SNOW - Snowflake's Data Marketplace: The Key To Unlocking The Potential Of Generative AI

2023-12-07 23:27:17 ET

Summary

- Snowflake's stock price remains highly valued despite a huge decline since 2021, making some investors hesitant to buy.

- Its Data Cloud enables better AI results.

- The company's strengths include its first-mover advantage, high switching costs, network effects, and its role in the generative AI revolution.

Although Snowflake's ( SNOW ) stock price is down 37% from when I last wrote about the company on August 30, 2021, it remains one of the most highly valued stocks in the market based on traditional valuation methods. Some investors take one look at the company's price-to-sales (P/S), forward price-to-earnings (P/E), and price-to-free cash flow and refuse to consider buying the stock, even after its recent sterling third quarter 2024 earnings report.

This article will discuss what Snowflake does, its market opportunity, how it enables generative AI, and how the stock still has potential upside at even these elevated valuations. Consider buying if you are an aggressive long-term investor who would be interested in a company that enables the generative AI revolution.

What the company does for customers

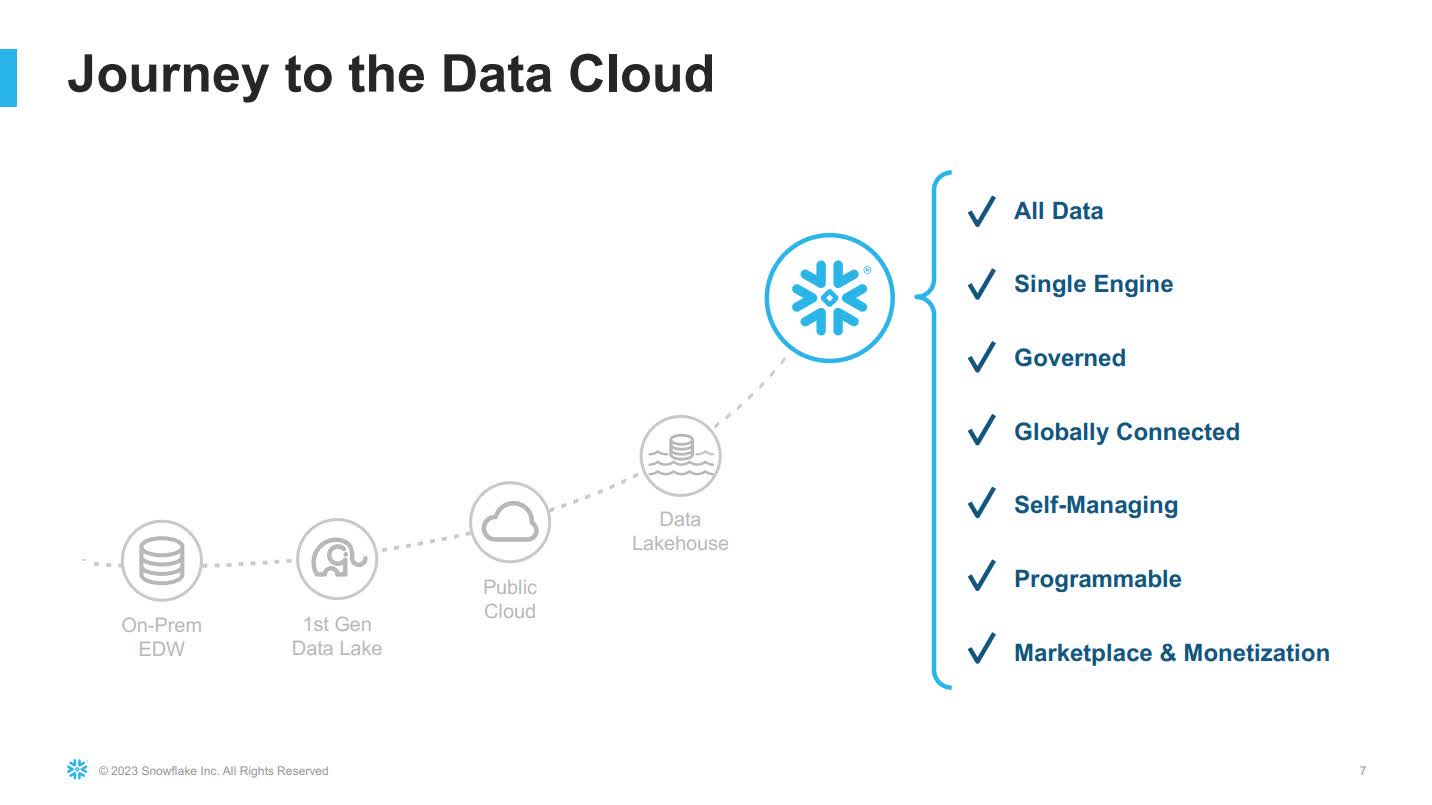

Snowflake first emerged as an on-prem enterprise data warehouse , a data management system that stores and manages structured data within a customer's own data center. The company eventually transformed into a data lake, a centralized repository of raw, unstructured, and semi-structured data in its native format. Unstructured data is information that is challenging to organize for a user to search effortlessly. It is nearly impossible to process and analyze using traditional data analysis tools. Some examples of unstructured data include the Internet of Things ("IoT"), video, audio, images, social media posts, and email data.

Snowflake later moved to the cloud and became a data lakehouse, a unified platform for storing, processing, and analyzing structured and unstructured data. More recently, the company started calling itself a Data Cloud, defined by Snowflake as " a single platform connecting businesses globally, at practically any scale to bring data and workloads together ."

Snowflake Third Quarter Fiscal Year (FY) 2024 Presentation

{kind=link}

The company also provides customers on its platform access to a Data Marketplace where they can buy, trade, and gain free access to third-party data. Customers can also find many third-party apps on the marketplace that they can use to extend Snowflake's platform's functionality. Snowflake Management was not the first to think of a data marketplace; a few previous efforts failed to gain traction while Snowflake's Data Marketplace has grown in prominence.

Management has included forecasts in its presentations that by the end of 2026, its opportunity will increase to $248 billion , consisting of $173 billion in the Data Warehouse, Data Lake, and Unistore opportunity; $51 billion in Data Science and ML applications; $14 billion in collaboration and Data Engineering; and $10 billion in cybersecurity. Those estimates come from Gartner ( IT ) data from the first quarter of 2022, before generative AI appeared. Consequently, this opportunity may be even more appealing by the time we get to 2026.

