SNOW - Snowflake Q2 Earnings Preview - Watch For Spend Optimization

2023-08-22 16:00:47 ET

Summary

- Snowflake openly addresses challenges primarily due to cost pressures, emphasizing adaptability and resilience.

- Snowflake's guidance for the second quarter shows ambitious growth, despite challenges, reflecting confidence in its solutions.

- Snowflake remains the dominant leader in cloud-based data warehousing, while Databricks carves out a niche in AI workloads.

- Before Q2 earnings, SNOW stock is a Hold and spend optimization will be the key to watch for.

Snowflake, a trailblazer in the cloud data platform industry, has openly addressed the challenges it recently encountered. With unparalleled candor, the company has attributed these hurdles primarily to escalated cost pressures. However, rather than casting blame, Snowflake has embraced this situation as an opportunity to emphasize its adaptability and resilience.

The crux of the issue lies in the prudent approach of Snowflake's mature customers. These industry leaders, driven by financial prudence, have embarked on a journey of optimization and moderation when it comes to their Snowflake expenditures. It's a testament to Snowflake's commitment to customer satisfaction that even amid these circumstances, the performance of its younger customer base has managed to outshine expectations.

It's worth noting that Snowflake is navigating these waters with a firm hand on the rudder of cost control. One particularly telling example is the strategic decision made by customers to store less data within the Snowflake ecosystem. This pragmatic approach has impacted both storage and compute revenue, showcasing an astute balance between efficiency and expenditure.

Snowflake’s Future And Promise It Hold For Investors:

In projecting forward, Snowflake's guidance reveals an ambitious yet attainable path. The company envisions a "normal" revenue beat in the second quarter, thereby setting the stage for a promising second half of the fiscal year. Anticipating a commendable 27% growth during this period, Snowflake is aiming high despite the challenges faced. This speaks volumes about its confidence in its solutions and its determination to drive progress.

Critically, this guidance reflects not just an incremental strategy, but a well-calculated plan founded on sound methodology. Snowflake remains steadfast in its approach, choosing not to inflate expectations artificially. It's this very transparency that sets Snowflake apart, showcasing its commitment to integrity even in the realm of financial projections.

While one might initially perceive this guidance as a pragmatic one, it signifies something greater—an unwavering belief in the potential for a more robust second half, propelled by the momentum built from a resilient first half. Snowflake's refusal to deviate from its tried-and-true guidance methodology speaks volumes about its commitment to authenticity, eschewing excessive buffers in favor of accuracy.

In essence, Snowflake's journey through these recent challenges is a testament to its unwavering commitment to growth, innovation, and the welfare of its clientele. With each strategic move, it solidifies its position not just as a market leader, but as a beacon of transparency and steadfastness.

Lets look at few noteworthy points that have emerged in the recent quarter. These aspects highlight both challenges and strategic moves that Snowflake has undertaken, shaping the company's path forward.

Operational Margin Outlook: The second consecutive quarter has brought about a sense of disappointment in the operational margin outlook. Snowflake has made the decision to revise its FY24 operating margin target, adjusting it from 6% to 5%. This recalibration is not without reason, with the recent Neeva acquisition contributing to this shift. Additionally, a distinct course of action has been taken in terms of net new sales representative hires, signaling a period of strategic reflection.

Sequential cRPO Decline: An aspect that merits attention is the sequential decline in cRPO (contracted remaining performance obligations) by a substantial $70 million. This decline, a first-ever for Snowflake, serves as an indicator of the challenging environment surrounding new bookings. This shift underscores the need for a deeper analysis of the factors impacting customer engagement and new commitments.

Neeva Acquisition: A remarkable move that has stirred interest is the acquisition of Neeva, a company boasting a modest workforce of just 40 employees. The appeal of this deal lies in Neeva's cutting-edge search technology - a technological treasure trove that Snowflake aims to harness for enterprise-level use cases. This strategic alignment demonstrates Snowflake's penchant for innovative expansion and a keen eye for solutions that can elevate its offerings in an ever-evolving market.

