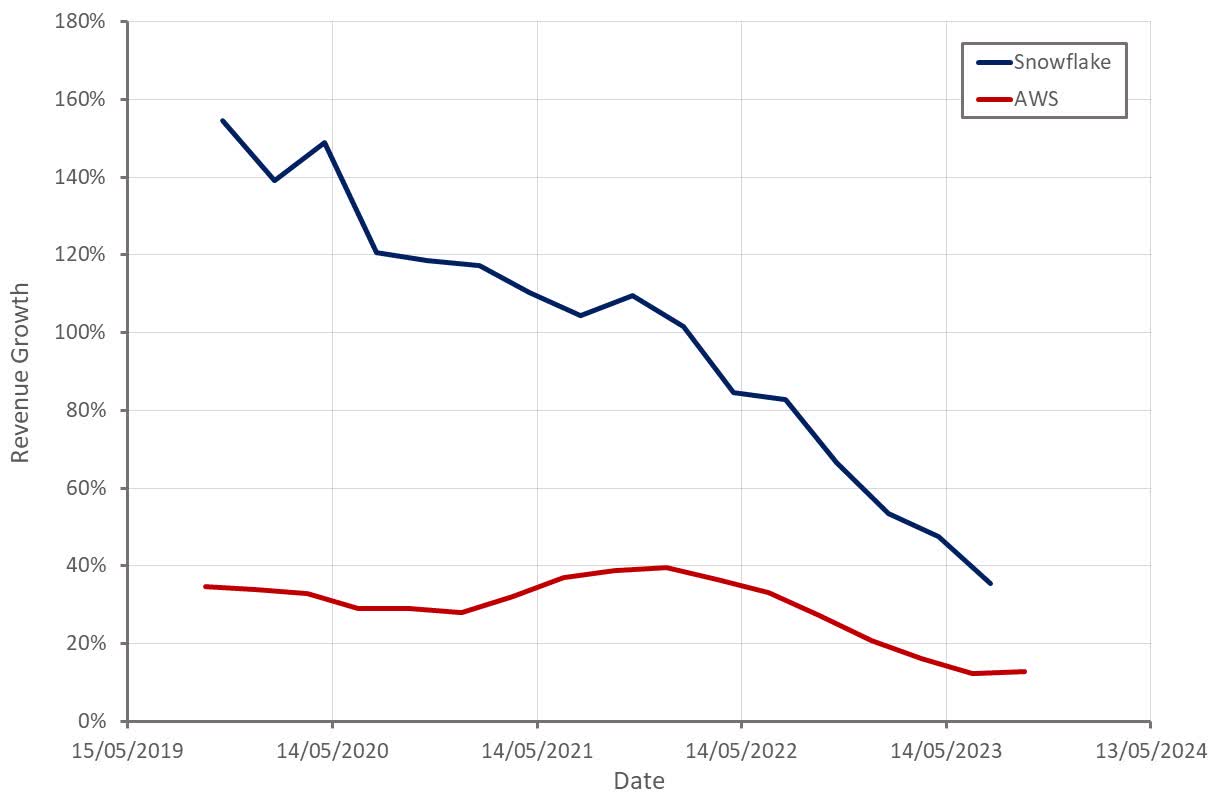

The difficult operating environment can also be seen in AWS' ongoing struggle. The vast majority of Snowflake's revenue comes from workloads running on AWS and the two businesses show somewhat similar growth trends. While AWS' growth appears to have stabilized, there is no sign of acceleration that would provide optimism regarding Snowflake's near-term prospects.

Figure 2: Snowflake and AWS Revenue Growth (Source: Created by author using data from company reports)

{kind=link}

Snowflake's data platform potentially gives it exposure to the current AI boom and the company is increasing this exposure through innovations like Snowpark. While generative AI is front of mind for many customers, the size and timing of any consumption benefit for Snowflake is unclear.

Investment in AI has obviously surged in 2023 as evidenced by NVIDIA's rapid data center revenue growth. The primary benefit so far has been for semiconductor companies though. Snowflake doesn't expect AI spend to really begin impacting the software layer until next year. Organizations are still struggling to get GPUs and there is a time lag between when hardware is received and actually deployed in a data center. Snowflake has stated that it typically takes 6 months from when the hardware is purchased to when it goes into production.

