SNOW - Snowflake: Take Advantage Of This Dip To Buy A Category Leader

2023-10-01 02:54:57 ET

Summary

- Snowflake stock presents a buying opportunity due to reduced valuation and strong long-term growth potential.

- The company is well-positioned to benefit from cloud adoption and data volume growth. Its consumption-based business model may be a headwind now, but unlocks tremendous growth in the future.

- The company has nearly $5 billion of cash on its balance sheet, improving its financial flexibility.

With the sharp correction in the broader markets over the past few months, investors have been running away from tech stocks like the plague. But in spite of high risk-free interest rates, I think it's a great opportunity to buy into the shares of iconic, high-quality software businesses while pessimism is high. A multi-year investment horizon is key here: it may take throughout most of next year for interest rate fears to quell and for macro pressures to subside. But strong companies with excellent production traction and category leadership will be able to power through the current macro crunch and deliver terrific results in the long run.

Snowflake ( SNOW ) is one great stock to look into that checks off all these boxes. The cloud data warehousing company is up this year, but only in-line with the S&P 500 and lagging behind most other tech companies. And versus 2021-era highs notched near $400, Snowflake is still trading at a fraction of its former worth.

I'll cut to the chase: I am bullish on Snowflake, considering this stock's once-heavy valuation premium has been reduced to much more normalized levels. I recommended buying Snowflake last year when the stock was trading in the ~$170s; I'm using the recent dip as an opportunity to buy more.

To me, Snowflake's product has never been more relevant: as more companies move technology assets into the public cloud and as data volumes themselves explode, the company will be able to continue chasing tremendous growth rates.

