MSFT - Snowflake: The Rally Is Just Getting Started - Don't Miss It This Time

2023-09-20 09:00:00 ET

Summary

- Snowflake Inc. stock has yet to benefit significantly from the generative AI boom that saw other AI infrastructure and SaaS stocks surge and keep their relative highs in 2023.

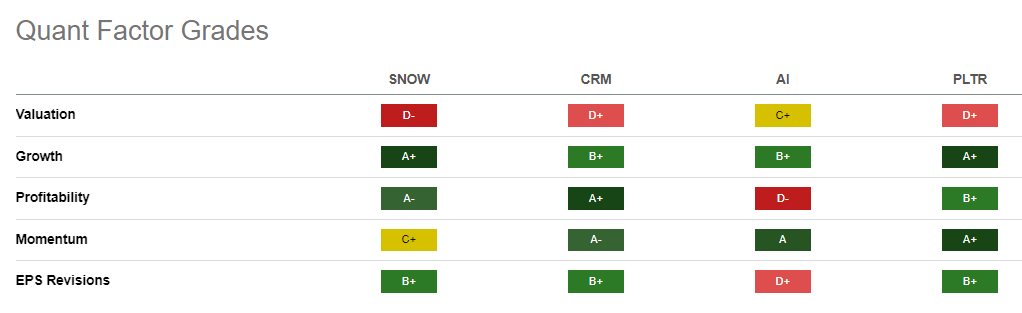

- SNOW's high-growth valuation is a mystery to value investors, but not for growth-focused investors, given its best-in-class "A+" growth grade.

- Snowflake faces tough competition from Databricks and challenges from Google Cloud. However, its consumption-based business should see a more robust recovery in the second half.

- While I was more cautious in May 2023, I gleaned SNOW could enter into a more robust uptrend recovery moving ahead, suggesting much-improved buying sentiments.

- Therefore, it's time for buyers still watching for an opportunity to consider striking at the current levels.

I last updated investors in leading data cloud company Snowflake Inc. ( SNOW ) in May, assigning SNOW a Hold/Neutral rating. That thesis has panned out according to my expectations, as SNOW has performed in line with the S&P 500 ( SPX ) ( SPY ) since my previous article.

As such, it's clear that SNOW has yet to experience the significant benefits from the generative AI boom that lifted the AI infrastructure stocks. In addition, pure-play AI SaaS stocks like C3 [AI] and Palantir ( PLTR ) have also benefited from the AI boom, even though near-term monetization remains questionable.

{kind=link}

Despite that, I believe it's justified why investors have not lifted SNOW's valuation, notwithstanding its best-in-class "A+" growth grade, as seen above. SNOW's "D-" valuation grade suggests it remains priced at a premium relative to its peers, indicating significant optimism is reflected.

However, it's crucial to consider Snowflake isn't a SaaS stock per se, as its business model is primarily consumption-based. As such, the ongoing cloud optimization has hurt its near-term growth cadence, increasing the execution risks to justify its high-growth valuation.

Therefore, I wasn't surprised that discussion about progress in its customers' optimization was a key feature in its fiscal second-quarter or FQ2 earnings call and a recent Goldman Sachs ( GS ) conference attended by CFO Mike Scarpelli.

Hence, it likely reassured investors that the company highlighted that it had experienced an improvement in customers' commitment through July, suggesting we should expect a more robust consumption cadence moving ahead.

However, competitive headwinds against its main rival, Databricks, could still ruffle feathers. Snowflake management acknowledged the underlying expertise in Databricks' data science capabilities. However, Snowflake has confidence that the TAM is big enough to accommodate the growth of Snowflake and Databricks.

Furthermore, Snowflake has benefited from its partnerships with Amazon Web Services or AWS ( AMZN ) and Microsoft Azure ( MSFT ), leveraging its multi-cloud value proposition. However, Google Cloud ( GOOG ) ( GOOGL ) remains a much tougher nut to crack as the Thomas Kurian-led cloud computing unit attempts to compete aggressively with Snowflake's offerings.

As such, I believe investors must pay close attention to the inroads made by Google Cloud as the company ramps up and further integrates its AI offerings. In addition, Databricks was also reported to be investing aggressively to catch up with Snowflake, which could impact Snowflake's profitability trajectory. Despite that, Databricks appears to have garnered a high valuation based on its most recent funding round, which could also support the market's perception of SNOW's high-growth valuation.

