SNOW - Snowflake: The Data-Driven Age Of Generative AI

2023-10-01 00:32:20 ET

Summary

- Snowflake is the most expensive buy-rated stock in my coverage universe.

- Generative AI has only increased the importance of data over the long term.

- Snowflake continues to post envious growth rates in spite of the tough macro environment.

- The latest Databricks funding round highlights the value in the stock.

Snowflake ( SNOW ) is likely the most expensive buy-rated stock in my coverage universe. The company has traded at the top of the tech sector in terms of valuation ever since it came public and the rising interest in generative AI has only helped the company continue that trend. SNOW has posted resilient growth rates in spite of the tough macro environment though it has felt a quantifiable impact. The company has a net cash balance sheet and is generating positive free cash flow, two features that help to improve its financial safety even if macro conditions worsen. While the stock is by no means cheap, I continue to rate the stock a buy as a pure-play investment on the growth of data.

SNOW Stock Price

SNOW crashed in 2022 and recovered this year like other tech stocks, but during that whole period maintained a premium valuation. Generative AI has only increased the importance of data - this is no hype-driven rally.

I last covered SNOW in July where I explained why the company’s partnership with Microsoft Azure ( MSFT ) was a game changer. The company continues to position itself to benefit from the generative AI opportunity.

SNOW Stock Key Metrics

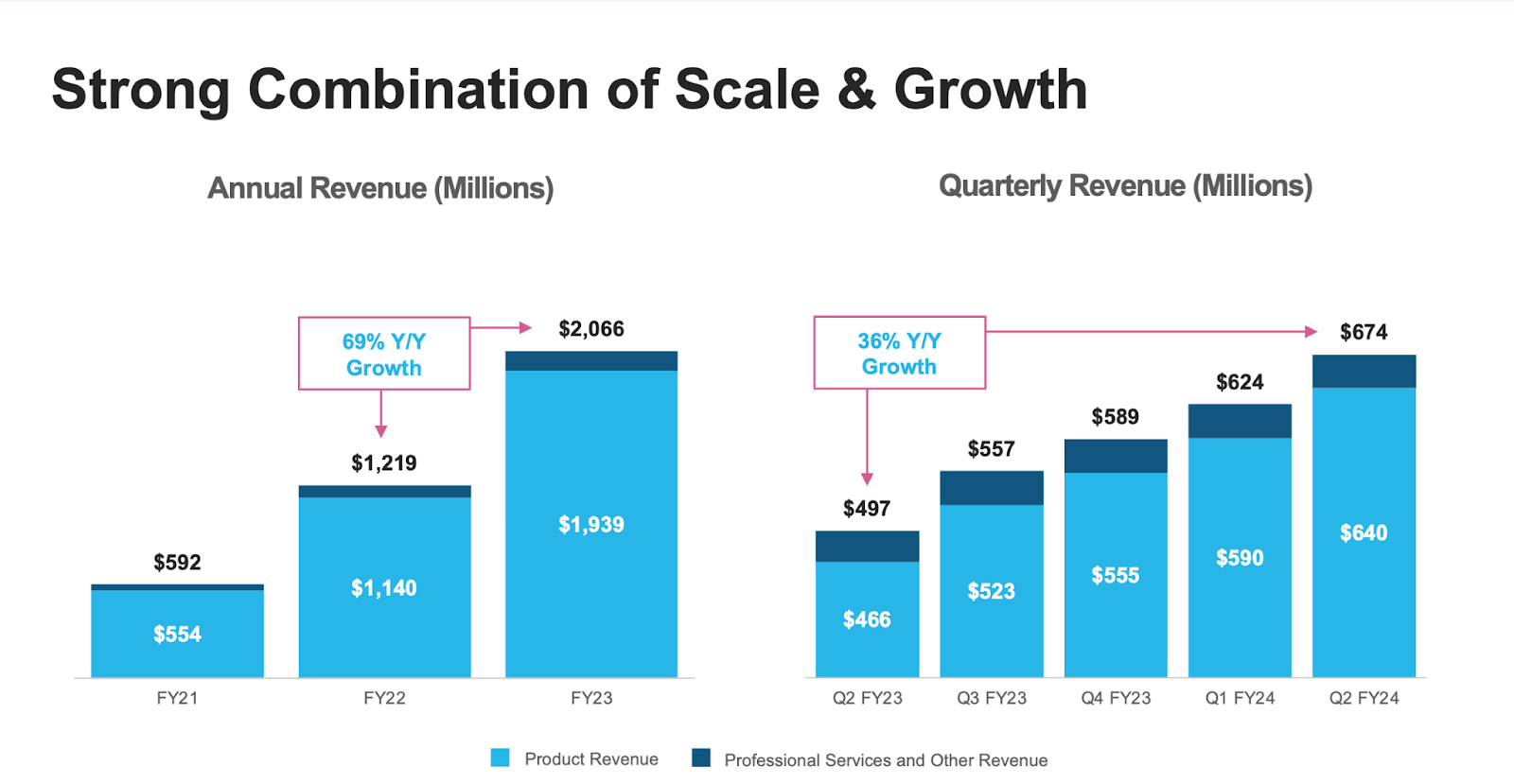

In its most recent quarter, SNOW delivered 36% YoY revenue growth to $674 million, marking a sequential step-down from the 48% YoY growth posted in the first quarter. Cloud optimization continues to pressure SNOW and other cloud plays.

