SNOW - Snowflake: I Expect The Stock To Be A Winner In 2024

2024-01-10 04:56:38 ET

Summary

- The company is well-positioned in the cloud data warehousing market and has the potential for strong growth through at least 2028.

- I am bullish on the macro backdrop as Snowflake is poised to benefit from expanding IT budgets and improving CIO sentiment on falling interest rates.

- I calculate that SNOW shares may still offer about 24% upside to fundamentals.

Snowflake (SNOW) stock is poised to be a commercial winner in 2024: My bullish assessment is based on the company's strong product release roadmap, which will help drive >30% YoY topline growth in FY24 and FY25. In that context, it's promising to see SNOW's notable product advancements in AI and the company's broader ambition to democratize AI within enterprises through the cloud data warehousing value proposition. Moreover, I am bullish on the macro backdrop as Snowflake is poised to benefit from expanding IT budgets and improving CIO sentiment on falling interest rates. Valuation is my only concern relating to a SNOW investment, with shares trading at 21x EV/Sales ((FWD)). However, considering a long-dated residual earnings valuation framework, I calculate that Snowflake shares may still offer about 24% upside to fundamentals. I assign a Buy recommendation.

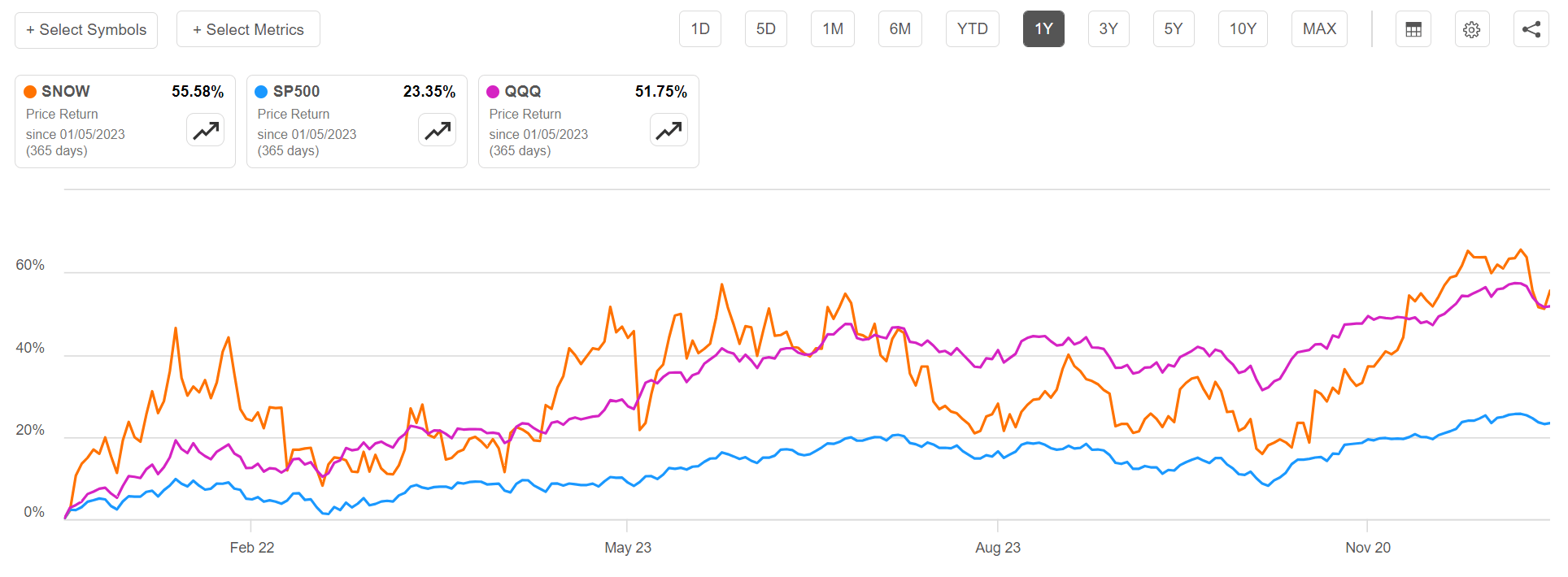

For context, Snowflake stock has outperformed the broad U.S. equities market in 2023, also when compared to the "Tech" benchmark. For the trailing twelve months, SNOW shares are up about almost 56%, compared to a gain of approximately 23% for the S&P 500 (SP500) and a gain of close to 52% for the Nasdaq tech-heavy Nasdaq 100 ( QQQ ).

