SNOW - Snowflake Q3 Review: Too Far Too Fast

2023-11-30 11:05:36 ET

Summary

- Snowflake's stock is jumping up 7.5% after reporting strong Q3 earnings with revenues of $734.2M and non-GAAP adj. FCF of $110.8M.

- The company's total customer count growth is slowing, but the number of customers with over $1M in product revenue increased by 52% y/y.

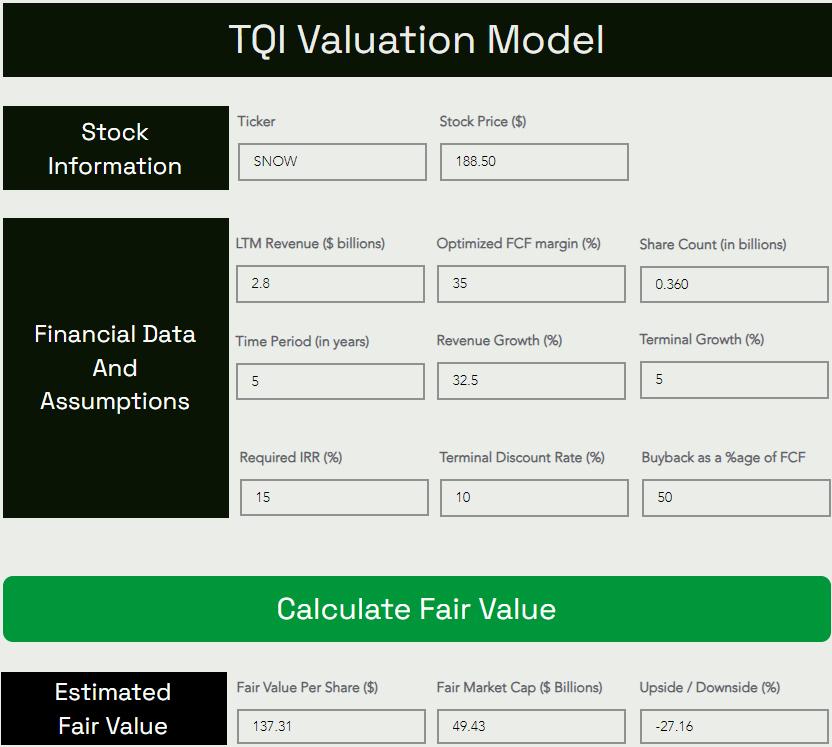

- Snowflake's valuation is deemed too high at ~100x P/FCF, with my fair value estimate of $137 per share implying a downside of -27% from current levels.

- In this note, I share my analysis of Snowflake's Q3 FY2024 report and update my valuation model for SNOW. Read on to learn more.

Introduction

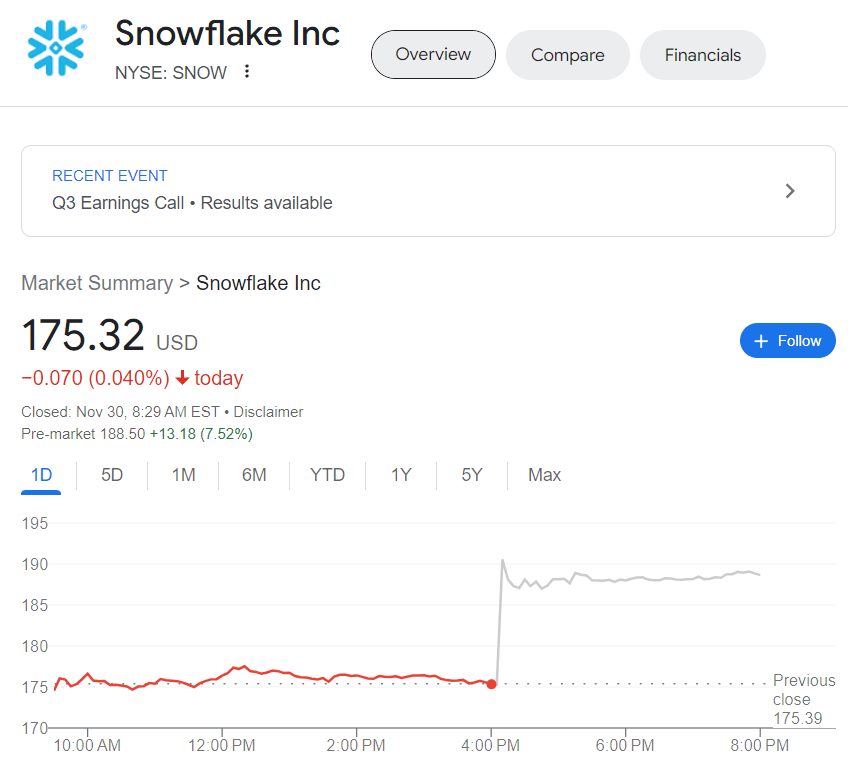

On the back of reporting a double beat, Snowflake Inc. (SNOW) stock is jumping 7.5% in pre-market hours to $188.50 per share or ~$68B fully-diluted market capitalization. While the data cloud company is growing rapidly in the era of AI as enterprises race to get their data in order, Snowflake's stock appears to be running ahead of its skis at >20x P/S.

{kind=link}

In today's note, we will review Snowflake's latest quarterly report, and re-run it through TQI's Valuation Model to see if it is an attractive investment at current levels.