{kind=link}

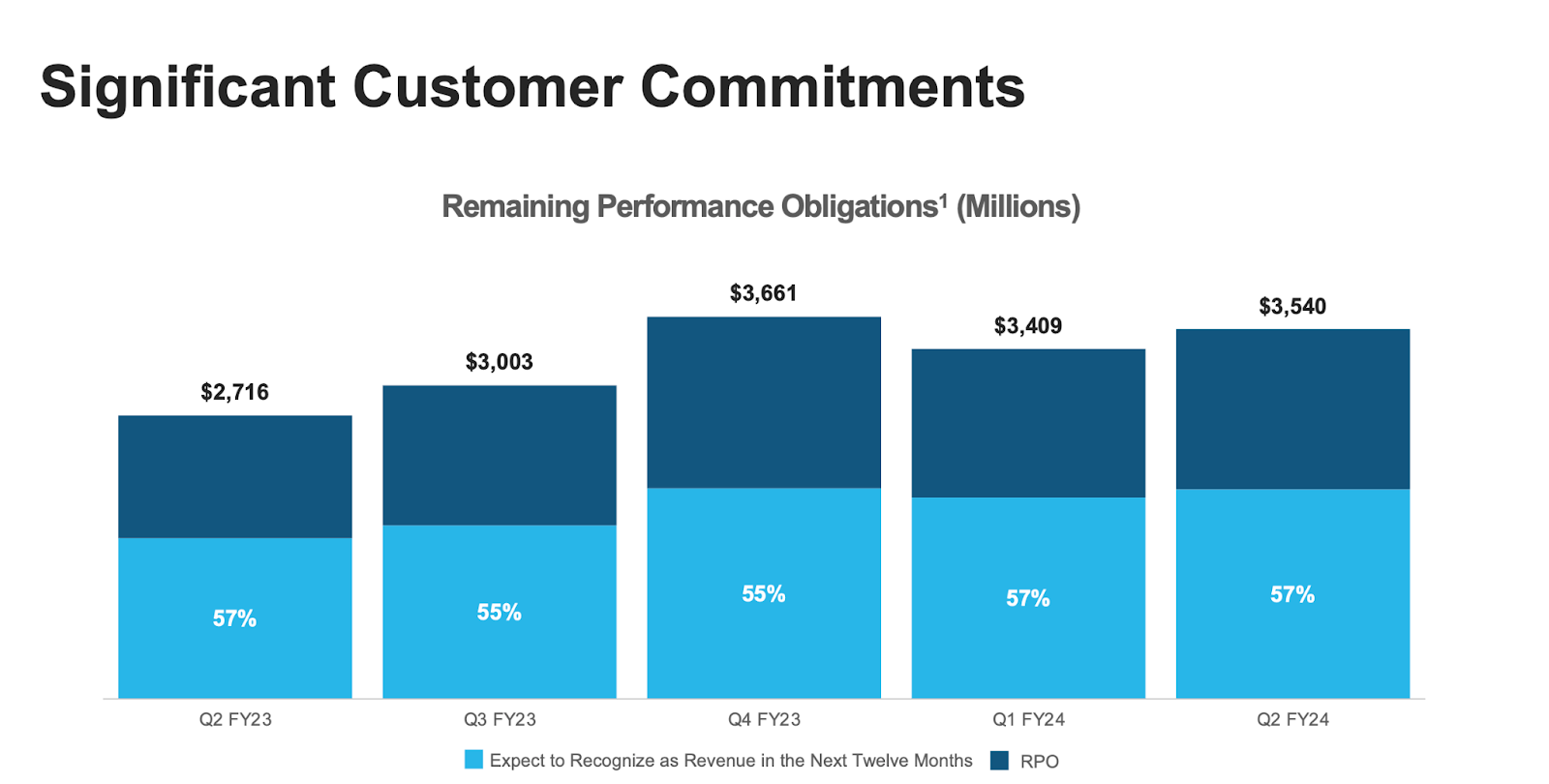

SNOW still delivered 30% YoY growth in remaining performance obligations (‘RPOs’) which ranks near the top of the tech sector. One can argue that such growth is not enough to justify the current valuation, but again macro is pressuring that number.