In summary, the landscape that Snowflake navigates is one of dynamic challenges and strategic maneuvering. The revision of the operational margin outlook, the unexpected decline in cRPO, and the acquisition of Neeva all paint a picture of a company that is not only adapting to the currents of change but also proactively seeking ways to leverage emerging technologies for enhanced enterprise solutions. As we look ahead, understanding the implications of these developments will be key to appreciating Snowflake's evolving trajectory.

Competitive Landscape With Databricks :

If we delve deeper and analyze the industry, a trend emerges where the competitive discourse and the level of alignment between Snowflake and the privately-held powerhouse Databricks appear to be on the rise.

Infrequent Customer Migration : It's essential to emphasize that while discussions about competitive positioning intensify, the practical phenomenon of customer migration – specifically, the shifting of data warehousing initiatives from Snowflake to Databricks – remains an infrequent occurrence. Company data suggests that Databricks' remarkable growth, exceeding a staggering 100%, has yet to reach the scale of Snowflake, accounting for less than 10% of Snowflake's expansive presence.

Snowflake's Unassailable Dominance : Within the realm of cloud-based data warehousing, Snowflake maintains its position as the undisputed leader and standard-bearer. Its unparalleled architecture and capabilities firmly establish it as the go-to solution for organizations seeking robust and efficient data warehousing services.

Databricks' AI Workload Advantage : While Snowflake maintains its stronghold as the de facto data warehousing standard, our inquiries and interactions indicate a noteworthy nuance. A prevalent sentiment emerges from these, suggesting that Databricks is carving out a distinctive niche in being better-suited for AI workloads. This is a significant pivot that shouldn't be overlooked, as AI workloads continue to gain prominence in the modern data landscape.

