SNOW - Snowflake: Rapidly Improving Margins Fuel Upside Potential

2024-01-08 04:09:04 ET

Summary

- Snowflake's stock has experienced a pullback, but its attractive growth rate makes it a buy.

- There may be further downside risk in the short term, but the long-term outlook remains bullish.

- SNOW continues to add large customers, and its profitability is improving, making it an appealing investment.

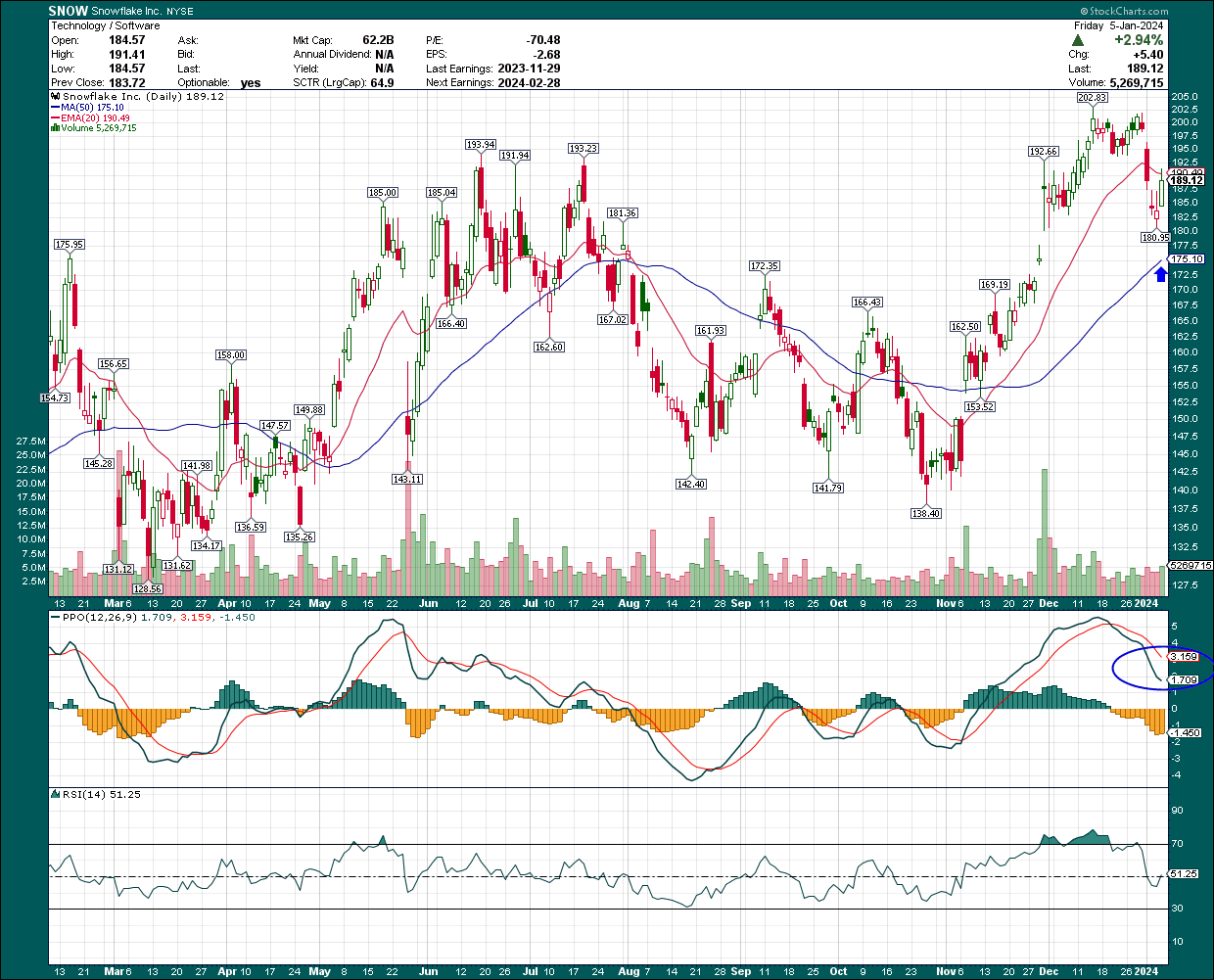

Shares of burgeoning cloud data service provider Snowflake ( SNOW ) have been flying since the bottom in October. There's been a sharp pullback to start the year, but given the company's extremely attractive growth rate in the years ahead, I consider the stock a buy. The short-term picture is somewhat murky, but any further weakness would be a chance to average in at more favorable prices.

Is downside action complete?

The answer to that is as yet unknown, but I wouldn't be surprised to see the stock trade down a bit further in the short term. After peaking at just over $200 in December, shares are under $190 but also failed the 20-day exponential moving average. With that line moving down, a 50-day simple moving average test is possibly in the cards.

