SNOW - Snowflake: Stellar Revenue Growth But Valuation Is Too Generous

2023-11-03 13:59:51 ET

Summary

- Snowflake's stock has underperformed the broader market, but the company continues to show strong revenue growth and investment in R&D.

- The gross margin has not expanded despite revenue growth, indicating a potential ceiling for this metric.

- The stock is overvalued based on ratios analysis and discounted cash flow, and the current Fed's hawkish stance does not favor growth companies.

Investment thesis

Since my initial cautious thesis about Snowflake ( SNOW ), the stock substantially underperformed the broader U.S. market over the last six months. The company continues demonstrating stellar revenue growth and invests substantial funds in R&D, which is a strong sign that the management is committed to building long-term value for shareholders. On the other hand, the gross margin demonstrated almost no expansion in recent quarters despite massive top-line growth, which might indicate that SNOW achieved its ceiling in terms of this metric. The valuation is far from being attractive based on both ratios analysis and discounted cash flow. Moreover, the current Fed's hawkish stance does not favor growth companies that have not achieved sustainable profitability. That said, I reiterate my cautious "Hold" rating for SNOW.

Recent developments

The latest quarterly earnings were released on August 23, when the company topped consensus estimates. Revenue demonstrated solid growth momentum with a 35.6% YoY increase.

Seeking Alpha

Despite massive revenue growth in recent quarters, the gross margin is not improving much as it is dancing around the 65% to 68% range. This might indicate that SNOW achieved its ceiling in terms of the gross margin, which can become a disappointing factor for investors if the metric continues to stay flat despite massive revenue growth. The operating results did not improve much on a YoY basis either. However, it is important to underline that the SG&A to revenue ratio is declining, and the portion of sales reinvested in R&D has expanded in recent quarters. This indicates a strong commitment to innovation, which is a good signal for long-term investors.

The company's levered free cash flow [FCF] ex-stock-based compensation [ex-SBC] is still negative. I do not see a big problem here, as SNOW has a substantial net cash position of $4.5 billion with almost no leverage. That said, I think that the company is very firmly positioned to continue investing substantial funds into innovation to fuel massive revenue growth.

Seeking Alpha

The upcoming quarter's earnings are scheduled for release on November 29. Quarterly revenue is projected by consensus at $713 million, indicating a 28% YoY growth. The strong revenue growth momentum is a solid positive sign for investors. However, there is an apparent trend for revenue deceleration as the business scales up. Despite sequential revenue growth, the adjusted EPS is expected to decline QoQ from $0.22 to $0.16.

Seeking Alpha

Despite demonstrating stellar revenue growth during the latest earnings call, the management acknowledged that the company operates in a challenging environment due to multiple macro headwinds. I agree with that, as it looks like the Fed's tight monetary policy is starting to work. Last week's big tech earnings disappointed the market, mostly due to cautious near-term guidance rather than the latest quarter's performance. That said, there is a high probability that SNOW might also deliver stellar revenue growth in the upcoming quarter's earnings release, but the management's guidance for the foreseeable future might be cautious.

The current environment of high-interest rates and large corporations seeking efficiency does not favor growth companies like SNOW either. The Fed's monetary policy is still tight, with interest rates at their multidecade highs , which weighs on business spending. Therefore, I see no positive catalysts for SNOW in the near future.

Now let me switch to looking at the stock from the secular standpoint. The company operates in a promising cloud-based data analytics industry, which is expected to compound at 23% in the next couple of years. I believe that the industry's growth prospects for the years beyond are also bright as the shift to greater digitalization and deeper business analysis is apparently secular. Cutting-edge artificial intelligence technologies add more options and opportunities to expand the depth and quality of data analysis, which is also a solid secular tailwind for companies like SNOW. I like that the management recognizes the need to invest and expand to the AI field. This is evidenced by multiple AI innovations announced during the company's latest Snowday 2023 event.

SNOW's latest quarterly presentation

{kind=link}

It is also crucial that Snowflake is building an entire ecosystem of multiple solutions for its extensive customer database, which makes the company well-positioned to fuel revenue with upselling and cross-selling opportunities. Striving to make SNOW a comprehensive one-stop-shop for data analysis is also likely to build long-term value for shareholders. Having strong cross-selling opportunities also means that customer acquisition costs are poised to go down as the network expands, which is also a solid long-term bullish sign.

SNOW's latest earnings presentation

To conclude this part, I recognize the company's solid long-term bright prospects and the management's strong commitment to innovation and building an extensive ecosystem of multiple solutions, which will likely drive up customer retention and the long-term value of each customer. However, over the short term, sentiment prevails in the stock market, and that is the main reason I am still cautious about SNOW from a tactical perspective.