Brief Review Of Snowflake's Q3 FY24 Earnings

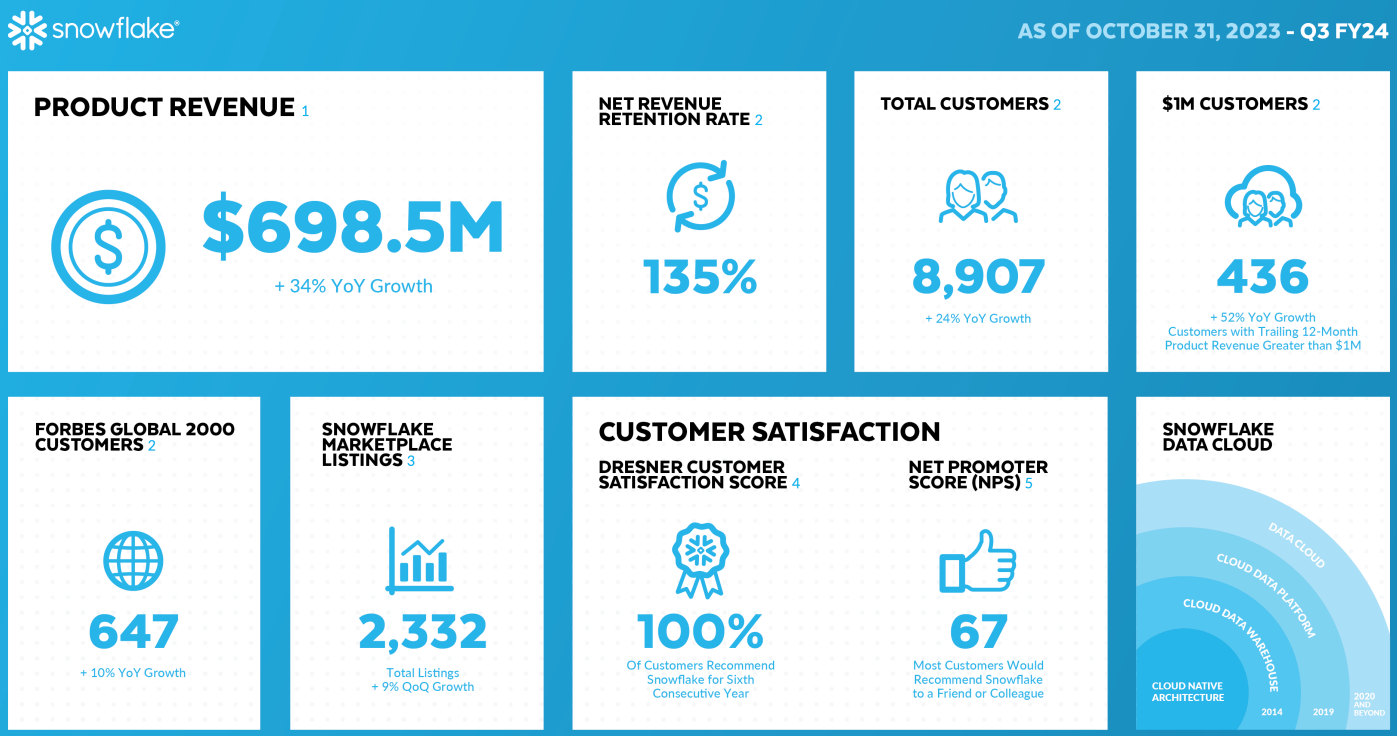

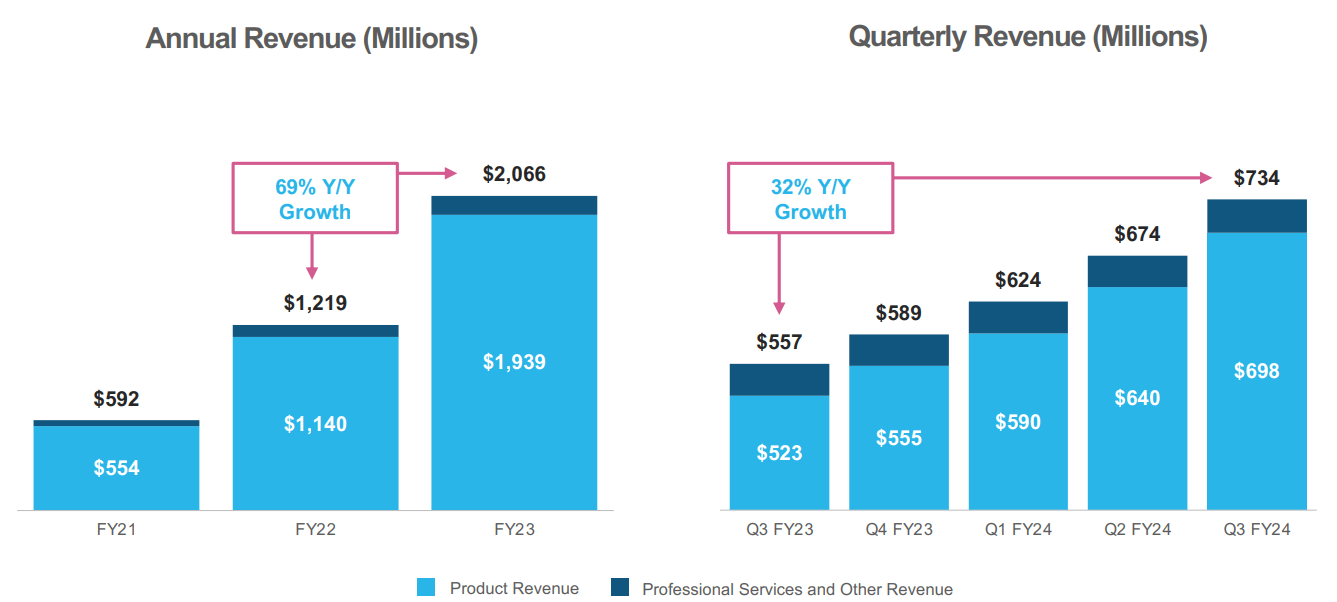

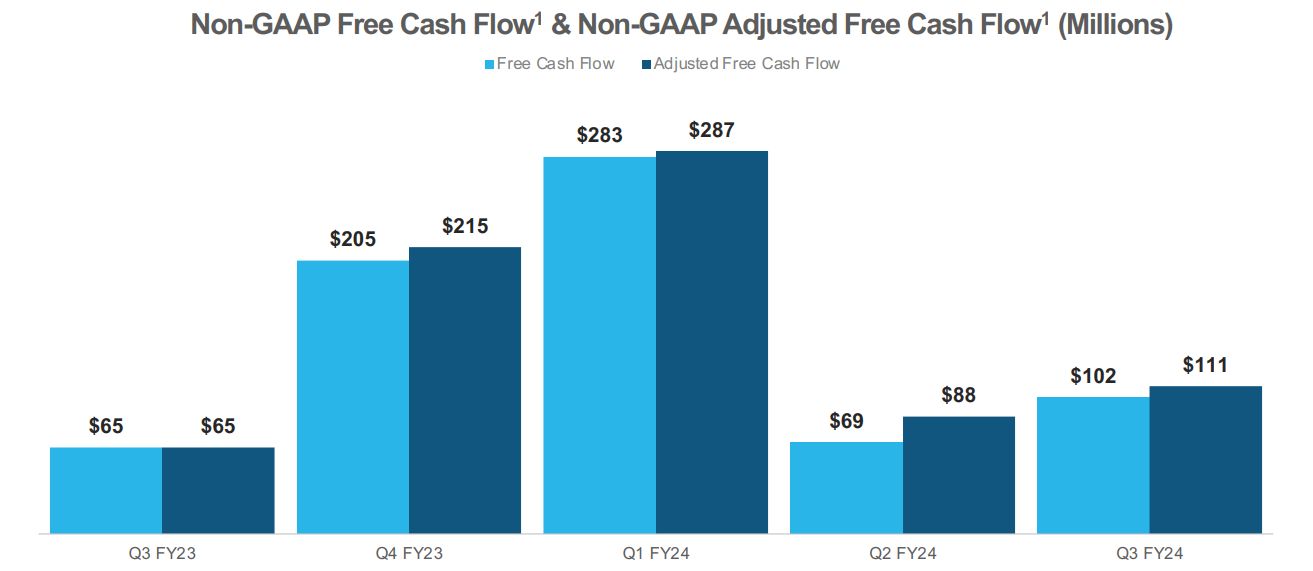

For Q3 FY2024, Snowflake reported quarterly revenues of $734.2M (vs. est. of $713.54M), a figure that reflected ~32% y/y growth. Of these, product revenues made up $698.5M (up ~34% y/y), with professional services making up the rest. Furthermore, an improvement in product gross margins and a reduction in operating expenses as a percentage of revenues drove Snowflake's non-GAAP adj. FCF margin to +15% in Q3 FY2024, resulting in quarterly adj. FCF of $110.8M.

{kind=link}

Management commentary on Q3 FY2024:

During Q3, product revenue grew 34% year-over-year to reach $698 million and non-GAAP adjusted free cash flow was $111 million, representing 70% year-over-year growth. These results reflect strong execution in a broadly stabilizing macro environment "

- Frank Slootman (Chairman and CEO, Snowflake)

While Snowflake is growing revenues rapidly at scale whilst generating positive free cash flow, Snowflake's revenue growth rates have decelerated significantly during recent quarters, with management blaming macro headwinds for the rapid deceleration. Hence, I was pleased to hear that Slootman and Co. are now seeing a more stable macro environment.