{kind=link}

That line is currently about $176 but rising quickly, so it wouldn't take a huge amount of selling to get there. Importantly, the PPO is pointed sharply downward, indicating a quick retrace from unsustainable levels above 5. As we get closer to the centerline, momentum favors a reversal back to the upside. In short, I think there's potentially a bit more downside risk here short term, but the long-term picture remains quite bullish, which we'll dig into below.

Growth is slowing but plenty left in the tank

Anytime a company that grows as quickly as Snowflake starts to see growth rates tail off, it can spell disaster for the stock. Admittedly, the stock is still down over half since its peak in 2021. However, despite the fact that growth rates are slowing off of unsustainable levels, there are years and years of high rates of growth from multiple levers left ahead.

{kind=link}

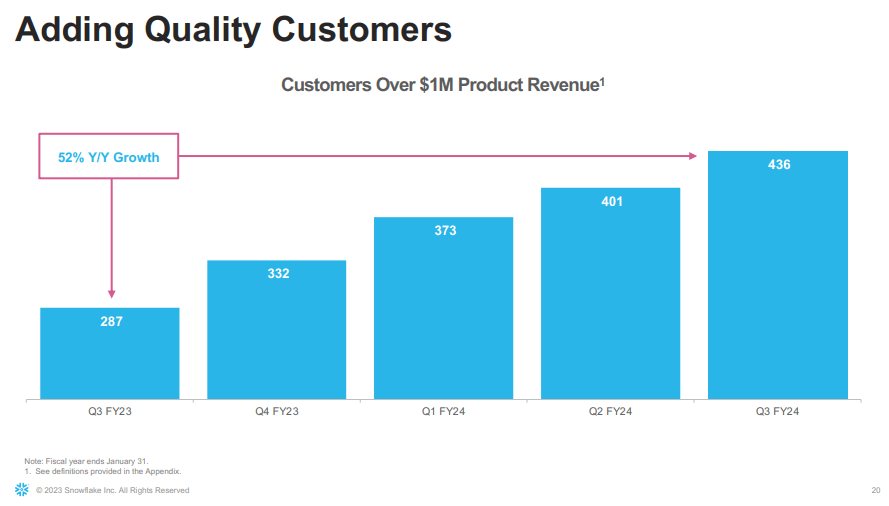

Snowflake continues to add large numbers of big customers, defined as those with at least $1 million in annual product revenue. In the most recent quarter, that number was up over half from the prior year period. This kind of growth cannot continue forever, but much of the attractiveness of the growth story here is that Snowflake is attracting customers from the top echelons of commerce across the globe. The platform works, and it's convincing large companies with big data needs, big budgets, and staying power to join the platform.

{kind=link}

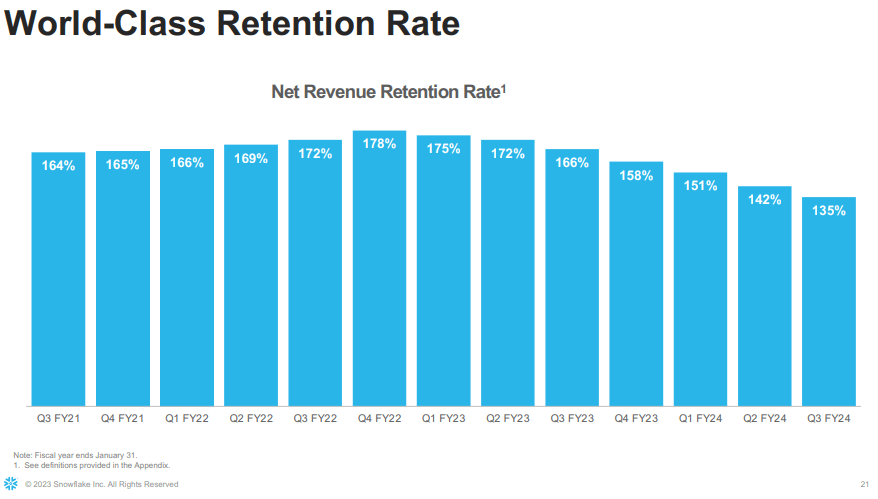

One thing that has certainly fallen off in recent quarters is the company's net revenue retention rate, which is now 135%. That's a long way off the high of 178% from the last quarter of FY2022, but importantly, still extremely strong. This is essentially a measure of second-year usage of the platform of customer cohorts over first-year usage of the platform, so anything above 100% is favorable. It is important that we see this number stabilize, or it could spell trouble for the stock. Adding customers is one way to boost growth, but if this number continues to fall, it could be a net headwind over time. We are not there yet, but if I have a concern about Snowflake's future growth, it's right here.