Figure 3: NVIDIA Data Center Revenue (Source: Created by author using data from NVIDIA)

{kind=link}

Snowflake

Snowflake originally focused on providing a scalable cloud database, based on a cost advantage from separating storage and compute. From an investor perspective, the most compelling part of the company is the vision around enabling data sharing and bringing applications to the data. This is supported by Snowflake's strong governance capabilities and product innovations like Snowpark and Streamlit, which enable data science workloads and make Snowflake an application platform.

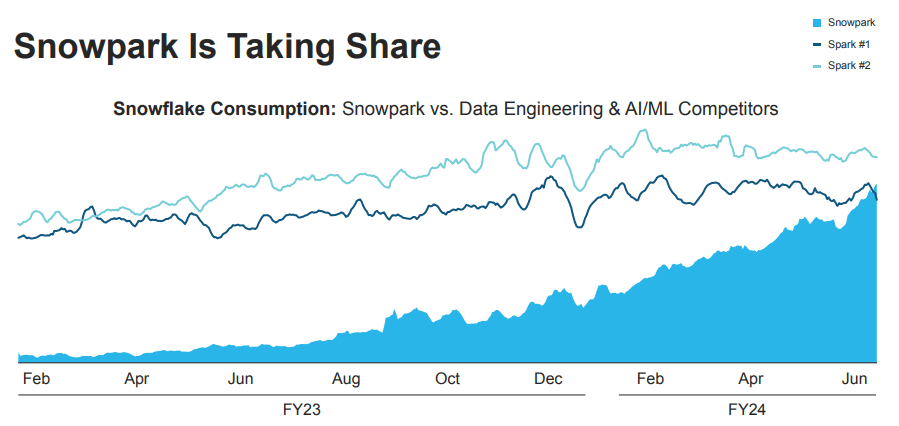

Snowpark is the programmability platform for Snowflake and takes the platform more in the direction of Databricks. Snowflake added over 400 Snowpark customers in Q2 FY2024 and consumption increased 70% sequentially. Adoption is particularly strong amongst larger customers, with 63% of Snowflake's Global 2000 customers using Snowpark on a weekly basis. While Snowpark's revenue is growing, it is still relatively small (a couple percent of revenue).

Figure 4: Snowpark Consumption Growth (Source: Snowflake)

{kind=link}

Container Services is another recently announced product that should help to drive long-term growth. Container services are a part of Snowpark and are similar to virtualization, allowing any workload to be deployed on Snowflake. Since being announced several months ago, hundreds of customers have requested access to the private preview of Snowpark Container Services.

Native apps allow developers to focus on application development as Snowflake takes care of things like security and deployment. Streamlit is a framework for data scientists to create applications and experiences for AI and ML. There are now over 145,000 monthly active developers on Streamlit, a 160% increase YoY. Snowflake is supporting this business through a start-up program, which contributed approximately 20% to new customers in the second quarter.

Unistore is another important introduction for Snowflake as it allows the company to address use cases that otherwise would not be suitable for an OLTP database. Unistore utilizes what Snowflake refers to as a hybrid table, which features a storage system optimized for analytics and a storage system optimized for fast reads and writes.

Table 1: Snowflake Product Adoption (Source: Created by author using data from Snowflake)

Given Snowflake's recent struggles, it would be reasonable to question the company's competitive position, but there is no real reason to think that competition is a large issue for Snowflake at this point in time.

Snowflake and Databricks are encroaching on each other's core markets. Snowflake reportedly doesn't see a lot of competition from Databricks in SQL and competes with Databricks within existing customers on a workload-by-workload basis based on cost.

In terms of the hyperscalers, the majority of Snowflake's revenue comes from workloads on AWS (~78%), followed by Azure (~20%) and then GCP (~2%). Snowflake's contribution margin for workloads on AWS and Azure is 80-82%, compared to only around 58% for GCP. This suggests that Google is competing more aggressively with its BigQuery product.