{kind=link}

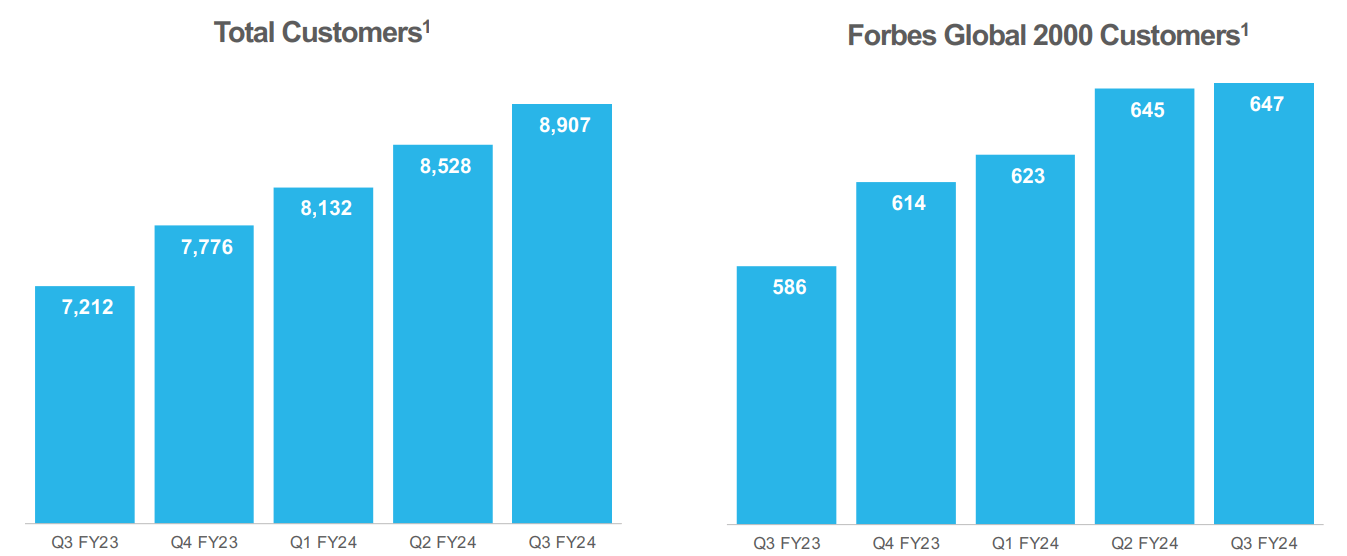

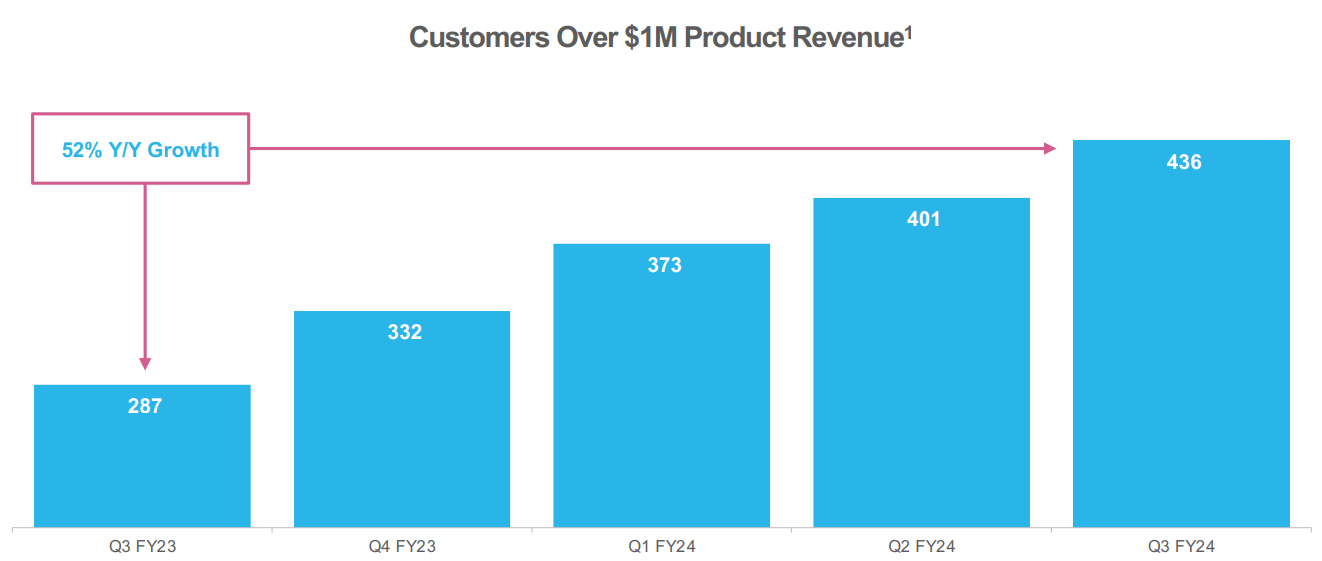

In Q3, Snowflake's total customer count growth slowed to ~23% y/y; however, as we know, Snowflake has been focusing on quality over quantity when it comes to acquiring new customers. While Snowflake added just two Forbes Global 2000 customers in Q3, Snowflake's "Customers over $1M Product Revenue" count rose 52% y/y to 436 organizations. According to SNOW's management:

In the long run, such large enterprise customers could conservatively spend $10M or more on its platform annually.