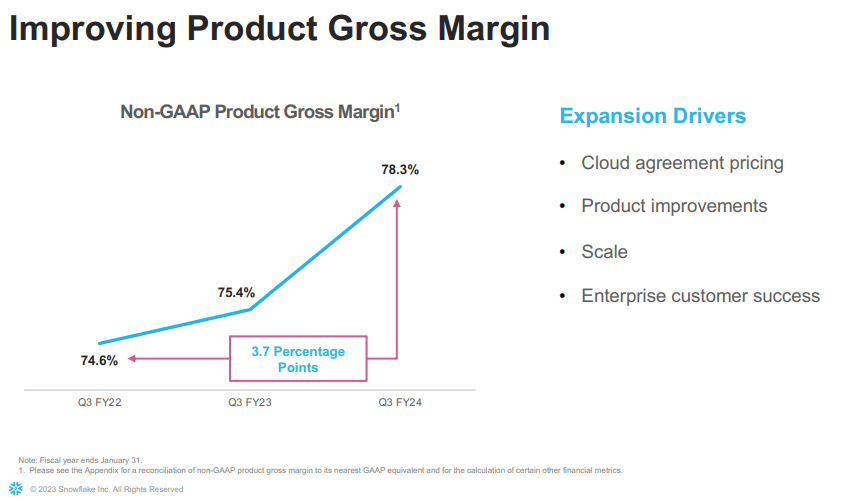

On the profitability side, we see a much rosier picture.

{kind=link}

Gross margin has moved higher by 370bps over the past two years, and you can see the drivers to the right. The company's scale will only continue to improve as the years go on, and Snowflake is producing earnings consistently now, thanks in part to its growing gross margins.

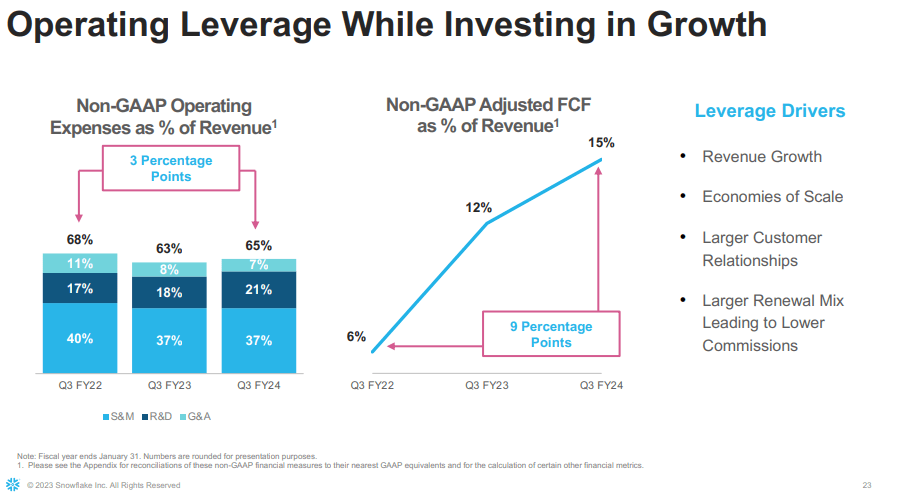

But that's not the only lever it can pull.

{kind=link}

Operating expenses continue to be leveraged down, and again, as revenue continues to grow, this should only get better. We know software companies see massive operating leverage over time as they grow, as they can sell essentially limitless access to its services without commensurate expense growth. Snowflake is still building for the future, but we should see these expense numbers continue to fall over time.

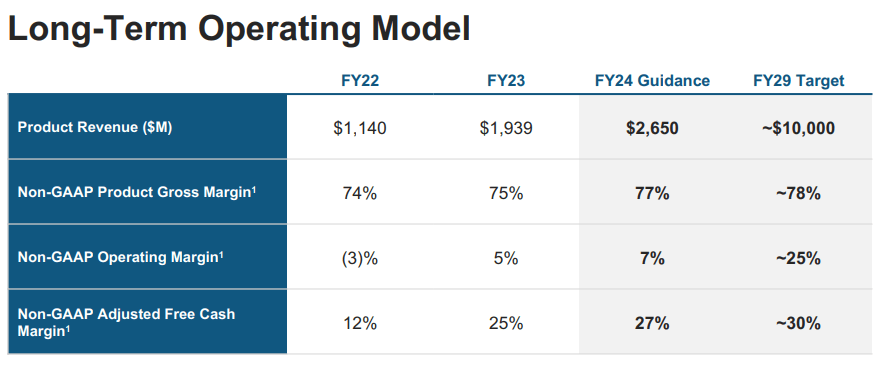

Finally, the company's guidance for this year shows ~7% operating margin, but much, much higher margins over time.

