SNOW - Snowflake: Great Product But Execution Raises Questions

2023-12-05 07:29:13 ET

Summary

- Snowflake offers a great product for the age of data and AI, solidifying its presence and relevance in the industry.

- Positive business indicators include a robust 135% net revenue retention rate and outpacing major competitors in revenue growth in the latest quarter.

- However, Snowflake grapples with substantial stock-based compensation leading to share dilution despite considerable buyback efforts.

- Escalating expenses in sales, marketing, and R&D raise doubts about sustained revenue growth amidst increased competition.

- SNOW's exceedingly high valuation metrics are challenging to justify, indicating potential risks at current price levels.

In the data and AI landscape, Snowflake ( SNOW ) stands out with its promising platform, expected to attract substantial demand in the near future. Yet, the recent FQ3 2024 report sparks significant financial concerns. Questions arise about Snowflake's future growth sustainability due to mounting expenses, challenges from substantial share dilution, and whether its exceptionally high valuation makes sense. With these uncertainties in mind, it's challenging to justify SNOW as a buy at the moment.

The good: solid platform, strong revenue expansion, and robust balance sheet

First off, let's take a moment to acknowledge certain positive aspects of Snowflake's business.

Snowflake offers a great product for the age of data and AI

Snowflake has emerged as a pivotal player in the era of data and AI, offering a transformative platform that caters to the burgeoning needs of businesses reliant on these technologies. With a commendable market share of 19.59% in the competitive landscape of data warehousing, Snowflake has not only solidified its presence but also signifies its relevance in this domain. Based on my seven-year experience in data analytics, Snowflake is commonly regarded as a superior data platform, frequently preferred by companies aiming to establish a robust data infrastructure, particularly among early-stage startups.

Snowflake's competitive edge lies in its holistic approach to data management, surpassing many counterparts like Google ( GOOG ) Cloud or Microsoft ( MSFT ) Cloud. Unlike these competitors, Snowflake offers an all-encompassing platform that seamlessly integrates a data warehouse, database, data lake, and an array of additional services tailored for AI and reporting. By consolidating these critical elements into a cohesive ecosystem, Snowflake minimizes the complexities associated with navigating multiple platforms, offering companies a singular, robust solution that streamlines data management and empowers efficient decision-making processes.

What also sets Snowflake apart is its astute understanding that AI's efficacy heavily hinges on robust and accessible data.

From the recent earnings call :

We said it many times, there's no AI strategy without a data strategy. The intelligence we're all aiming for results in the data, hence the quality of that underpinning is critical. Meanwhile, Snowflake has announced and showcased the plethora of new technologies that let customers mobilize AI.

For example, Snowflake Cortex , a pioneering addition to Snowflake's offerings, taps into AI and machine learning directly within its platform. The service bridges data and AI by handling complex language models, seamlessly integrating AI capabilities within Snowflake. This deep connection between data storage and AI strength increases Snowflake's appeal for businesses seeking advanced AI solutions, showing its dedication to leading in tech innovation amid the growing importance of data in AI development.