{kind=link}

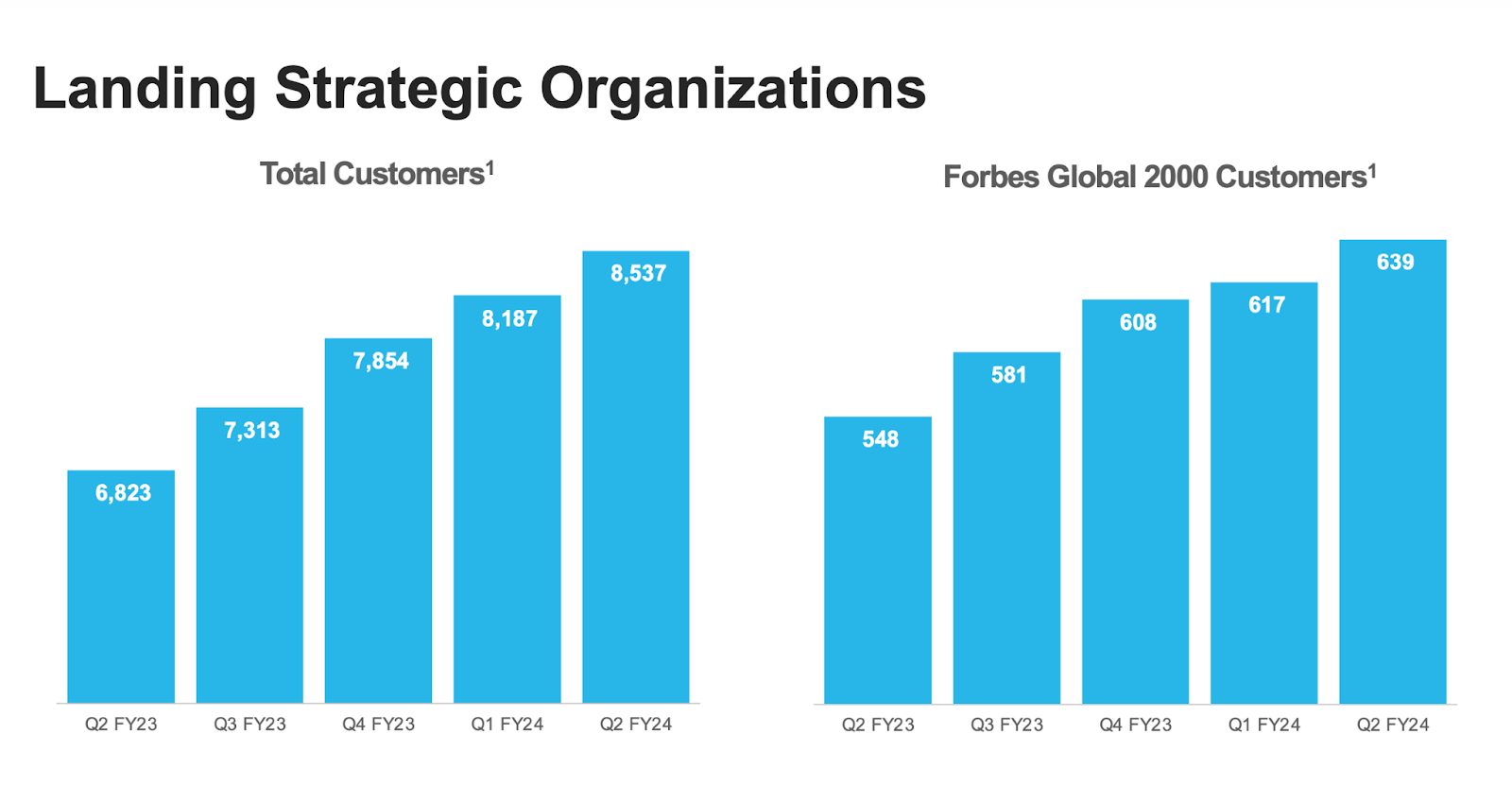

SNOW continued to grow its customer count - not an easy feat given that organizations have shown greater hesitancy in embarking on exploratory IT spend.

