MSFT - Snowflake: Getting Closer To A Profit

Summary

- A large position has been taken in Snowflake at Joel Greenblatt's Gotham Asset Management.

- Snowflake has also been held at Berkshire Hathaway since its IPO.

- This article will explore the value proposition these prolific value investors might be seeing in Snowflake.

Big new buy at Gotham

{kind=link}

A brand new entrant to Gotham Asset Management's mrq 13F filing is Snowflake (NYSE: SNOW ). For those unfamiliar, Gotham Asset Management is Joel Greenblatt's fund, the investor who is famed for 50% yoy returns in his first fund, his series of value investment books, and his Magic Formula screener. Snowflake has always been a bit of a mystery to me. Growing its client base at a fast clip but still highly unprofitable on a GAAP and Non-GAAP basis, I always wondered what Buffett and Berkshire ( BRK.B ) ( BRK.A ) saw in this IPO (which was the largest ever). It was so uncharacteristic of all the things Warren Buffett and Charlie Munger had preached that I never gave it any thought and simply chalked it up to Todd Combs and Ted Weschler making a wager.

Now that we see Greenblatt making a move after the large drop in share price, that has spiked my interest even more. I am not going to take the typical customer acquisition/future growth possibilities assessment in most articles that analyze unprofitable tech stocks. I want to take a look at the numbers now and see the prospects of digging out of the hole. Snowflake is Greenblatt's largest single stock holding as the top two are the ETF ( SPY ) and his hybrid SPY ETF called ( GSPY ). My thesis is this stock is still a hold. There are no GAAP or Non-GAAP earnings to support this play, but if a couple of investors I respect are holding it, I wouldn't recommend selling it either. They get far more perspective and possibly private presentations that we lack. The top line growth also might be worth waiting on if you believe it's about to turn into profits. It seems like it will soon, and when it does, I'm interested.

Berkshire ownership history

{kind=link}

At a market value of a tad over $1 Billion, Berkshire Hathaway's position is number 26th on their list of holdings just above McKesson ( MCK ). First bought in Q3 2020, the average estimated price paid is $238.1. If the purchase price is accurate, Berkshire is down close to 40% on their initial investment. Gotham's purchase price is estimated at $169, down 15.3% from its purchase price. So a couple of value whales are in it for far more than you could get it for in the market right now, how does it look from a value perspective?