Financial Analysis

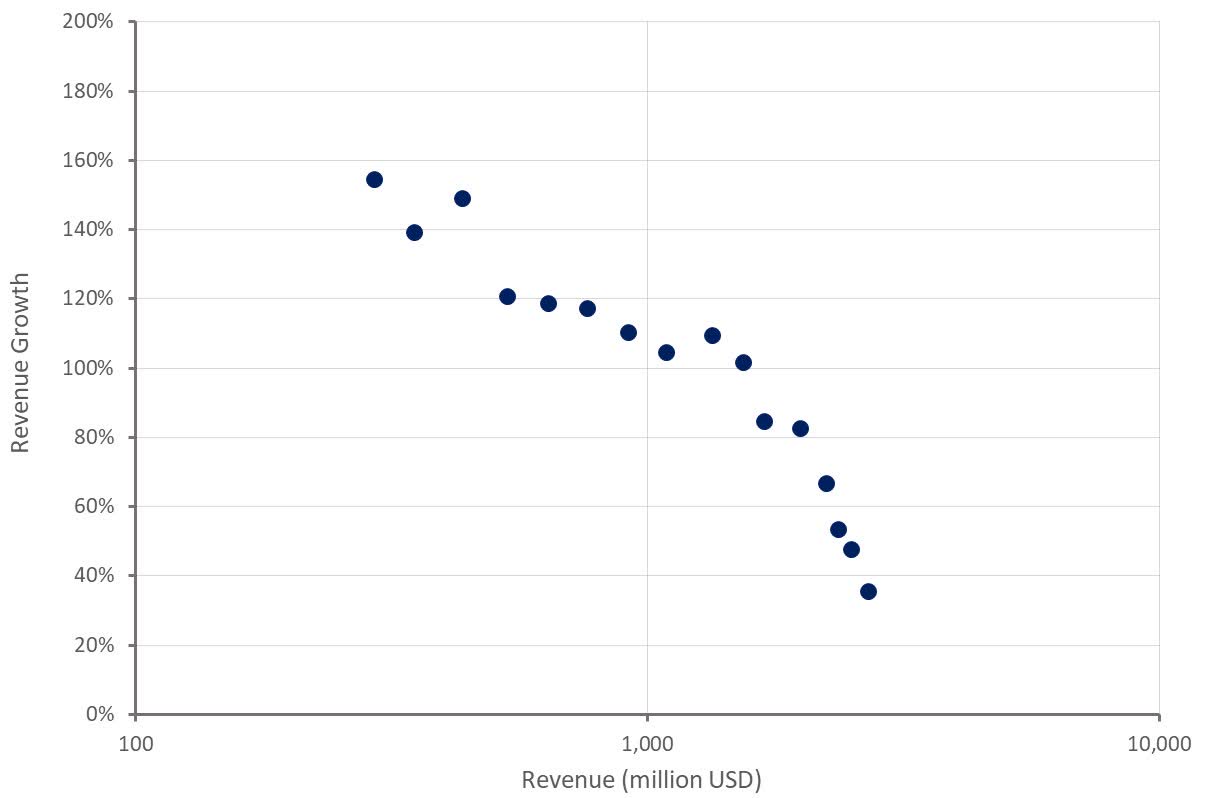

Snowflake's revenue increased roughly 35% YoY in the second quarter, with growth continuing its steady slide lower. Snowflake is guiding to 670-675 million USD in product revenue in the third quarter, representing YoY growth of between 28% and 29%. This forecast assumes that consumption will continue to be a headwind amongst Snowflake's largest customers.

While the company has seen signs of stabilization, there is no evidence of recovery yet, which suggests that growth will remain depressed for some time yet. I estimate that total revenue in the third quarter is likely to come in at around 727 million USD, which would be roughly a 30% YoY increase.

For the full fiscal year, Snowflake expects revenue to grow 34% to approximately 2.6 billion USD. New products (Streamlit, Unistore) should help to support growth in 2024, but it will take time for customers to ramp consumption.