{kind=link}

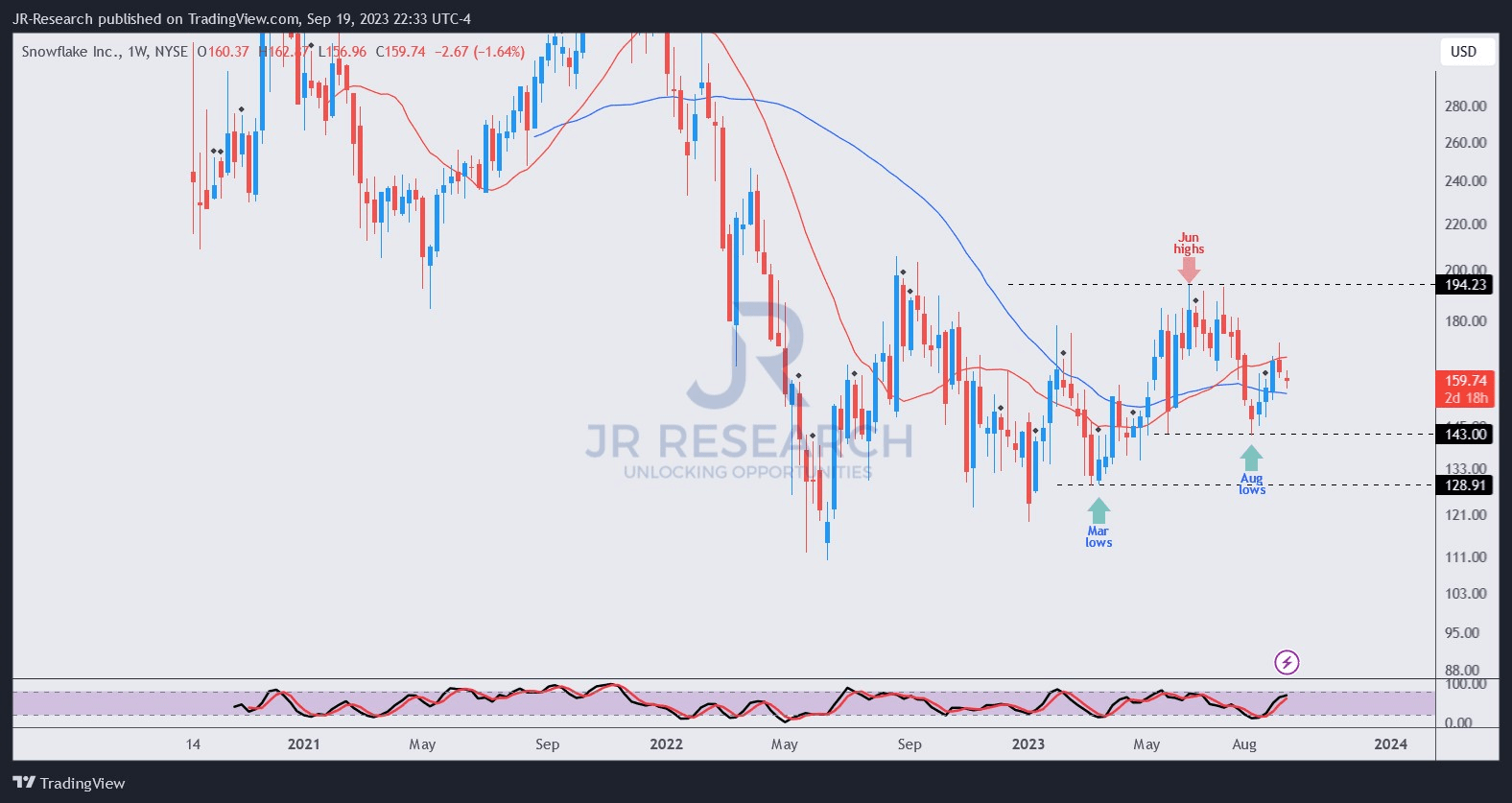

SNOW buyers have robustly held their March 2023 lows ($130 level), suggesting the worst selloff in SNOW is likely over.

In addition, the recent pullback from its June highs ($195 level) was well supported, as buyers returned as it formed its August lows ($143 level). As such, it helped create a higher low market structure for SNOW, bolstering my confidence that SNOW is likely on its way to recovering its uptrend bias.

However, my bullish thesis is still developing, requiring buyers to help maintain SNOW's August lows firmly. That said, I gleaned that buying sentiments in SNOW have improved markedly, suggesting investors are increasingly confident in the company's execution as market conditions improve.

As such, the risk/reward profile supports my thesis that momentum buyers could return, helping lift SNOW upward to re-test and break through its June highs potentially.

Rating: Upgraded to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Snowflake: The Rally Is Just Getting Started - Don't Miss It This Time