{kind=link}

Snowflake Is Well-Positioned In A Structural Growth Market

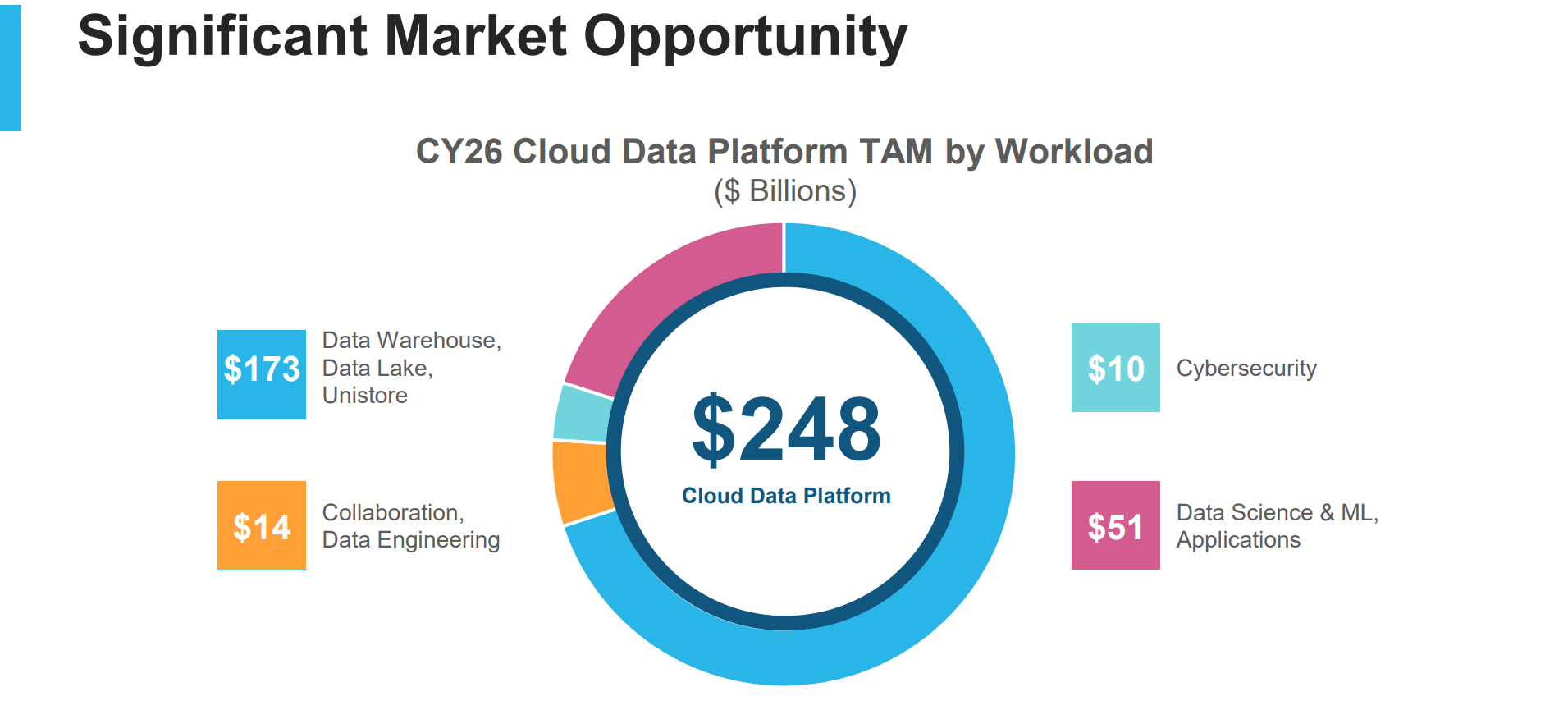

Snowflake stands as an early frontrunner in the cloud data warehousing realm, with promising potential for strong growth through at least 2028 (I estimate 25-30% CAGR over the next 5 years). On that note, I am especially bullish on Snowflake's broad presence with enterprises and the possibility of scaling in-logo penetration with an expanding product range to accommodate cloud workloads. Notably, as of Q3 2023 Snowflake serves more than 436 customers generating more than $1 million in sales each, and claims a 135% net retention rate. In 2022, Snowflake management projected that the company's TAM may potentially be as high as $248 billion.