The company's strengths

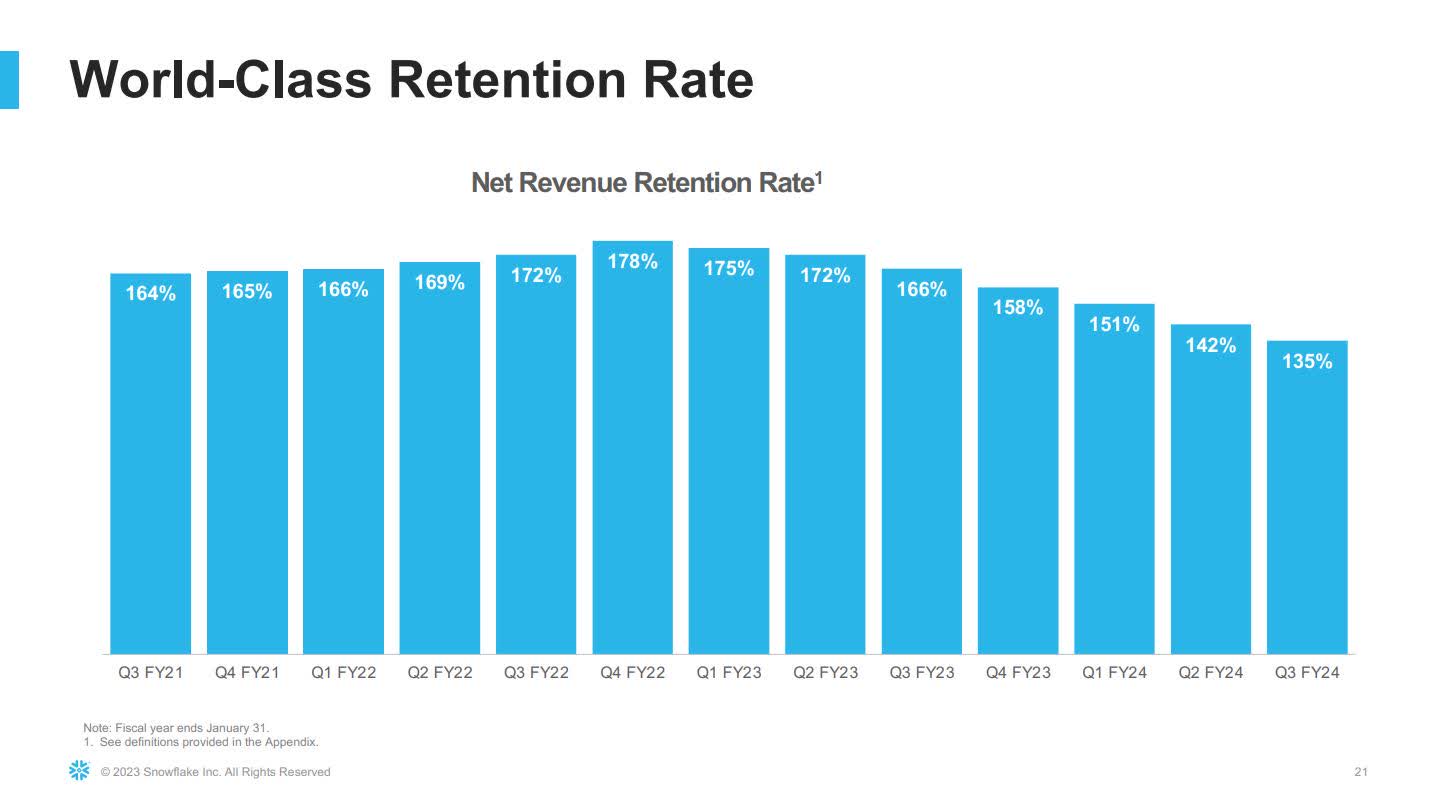

Snowflake didn't invent the concept of a data warehouse or data lake. Nevertheless, it was among the initial companies to bring the data warehouse concept to the cloud, giving it a first-mover advantage. It established itself as a market leader before Amazon's ( AMZN ) Redshift, Alphabet's ( GOOGL ) ( GOOG ) BigQuery, and SAP's ( SAP ) Business Warehouse were able to gain serious traction. A key element of its success was enabling companies to exchange data, which later turned into its Data Marketplace. The more customers use its tools and exchange data on the platform, the more expensive it becomes to leave the platform for another solution. Thus, Snowflake has developed a robust switching cost moat and, to a lesser extent, a network effect moat .

High switching costs come from the time, effort, and cost of shifting company data from Snowflake's platform to another data vendor's platform. There is also the risk that a company could lose or corrupt data by extracting data from one system and adding that data to another. Last, all the time and expense that an organization uses to train employees on Snowflake's platform is lost, and the company must spend money to train personnel on a new data system. Often, once a company joins Snowflake, it rarely leaves. You can measure the strength of this switching cost moat through the Net Revenue Retention Rate ("NRR"). A high NRR indicates a company successfully retaining its customers and generating recurring revenue. Snowflake recently reported that its third quarter NRR was at 135%, an excellent number.

Snowflake Third Quarter FY 2024 Presentation

{kind=link}

Snowflake's network effect comes from partners and customers. One side of its network consists of a massive partner ecosystem. The below image shows its more prominent partners.

Snowflake Third Quarter FY 2024 Presentation

{kind=link}

The other side of the network consists of a growing customer base filled with many notable names, as shown in the below image.

Snowflake Third Quarter FY 2024 Presentation

{kind=link}

The value of Snowflake's platform drastically increases as the number of partners and customers increases. The more partners that join the platform, the more expertise and support will be available to customers, making them more likely to adopt and stick with it. On the other side of the network, as more customers use the platform, they create more data, making it more valuable for other customers to join. Customers covet Snowflake's data-sharing capabilities, as they help them access and analyze data from other customers, providing deeper insights and a competitive advantage.

These competitive advantages prevent larger companies like Amazon from quickly crushing it. Additionally, you can view Snowflake as the Switzerland of Data Platforms, a cloud-agnostic architecture. Customers can host it on the top three cloud providers: AWS, Azure, and Google Cloud. In contrast, some data platforms have tight integration with one specific cloud platform. For instance, Amazon's platform hosts Redshift. Snowflake's multi-cloud flexibility appeals to customers who want to avoid vendor lock-in.