{kind=link}

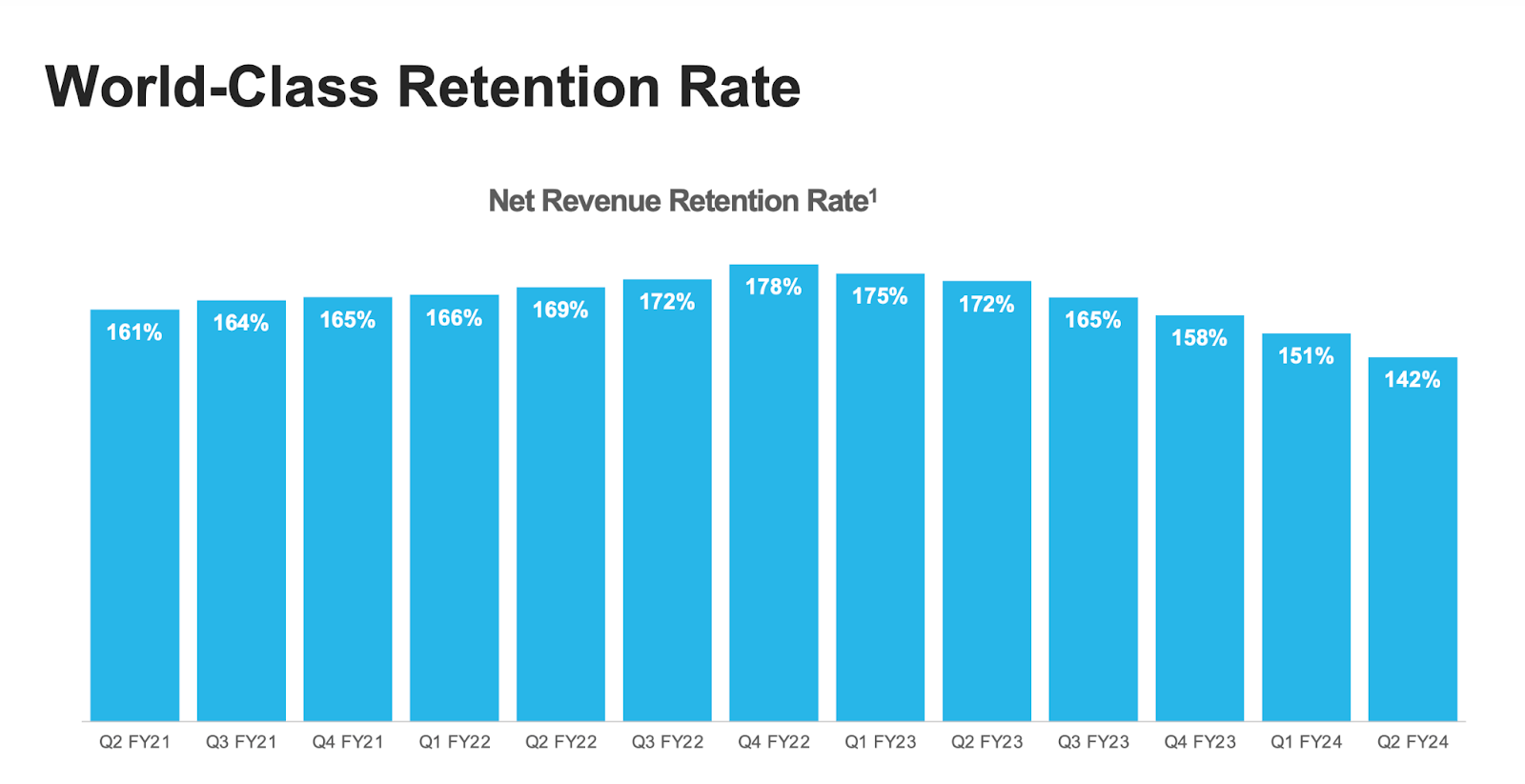

SNOW saw its net revenue retention rate decline to 142%, the 6th consecutive quarter of sequential declines since the company peaked at 178%.

{kind=link}

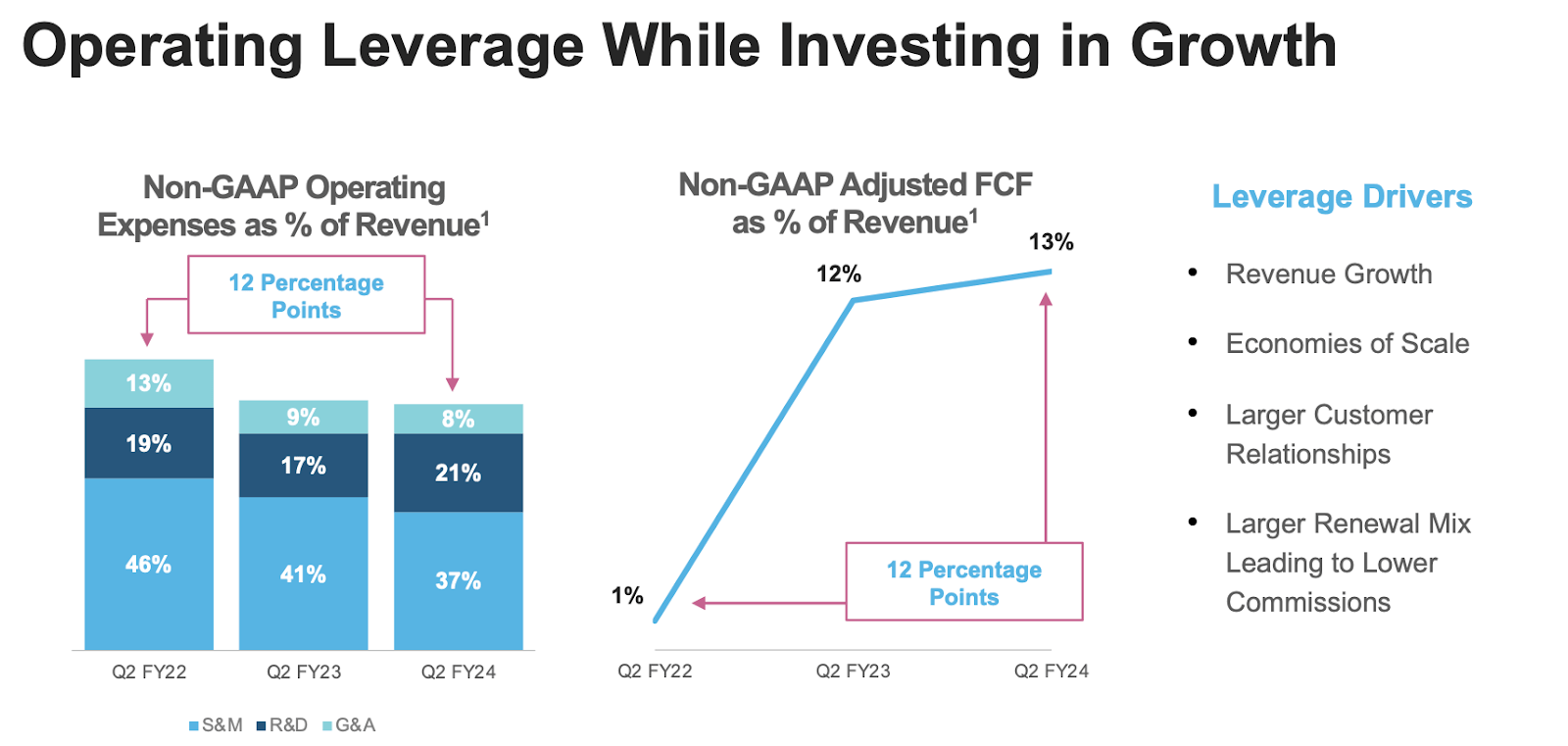

Like many other tech peers, SNOW has offset the pressured top-line growth with margin expansion. SNOW doubled its non-GAAP operating margin to 8% as it realized operating leverage. A crucial element of the operating leverage thesis is that sales commissions are considerably lower on renewed contracts.