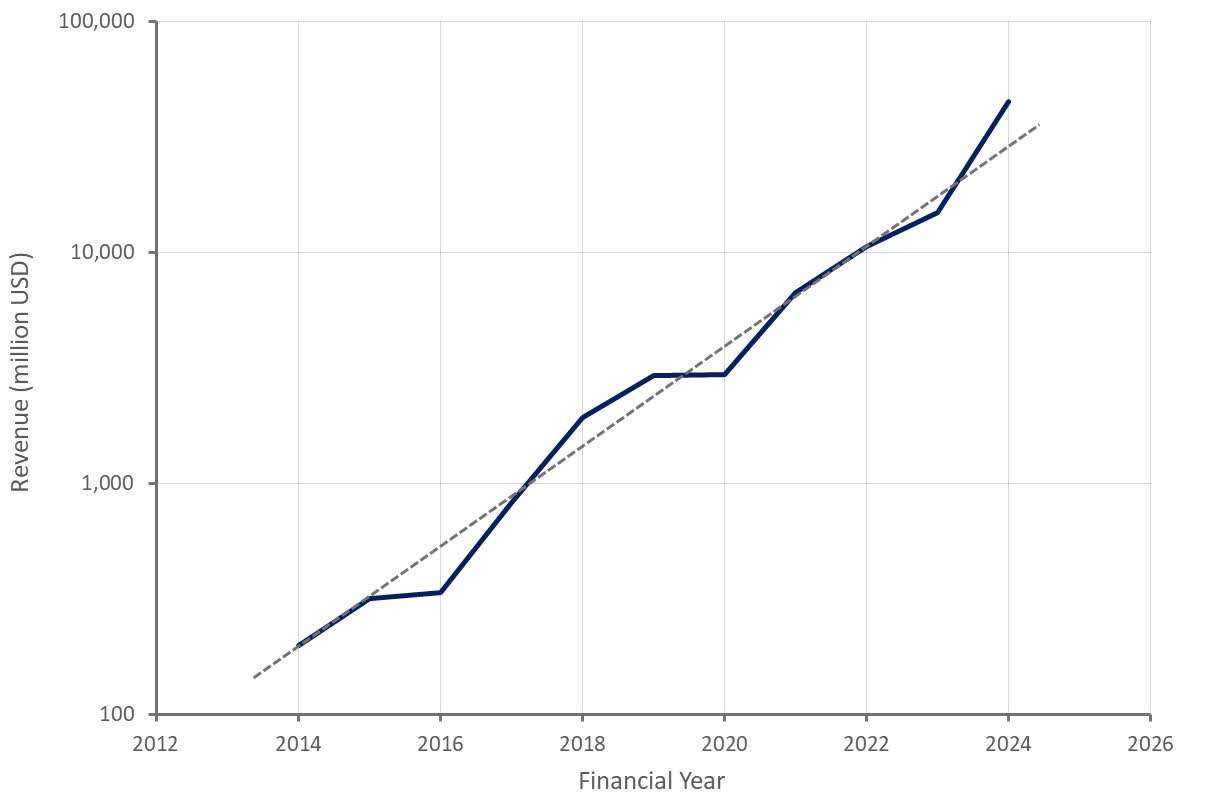

Figure 5: Snowflake Revenue Growth (Source: Created by author using data from Snowflake)

{kind=link}

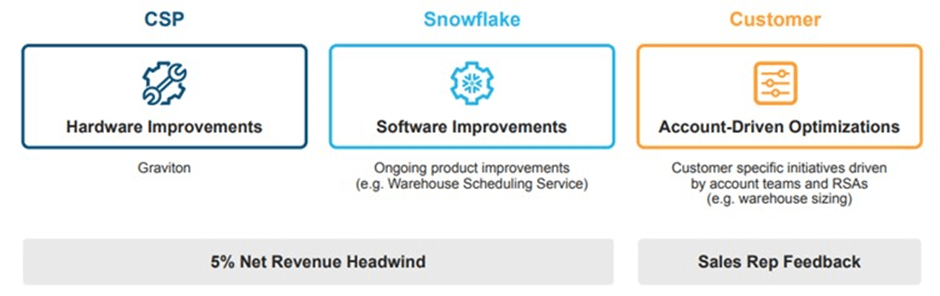

Snowflake's net revenue retention rate was 142% in the second quarter, continuing to fall in the face of consumption headwinds. Snowflake is facing multiple optimization efforts, across hardware, internal software improvements, and customer actions. The most important of these at this stage is likely customer optimization efforts.