Valuation update

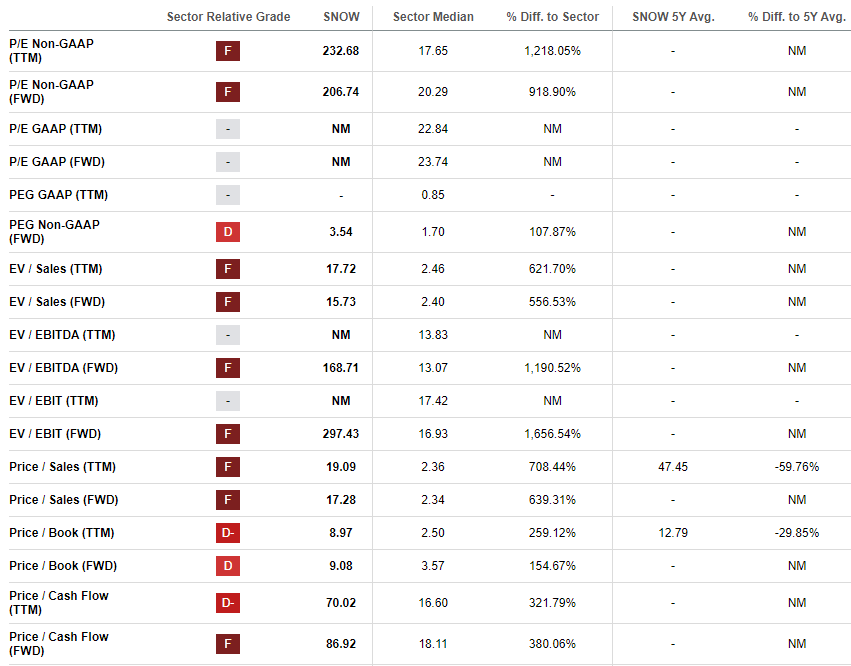

The stock price rallied by slightly more than 5% year-to-date, which indicates a notable underperformance compared to the broader U.S. market. Seeking Alpha Quant assigns the stock with the lowest possible "F" grade, meaning the stock is substantially overvalued based on the ratios analysis. Given SNOW is an aggressive growth company, I am okay with substantial P/E ratios. However, the company is valued at more than 17 forward sales, which apparently is a clear indication of a substantial overvaluation.

{kind=link}

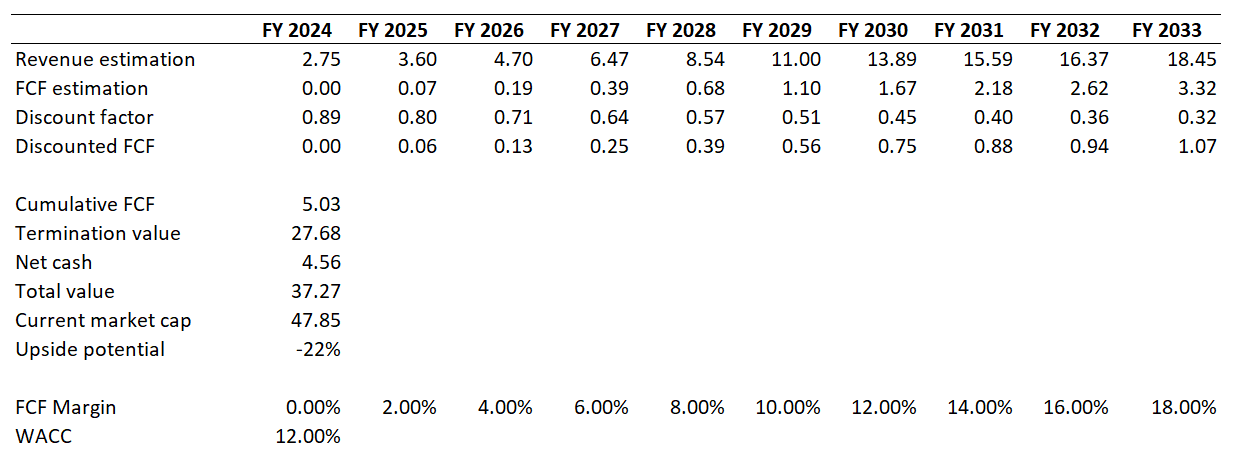

I need to simulate one more approach to get more confidence. For growth companies, I use discounted cash flow [DCF]. I use an elevated 12% WACC for discounting due to the recent hawkish Fed's rhetoric indicating higher interest rates for longer. I use long-term consensus revenue estimates projecting about 24% CAGR for the next decade, which I consider a bit optimistic. I use a zero TTM FCF margin for the base year and expect a two percentage points yearly expansion.

{kind=link}

According to my DCF simulation, the business's fair value is about $37 billion. This indicates a substantial 22% overvaluation, meaning that my target price for SNOW is around $110.

Risks to my cautious thesis

The U.S. stock market has been highly volatile recently because the American economy sends mixed signals to investors. While in his latest press conference, Jerome Powell has been hawkish , the environment is changing very rapidly. We live in a massive globalization era, and the U.S. monetary policy depends on numerous factors outside of the Fed's control. That said, there is no guarantee that the next press conference will still be hawkish. There is a high probability that even slight dovish signals from the Fed will be enough to be a strong catalyst for aggressive growth stocks like Snowflake.

Snowflake currently trades at less than half of its all-time high values of late 2021, which might be the signal to buy for some investors. Sometimes investors tend to overreact to quarterly earnings, and it works in both positive and negative ways. That said, in case the nearest earnings release is considered strong by investors, this might be a solid catalyst to make SNOW a big upward mover with double-digit intraday growth.

Bottom line

To conclude, SNOW is still a "Hold" to me. My valuation analysis suggests that the stock is substantially overvalued, which is a huge red flag amid the current Fed's hawkish stance. Moreover, I would like to look at how the next few quarters will unfold because profitability metrics demonstrate mixed signals as the gross margin struggles to expand notably despite a staggering YoY revenue growth in multiple recent quarters.

For further details see:

Snowflake: Stellar Revenue Growth, But Valuation Is Too Generous