SNOW - Snowflake: Uncovering The Upside Potential From The Make-Or-Break Year(s) Ahead

2023-12-23 04:08:49 ET

Summary

- Despite promising product launches, Snowflake shares continued to underperform major cloud peers during 2023.

- 2024 could be a make-or-break year for the company, where it turns out whether it can restore its former glory.

- After taking a deeper dive into fundamentals, I believe there is a real possibility for the latter.

- Now is a good chance to take advantage of the share’s diminished valuation premium because, in the case of positive fundamental surprises, it could build up quickly again.

- Investing in Snowflake’s shares is a riskier investment than usual, suiting those investors who can bear large fluctuations in the share price even under relatively peaceful market conditions.

Introductory thoughts

Snowflake (SNOW) is one of the most interesting public SaaS companies in the modern cloud era with its unique data-as-a-service concept. The Snowflake Data Cloud enables companies to make the most of their data thanks to its unparalleled speed, scalability, and efficiency. Whether it's about analyzing proprietary data, collaborating with others, developing applications, or more recently executing AI/ML workloads, the company's platform comes in handy. Data is everywhere.

However, what seems to be an obvious advantage on the one hand, could be also a disadvantage on the other hand. The wide array of possibilities the Snowflake Data Cloud offers is hard to communicate in a nutshell. What makes this harder is that the service what Snowflake provides is less mission critical for the first sight than for example cybersecurity services of CrowdStrike (CRWD) or observability services of Datadog (DDOG). In times of rigorous IT budget cuts companies tend to postpone investments in their data ecosystem more likely as short-term cost control efforts outweigh medium/long-term efficiency improvements.

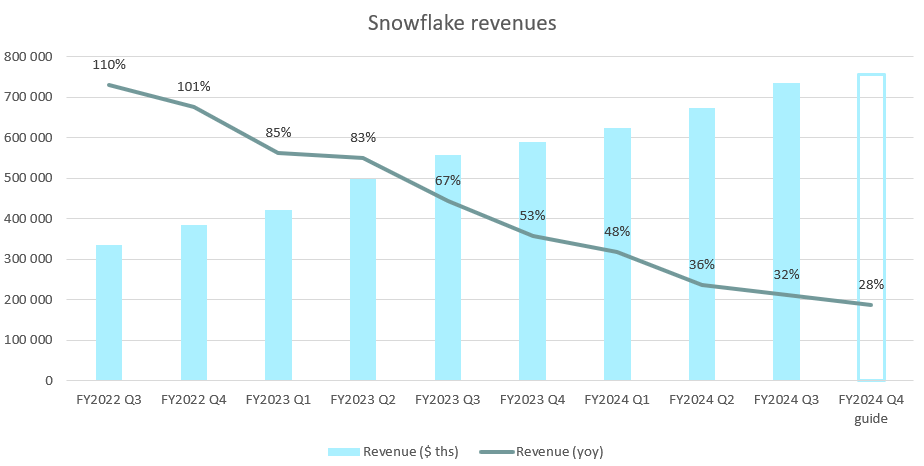

Snowflake suffered significant growth headwinds resulting from these cost optimization efforts and delayed investments leading topline growth to sink to ~30% levels from more than 100% 2 years ago:

{kind=link}

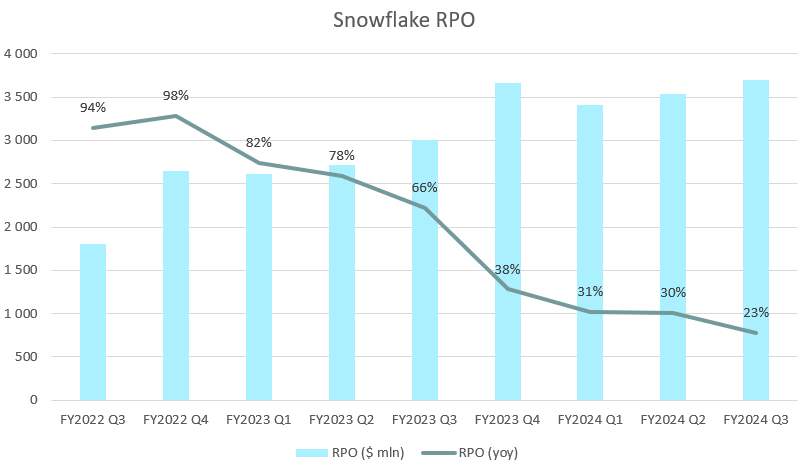

Although the pace of this slowdown shows signs of deceleration, the company still faces these headwinds. Recently this could have been evidenced in muted growth of Snowflake's business pipeline as measured by the company's remaining performance obligations (RPO):