Retention rates are solid, sales growth is still higher than competition

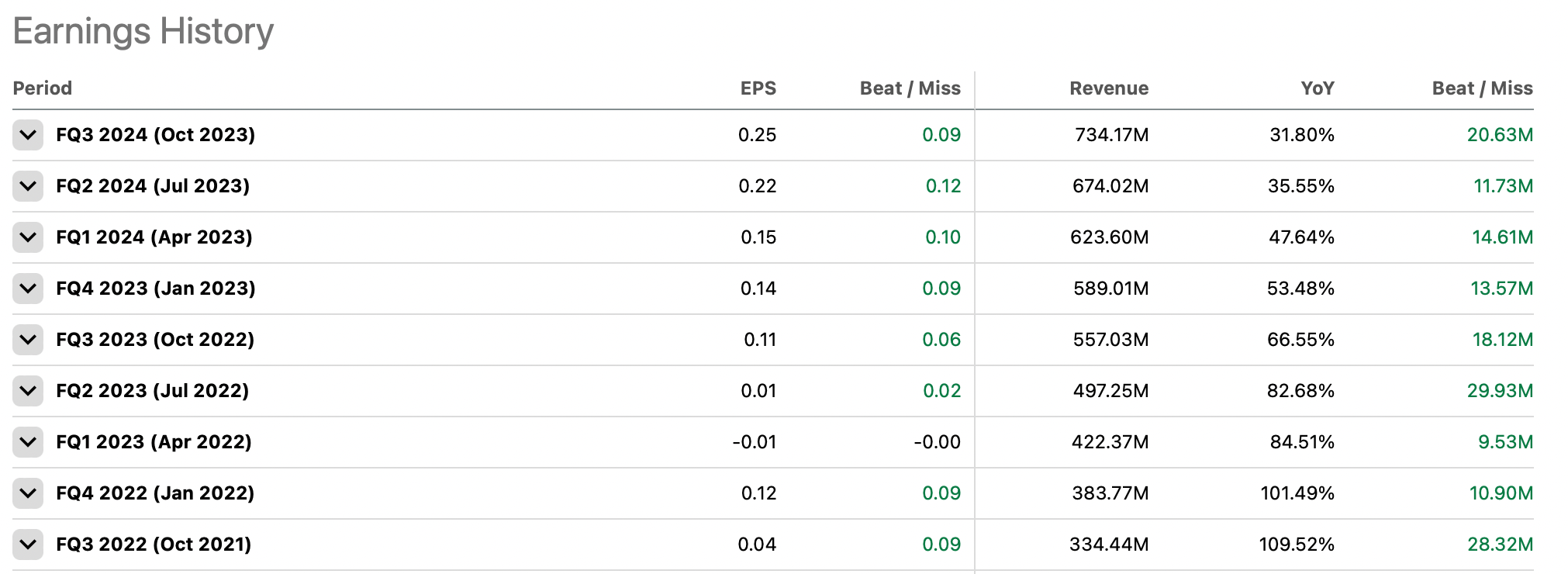

Another encouraging indicator is Snowflake's expansion rates. In FQ3 2024, (ending October 2023) Snowflake achieved a net revenue retention rate of 135%, which means the company can significantly increase its sales numbers without the need to onboard new customers. However, it's important to note that Snowflake employs a distinct method to calculate this metric, which might differ from the approach used by other software companies.

We expect our net revenue retention rate to decrease over the long- term as customers that have consumed our platform for an extended period of time become a larger portion of both our overall customer base and our product revenue that we use to calculate net revenue retention rate, and as their consumption growth primarily relates to existing use cases rather than new use cases.

Strong expansion rates have enabled Snowflake to substantially increase its revenue over time, outpacing competitors in the latest quarter. For instance, while Google Cloud, Microsoft Azure, or Amazon's ( AMZN ) AWS reported growth rates of 23%, 28%, and 12% respectively in Cloud revenue in Q3 2023, Snowflake's growth surpassed these figures.

The company maintains a relatively safe balance sheet with no long-term debt

Finally, Snowflake does maintain a solid balance sheet, which reduces the risks associated with investing in the stock. With $3.55 billion in cash and short-term investments and no long-term debt, financial risks are somewhat limited. The solid financial foundation might strengthen Snowflake against market changes and position it advantageously for strategic growth endeavors, such as AI development.

The bad: financial analysis raises questions

Despite the mentioned positive aspects, there are various negative signals from the FQ3 2024 report that prevent us from recommending SNOW as a buy. These indicators also raise concerns about the sustainability of Snowflake's growth trajectory.