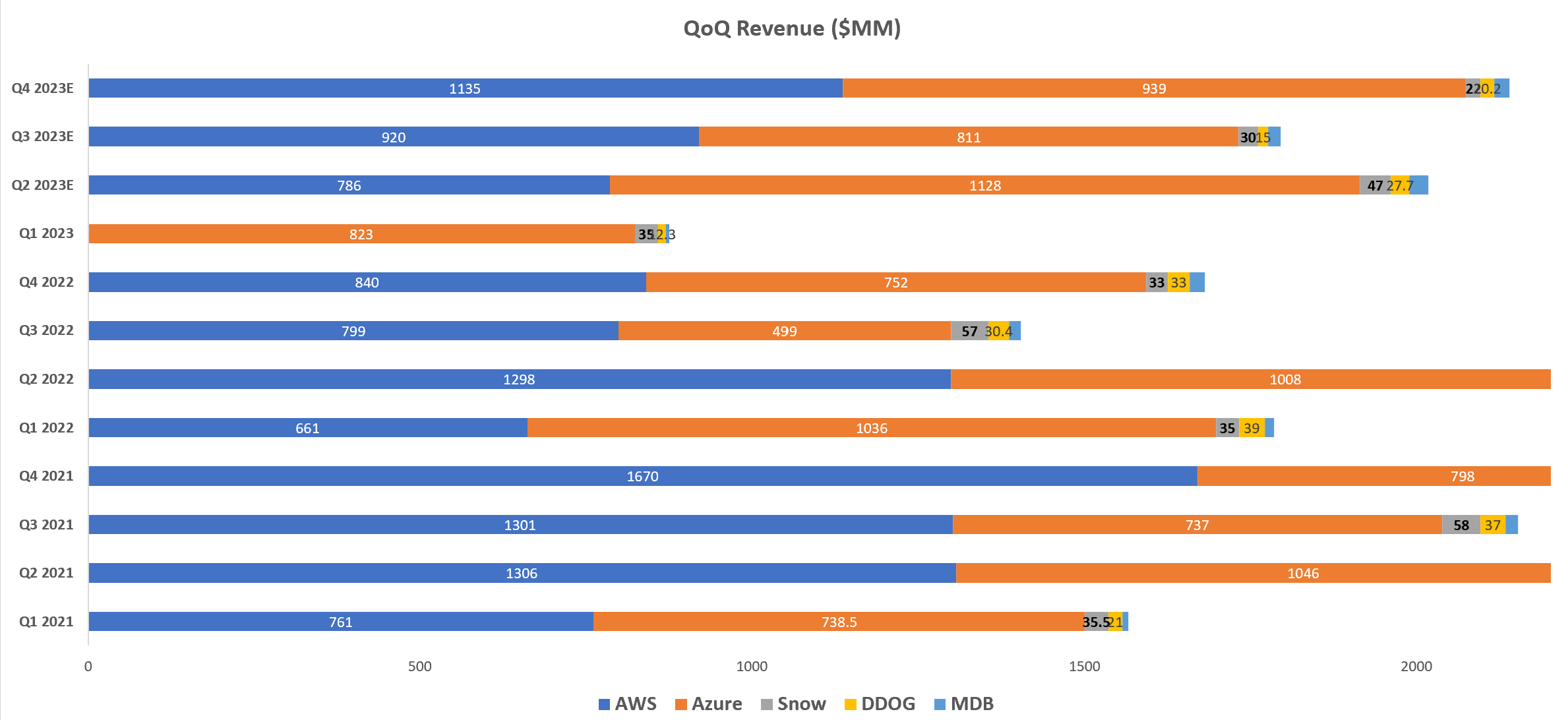

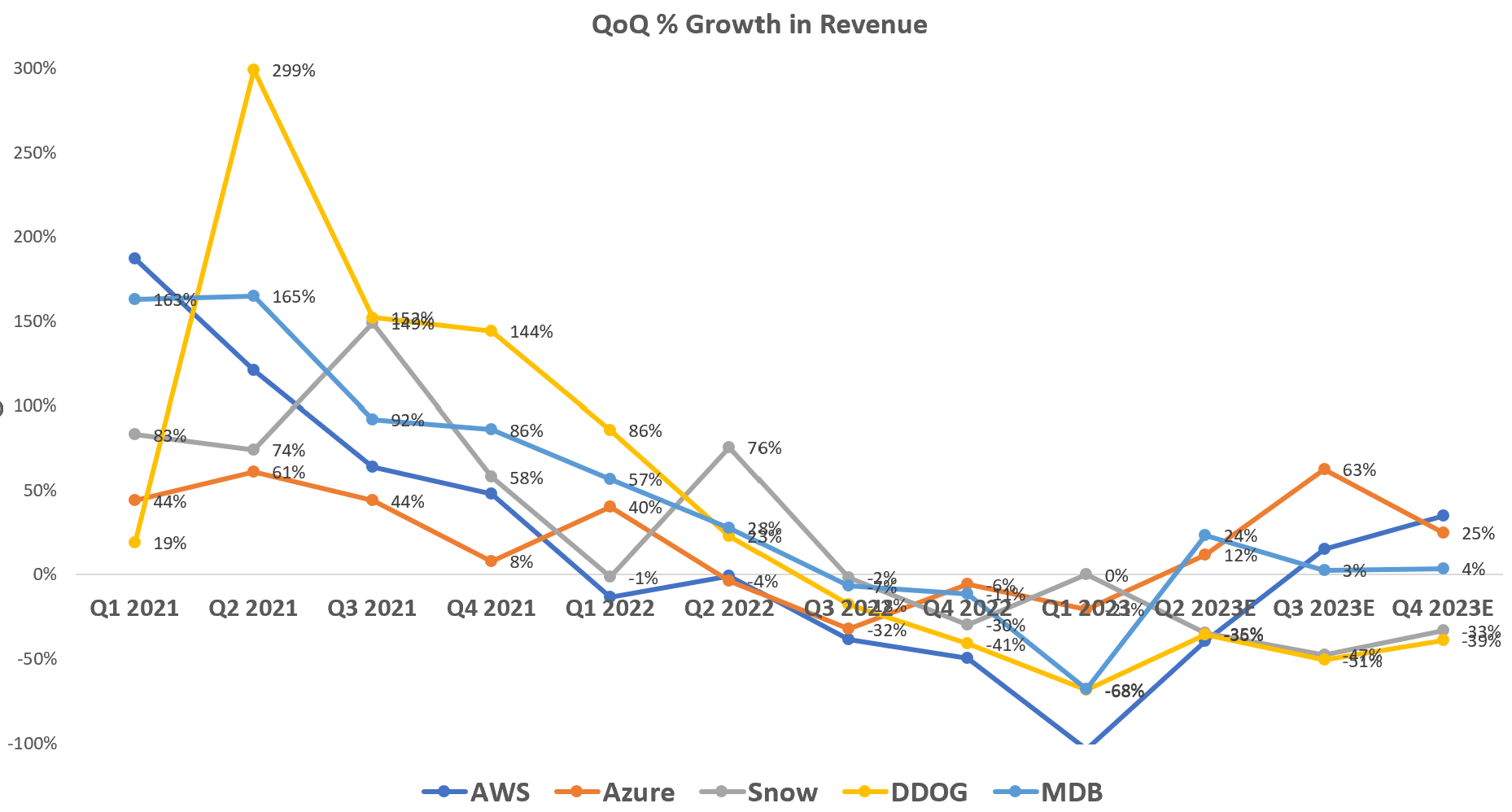

Let's analyze the data to substantiate this perspective. Chart below illustrates the sequential revenue growth patterns among key players in cloud infrastructure and software. In this context, it becomes evident that AWS faced a decline in sequential revenue growth year-over-year in Q1 2022 – a retrospectively significant red flag for the industry. The trend further deteriorated in Q3 2022, positioning AWS to soon lap over this challenging phase. Azure, on the other hand, encountered optimization headwinds that were comparatively less severe.

Looking specifically at Snowflake, it's noteworthy that the Q4 2022 period marked a notable decline in progressive growth by $33 million. This decline occurred approximately two quarters after AWS and Azure started experiencing pronounced pressure due to optimization efforts. This timing aligns with two key factors:

- Snowflake's explicit mention of significant enterprise optimization initiatives, which surfaced in the recent Q1 2023 quarter,

- accounts from customers that suggest a trend of first reducing excess spending on AWS and Azure before addressing smaller expenditure categories.

{kind=link}

Chart made using Company data and forecast model

{kind=link}

Chart made using company data and forecast model

Growth Expectations:

Guidance for Q2 2024 Product Revenues: Snowflake's guidance for Q2 predicts product revenues of $625 million, indicating a sequential increase of $35 million or 34%. However, this projection reflects a significant year-over-year decline of 51%. Notably, this decline is more pronounced than the flat sequential growth in Q1 and even worse than the 31% drop in sequential growth observed in Q4.