Figure 6: Sources of Optimization (Source: Snowflake)

{kind=link}

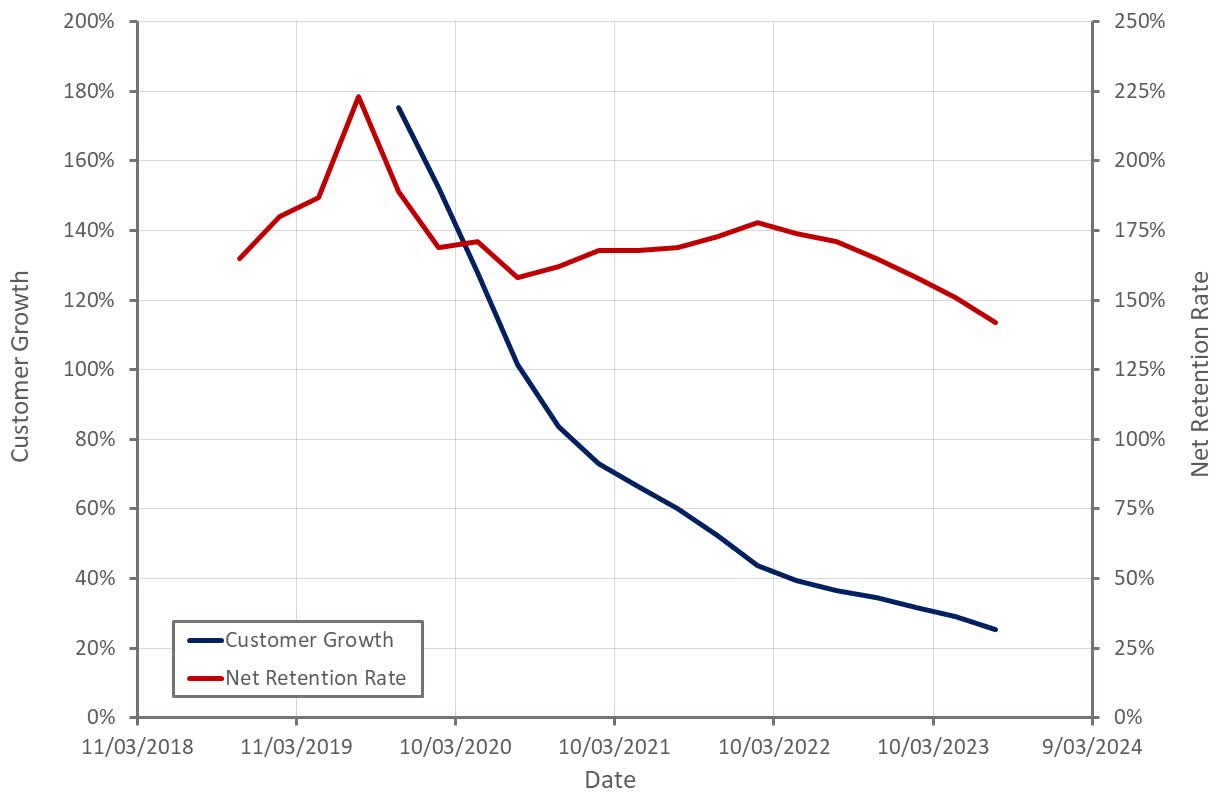

Snowflake has suggested that weakness is being driven by optimization efforts amongst its largest customers. Despite this, there remains an enormous expansion opportunity amongst larger organizations. 639 of the Global 2000 are currently Snowflake customers and they are on average only spending around 1.5 million USD annually. The pace of customer additions also continues to moderate though.