Share-based compensation leads to extreme dilution despite share buybacks

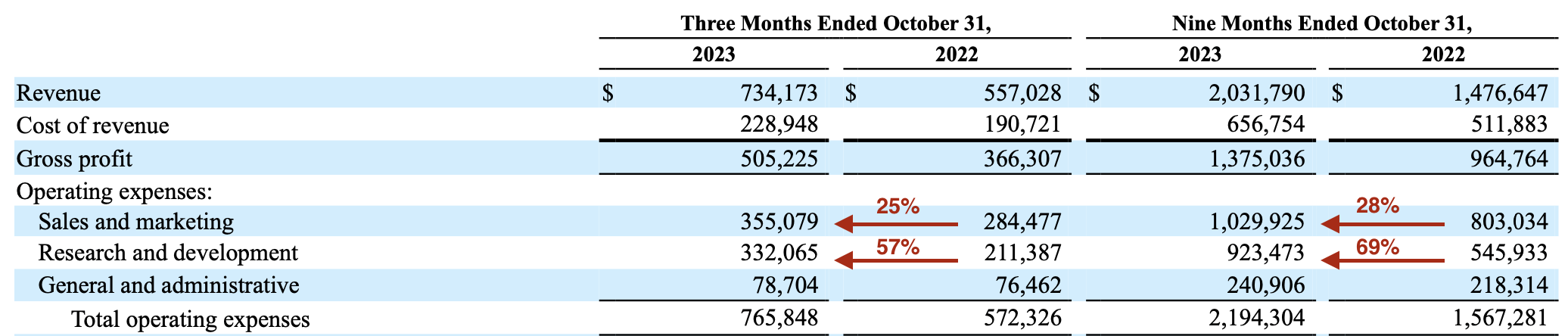

Firstly, Snowflake faces a substantial stock-based compensation (SBC) expense issue, impacting its financial standing. In FQ3 2024, the company allocated $298 million to SBC, a considerable amount compared to its $734 million revenue and a 30% increase from the previous year's quarter. Despite investing $591 million in stock repurchases this year to counter share dilution, the number of outstanding shares still rose from 320,135 in FQ3 2023 to 329,310 in FQ3 2024.

While this strategy helps Snowflake show positive cash flows on paper, (SBC is a non-cash expense) stakeholders might grapple with the real and substantial impact of significant dilution caused by this practice. If Snowflake doesn't address the SBC concern, it faces a challenging choice: either spend extensively on buybacks, depleting its cash reserves and heightening risks, or endure substantial dilution, putting strong pressure on the stock price.

Growth seems to be fuelled by extreme marketing spend, R&D expense explodes

Then goes Snowflake's expense structure. While the company's revenue does grow significantly, so do its sales and marketing and R&D expenses. For instance, in the latest quarter, sales and marketing expenses increased by 25% year-over-year, while R&D spend went up by enormous 57%. Some of these expenses are linked to the earlier mentioned SBC costs, but they don't entirely account for the substantial increase.

{kind=link}

Snowflake's high spending on sales and marketing raises doubts about the sustainability of its revenue growth, hinting at potential artificial inflation. Similarly, the company's substantial and rapidly growing research and development expenses pose questions about Snowflake's ability to manage these costs, especially in the face of increasing competition. For comparison, Google's Cloud business generates a positive operating income while having sales approximately ten times higher.

Revenue growth is slowing down, while competition intensifies

Furthermore, although Snowflake outpaces its competition in revenue growth, there's a noticeable decline in its growth rate over time. As the market emphasizes cloud solutions and larger competitors like Microsoft, Google, and Amazon intensify their presence, the question arises whether Snowflake can regain the remarkable expansion rates it saw in the post-pandemic period.

{kind=link}

SNOW's extreme valuation is difficult to justify

Finally, when considering valuation, it becomes challenging to rationalize the exceedingly high valuation metrics attributed to SNOW.