{kind=link}

RPO grew 23% yoy in the most recent FY24 Q3 quarter a further significant slowdown from previous ~30% levels. In the top of that the number of Forbes Global 2000 customers - probably the most important customer cohort from a future growth perspective - grew only by 2 to 647 in total, which has been by far the softest print since the company publishes this metric:

Snowflake FY24 Q3 earnings presentation

I believe these numbers demonstrate it well that regardless that you have a service, which could be a game changer for many, if it's characterized by a rather complex sales motion and by a shallow learning curve (Snowflake customers reach their initially contracted capacity in 240 days on average) you'll have a hard time selling it in this environment.

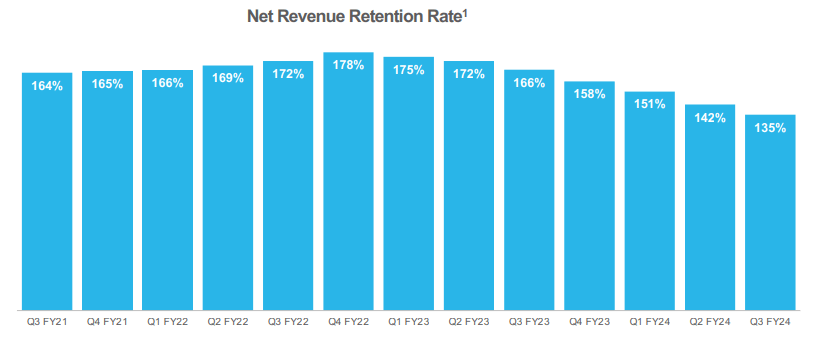

Although this is especially true for new customers net revenue retention numbers show that existing ones reined in their Snowflake spending as well:

{kind=link}

Thanks to Snowflake's per-second, usage-based pricing for compute and storage this has been quite easy to accomplish. This could have been painful on the short run, but I believe it will pay off on the long run. Snowflake had a chance to demonstrate the flexibility of its platform, which could increase customer loyalty further. Switching from Snowflake to another platform is already a complicated process, but why would you do it anyway, if it's also attractive from a cost perspective?

Based on this, I believe the main challenge for Snowflake in 2024 will be addressing new customers and efficiently promoting new products for existing ones. Luckily, the still vibrant AI-narrative, which celebrated its one-year anniversary recently provides a strong sales motion and draws organization's attention to the need for a data strategy. Based on Snowflake's numerous product enhancements over the past 1-2 years I believe they are in a good position to capitalize on this trend.

So, after another year of underperformance against market leading cloud service providers (e.g.: CRWD, DDOG) the question arises: Will Snowflake Break or Make in 2024? I'll share my thoughts on this in the upcoming paragraphs.

Cloud migration still in early innings

Just like many high performing SaaS companies Snowflake derives most its revenues from larger enterprises moving their workloads to the cloud. A good example for this is that the two fastest-growing customers in the recently closed FY24 Q3 quarter have been ones, who migrated significant workloads from a legacy vendor to the Snowflake Data Cloud. This makes up Snowflake's core business. Migrating on-prem data warehouses to the Data Cloud has several advantages, like enhanced flexibility, scaling, security, access, or lower total cost of ownership just to mention a few.

According to many industry experts the cloud transition is still in its early innings, so this could support Snowflake's revenue growth over the upcoming years. Looking at a recent study of Mordor Intelligence the Cloud Migration market is expected to reach a size of $629 billion for 2028 from $181 billion in 2023. This equals a CAGR of 28% over the next five years providing a solid base for Snowflake's core business.