Impact of Continued Cost Optimizations: There's a level of uncertainty surrounding the potential for upside growth due to ongoing cost optimizations among major customers. The concern arises from the fact that if large clients continue to optimize their cloud spending, it could potentially limit the positive impact on Snowflake's revenue growth.

Visibility on Optimizations at Guidance Setting: On the one hand, it might be assumed that Snowflake had foreseen the ongoing optimizations by its customers when it initially provided its guidance in late May. The company's statement about collaborating with large customers to optimize their environments suggests that they were aware of the potential challenges stemming from customers' cost pressures.

Historically-Weak Period and Conservative Guidance: On the other hand, Snowflake's decision to set the Q2 guidance shortly after a period of historically weak usage growth could have prompted the company to adopt a more cautious stance. This caution might have driven them to offer a conservative projection.

June Consumption and Investor Day: It's worth noting that Snowflake referenced in-line June consumption during its Investor Day, which took place in late June. This event provides an additional data point indicating that the company's projections were based on real-time information and assessments.

In summary, the provided points underscore the complex considerations that Snowflake faced when setting its guidance for Q2 product revenues. The interplay of ongoing customer cost optimizations, historical usage trends, the company's conservative approach, and the data available during Investor Day all contribute to the intricate backdrop against which the guidance was formulated.