{kind=link}

{kind=link}

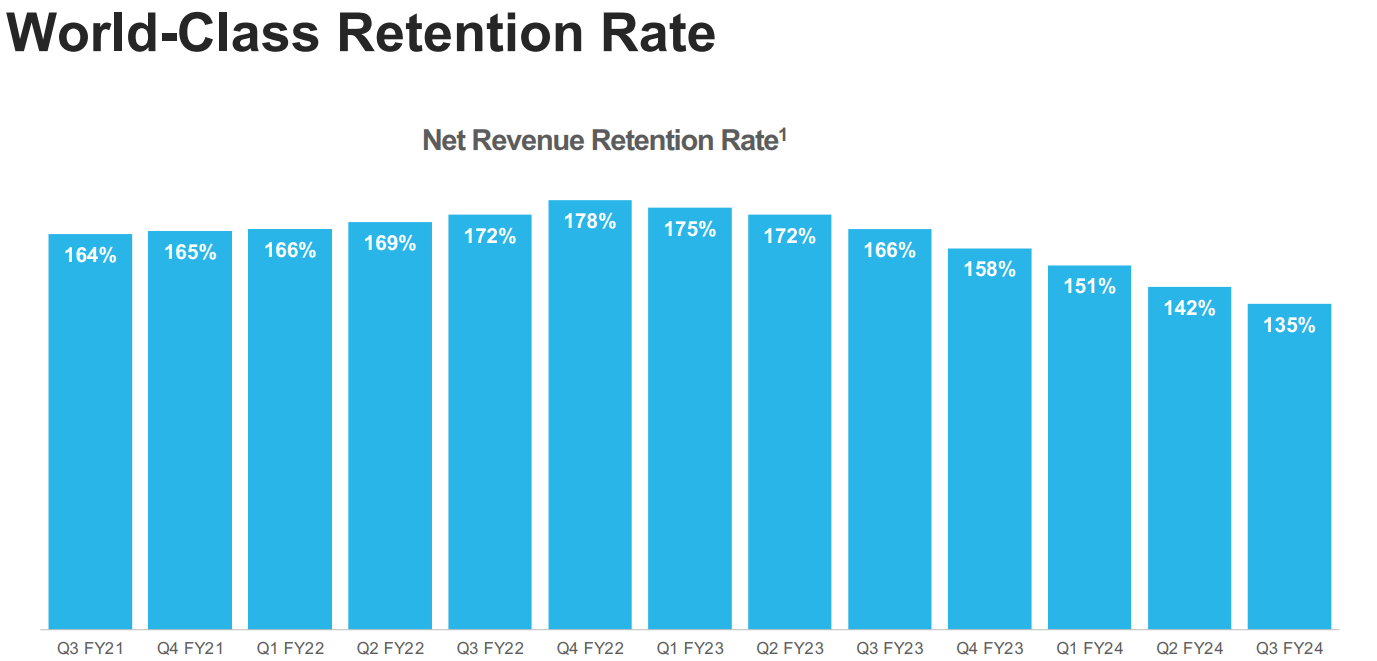

A lot of Snowflake's enterprise customers are scaling up their spending on its platform [moving over their data and workloads to Snowflake], and this is reflected in SNOW's net retention rate of 135%. As I see it, Snowflake continues to extract more revenues from its existing customers, albeit at a slower pace than it did in the past. As investors, we must continue to monitor SNOW's NRR closely, as further moderation here could signal a more pronounced slowdown in the business.

{kind=link}

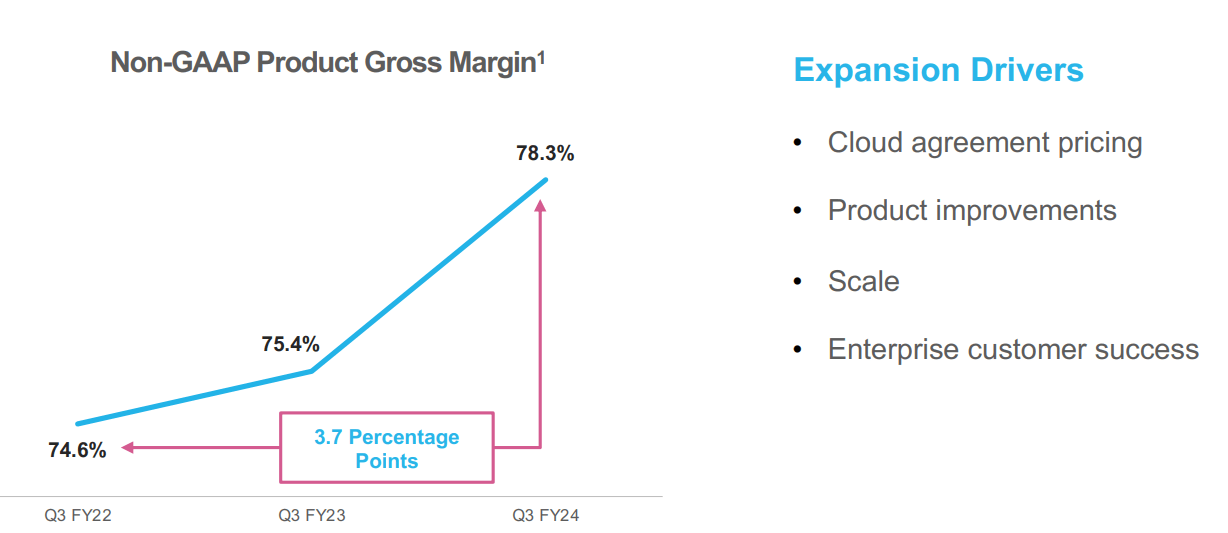

As we have discussed in the past, the strength of Snowflake's platform increases with scale, as it could negotiate better deals from cloud vendors, and better prices mean more and more customers will choose to join Snowflake. In Q3, SNOW's product gross margin improved to 78.3% (up +290 bps y/y).