A consumption-based business in the age of Generative AI

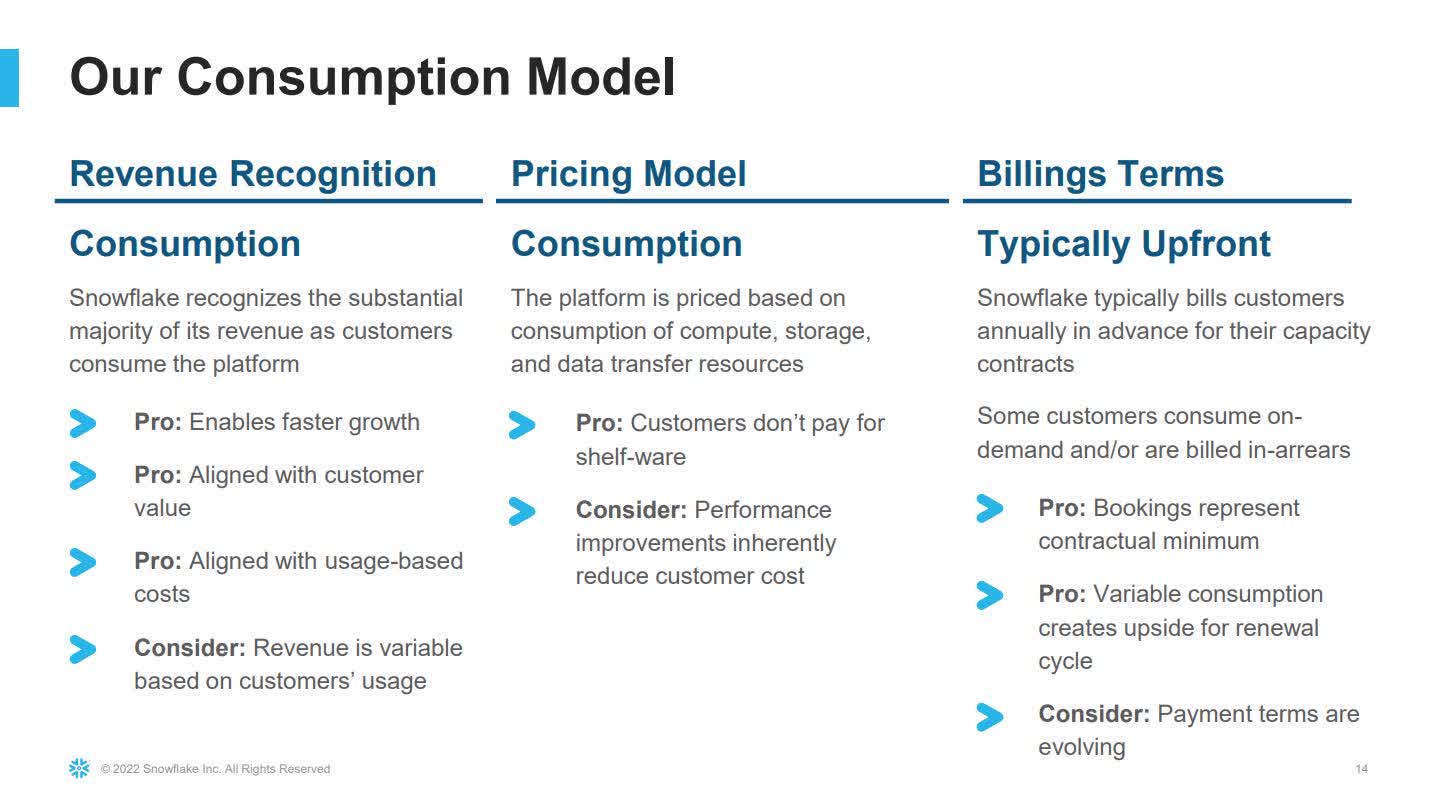

Snowflake is a consumption-based business, meaning the company generates additional revenue the more customers use the platform's computing resources, storage, and data transfer services. Since Generative AI vastly increases customers' computing and data storage needs, demand for Snowflake's services could go through the roof if the technology continues to proliferate and becomes more than a fad.