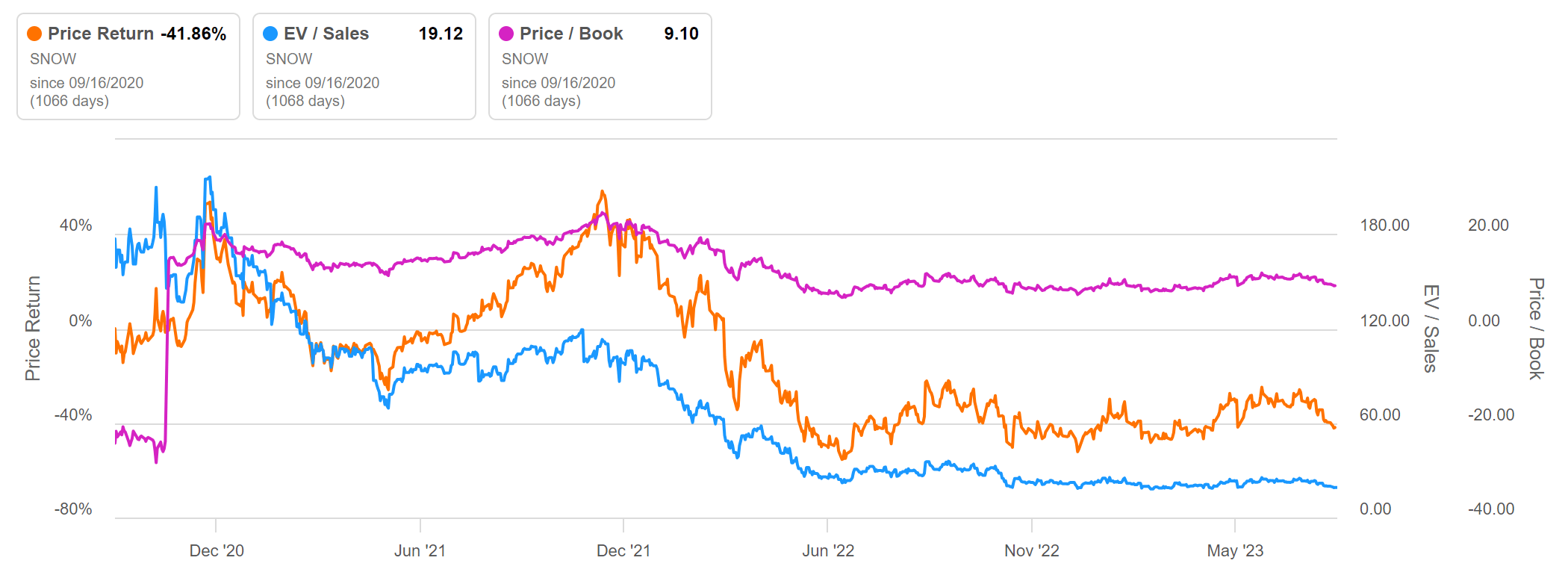

SNOW Stock Valuation :

Currently, Snowflake's shares have seen a year-to-date increase of only 5%, and they have experienced a slight decline in value since the Datadog financial report. Despite this, Snowflake's stock remains the highest-priced high-growth software stock. It holds a valuation of 15X of revenues for FY 2024 and FY 2025, making it almost on par with MongoDB in terms of valuation. With Q2 earnings around the corner and scheduled for Aug 23 rd , this stock is a Hold and spend optimization will be the key to watch for.

{kind=link}

Seeking Alpha

Conclusion :

In summary, a reasonable interpretation emerges: Snowflake could potentially face several more quarters of optimization-related challenges to overcome. This projection persists even as AWS offers signals that it might be approaching the culmination of its optimization phase. This narrative underscores the dynamic nature of optimization headwinds in the cloud landscape and implies that Snowflake's journey through these challenges might extend further, despite AWS nearing the end of its optimization cycle.

In conclusion, the competitive interplay between Snowflake and Databricks has become more palpable, yet the core dynamics reveal that Snowflake's dominance in cloud-based data warehousing remains steadfast. Databricks' rapid growth, while remarkable, has not reached the magnitude of Snowflake's presence, with customer migration remaining an uncommon event. It's crucial to acknowledge Databricks' strategic advantage in catering to AI workloads, a facet that accentuates the evolving landscape of data utilization.

For further details see:

Snowflake Q2 Earnings Preview - Watch For Spend Optimization