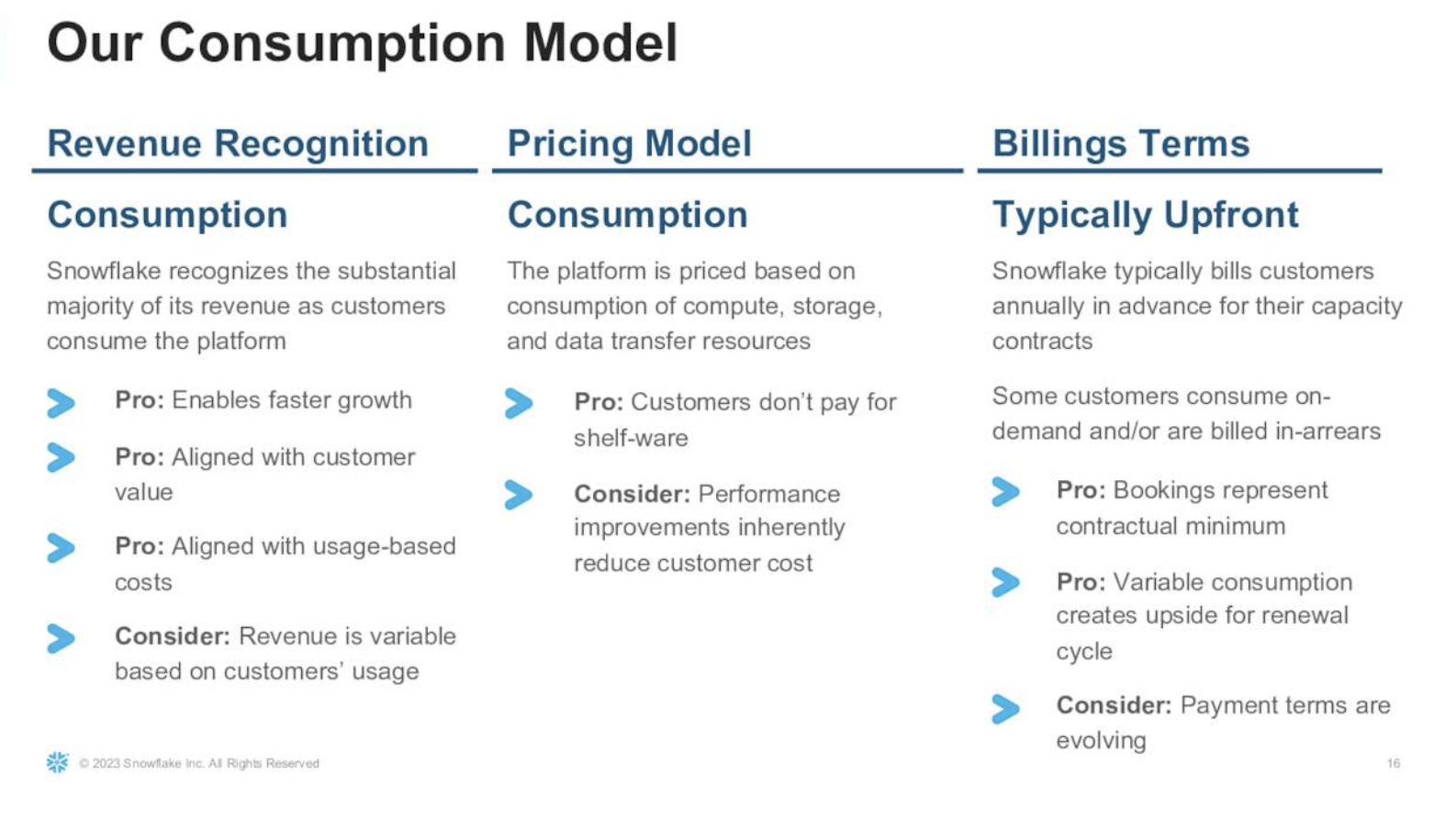

Of course, 2023 threw Snowflake's growth trajectory temporarily off. As a reminder for investors who are newer to Snowflake, unlike many other software companies, Snowflake generates revenue on a consumption basis instead of subscription. This means that during a macro downturn when its customers are ingesting less data, it will also generate less revenue (unlike a subscription product where the same monthly fee is charged regardless of usage rates).

Snowflake business model (Snowflake Q2 earnings deck)

{kind=link}

In turn, however, when macro conditions rebound and usage picks up steam, Snowflake will also rebound faster than subscription-based businesses.

I'd focus on the long-term bullish drivers here, which to me include:

- Secular tailwinds in both cloud adoption and data volume growth. Snowflake straddles two important trends in computing: moving of technology assets into the cloud, as well as data volumes exploding as companies seek to understand everything they can about their customers. Snowflake's usage-based pricing model helps the company to capture tremendous upside here.

- Large TAM. Snowflake estimates its overall cloud data platform TAM at $248 billion, suggesting that at its current scale, Snowflake is only single-digit percentage penetrated into this market.

- Massive gross margin profile leading to a highly scalable business. Snowflake captures an ~80% pro forma gross margin on its product revenue, which means nearly every dollar of incremental revenue flows to the bottom line. The company is still growing at a >30% clip, enabling it to achieve enormous scalability down the road as opex shrinks as a percentage of revenue.

- Enterprise focus. Snowflake has over 400 customers that generate more than $1 million in ARR. The company's blue-chip brand profile and its sales focus on large customers helps to stabilize its revenue base, even in a macro downturn.

- Cash-rich balance sheet. Snowflake has nearly $5 billion of cash on its books against no debt, which enables tremendous financial flexibility to chase growth opportunities.

Stay long here and use the dip as a buying opportunity.