{kind=link}

This is exactly what we're looking for as revenue grows, and expenses shrink on a relative basis. We'll see if Snowflake can get there, but all indications at the moment are that it has every opportunity to do so. That's the growth story you're buying here.

More short-term, analysts have become much more bullish lately.

{kind=link}

Almost all EPS and revenue revisions for the past 90 days have been higher. After a few quarters of moves lower, it appears we've reached the inflection point and have moved past the bottom. If these moves stick, that should correspond to a sustainable bottom having been formed in the stock.

Growth versus valuation

As we look to wrap up here, the consideration of growth versus valuation is an important question. We know Snowflake has been growing at rapid rates, and in all likelihood, will continue to do so for some time to come. The question, then, becomes whether the stock is valued favorably. Valuation is always in the eye of the beholder as valuing something is inherently subjective. However, we have some clues we can use to make a judgment.

First, the only dark mark on Snowflake's Quant Rating is the valuation. For what it's worth, it's up from F to D in recent months, but it's obviously quite a low rating. We know Snowflake isn't going to be cheap given its growth rates and the fact that it's still very early in its growth cycle. It has minimal earnings, so P/E is useless, but we can focus on price-to-sales.

Seeking Alpha

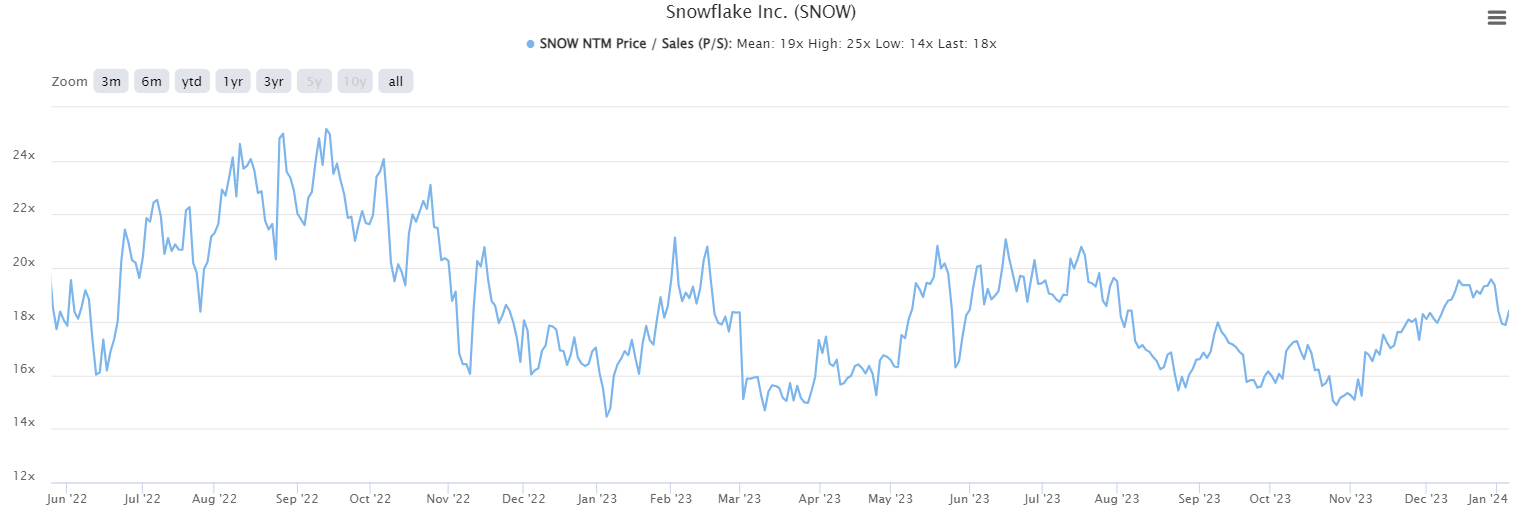

Sales are growing at 30%+ annually through 2026 according to current analyst estimates. That growth rate looks sustainable given net retention rates and customer growth, so we can value the stock using these assumptions.

{kind=link}

The stock is at 18X forward sales at the moment, which is just under the post-COVID average of 19X sales. Snowflake's growth rates have slowed recently, but that's just because the base from which it's growing continues to get larger. That's a net negative for the valuation, but the offsetting factor is that Snowflake's profitability is much better than it was, and improving all the time. In other words, while top line growth rates may be slowing due to the law of large numbers, the value of each dollar of revenue continues to increase given gross margins and operating expenses are both improving.

Given this, I see Snowflake's valuation as just fine for the long-term bull case, and given the improvements in profitability that are coming in quite quickly, I think it's a long-term buy. Short-term, we may see a bit more weakness in the stock until it finds support, but for long-term holders, I see a very bright future.

For further details see:

Snowflake: Rapidly Improving Margins Fuel Upside Potential