Story up until now

{kind=link}

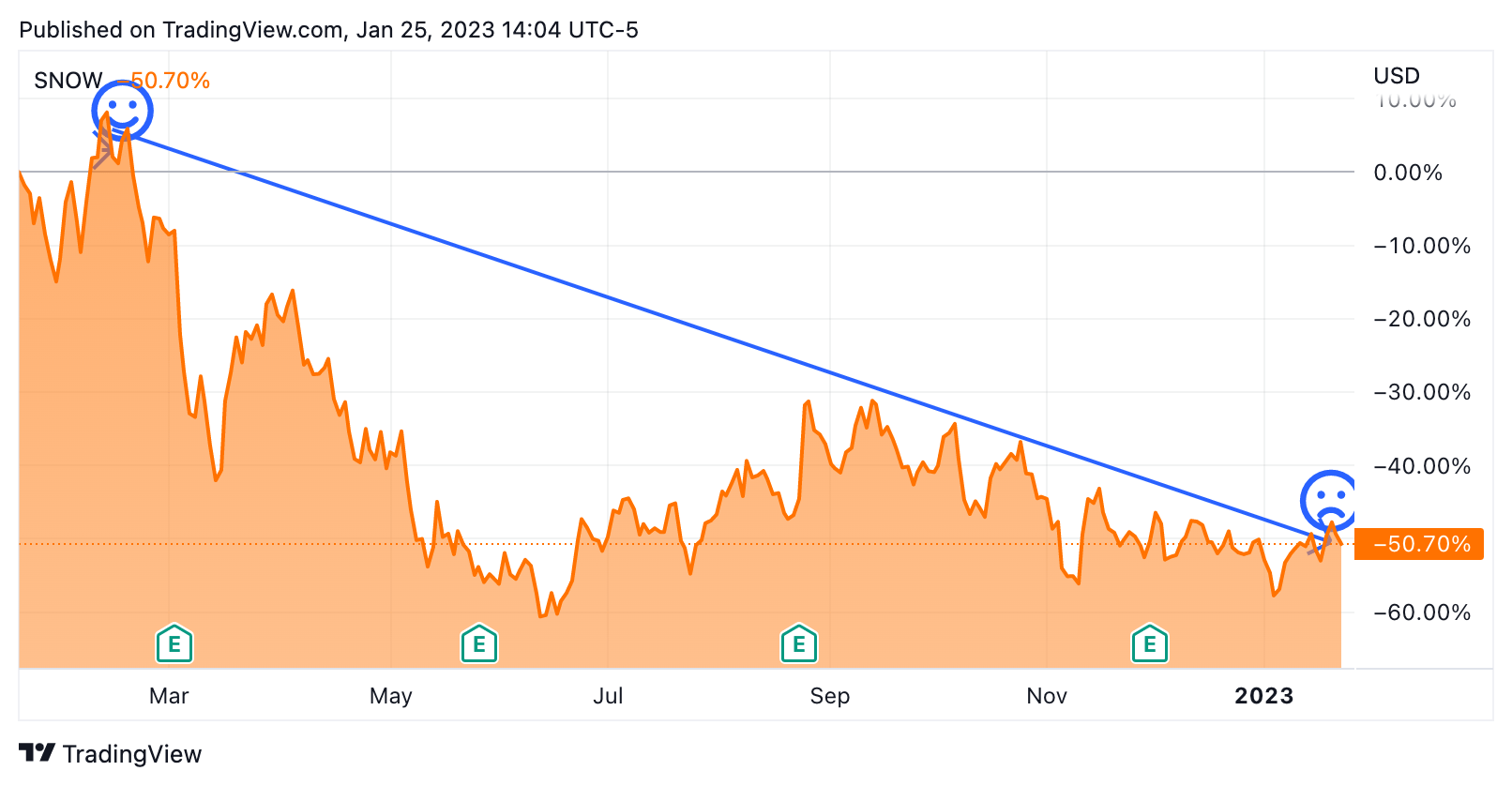

I'm not much of a chartist, but I can draw a line. The one-year chart for Snowflake is straight down by 50%. Even though the emoji at the bottom is sad, these charts oftentimes make me happy. If the price is right, bottom-fishing a chart adds some resistance by virtue of psychological reinforcement in the investor that the stock can't go down any further. While I know that the latter statement in the prior sentence is often not true, it does give me some added confidence when placing bets. If a stock has amazing heuristics and a parabolic chart, I can still feel a bit nervous on the flip side of this argument.

What they do

From the 2022 10K, here is a summary of what Snowflake does:

Our platform is the innovative technology that powers the Data Cloud, enabling customers to consolidate data into a single source of truth to drive meaningful business insights, build data-driven applications, and share data. We provide our platform through a customer-centric, consumption-based business model, only charging customers for the resources they use.

Snowflake solves the decades-old problem of data silos and data governance. Leveraging the elasticity and performance of the public cloud, our platform enables customers to unify and query data to support a wide variety of use cases. It also provides frictionless and governed data access so users can securely share data inside and outside of their organizations, generally without copying or moving the underlying data. As a result, customers can blend existing data with new data for broader context, augment data science efforts, and create new monetization streams. Delivered as a service, our platform requires near-zero maintenance, enabling customers to focus on deriving value from their data rather than managing infrastructure.

Whew, that description was a mouthful. Turning to my Morningstar analyst reports helped nail down some succinct descriptions of what makes them special. It seems to be their "stickiness" and large 3000+ customer roster that includes 30% of the Fortune 500. Data Lakes are a new terminology frequently associated with Snowflake, bucking the trend of data warehouses. The difference is mainly being able to access data with more flexibility and using raw data combined with AI to create easily queried insights. Morningstar Analyst Julie Bhusal Sharma is bullish on the name due to the items summarized above.

The main takeaway for the layman that I got from the report is that Snowflake's platform makes it easy for customers to migrate data from other platforms into their cloud-based platform. This ease of migration plus faster data accessibility leads to more customers. Migrating any data from a warehouse in a silo to a new server can be next to impossible after you code the servers to perform different functions. In a simple startup I was involved in, we had 4 small, cheap servers. All the servers were coded in different languages to perform different functions within the software. If we chose to move this data, I can only imagine the migration would require some re-coding and or rebuilding of the app after migration. Not only that, but the pre-beta software data took forever to load. What would happen to a massive web app trying to move things around is beyond my comprehension.

The Software as a service model can run its cloud computing across Azure, AWS, and Google cloud. The one item I didn't like about Snowflake in Morningstar's report is that it used Google ( GOOG ) ( GOOGL ), Microsoft ( MSFT ), and Amazon ( AMZN ) as comps in the report. Snowflake seems to be more of a cloud computing enhancement offered through data center companies as a medium. Thus they are both a customer and competitor of these behemoths, which is very difficult competition to deal with.

