SNOW - Snowflake Stock: Outlook As It Shows 'Signs Of Stabilization'

2023-10-19 11:45:27 ET

Summary

- Snowflake stock has experienced significant volatility since its IPO in September 2020, with highs of $429 and lows of $108.

- The company's revenue growth has been slowing, its margins falling, and order book growth is also in decline.

- Despite these unexciting fundamentals, the stock chart suggests institutional accumulation and the stock has the potential to hit a target price of $280 within a year or two.

- We rate the name at Accumulate, but this is not an easy call, as our article explains.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Will Snowflake Stock Rebound?

Snowflake, Inc (SNOW) is an enterprise software company focused on business analytics. The company was founded in 2012 - in the thick of the "Internet 2.0" era - raised a large amount of venture capital funding and went public in September 2020. It was a hugely well-publicized IPO , and since many folks forget that an IPO is an exit event for prior investors, many rushed to buy the stock. Providing exit liquidity to longtime institutional holders in a selling frenzy isn't usually a great idea, and unless those who bought the IPO got out as the stock ran up, they have been left holding a rather heavy bag of stock certificates.

The IPO was "priced" at $120/share, meaning, if you were an institutional buyer able to acquire stock before trading started, you paid in the vicinity of $120/share. The stock began trading at $245 - a nice one-day markup if you could get it! - and peaked at $429 in December 2020. A drop to $184 by May 2021 followed, and then a final run-up to $406 in November 2021 marked the top of the hype cycle. Whether institutional investors could realize their gains at those peaks would depend on any lockup provisions to which they had agreed, but there's every chance that the 2021 highs provided further exit liquidity for the bigs (since it was over a year past the IPO). Unusually for growth stocks, the name did not make a new high in 2021; once that $406 was struck, the market turned, and down came the house that Frank built . The stock hit its lows at around $108 in June 2022 and has since trended somewhat sideways in a range-bound fashion, for the most part between around $120-190/share.

So what, you may ask. Just another overhyped tech stock. Move on.

Well, you may be right, but before you leap to that conclusion, let's take a look at the earnings progression, and let's look at the stock behavior of late to try to figure out whether Snowflake stock can rebound.

SNOW Earnings Review

The company has a January 31year end, so quarter ends are July 31, October 31 and so forth. Last quarter, Seeking Alpha noted the sellside community talking about the "green shoots of recovery" following "stabilization" in usage stats for the company's analytic applications.

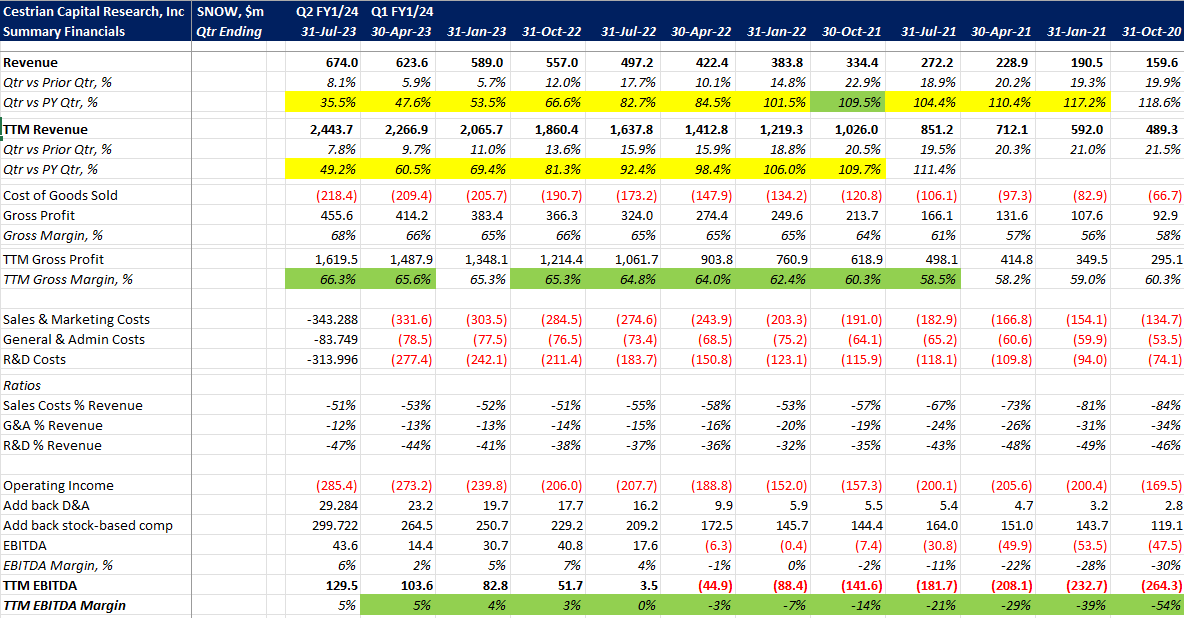

Here's the numbers up to and including the most recently reported quarter. Firstly, revenue down to EBITDA.