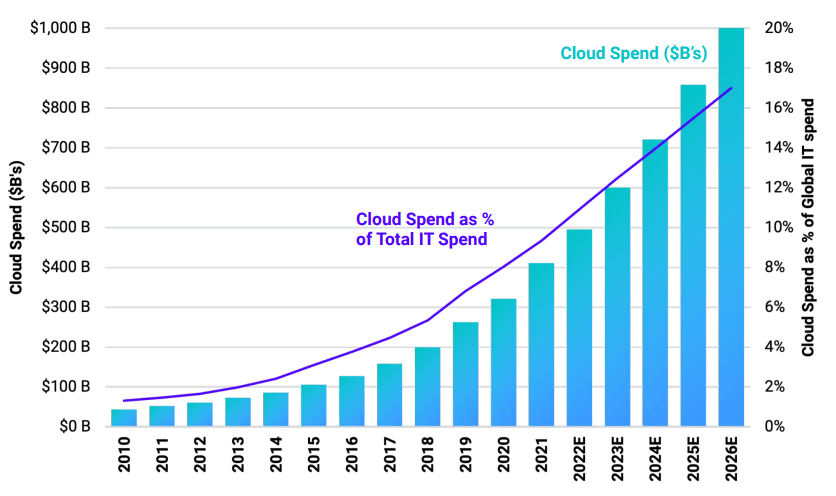

Looking at it from another angle, the share of cloud spending within total IT spending is expected to continuously grow in the upcoming years, reaching only 20% for 2026 according to Gartner:

{kind=link}

This also supports the fact, that the adoption of cloud services is still in its earlier stages providing sufficient growth opportunities for leading companies in the space.

Looking at the largest and most innovative players like CrowdStrike, Snowflake, Datadog, Zscaler (ZS) or MongoDB (MDB) we could have observed that their respective revenue growth rates declined to 25-40% yoy during the recent cloud optimization cycle, and now seem to be bottoming. I believe that these growth rates should represent a rather conservative scenario over the upcoming years as times like these when all customers begin to optimize their cloud spending are quite rare. Of course, in case of a prolonged recession this could happen, but these companies showed over the past two years that they can withstand significant external shocks as well.

Beyond cloud migration - The Snowflake data ecosystem

As more and more customers move their on-prem data warehouses to Snowflake's platform more and more of them get acquainted with the company's broader product portfolio. Snowflake has made huge efforts in recent years to create an own developer framework for the Snowflake Data Cloud, which enables more efficient programmability combined with faster runtimes and enhanced security features. This is how Snowpark was born, providing a very efficient way for interacting with your data within Snowflake, transforming it, building data pipelines, applications, or even large language models.

The launch of Snowpark in June 2021 has been a crucial milestone in the data analytics market as it brought a significant competitor for Apache Spark to life. Apache Spark is an open-sourced analytics engine developed at University of California, Berkeley by the same team who founded Databricks in 2013, Snowflake's main independent competitor in the data warehousing/analytics market. Apache Spark is one of the most popular engines for processing large-scale data primarily supported by programming languages such as Java, Python, Scala and R.

Snowpark managed to support Java, Python, Scala for the end of 2022. However, the recent announcement of Snowpark Container Services extended its reach to R and virtually any other programming language as well, because it enables developers to bring their code to the Snowflake Data Cloud. Thanks to the flexibility offered by containers data stays within the Data Cloud resulting in better performance and security features.

With this, Snowpark Container Services is ideal for running real-time AI/ML applications within the Snowflake Data Cloud and developing in-house LLM models based on proprietary data. Since the recently announced partnership with Nvidia, this process can be enhanced by Nvidia accelerated GPUs as well. This way Snowflake established itself as an important player in LLM development, which market is expected to grow at 20%+ in the upcoming 5 years to reach $40 billion. Currently, 70 customers are using Snowpark Container Services in private preview with many of them for developing large language models.

All in all, with the help of Snowpark, there is an endless range of use cases for customer data stored in the Snowflake Data Cloud. The easiest way for Snowflake to monetize Snowpark is to migrate those workloads from other engines (e.g.: Spark) to Snowpark, where the data resides within the Snowflake Data Cloud already. Customers can significantly increase runtimes and decrease costs by performing these workloads within Snowflake, instead of moving data in and out. Thanks to the fully managed service the company provides this comes with a higher degree of simplicity compared to Databricks for example, which requires much more deployment and administration efforts.

As of the end of the FY24 Q2 quarter 63% of the company's global customers utilized Snowpark at least on a weekly basis, while consumption grew 47% qoq in FY24 Q3 equaling a yoy growth rate of more than 500%. These large numbers are partly the result of a low basis as Snowpark entered general availability in several programming languages only in 2022. According to management comments from the Q2 earnings call revenues from Snowpark could make up a few percentage points of total revenue this year, but they can be more meaningful in the upcoming ones.