{kind=link}

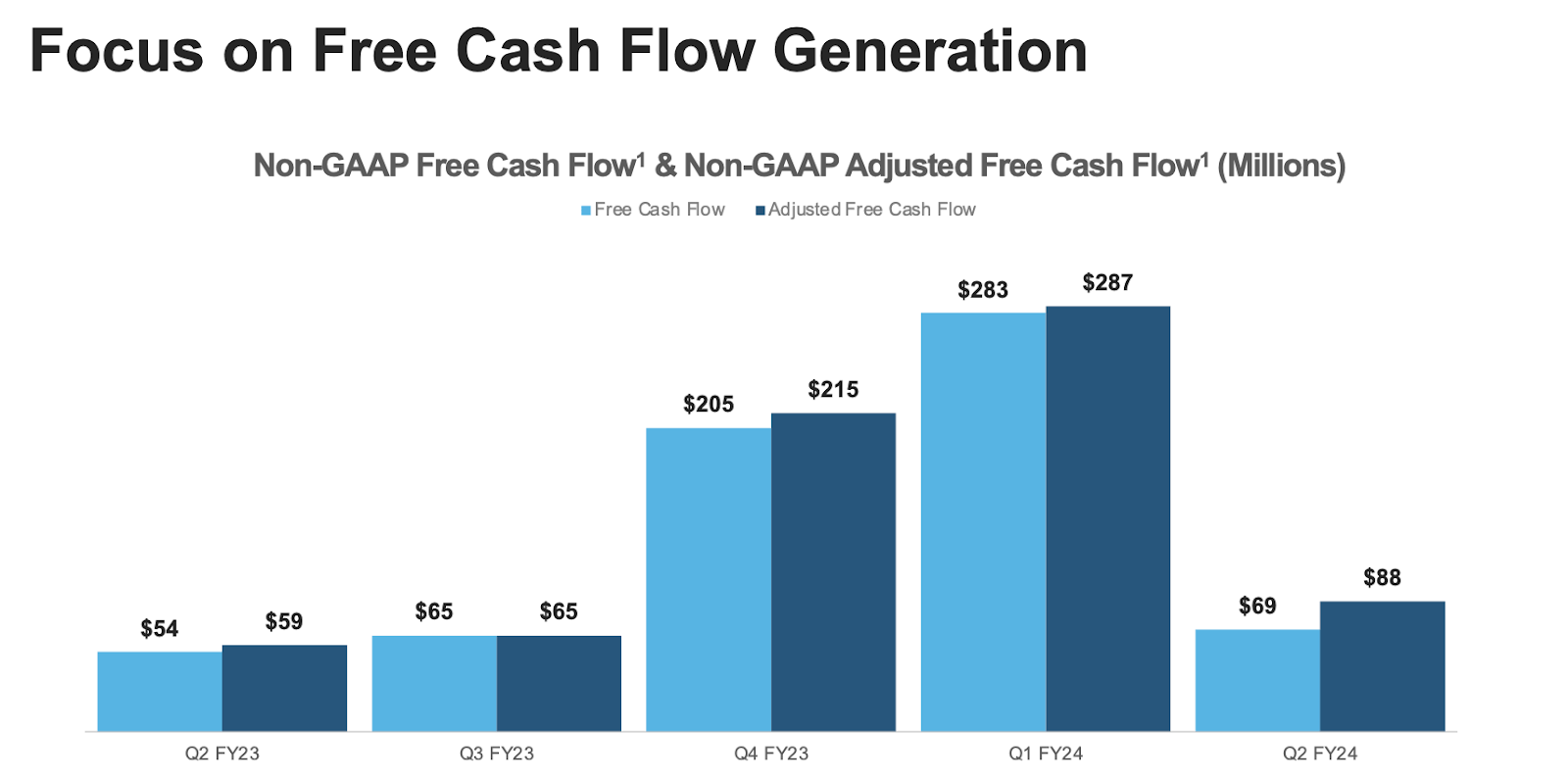

With minimal CapEx needs, SNOW is also generating positive free cash flow. I note that free cash flow can vary greatly quarter to quarter due to seasonality.