Snowflake Second Quarter FY 2023 Investor Presentation

{kind=link}

Companies were already gravitating to Snowflake's data cloud solutions before last year. Still, once OpenAI introduced generative AI to the market in late 2022, Snowflake's solutions only became more important. Data is one of the most critical resources in generative AI, the "oil" that fuels powerful AI models. Those AI models run best on heavily refined "oil" and can create biases and incorrect answers when run on crude "oil," which can be extraordinarily damaging to people's lives. Snowflake is like a refinery that optimizes, cleans, and prepares data for advanced machine learning ("ML") and AI models, which has become extremely valuable in the emerging age of generative AI. Imagine John D. Rockefeller, the founder of Standard Oil, who built some of the most technologically advanced oil refineries at the beginning of the oil age; his company, now known as Exxon ( XOM ), achieved massive success -- Snowflake's Chief Executive Officer ("CEO") Frank Slootman is attempting to achieve similar success as a company at the dawn of a new era, the AI age. CEO Slootman said during the third quarter earnings call :

Generative AI is at the forefront of customer conversations, which in turn drives renewed emphasis on data strategy in preparation of these new technologies. We said it many times, there's no AI strategy without a data strategy. The intelligence we're all aiming for results in the data, hence the quality of that underpinning is critical. Meanwhile, Snowflake has announced and showcased the plethora of new technologies that let customers mobilize AI.

Source: Snowflake Third Quarter FY 2024 Earnings Call

CEO Slootman highlighted that one impediment to companies using new technologies like generative AI is " broad access to quality data, " which Snowflake can help with through its data-sharing capabilities. He said, " 28% of all our customer share data, up from 22% a year ago and 73% of our $1 million-plus customers are data sharing up from 67% a year ago. "

Even though many of Snowflake's existing products can help in generative AI applications, the company is doubling down on the proliferation of the new AI technology. At Summit 2023 in June, management announced Snowpark Container Services, which allows developers to run complex data-intensive applications, such as machine learning and artificial intelligence models, directly alongside their data in Snowflake. Snowflake's June press release on its new container services states:

At Summit, we announced Snowpark Container Services (private preview), which enables developers to effortlessly register and deploy containerized data apps using secure Snowflake-managed infrastructure with configurable hardware options such as accelerated computing with NVIDIA GPUs. This additional flexibility drastically expands the scope of AI/ML [machine learning] and app workloads that can be brought directly to Snowflake data.

Source: Snowflake press release

Snowflake's management also announced plans to make it much simpler for its customers to securely access large language models (LLMs) from their Snowflake accounts. LLMs are generative AI models able to understand and generate human-like language. Snowflake will initially support LLMs from three companies: AI21 Labs, Reka, and NVIDIA's ( NVDA ) NeMo framework . Customers will soon be able to find these LLMs on the Snowflake Marketplace. Expect the new product announcements at Summit 2023 to become a growth catalyst in fiscal 2025 (calendar year 2024).

{kind=link}

The company has also recently been on the hunt for any company that can improve its ability to extract data or increase its AI capabilities for customers. Snowflake's most recent acquisitions are Neeva, Streamlit, and Applica. Neeva is a search company that utilizes generative AI and other technologies to give users a more powerful search engine to discover hidden patterns and insights within data. Management plans to integrate this AI-powered search engine into its Data Cloud. Streamlit is a platform that developers can use to build generative AI apps. Applica is a Polish-based AI platform specializing in document understanding. In a press release , Snowflake said about the company, " With this acquisition, Snowflake's customers will be able to more easily leverage unstructured data in the Snowflake Data Cloud. " This acquisition should improve Data Cloud users' ability to extract data from unstructured documents like PDFs, emails, and contracts. Investors should not be surprised if the company makes additional bolt-on acquisitions to increase its ability to support AI applications.