Q2 download

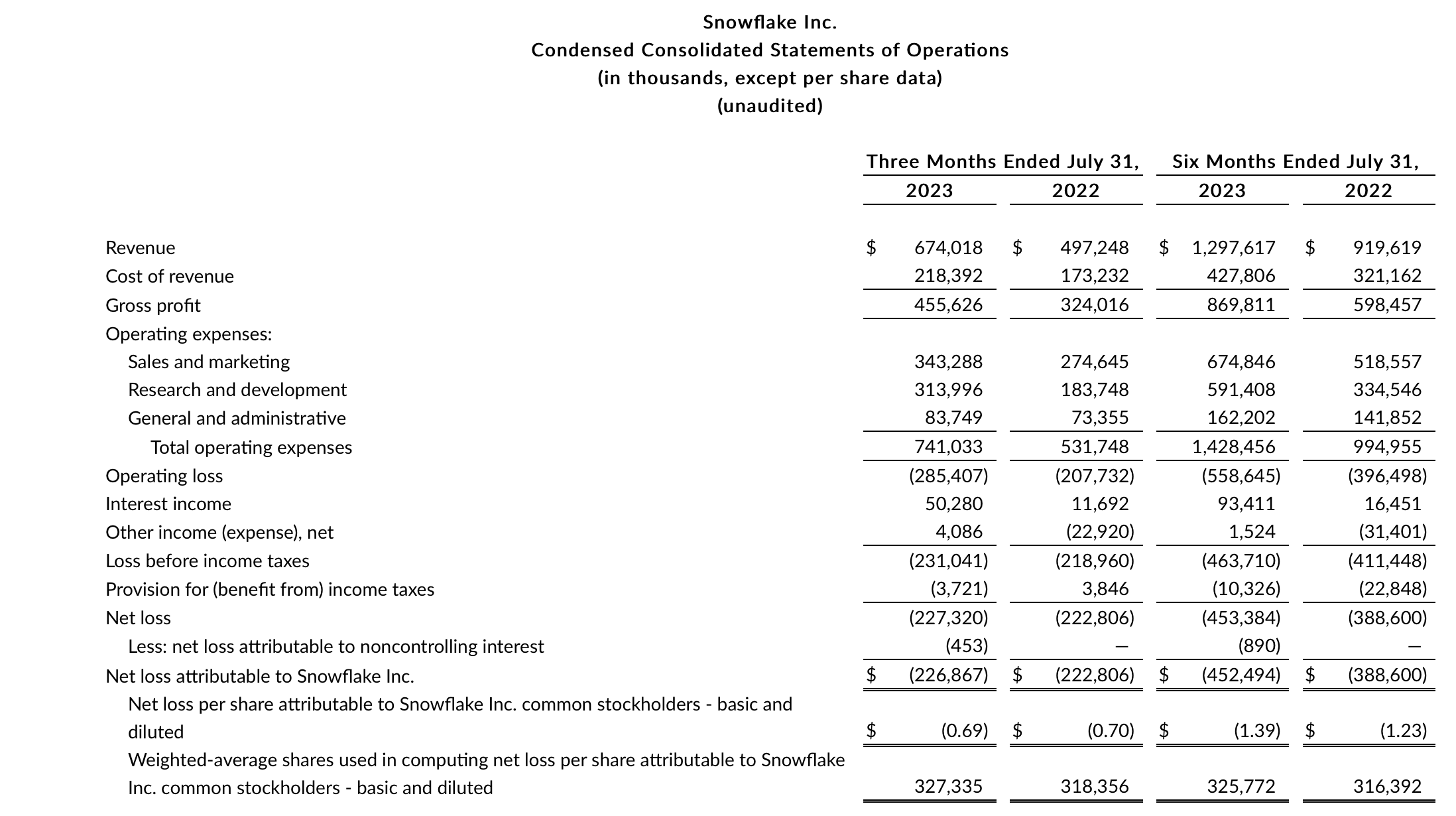

Snowflake's most recent trends showcase a business that is still chugging along and executing new deals and upselling existing clients, even in spite of softer macro conditions and slower usage rates. Take a look at the Q2 earnings summary below:

Snowflake Q2 results (Snowflake Q2 earnings deck)

{kind=link}

Snowflake's Q2 revenue grew 36% y/y to $674.0 million, ahead of Wall Street's expectations of $662.3 million (+33% y/y). Of course, Snowflake's growth rates do mark considerable deceleration from prior trends: Q1 growth had clocked in at 48% y/y and Q4 at 53% y/y; in FY22 (corresponding to most of calendar 2021), Snowflake had grown revenue at just over a >2x y/y pace.

Lower consumption, of course, is the culprit here: but the company does believe that consumption trends have inflected and reached a stabilization point. Per CFO Mark Scarpelli's remarks on the Q2 earnings call :

Consumption came in line with our expectations for the quarter. In May, we saw a return to growth with strength continuing into June and July. From a booking standpoint, we saw promising signs of stabilization with new bookings outperforming our expectations. However, we believe, productivity has room for further improvement."