{kind=link}

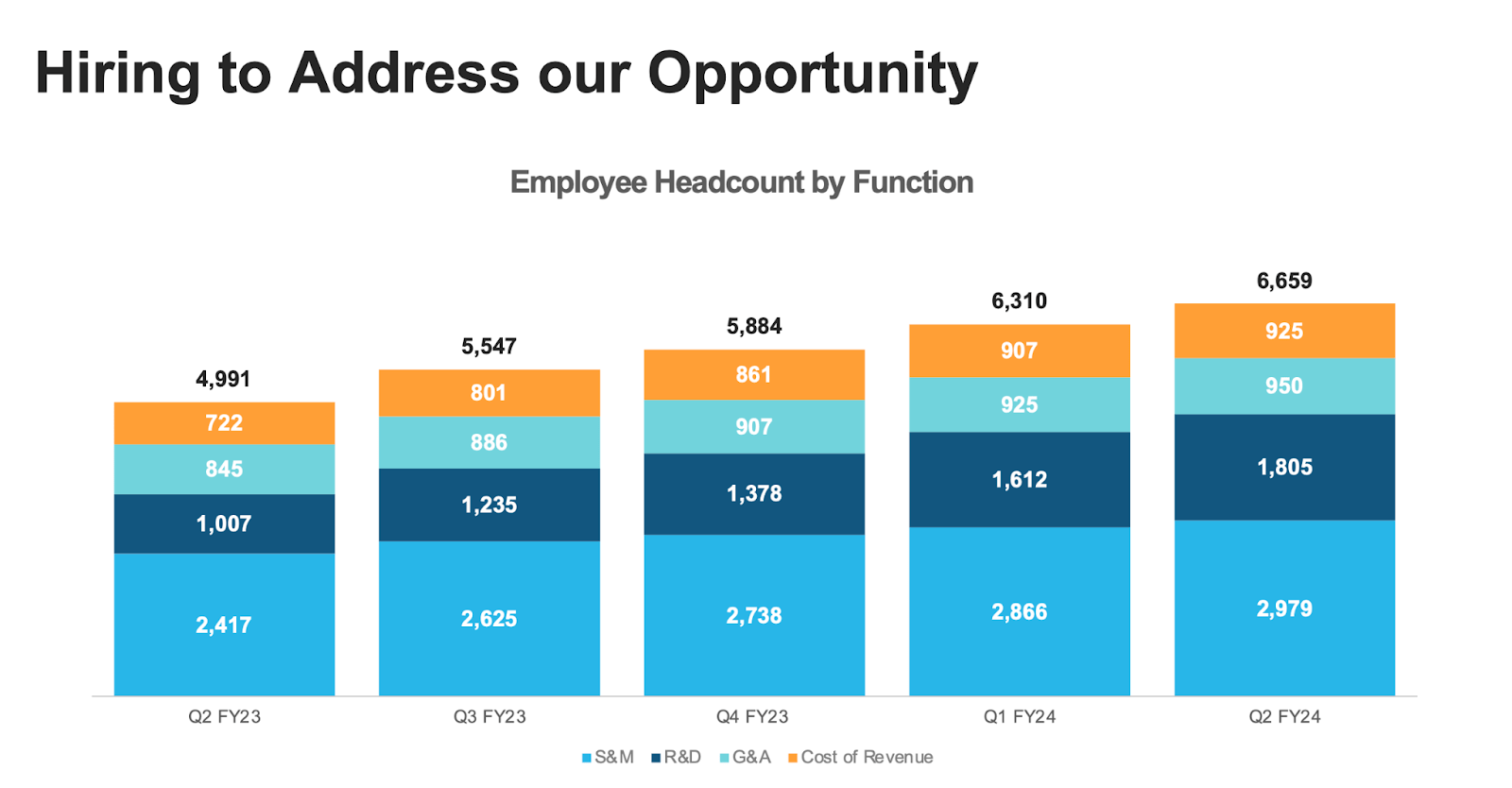

Unlike other tech peers who have taken advantage of the tough macro environment to do large layoffs, SNOW has continued to grow its headcount. This is largely influenced by the fact that the stock has continued to trade at premium valuations.

{kind=link}

SNOW ended the quarter with $4.9 billion of cash and no debt, representing a bulletproof balance sheet.