Figure 7: Snowflake Customer Growth (Source: Created by author using data from Snowflake)

{kind=link}

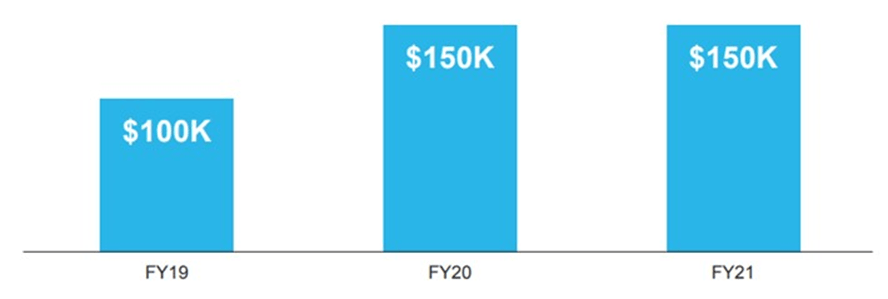

While Snowflake's high net retention rate is one of the factors that has attracted investors to the company, it really needs to be understood in the context of Snowflake's business. Customers generally land small and ramp consumption rapidly. Once this initial ramp is completed, expansion is likely to proceed at a much lower level. With Snowflake's customer base maturing, it is natural that the company's aggregate net retention rate moderates towards a lower level.

Figure 8: Median Initial Capacity Contract Size for Customers Over $1M Product Revenue (Source: Snowflake)

{kind=link}

Snowflake's gross profit margin has been steadily improving as the company scales and now sits at around 68%. The second quarter did see a one-time 4 million USD credit from one of the CSPs though.