Balance sheet

{kind=link}

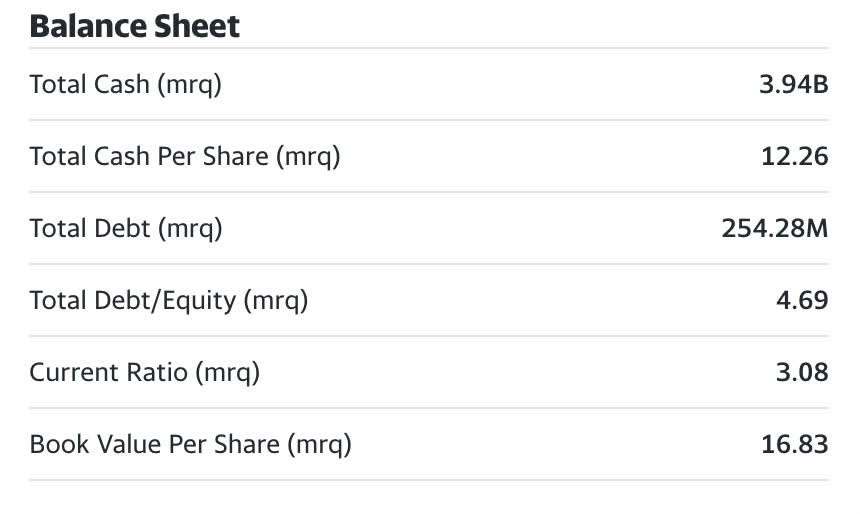

Both total current assets and current debt are trending upwards. The amount of debt is small however, thus we would assume that some of the additions to current assets are derived from share dilution. Shares outstanding have increased from 305 million to 321 million shares outstanding. As an unprofitable business, these are the main sources of capital for the time being. Below is a snapshot summary of the balance sheet.

{kind=link}

Typical for early-stage tech and IT companies, Snowflake has a very liquid balance sheet. Almost $4 billion in cash and a debt-to-equity ratio of only 4.69%. The balance sheet thus far is the most appealing thing about Snowflake to me. This is as close to zero debt as you will get. Very healthy indeed.

Income statement trends

{kind=link}

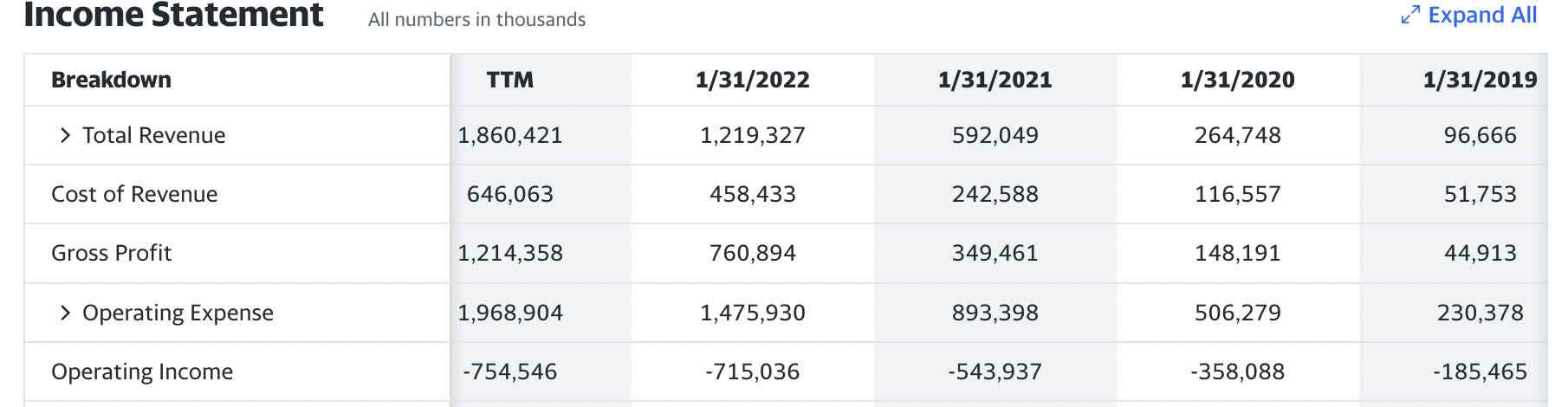

Here's where the obvious play in Snowflake is, in the top line. From 2019 to 2022, revenue has grown from $96.6 million to $1.2 Billion. A staggering 88.77% CAGR in revenue over that period. TTM is at $1.86 Billion, meaning that the numbers continue their trend as they spend to grow. The cost of revenue has a CAGR of 72%. Therefore their revenue growth is trending well ahead of their cost of revenue growth. Snowflake is truly a shot out of a cannon that nobody saw coming.

In 2019, revenue as a percentage of operating expenses was 41%. In 2022 that number is 82%. Revenue as a percentage of expense has nearly doubled and Snowflake is now at only an 18% differential in breaking even between revenue and opex. This is one of the better top-line growth stories I've seen.