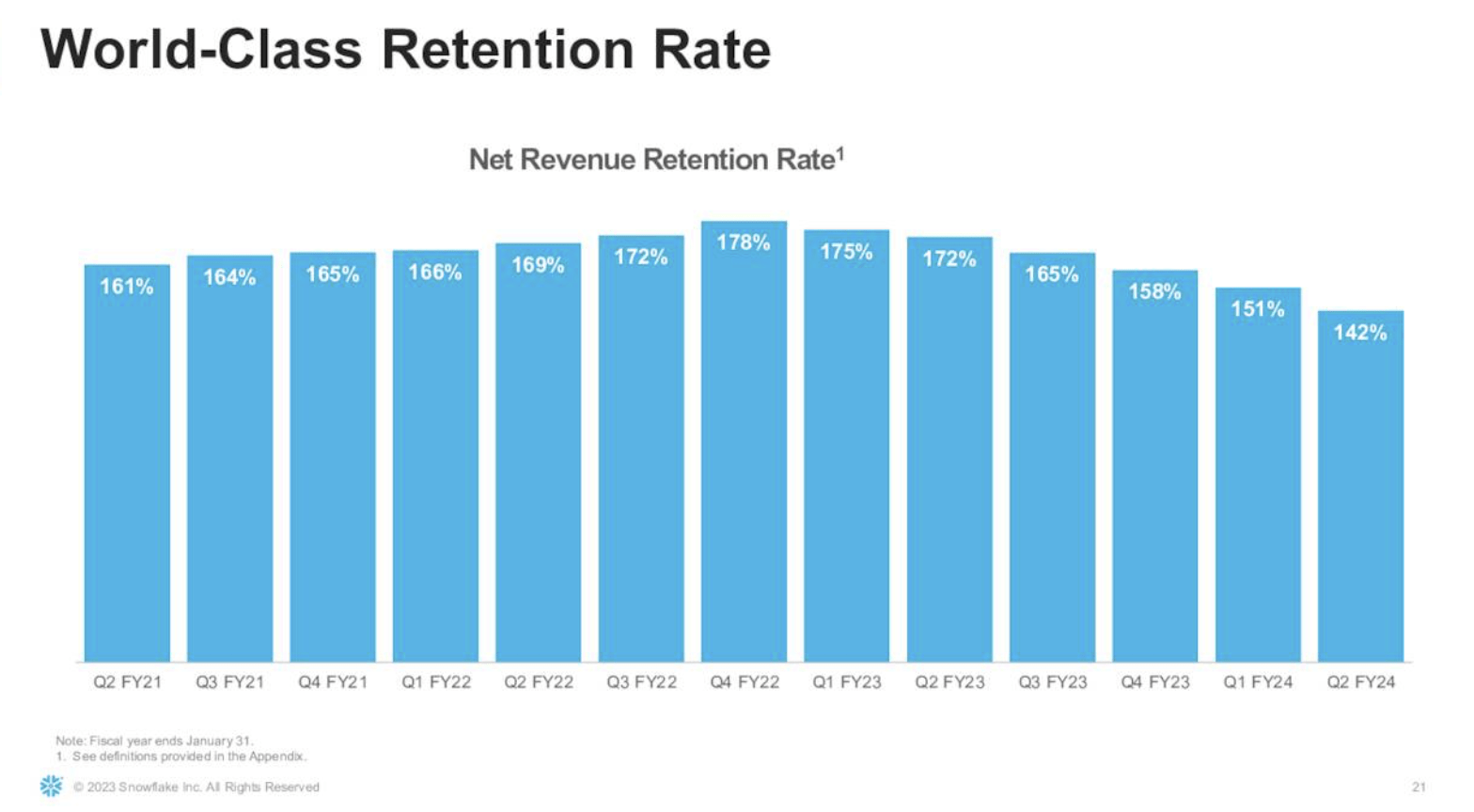

We note that in spite of lower usage rates, the company still managed to notch incredibly high net revenue retention rates of 142% in the most recent quarter.

Snowflake net retention rates (Snowflake Q2 earnings deck)

{kind=link}

Though a slowdown from prior quarters, we note that most SaaS subscription software businesses see retention rates in the 100-120% range, showcasing the power of Snowflake's consumption-based model even in a downturn scenario.