Let's assume Snowpark revenues make up 5% of total revenues this year, grow at an average of 25% qoq (144% yoy) through FY25 (CY2024), while the rest of the business grows at ~35%. This would mean that for FY25 the share of Snowpark revenues would increase close to 10% accounting for 18% of total topline growth and increasing the yoy revenue growth by 5%-points (35% vs 40%). This shows that Snowpark has significant potential for boosting topline growth over the upcoming years that could be materially enhanced by new AI/ML workloads, which are only in the very early innings.

An important accelerator of these AI/ML workloads could be the recently announced Snowflake Cortex , which is currently in private preview. It provides a fully managed services enabling data analytics and building of AI apps for users of all skillsets. It enables to easily establish LLM-based models for answer extraction, sentiment detection, text summarization or translation using unstructured data and also enables creating ML-based models for forecasting or anomaly detection. As these are generally occurring use-cases at several customers Snowflake Cortex could be an important driver in increasing business efficiencies.

A good example that more and more customers are curious about these workloads is that 30% of Snowflake customers processed unstructured data in the Q3 quarter, while consumption of it grew 17-fold yoy.

Another recently launched product, which helps customers in simplifying data engineering processes is Dynamic Tables , currently in public preview with more than 1,500 customers using it. It provides an easy way to prepare data for consumption within the Snowflake Data Cloud. According to management the product has outpaced initial expectations, so another one to add to the list of potential revenue reaccelerators for next year.

To continue the list of recent innovations and product launches there is Unistore , which enables delivering transactional and analytical workloads on a single platform opening up several new use cases for Snowflake. It could go into general availability next quarter and ready to ramp next year.

On the top of those innovations I've mentioned above, there are several other ones in the pipeline, some of which I'll discuss in the upcoming paragraphs. I believe that Readers could a get good grasp of how transformative these recently launched products of Snowflake could be, even if some of them won't be utilized as much as others. Thanks to these innovations the Snowflake data ecosystem became so versatile that the company had to come up with a new sales strategy recently:

"Now we have a ton of irons in the fire, and they're now all getting hot. So from a sales standpoint, we have much more specialization happening and that is going to literally going all over the world because it is impossible for a single person to be to be expert in all these technologies and all these disciplines. So we're going to have people that have general purpose capabilities, sort of core skills, if you will, and then we will have teams of specialists that will augment these groups wherever they're needed. " - Frank Slootman, Chairman and CEO on Q3 earnings call

Based on this, I believe it will be a real challenge to communicate the entire scope of possibilities the Snowflake platform offers, so a lot will depend on the salesforce in the upcoming years. I believe this will result in increased investments in S&M, so investors should be prepared for a potential compression in margins. Although, this will probably happen anyway thanks to increased amortization of software development costs (see all the new product launches discussed above).

Better together

Another unique feature of the Snowflake data ecosystem is the possibility of sharing data, workloads, models, applications within the Snowflake Data Cloud. This forms also the core part the company's mission statement, which sound as follows: "We're on a mission to mobilize the world's data by building the greatest data and applications platform."

Data sharing within Snowflake provides an efficient way for companies to share data with clients or partners. The data stays within the Data Cloud, so it's a secure way of sharing, while customers can manage access to their data easily. It's also possible to share data within the Snowflake data ecosystem by using listings on Snowflake's public marketplace. This way customers can monetize their data assets within the Snowflake community conveniently.

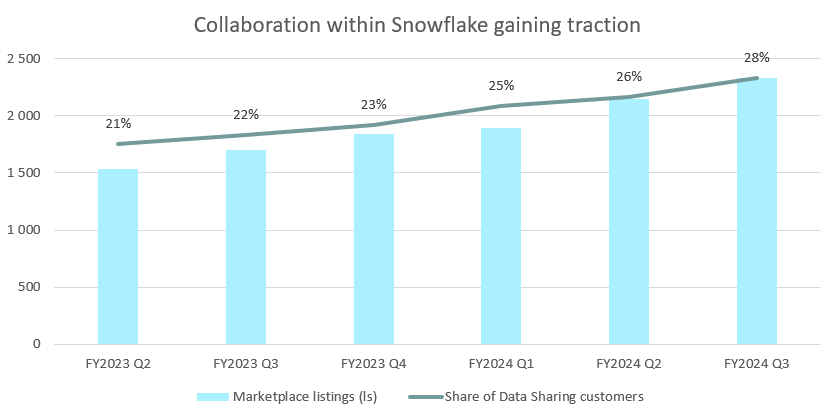

Looking at the numbers the share of customers using data sharing regularly and the number of marketplace listings of datasets and data services is growing nicely:

{kind=link}

The number of marketplace listings reached 2,332 for the end of FY24 Q3 growing 37% yoy. In Q1 and Q2 the number has grown by 39% and 40% yoy, respectively, so the growth dynamic is keeping up. This shows that Snowflake is on a good path to create a worldwide data sharing community, where the company acts as the key intermediary.