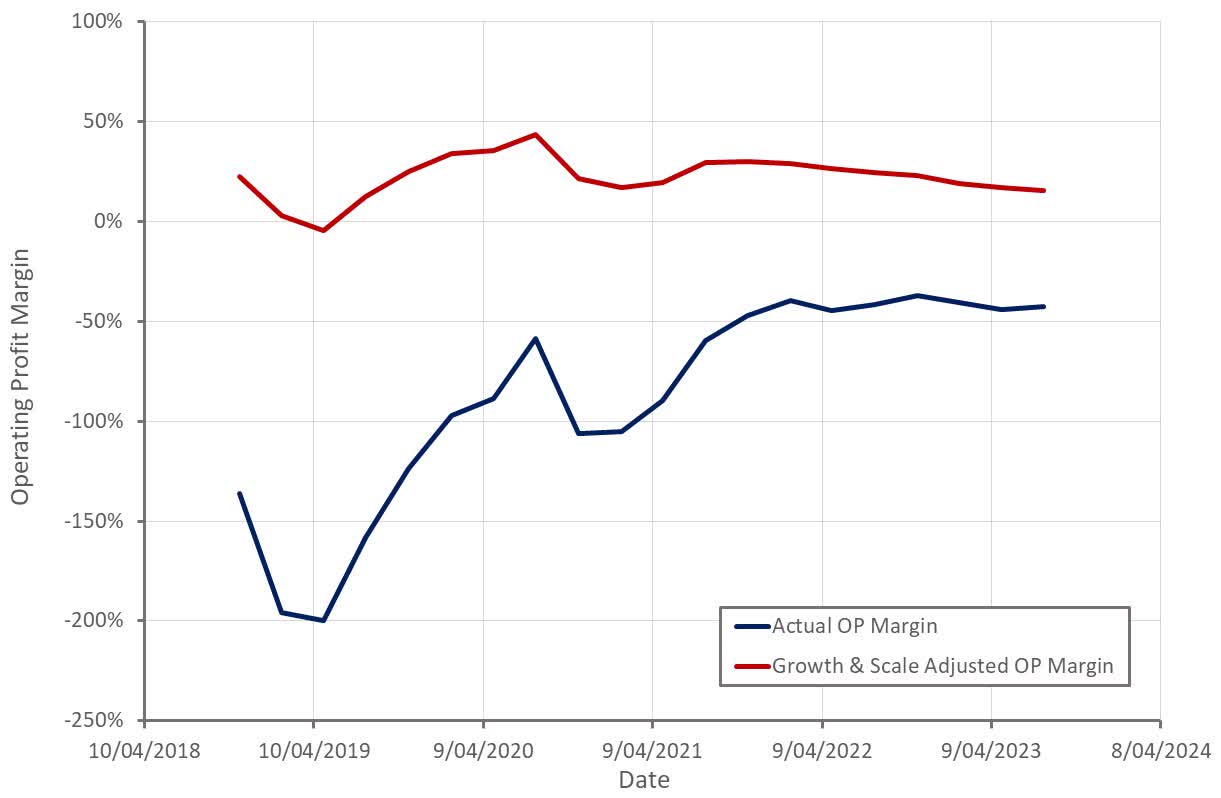

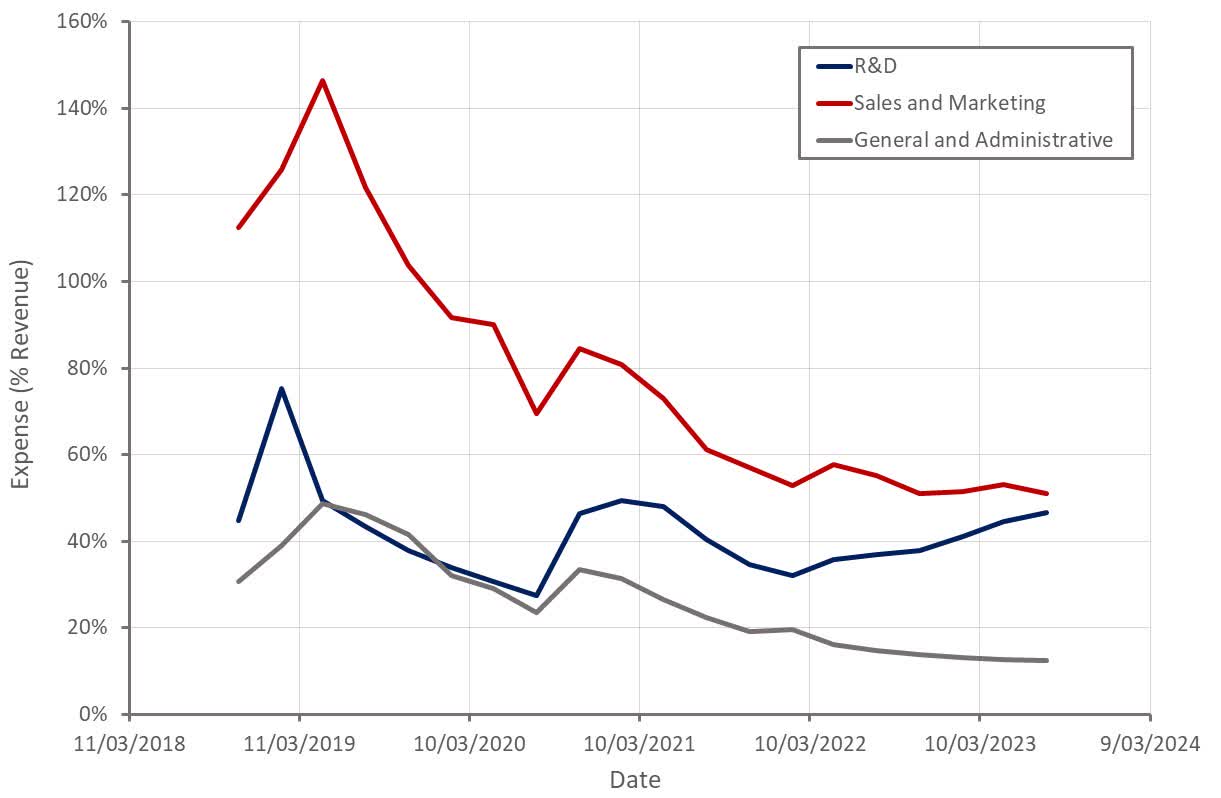

While Snowflake's gross profit margin is improving, the company's operating profit margin has been fairly flat over the past 2 years. This is largely the result of Snowflake increasing its investment in R&D. With important new products beginning to scale in the next 1-2 years, operating profit margins should begin to improve.