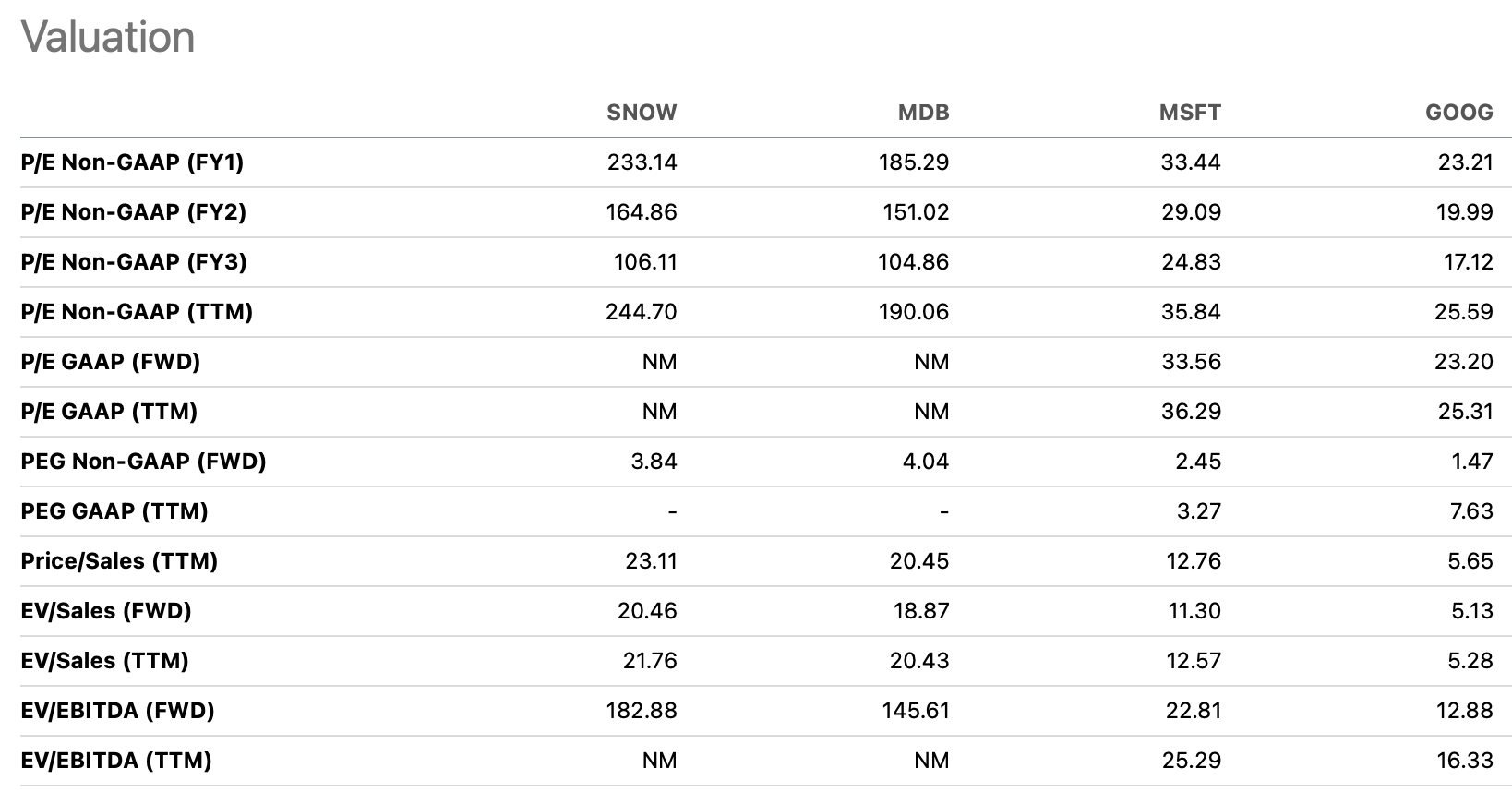

With an EV/SALES ratio around 22 and a forward EV/EBITDA reaching 183, coupled with a P/S ratio of 23, Snowflake's valuation reaches an unparalleled level among its competitors and within the technology sector. The non-GAAP P/E ratio reaching a sky-high 233 appears unjustifiable, even in light of its 40% earnings growth. Even more concerning is the PEG ratio, ideally resting between 1-2 for healthy valuation, sitting at nearly 4.

Looking ahead, the forecasted 3-year forward P/E ratio of 106 implies a prolonged period before the company might reach a more rational valuation. Such lofty figures suggest that SNOW faces an extended journey before achieving a balanced valuation, highlighting the extraordinarily high risks accompanying its current price levels.

{kind=link}

Key takeaways

In summary, Snowflake excels in the data and AI landscape, offering a robust platform integrating diverse data management services, establishing itself as one of the leader in the data warehouse and cloud spaces. Undoubtedly, in the AI era, Snowflake's product is poised for substantial demand in the near future. Positive business indicators include a robust net revenue retention rate of 135%, strong revenue growth surpassing major players like Google Cloud, Microsoft Azure, and Amazon AWS, and a sound balance sheet.

However, amid these strengths, numerous concerning signals are brought to light by the FQ3 2024 report. Snowflake faces a significant stock-based compensation issue, resulting in notable share dilution despite attempts at stock buybacks. Escalating expenses in sales and marketing, coupled with substantial growth in R&D spending, raise doubts about sustained revenue growth amid intensifying competition. The company's decelerating revenue growth rate and its extreme valuation metrics point to impending challenges in justifying its valuation and achieving a more balanced financial standing.

As a result, it is challenging to recommend SNOW stock as a buy until the aforementioned concerns are resolved.

For further details see:

Snowflake: Great Product, But Execution Raises Questions