Valuation

{kind=link}

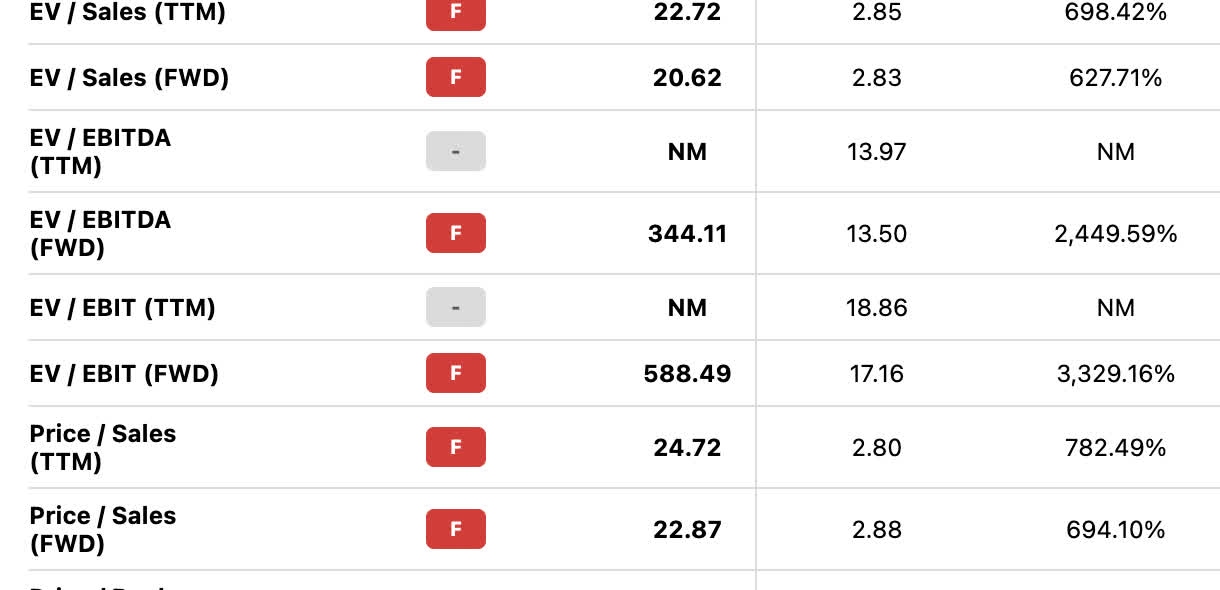

I like to dream about the future, but fortunately being a numbers guy, my rationality brings me back down to earth. Looking at Snowflake Non-GAAP and price-to-sales numbers on the left compared to the industry comps on the right, the premium for Snowflake is staggering. Even after being cut in half.

Pricing a company purely on price-to-sales is more of a momentum strategy for funds looking to turn over their portfolios within a year, riding the news cycle. However, as demonstrated above on the income statement, even though losses increase due to increased expenses, the revenue percentage to expenses might show positive earnings in the not-too-distant future.

Catalysts

{kind=link}

Above is a compilation of analyst estimates on a GAAP eps basis for 2023 and 2024. The majority are predicting profitability versus losses in the not-too-distant future. While I've seen these wrong too many times to count, my analysis of the income statement shows that the possibility is certainly on the horizon. Uber ( UBER ) is an example of a company that I had been waiting to turn a profit for the longest time but never happened. Peter Lynch recommends waiting until a company turns a profit and I adhere to that rule. If they do, there will still be enough upside left for all of us. Turning a positive GAAP or Non-GAAP bottom line is my number one catalyst.

Risks

Most analyst reports show the biggest risk is over saturation and the lack of a moat that any data center or cloud computing company has. While Snowflake has been lauded for over 100% customer retention rate ( I guess meaning they upsell existing customers at each renewal), I have to imagine the next big data company is out there lurking or already exists and is just tweaking the product. Snowflake seems to have the secret sauce at the moment looking at their top-line growth. However, if that slows or reverts, they may fall into the data lake abyss.

Conclusion

After getting up to snuff on analyst reports and reviewing how they are pricing this stock, I think it is still being priced on a price-to-sales basis. Not only is it being priced on a price-to-sales basis, but also forward 2024/25 numbers. For me to even consider a pre-profitable stock a buy on a price-to-sales basis, it needs to be a single-digit multiple. However, I do realize the top line is growing at breakneck speed with improving margins. Once it turns profitable, Snowflake will be on my watch list as a possible buy after turning a profit. For now, it's a hold, but I certainly am starting to see what Berkshire and Greenblatt's team have been looking at all along.

For further details see:

Snowflake: Getting Closer To A Profit