{kind=link}

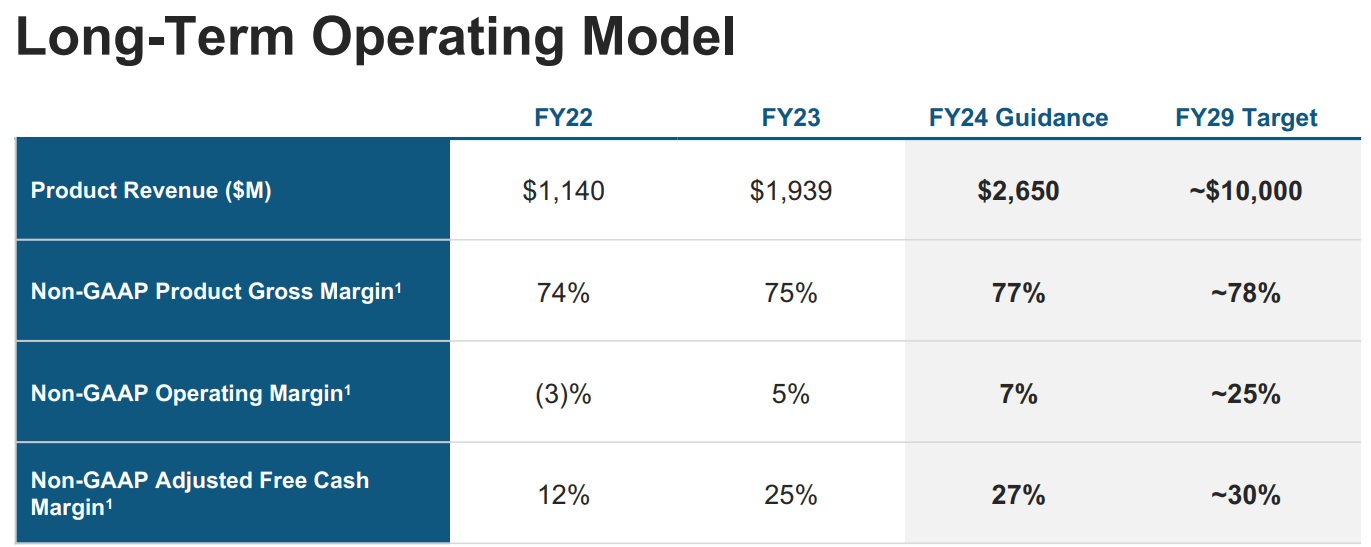

For product margins, Snowflake is already hitting long-term operating model targets and management talked about multiple margin headwinds capping product gross margins at current levels during yesterday's earnings call. Therefore, I wouldn't bet on further gross margin expansion from here, at least for the foreseeable future.

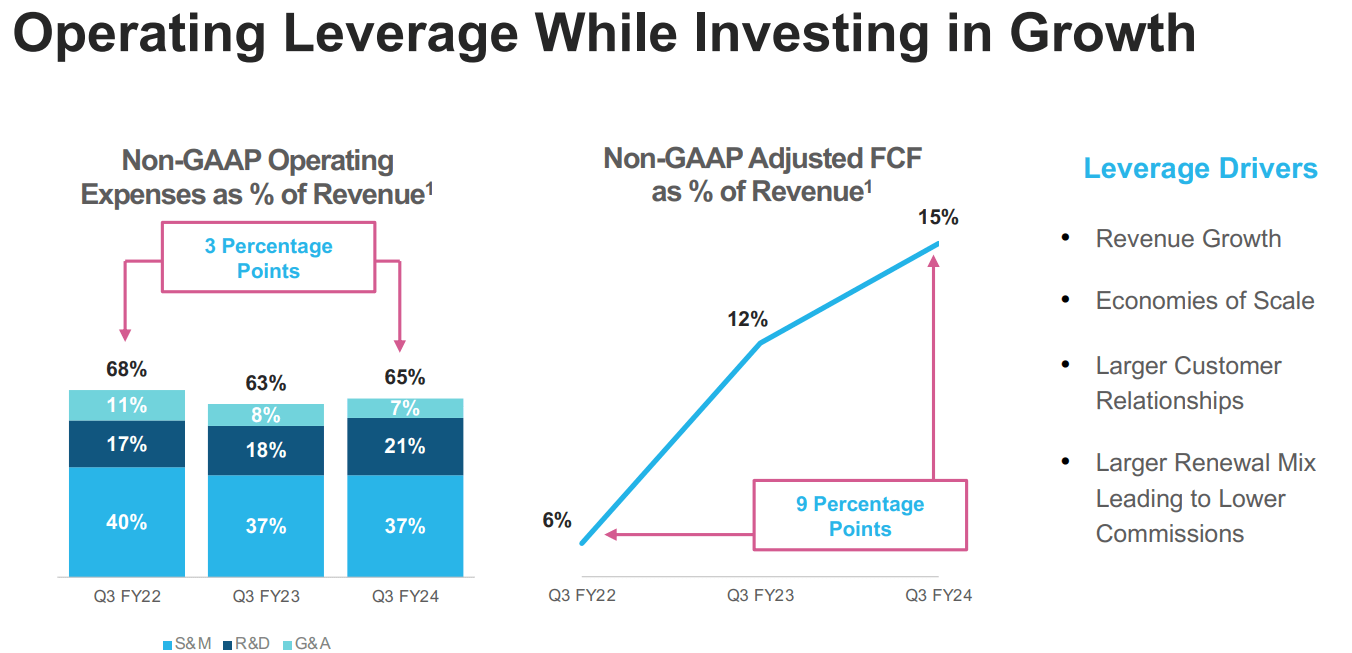

In addition to revenues scaling up and gross margins expanding, Snowflake is showing signs of operating leverage and generating significant amounts of free cash flow. During Q3, Snowflake's adj. FCF rose by ~70% to $111M.

{kind=link}

{kind=link}

While Snowflake's growth rates are moderating as its revenue base grows, the business looks very healthy at this moment in time.