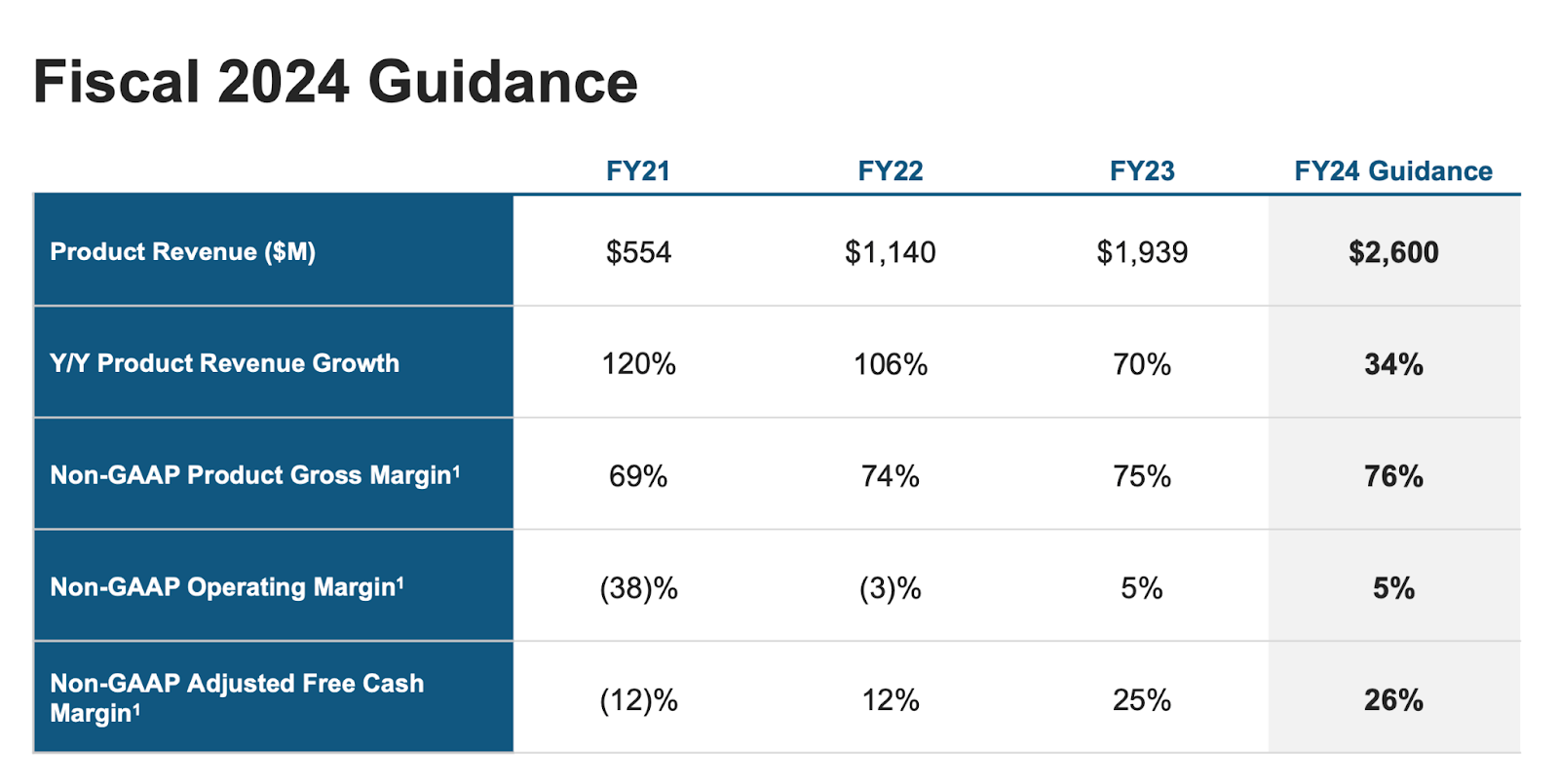

Management reiterated expectations for $2.6 billion in product revenue this year. Given that the company has already generated $1.23 billion in product revenue in the first half of the year, this guidance looks conservative. The flip side to that is that Wall Street is likely to be disappointed if SNOW does not end up materially beating on guidance.

{kind=link}

On the conference call , management noted that they did not repurchase any stock in the quarter but intend to “opportunistically” repurchase shares. I continue to view share repurchases as a poor use of capital given the stretched valuation. Management noted that in spite of the tough macro environment, they executed strongly on renewals, with one customer renewing a $100 million three-year term. I remind readers that SNOW operates on a consumption-based model, with customers committing to a minimum spend.

While SNOW has not yet seen a material impact from the rise of generative AI, management remains of the view that “being extremely organized on your data is going to become a premium thing.” A potentially overlooked impact from generative AI is that it may help bring a quicker end to cloud optimization headwinds as customers may wish to retain more data to allow for better AI outcomes.

Is SNOW Stock A Buy, Sell, or Hold?

SNOW is a data warehouse and data lake, enabling its customers to store and manage structured and unstructured data. Generative AI has only made data more valuable than ever before while also adding tailwinds to the “growth of data” thesis.