SNOW Fundamentals I (Company SEC filings, YCharts.com, Cestrian Analysis)

{kind=link}

The key points to us are:

- Recognized revenue growth has been slowing fairly dramatically, from over 100% pa. as recently as the January 2022 quarter to just +36% pa. in the July 2023 quarter. TTM revenue growth - a slower-burn measure of course - has now dropped to 49% pa.

- Gross margin has ticked up somewhat, to 66% on a TTM basis from around 60% at IPO time. This is low for a software company and reflects the degree of pay-away to third party cloud vendors required to host the 'data lake' model they operate. Low gross margin matters because it caps the potential cashflow margins at which the company can ever operate.

- EBITDA margins were heavily negative at IPO time - more than 50% in the red - but have trended up to +5% on a TTM basis lately. Note there was no improvement in TTM EBITDA in the July 2023 quarter, the first time since IPO that this measure of profitability did not improve each quarter.

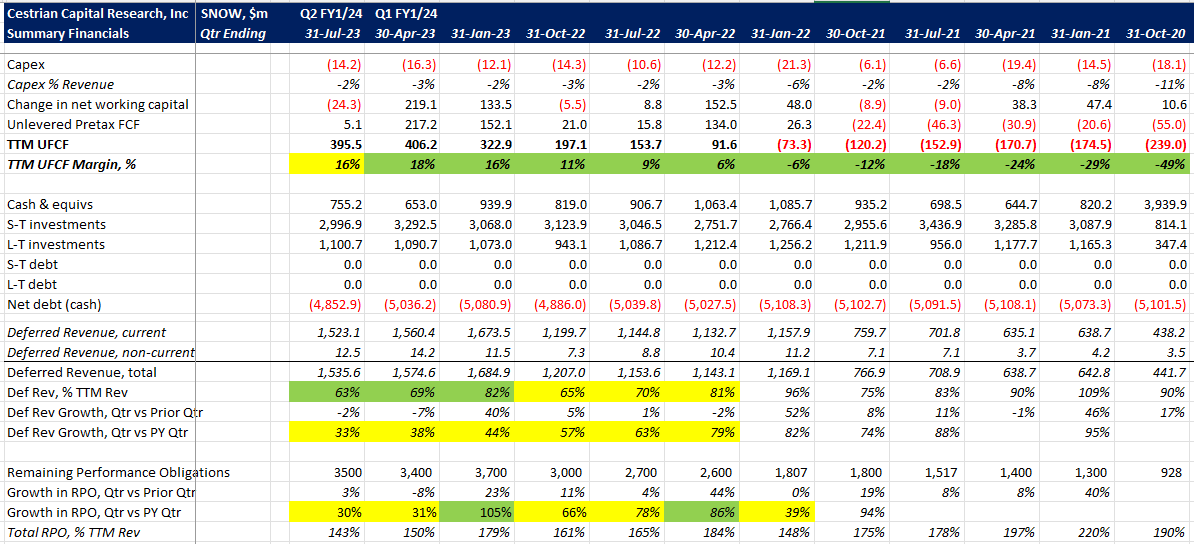

Let's now look at cashflow, the summary balance sheet, and the order book in the form of remaining performance obligations (RPO).

SNOW Fundamentals II (Company SEC Filings, YCharts.com, Cestrian Analysis)

{kind=link}

The first thing to note here is that cashflow margins run ahead of EBITDA margins, and that is because the company has an upfront billing model. At +5% TTM EBITDA margins the company also has +16% TTM unlevered pretax free cashflow margins. This is a good thing, a sign that the company has some power in its supply chain. If you look at that change in net working capital line, you see that for the most part the company sees a cash inflow from working capital each quarter. And in the simplest of terms what that means is that the company collects cash from its customers before it provides service, and pays its suppliers (including staff of course) after it receives service. Which means that it has power over both its customers and its suppliers - a hallmark of a high quality business. That said, TTM UFCF margins dropped in the most recent quarter, as did TTM EBITDA margins, and as per TTM EBITDA margins this is the first quarter in which that happened since IPO. So you would have to say that at present it looks like the company is spending more to grow less, never a good look.