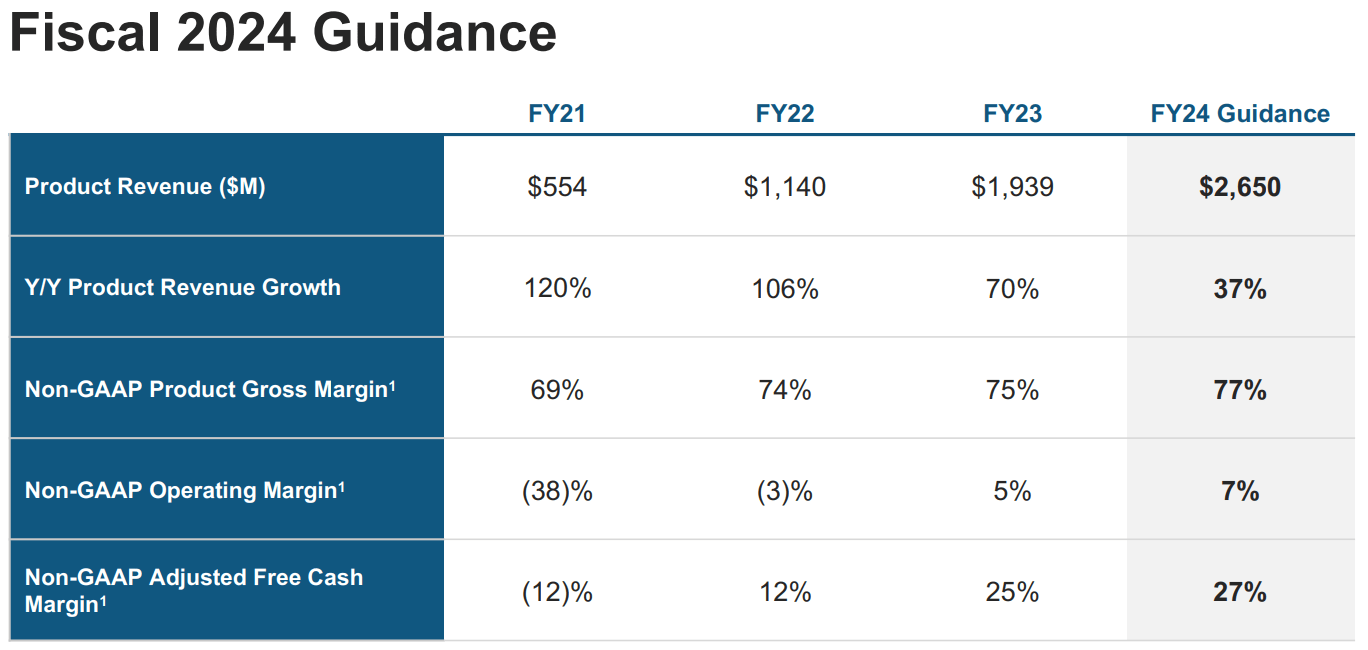

For Q4, Snowflake is projected to deliver Product revenues of $716-$721M (growth of ~29-30% y/y), which came in higher than Wall Street estimates but still implies further growth deceleration. Given seasonality patterns and management's history of sandbagging guidance, I am satisfied with the updated guide for Q4 and FY2024.

{kind=link}

Overall, Snowflake registered a strong quarter and lifted guidance for the full year. However, let us now evaluate Snowflake's valuation to see if the stock makes sense here as an investment or not.

SNOW Stock Fair Value And Expected Returns

Before I share my updated valuation model, I would like you to read this excerpt from one of my previous notes on Snowflake:

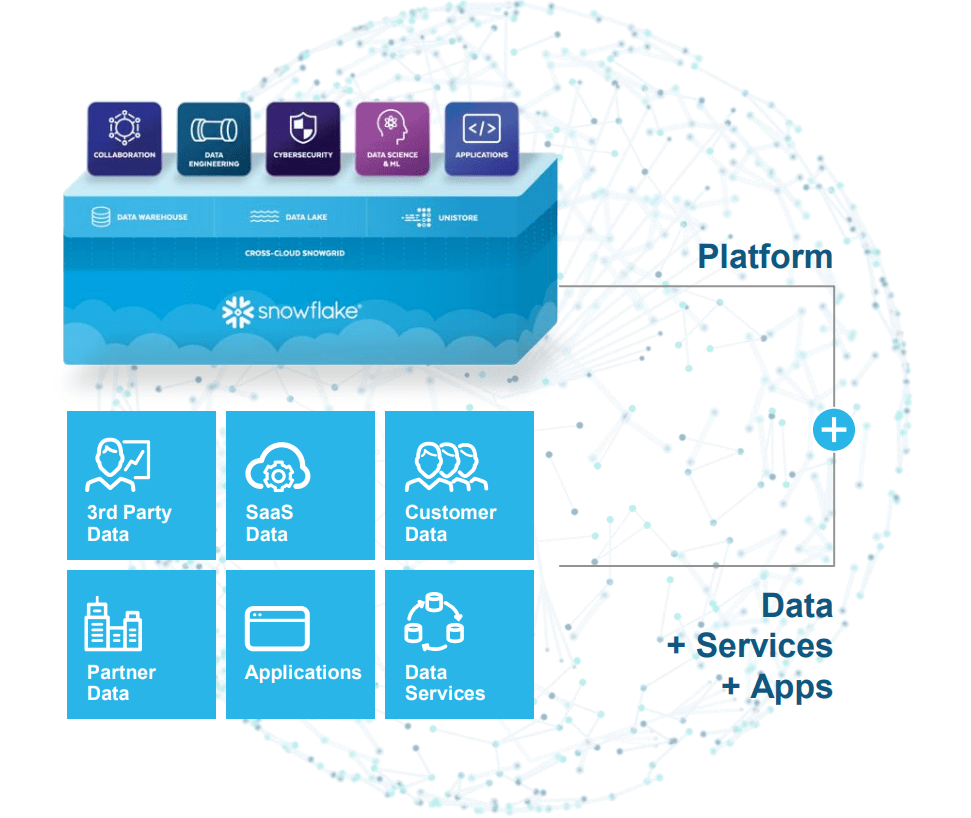

Snowflake is pioneering the Data Cloud - a global network where thousands of organizations mobilize data with near-unlimited scale, concurrency, and performance. Inside the Data Cloud, organizations unite their siloed data, easily discover and securely share governed data, and execute diverse analytic workloads. Snowflake delivers a single and seamless experience across multiple public clouds. Snowflake's platform is the engine that powers and provides access to the Data Cloud, creating a solution for applications, collaboration, cybersecurity, data engineering, data lake, data science, data warehousing, and unistore.