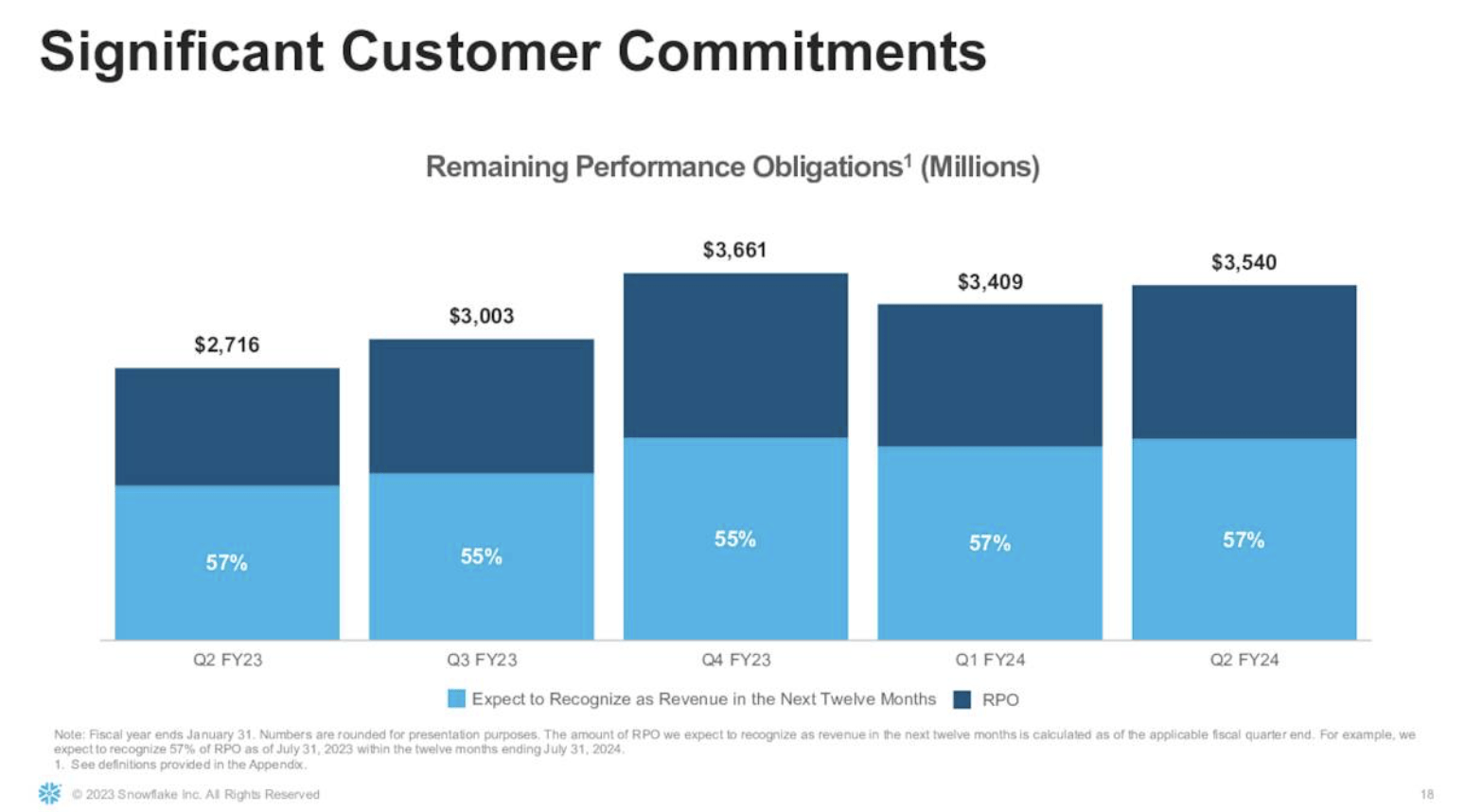

The company also continued to grow RPOs by 30% y/y to $3.54 billion, 57% of which is expected to be recognized as revenue over the next twelve months, indicating a strong backlog and pipeline of future revenue.

Snowflake RPOs (Snowflake Q2 earnings deck)