Next - remaining performance obligation (RPO). RPO is the total order book the company holds - the totality of all customer contracts that have been signed but have not yet been delivered. On the plus side is the size of the order book, which stands at 1.4x TTM revenue - that's a lot of revenue stored up for the future. But growth in the order book has stalled; it was down 8% sequentially from January to April and then up just 3% sequentially into the July quarter. RPO was up 30% on the year, which means it is growing more slowly than recognized revenue - and that's not a good look either. What you want in these high-visibility-revenue subscription software companies is a fat order book vs. the TTM revenue number (tick) and then the RPO growing faster than recognized revenue. Because then you have the ingredients for future acceleration in revenue growth and that is a potential upward catalyst for the stock price. Here though the look is that revenue growth may continue to slow. Not definitely - the relationship between the order book and revenue recognition is not linear - but it's a real possibility. So this is a downside risk for the stock. (There's no salve either from deferred revenue, which is the portion of RPO which has been invoiced already - that is showing similar slowing trends).

The balance sheet is positively swimming in net cash, around $3.8bn of cash and cash equivalents plus short-term investments. There is no debt. This is good, but it's doing nothing. The company ought, in our view, to be putting that huge cash pile to work. They could have acquired companies for cash at the market lows last year (our preferred use of cash) or they could be handing it back to shareholders by way of dividends (which is usually a negative stock price catalysts for growth names because it signals a failure of management imagination as to how to accelerate growth). But just sat there? Not so smart in our view.

Is SNOW Stock A Buy, Sell, Or Hold?

You can see that the fundamentals are unexciting. Yes, the company may accelerate this coming quarter, margins may tick up, RPO may grow quickly, anything can happen. But the numbers we see before us right now don't tell that story. To judge whether SNOW stock is a buy, sell, or hold, let's look at the valuation multiples in the light of that fundamental performance, and then take a look at the stock chart.

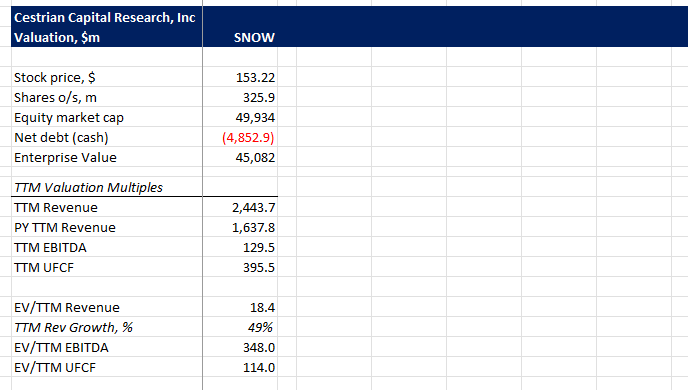

SNOW Fundamental Valuation Multiples (Company SEC Filings, YCharts.com, Cestrian Analysis)

{kind=link}

The market is asking you to pay 18x TTM revenue for a company presently growing at +49% pa on a TTM basis and +36% pa on a quarter-on-quarter basis. It's a profitable and cash generative business, but the margins are low and so the EBITDA and cashflow multiples are huge.

So why bother with this stock?

The answer lies in the stock chart, we believe.