{kind=link}

With businesses directing more investments towards AI leveraging their Cloud data reservoirs and the Cloud Data Platform market is poised to see a demand acceleration in 2024, and beyond. In that context, the synergy between Snowflake's strategic positioning in accommodating evolving market needs and the increasing demand for AI-driven solutions underscores my optimism for Snowflake's high growth prospects. Lastly, I project ample opportunities for operating leverage as Snowflake's commercial backdrop scales.

Product Release Outlook To Drive Growth Acceleration...

Snowflake is poised to capture new workloads through the introduction of several new products set to launch in Q4 and throughout FY'25, addressing emerging and previously unexplored customer needs. In the most recent December quarter, Snowflake introduced Snowflake Cortex, a fully managed service designed for hosting and serving AI models, LLMs, and vector functions. Additionally, they launched the Snowflake Native App Framework, which is an improved developer environment facilitating the creation, distribution, monetization, and deployment of data apps. Another highlight that has been introduced in 2023 is the Snowflake Container Services, offering fully managed containers within Snowflake without requiring data movement. They also presented Streamlit in Snowflake, an open-source app framework streamlining the process of building and sharing data apps. Lastly, Snowflake's recent data streaming offering Dynamic Tables is expected to launch in early 2024.

...On A Supportive 2024 Macro Backdrop

Snowflake's growth push coming from new products is further aided by a strengthening macro tailwind. Specifically, I am bullish on the macro backdrop as Snowflake is poised to benefit from expanding IT budgets and improving CIO sentiment on falling interest rates. Moreover, as enterprises are preparing to leverage data through GenAI, there is an expected increase in enterprises transitioning from legacy Data Warehouses to Snowflake's platform. On a related note, Snowflake's Snowpark is expected to show significant revenue growth, as enterprises show an increasing demand for handling unstructured data.

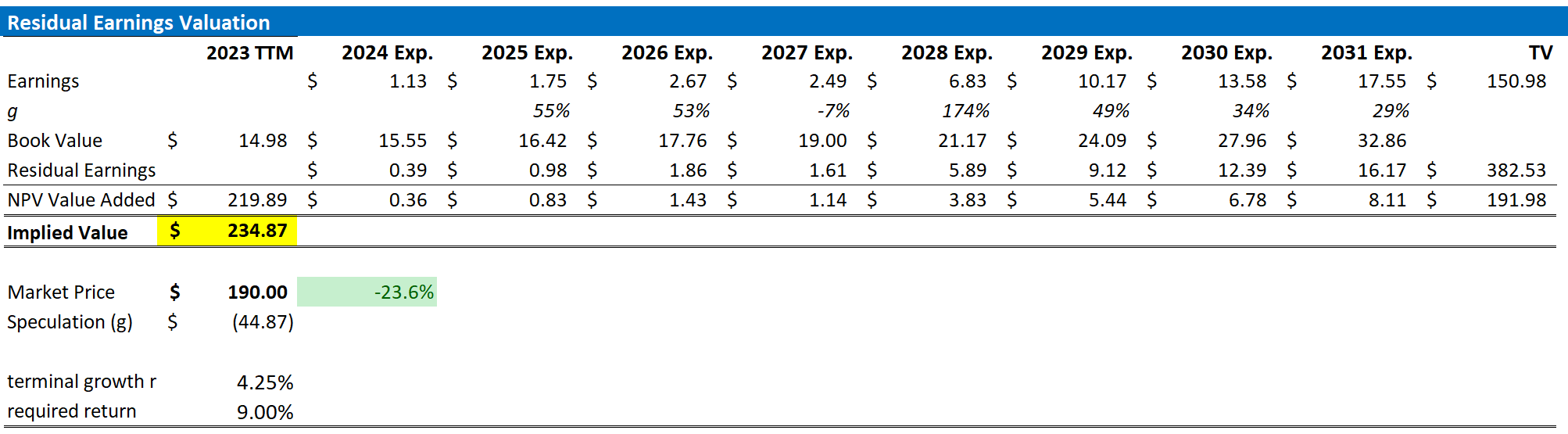

Valuation: Set Target Price At $235/Share

Admittedly, valuing a growth asset like Snowflake is difficult. Thus, I advise readers to approach my residual income model with some healthy skepticism. My model anchors on the idea that a valuation should equal a business' discounted future earnings after capital charge. As per the CFA Institute :

Conceptually, residual income is net income less a charge (deduction) for common shareholders' opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company's capital.