{kind=link}

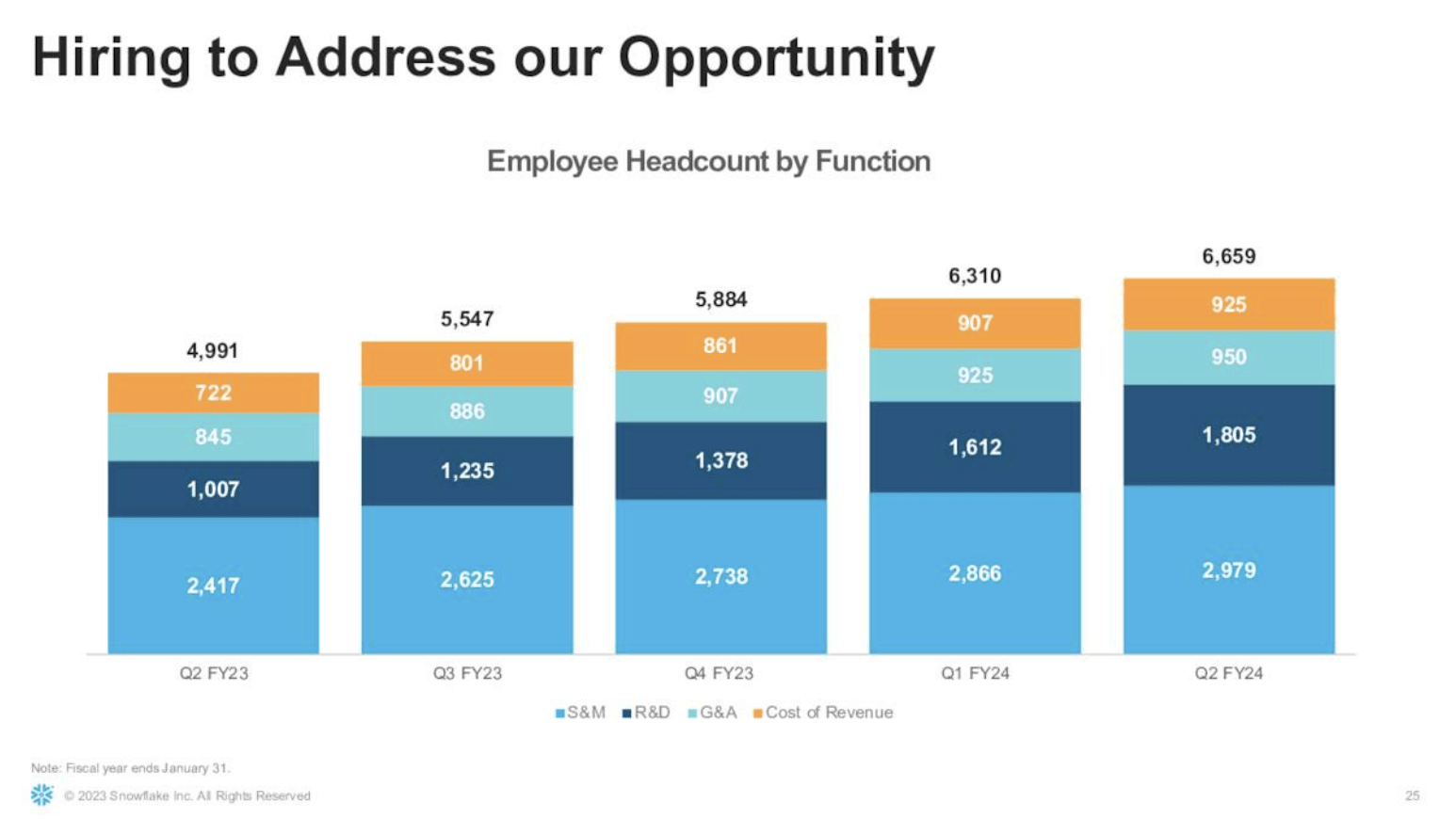

The one area that I'm wary on is headcount and opex. Snowflake's headcount has grown substantially over the past year, primarily in the R&D org which has seen headcount expand by nearly 2x to 1.8k to support AI-based innovation. Many peer software companies, meanwhile, have used the recession as an opportunity to trim headcount or at least slow down the pace of hiring, whereas Snowflake's headcount growth of 33% y/y more or less matches its pace of revenue growth.

Snowflake headcount levels (Snowflake Q2 earnings deck)

{kind=link}

In spite of this, Snowflake still delivered 8% of pro forma operating margin in Q2, a 4-point jump from 4% in the year-ago Q2; and we note that on top of 36% revenue growth, Snowflake still qualifies in the "Rule of 40" club.

Valuation and key takeaways

At current share prices near $153, Snowflake trades at a market cap of $50.37 billion. After we net off the $4.85 billion of cash on its most recent balance sheet, the company's resulting enterprise value is $45.52 billion.

Meanwhile, for next year FY25 (the fiscal year for Snowflake ending in January 2025), Wall Street analysts are expecting Snowflake to generate $3.59 billion in revenue, representing 30% y/y growth. This puts Snowflake's valuation multiple at 12.7x EV/FY25 revenue .

Needless to say, Snowflake isn't exactly cheap yet, but considering the company's premium growth at scale plus attractive margin profile, I still think there's plenty of upside left. My price target on Snowflake is $188 , representing 16x FY25 revenue and ~23% upside from current levels.

Be patient here and wait for the rebound.

For further details see:

Snowflake: Take Advantage Of This Dip To Buy A Category Leader