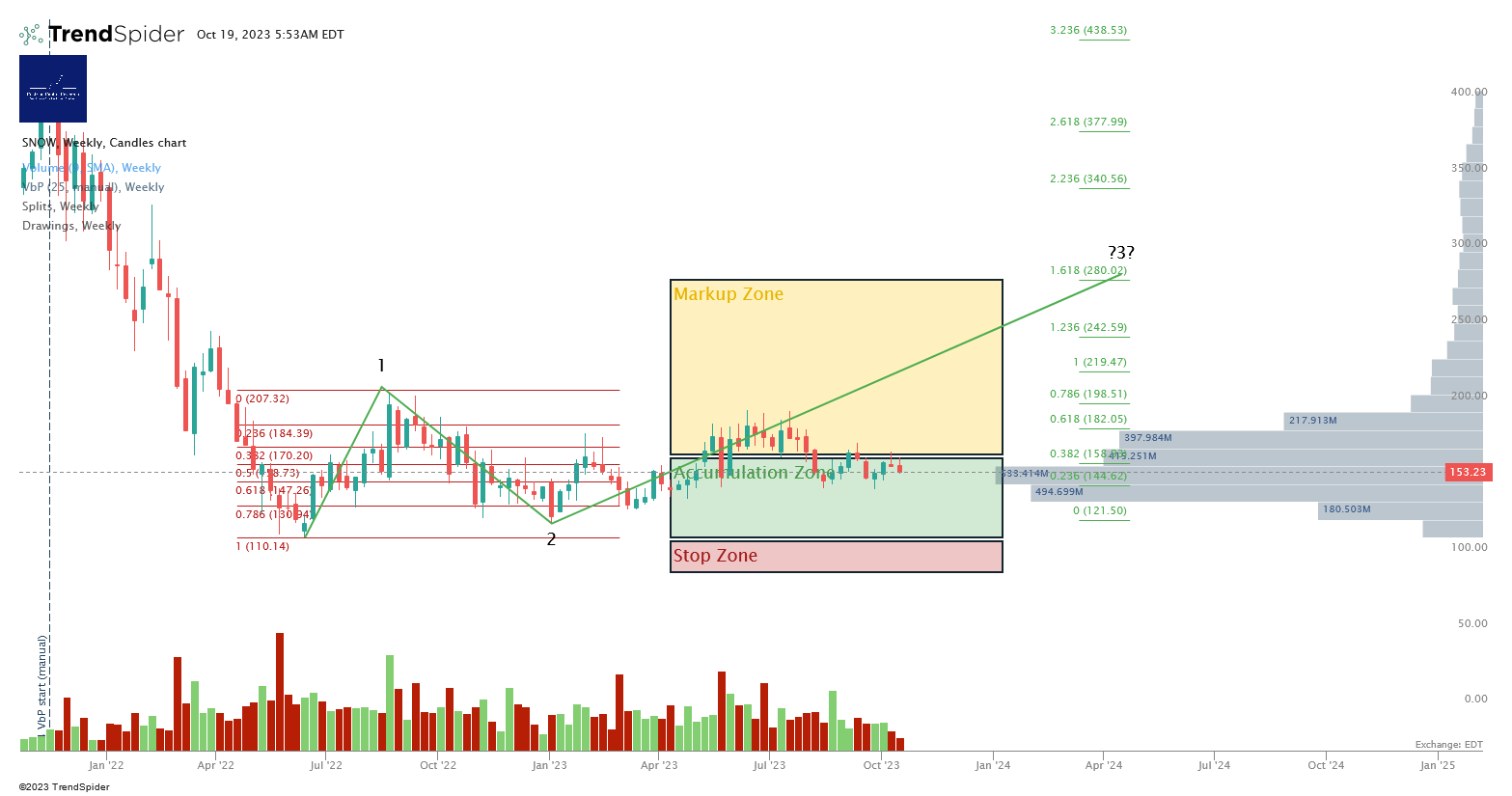

{kind=link}

The chart above shows SNOW from its 2021 peak. The gray bars on the right hand side show volume by price, and the clock on that starts at the 2021 highs. So the first thing you can see is that there was hardly any volume as the stock plummeted. In fact were you to look back to IPO time you would see very little volume up there at the highs - meaning only a few investors, likely retail given the low volume - were buying up there. Once the stock bottoms in June 2022, you see an initial Wave 1 impulse upwards, peaking at $230 in August 2022, then a Wave 2 correction that drops a little below the .786 Fibonacci retracement level in November 2022 and re-tests that level in January 2023. At which point the stock starts to drift upwards and with major increases in volume too. So what we have from around April 2022 to date is sideways, rangebound action at the lows, at high volume. And that is characteristic of institutional accumulation; slowly building positions without doing so too aggressively, lest the price run away to the upside.

Our best guess with SNOW is that the stock continues to move up. The context for that view is that we believe we are in a sustainable bull market - we wrote up our views on that recently here . Probably not banzai-up, no big dramatic moment, but gradually up. Based on that volume x price profile, which tells you the most likely price zone in which the bigs are buying, we believe the stock justifies an 'Accumulate' rating between $110-170, with the heaviest buying (so lowest risk) in the $130-$170 range. Above $170 we believe the stock is moving into our 'Markup' zone - this is where late money arrives! - and so over $170 we rate at Hold. If the company fundamentals do start to improve - per those green shoots above - and the market is supportive, we believe the stock can reach $280 within say a year or two. Risk management? With volatile names like this it can be risky to place stops too close to your entry point, so you have to decide how much downside you are prepared to risk in pursuit of that upside. Certainly if the stock were to drop below that $118 Wave 2 low, something bad has happened and you may well want your money back at that point. If you prefer to use trailing stops, be aware that names like this one can easily swing around 10% on any given day, so be careful to not have that stop hunted out only for the stock to reverse back upwards. As always with these high beta names, they aren't easy - but if they were, anyone could make the big bucks and as we all know, that's not how the market works!

Accumulate rating subject to all the above. If you just skipped to this part ... do read the article in full, because this isn't an easy call.

Cestrian Capital Research, Inc - 19 October 2023.

For further details see:

Snowflake Stock: Outlook As It Shows 'Signs Of Stabilization'