The short-term looks brighter

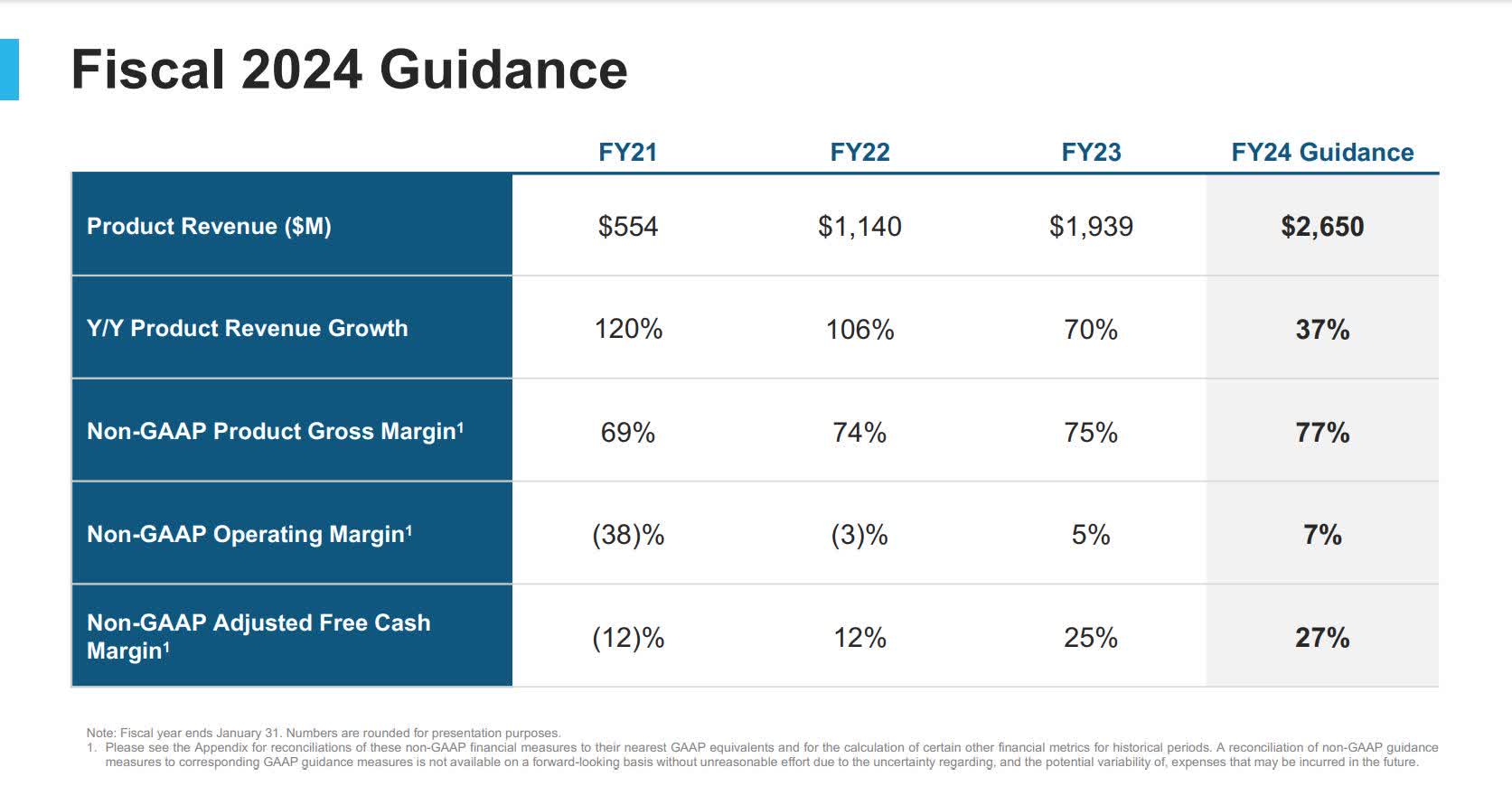

Snowflake recently reported earnings on November 29, and investors were pleased with the results. The company beat top and bottom-line estimates. More importantly, it increased fiscal 2024 product revenue guidance from $2.60 billion to $2.65 billion due to the improved consumption trends management observed during the quarter. Snowflake generates revenue in two ways: Product Revenue, the recurring revenue generated from subscriptions to Snowflake's cloud-based data platform, and Service revenue generated from professional services and support provided to customers. Snowflake stresses Product revenue since it is 95% of total revenue, and its recurring revenue stream is more critical than the non-recurring revenue from the Service segment.