{kind=link}

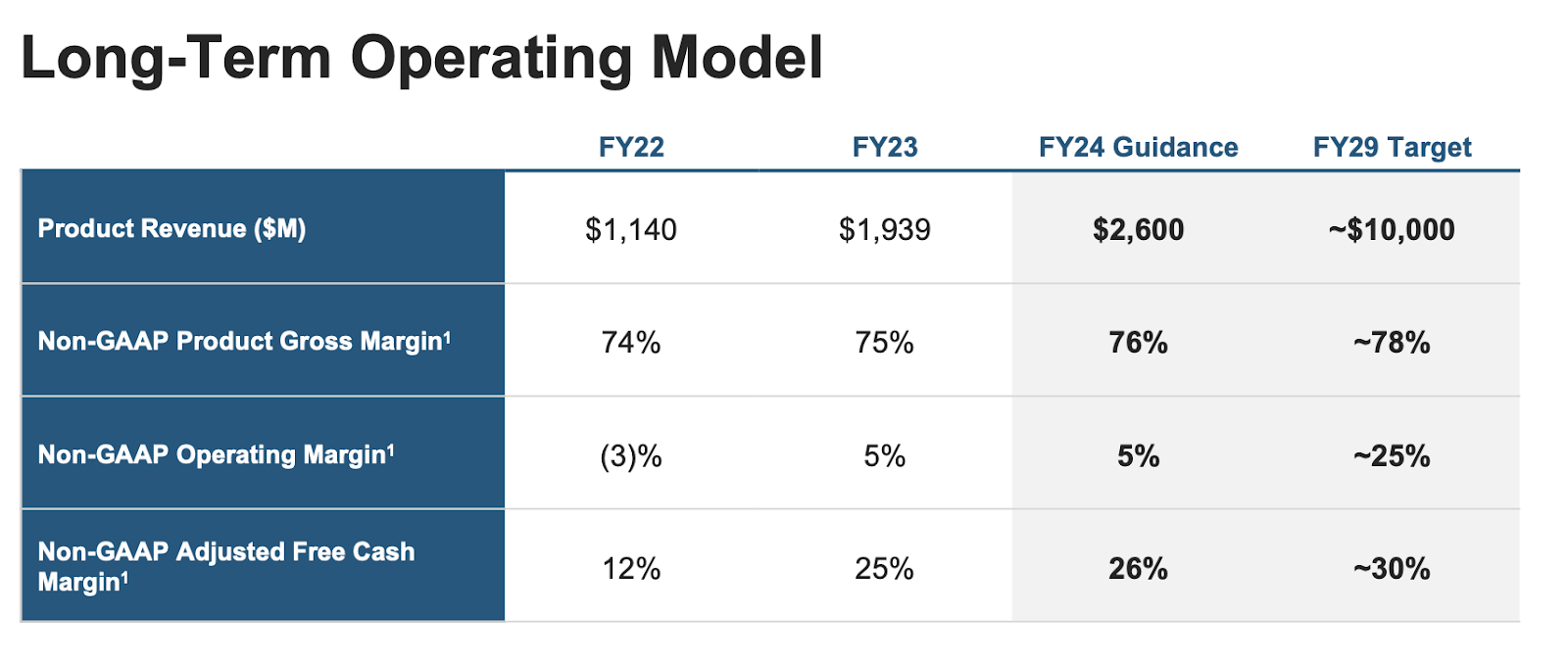

Management has given FY29 guidance of $10 billion in product revenue and 25% non-GAAP operating margins. Free cash flow margins are expected to be higher at around 30% due to both the prepaid revenue model of software as well as higher interest income earned from the higher interest rate environment.

{kind=link}

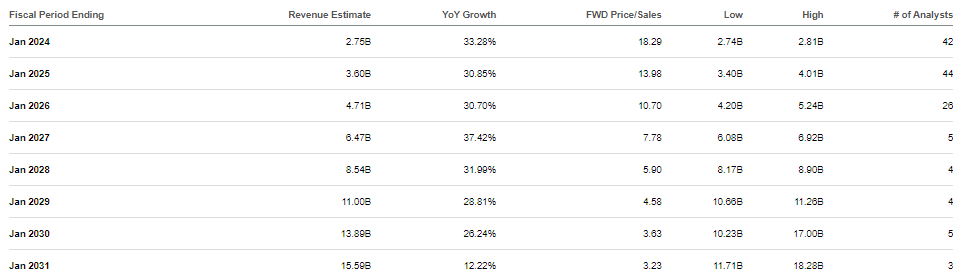

As of recent trading, SNOW was trading quite richly at around 18x sales. Wall Street has shown great confidence in the growth of data thesis.

{kind=link}

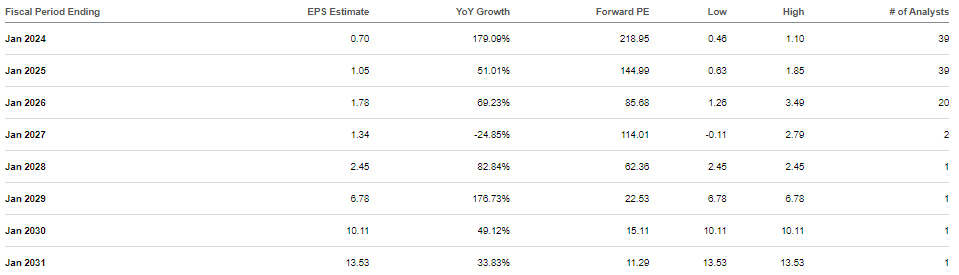

SNOW does not look cheap on an earnings basis until many years later.

{kind=link}

With the tech recovery well underway, such valuations may not be so crazy. Close competitor Databricks recently raised over $500 million at a $43 billion valuation . As part of the raise, the company noted that it had reached a $1.5 billion annualized revenue run-rate, with a 50% YoY growth rate in its latest quarter. That implies a valuation of around 29x sales, an exceedingly premium valuation. Yes, Databricks is generating a faster growth rate than SNOW but SNOW also has a larger revenue base. I again assume 25% growth exiting fiscal 2029, 30% long-term net margins, and a 1.5x price-to-earnings growth ratio (‘PEG ratio’). That implies an 11.3x price-to-sales valuation in FY29, or a stock price of $375 per share. That suggests around 17% potential annual upside over the next 5.5 years.

What are the key risks? Valuation is the most important concern. SNOW will need to see an acceleration in revenue growth as well as sustain elevated growth rates for many years in order to justify its valuation. If SNOW stumbles on its growth trajectory then I wouldn’t be surprised to see its valuation compress meaningfully. Competition may pick up, perhaps from the likes of Databricks, and that may pressure growth rates. It is possible that SNOW has earned a premium valuation in part due to the fact that Berkshire Hathaway ( BRK.B ) owns a stake in the company (which it acquired when the company came public). If BRK.B sells off this stake, then the valuation may compress. This is a stock that is well-loved by Wall Street and that is clearly visible in the valuation.

While SNOW is clearly richly valued, I reiterate my buy rating for the stock due to my confidence in the long-term trajectory of the growth of data, though note that there are cheaper buying opportunities elsewhere in the tech sector.

For further details see:

Snowflake: The Data-Driven Age Of Generative AI