That's a lot of technical terminology. Simply put, Snowflake builds software (for managing the use of cloud infrastructure) that sits between organizations and public cloud vendors. Also, Snowflake is building a marketplace for data providers (sellers) and organizations (buyers) - Data Cloud. As investors, all we need to know is that both of these platforms are gaining traction.

Amid a challenging macroeconomic environment, Snowflake continues growing like a weed, and it is doing so whilst improving margins. As we saw today, Snowflake is not yet profitable; however, it is already producing massive amounts of free cash flow.

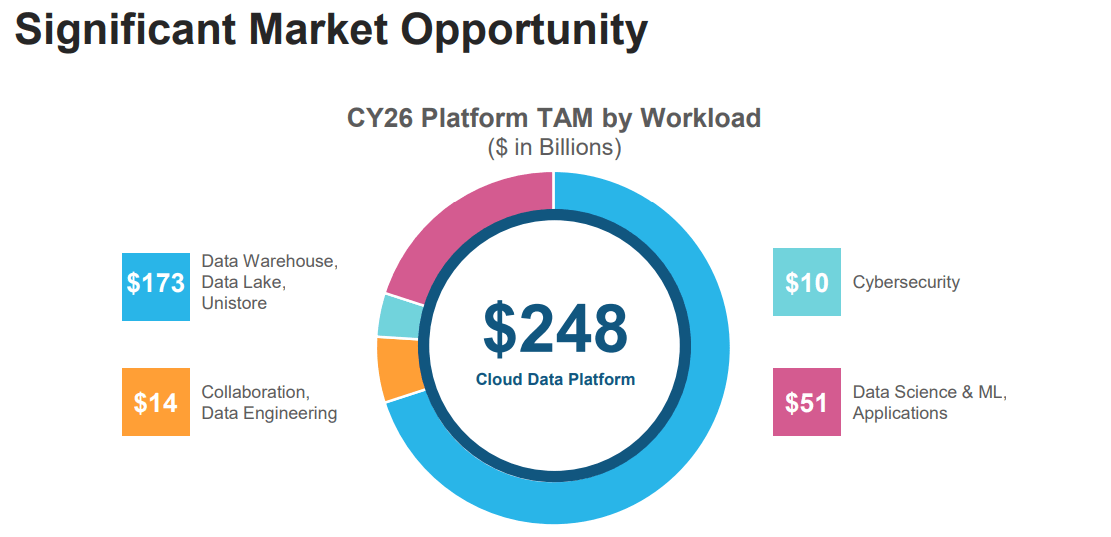

Having a cash (plus investment) balance of ~$4.9B [$4.5B as of end of Q3 FY2024] and no debt should provide management with added flexibility to remain aggressive during the impending downturn to capture market share. Snowflake is positioned to win big, and its total addressable market opportunity is expected to grow to $248B by 2026.

Source: Snowflake Stock: Don't Speculate, Just Accumulate (Slowly)

{kind=link}

{kind=link}

{kind=link}

Here's my updated valuation model for Snowflake:

{kind=link}

{kind=link}

Summary of update:

- Old FV estimate: $134.14, New FV estimate: $137.31

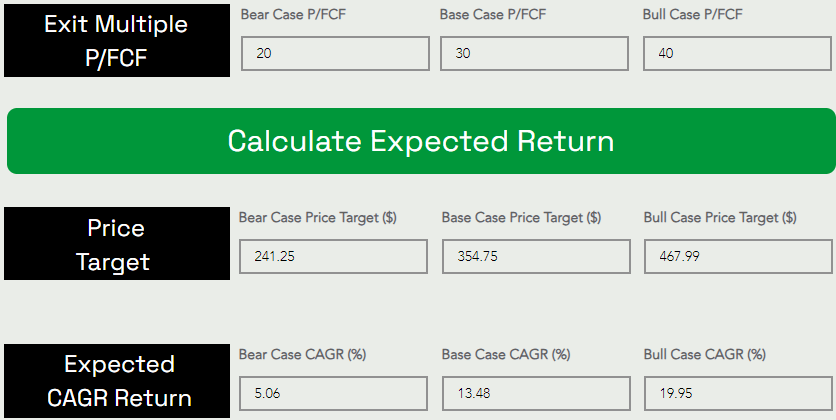

- Old Base case PT (5-yr): $347.91, New Base case PT (5-yr): $354.75

Final Thoughts

Given an uncertain macroeconomic backdrop, buying Snowflake at ~100x P/FCF is too hard for me despite having a bullish view of its long-term business prospects. If you have been following my work on SNOW, you know that I have been accumulating Snowflake shares in the low to mid-$100s since 2022. While I am ecstatic about the post-ER pop in SNOW, I think the stock has run up too far, too fast.

My updated fair value estimate for Snowflake is $137 per share, which implies a -27% downside from current levels. With SNOW's 5-year expected CAGR return falling short of our investment hurdle rate of 15%, it is not a "Buy" according to TQI's Valuation Model.

Paying a premium for a high-quality, rapidly growing business like Snowflake is not the worst idea out there, as SNOW could grow into this valuation within 12-24 months. However, I think broad market indices are overdue for a correction/pullback and Snowflake's Q3 report did nothing to justify chasing the stock at currently elevated levels.

Key Takeaway: I continue to rate Snowflake a "Hold/Neutral" at $188.50 per share, with the idea of resuming slow, staggered accumulation if the stock pulls back to the mid-$100s.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

For further details see:

Snowflake Q3 Review: Too Far, Too Fast