Snowflake Third Quarter FY 2024 Presentation

{kind=link}

The improved Product revenue guidance and encouraging language from management indicate that the steep drop in Product revenue growth since 2021 may have stabilized. Chief Financial Officer Mike Scarpelli said during the call:

Growth in September exceeded expectations. For three weeks, consumption grew faster than any other period in the past two years. Consumption continued to grow in the month of October. Q3 represented a strong quarter for bookings execution.

Source: Snowflake Third Quarter FY 2024 Earnings Call

Like many other cloud companies, Snowflake has suffered as companies started "optimizing cloud spending" post-pandemic due to a worsening economy. Cloud optimization is not necessarily a bad thing and can often result in increased spending in the long term. However, a poor global economy caused many companies to pull back on spending on consuming cloud resources far more than previous cloud optimization cycles, which hurt all cloud companies, including major ones like AWS and Azure.

The good news is that many cloud companies have recently produced improved results and included language in their earnings calls in the third quarter, indicating that cloud optimization is nearing its end. Snowflake is no exception. CEO Slootman said, "...the exposure to these drastic resets and optimization that we saw earlier in the year is getting less and less with each incremental quarter." So, investors' perception of Snowflake's near-term future has improved, a reason the stock jumped 7% higher the day after it released third-quarter earnings.

Risks

The global economy's health is still a risk factor for the company. If global growth does the unexpected and turns south, it could hurt Snowflake's fundamentals, and the stock would likely underperform the market.

Another risk is competition. Snowflake competes against larger competitors with more resources, like Amazon and Alphabet, and newer, smaller players that could disrupt Snowflake's Data Cloud market. This article explains how open-source start-ups may be more dangerous to Snowflake than AWS Redshift and Google's BigQuery.

Another thing investors should watch out for about this company is its high stock-based compensation ("SBC"). A high SBC can be terrible for investors as it can dilute existing stockholders and reduce profits. It can be even more detrimental for investors in a slowing economy, exacerbating dilution.

Last, Remaining Performance Obligations (RPO) only rose 23%, less than quarterly year-over-year revenue growth of 32%. RPO gauges future revenue growth and can give investors a clue about a company's ability to sustain its growth trajectory. When RPO growth is lower than revenue growth, it suggests a future where the top line is slowing -- bad news. Investors should continue monitoring this metric moving forward.

Should you buy it?

Snowflake generates debate among investors because of its valuation. The company currently has a nosebleed one-year forward P/E ratio of 168.76, far exceeding the 41.39% earnings-per-share growth analysts expect at the end of the 2025 fiscal period. It has a P/S ratio of 23.66, a valuation that even exceeds CrowdStrike and Datadog. No matter what traditional valuation ratio you use, the stock's valuation looks excessive.

One of the few ways of valuing Snowflake where one can come up with an acceptable valuation that is not totally at nosebleed level is by using a discounted cash flow ("DCF") model. Suppose that the company will achieve its goal of 30% free cash flow ("FCF") margins by 2029. When I plug the following numbers into a DCF calculator: a terminal growth rate of 2%, a discount rate of 10%, and a growth rate of 29.5%, the estimated stock value equals $220.58.

Snowflake DCF

| Today's reported Free Cash Flow TTM at 26.45% margin (Trailing 12 months in millions) |