Figure 9: Snowflake Operating Profit Margin (Source: Created by author using data from Snowflake) Figure 10: Snowflake Operating Expenses (Source: Created by author using data from Snowflake)

{kind=link}

{kind=link}

Conclusion

I expect Snowflake to modestly beat guidance in the third quarter, but forward guidance may disappoint investors. In addition to the difficult macro environment, it will take time for the impact of optimization efforts to wane and new products to scale.

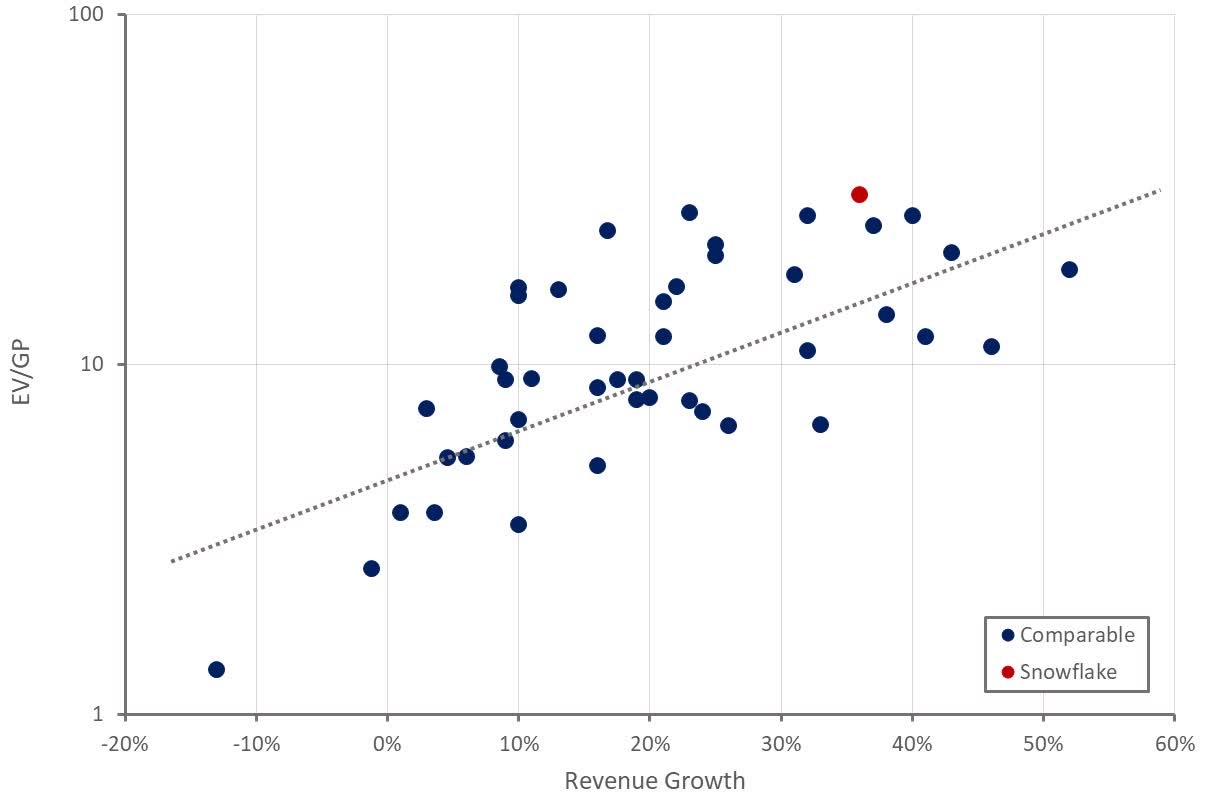

Snowflake's valuation is already high given its growth rate and margin profile, meaning that unless growth begins to stabilize and the company's outlook improves, the upside may be limited.

Figure 11: Snowflake Relative Valuation (Source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Snowflake: Despite Easing Headwinds, Recovery Will Take Time