With regard to my SNOW stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on Seeking Alpha.

- To estimate the capital charge, I anchor on SNOW's cost of equity at 9%.

- For the terminal growth rate after 2025, I apply 4.25%, which is about 150-175 basis points above the estimated nominal global GDP growth. The growth premium should reflect the structural expansion outlook of the cloud data warehousing market, with a tailwind coming from AI.

Given these assumptions, I calculate a base-case target price for COIN stock of about $235/share.

Seeking Alpha; Company Financials; Author's Calculations

{kind=link}

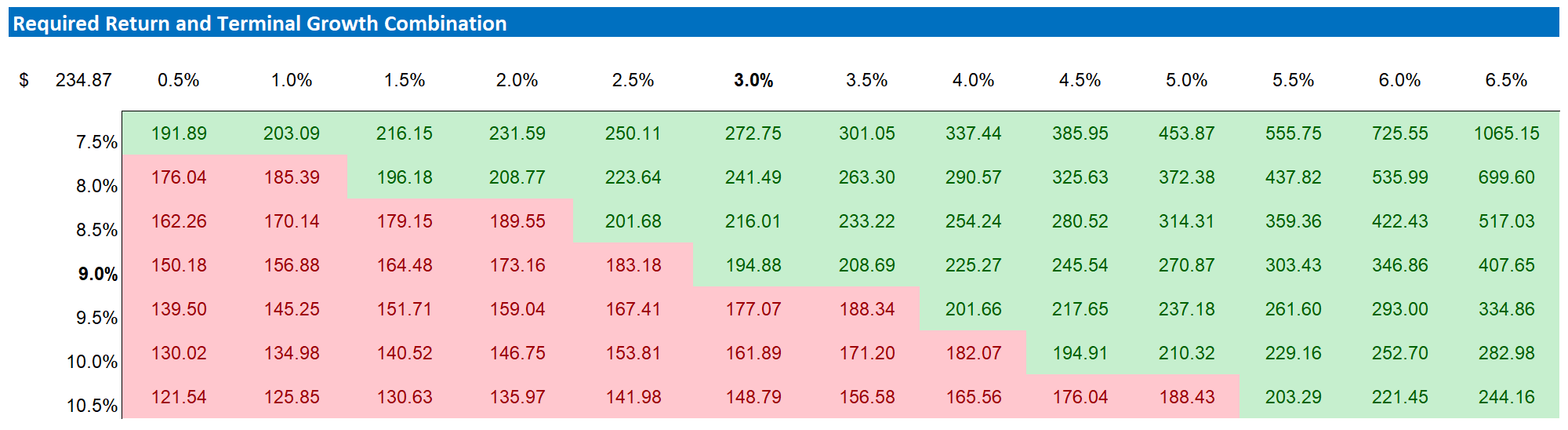

As I argued that my estimates for growth and equity charges may be conservative, I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I've included a sensitivity table to test different scenarios and assumptions. See below.

Seeking Alpha; Company Financials; Author's Calculations

{kind=link}

A Note On Risks

As a high-growth asset in a relatively young market, Snowflake's market outlook is promising, yet largely un-quantified and clouded. Investors should consider that this uncertainty drives risks. In addition, the landscape of the Data warehouse market is competitive, with various competitors, including hyperscale players, playing in the market. If Snowflake's offerings do not demonstrate sufficient competitiveness, or lose competitiveness over time, the company's long-term growth prospects might not align with the current optimistic projections. Lastly, Snowflake is a long-duration investment, meaning that SNOW valuation is sensitive to discount rates. In the event of a "higher for longer rates scenario" (e.g., fed funds rate >4% for multiple years), the share price would certainly be under pressure, even though the commercial outlook for Snowflake remains broadly unchanged.

Investor Takeaway

Snowflake is well-positioned in the cloud data warehousing market and has the potential for strong growth through at least 2028. In that context, the company is expected to experience strong growth in 2024 due to its product release roadmap and advancements in AI. Moreover, I am bullish on the macro backdrop as Snowflake is poised to benefit from expanding IT budgets and improving CIO sentiment on falling interest rates. Even though shares are trading at 21 times EV/Sales ((FWD)), assessing shares through a long-term residual earnings valuation method, I've found that Snowflake shares might still have around a 24% potential increase based on fundamentals. I recommend a Buy.

For further details see:

Snowflake: I Expect The Stock To Be A Winner In 2024