| $693.5 |

| Free Cash Flow TTM assuming a 30% margin (Trailing 12 months in millions) |

| 786.3 |

| Terminal growth rate |

| 2% |

| Discount Rate |

| 10% |

| Years 1 -10 growth rate |

| 29.5% |

| Current Stock price |

| $188.30 |

| Estimated Intrinsic value |

| $220.68 |

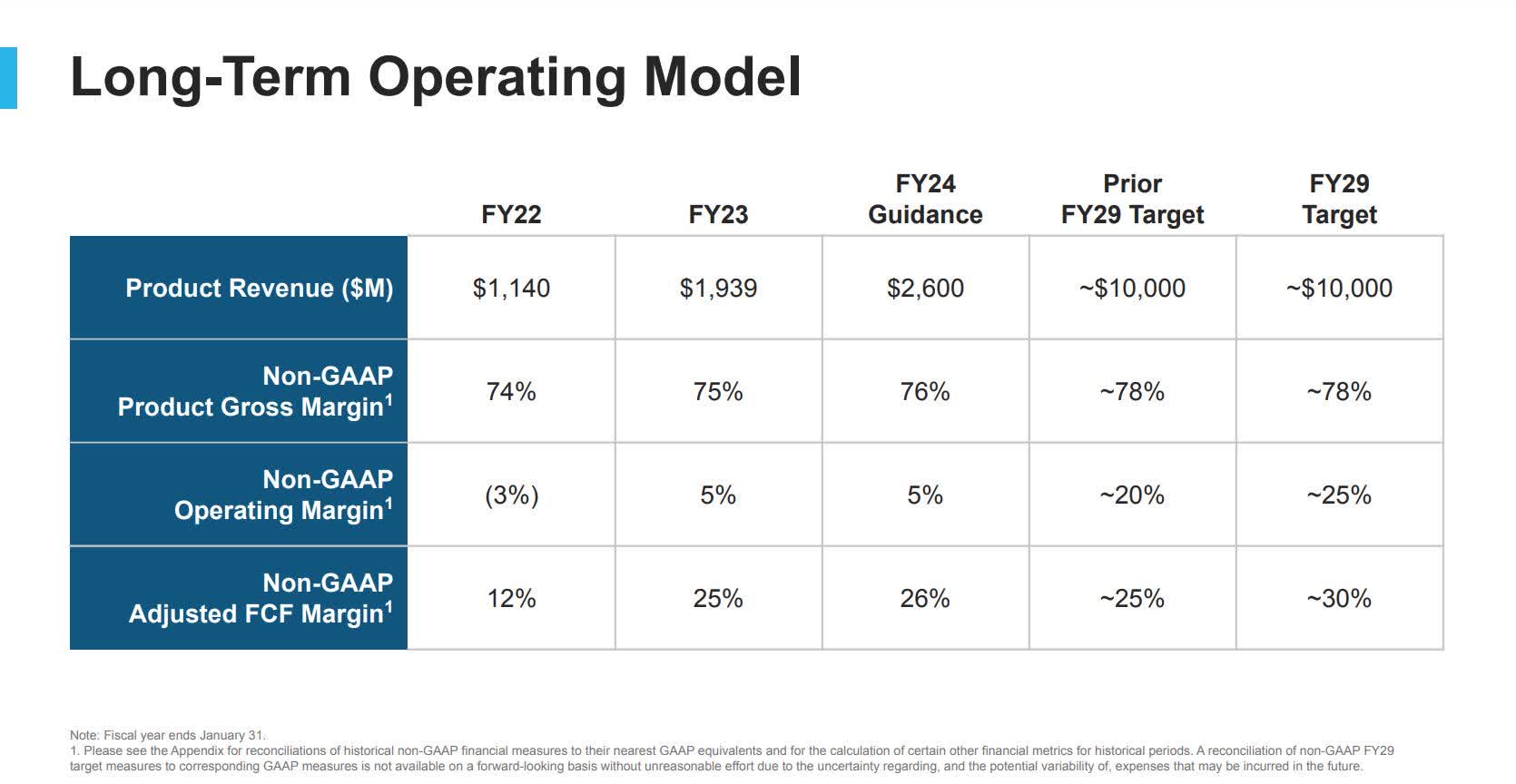

Only long-term investors should consider buying, as at current prices, the story could take multiple years to play out. An FCF growth rate of 29.5% annually over ten years is a very aggressive assumption. The above DCF assumes the company can hit its long-term guidance goals, mainly Product revenue and Adjusted FCF.

Snowflake Third Quarter FY 2024 Presentation

{kind=link}

Analysts forecast Snowflake's revenue to grow +30% annually for the next several years. It has a first-mover advantage in a large and growing data industry, has established a powerful moat against competition, and has solid customer growth. Yahoo Finance shows analysts predicting earnings-per-share growth over the next five years of 66.60% . While it is far from a bargain basement stock, aggressive growth investors can buy Snowflake at current prices and have a reasonable belief that it still has a decent potential upside. I rate Snowflake a Buy for aggressive growth investors.

For further details see:

Snowflake's Data Marketplace: The Key To Unlocking The Potential Of Generative AI