Besides sharing data, Snowflake customers also able to share their applications developed within the Data Cloud with others. The Native Application Framework, which enables customers creating applications that leverage Snowflake functionality will be generally available this quarter. The acquisition of Streamlit in 2022 has been an important milestone in this process, which provides an easy way for creating and sharing web applications for ML and data science. New applications, which enable more efficient utilization of Snowflake's Data Cloud are a good way for increasing consumption on the platform, hence they could be an important driver of topline growth reacceleration.

I believe the product innovations the company accomplished recently combined with the concept of creating a worldwide community of Snowflake customers puts them as one of the most promising stories within the technology space in the upcoming years. This idea is shared by Boston Consulting Group as well, who in cooperation with Fortune produce the list of The Fortune Future 50 companies almost every year (with the exception of 2022) since 2017. The list includes those 50 public companies who are perceived to have to best long-term growth prospects. The Top 3 for the past few years look as follows:

Fortune

Snowflake hasn't even been in the Top 10 in recent years but jumped to the first place for 2023 all of a sudden overtaking industry disruptors like CrowdStrike or Datadog.

Finally, there are some other hints that 2024 could mark a strong comeback year for the company. First, consumption trends seemed to have stabilized recently as management highlighted in the most recent earnings call: "Growth in September exceeded expectations. For three weeks, consumption grew faster than any other period in the past two years. Consumption continued to grow in the month of October." - Mike Scarpelli, CFO

This shows that there's a real possibility that the increasing adoption of new products coupled with increasing demand for AI/ML workloads could meet generally improving consumption on the platform next year. If this happens indeed, I believe it could be a very strong fundamental setup with material upside to current revenue estimates .

This could be further supported by the strengthening ties with Microsoft, which already bore fruit in the FY24 Q3 quarter:

"Yes, we actually saw quite a bit of energy coming from the Azure platform this quarter. The things that we worked on in the renewed relationship with Microsoft is really much better alignment in the field from a compensation standpoint that is just super, super important in our world. And we're seeing the effects of that. And the Microsoft platform really upticked during the quarter." - Frank Slootman, Chairman and CEO on Q3 earnings call

Currently, Snowflake consumption on Azure makes up only 21% of total consumption, whereas AWS makes up 76%. If we compare this to the 32% market share of AWS and 22% market share of Azure in the cloud infrastructure market there is plenty of room for business conducted on Azure to grow.

Last but not least, Snowflake is very close to earn the FedRAMP high authorization. This could provide the green light for handling critical federal data, like data from health or financial systems. If this happens, the federal business could emerge as a new growth pillar in the upcoming years.

Taking all these things together I believe Snowflake provides one of the most exciting stories on the stock market for 2024. Even top management is unsure how these new product launches could impact revenues over the upcoming quarters, so analysts will also have a hard time to model the possible impacts. A common method is to stay really conservative as long as there is a high degree of uncertainty. I think this is the reason that the consensus calls for ~30% yoy revenue growth for both calendar year 2024 and 2025, which seems overly cautious to me.

Risk factors

Great hopes could lead to great disappointment, so let's not forget to look at the main risk factors, which could prevent Snowflake shares from being a good investment for 2024.

First, as I already mentioned the Snowflake data ecosystem is becoming increasingly versatile. The solutions of Snowflake are mostly used by developers. High degree of technical expertise is required to understand the benefits of different products, which makes selling it also harder. I think it will take time until sales representatives develop the necessary sales motion with all the new product launches, which can be clearly communicated towards customers. However, the fully managed service the company provides eases this burden to some extent, and the adoption LLM-based user interfaces comes also in handy.

Another important risk factor for Snowflake is IT security. We have seen at other SaaS companies that a security breach can have serious impacts on the company's share price, and also on its business. Snowflake usually highlights the benefits of enhanced security features when arguing for the Data Cloud, so a possible breach could undermine the confidence in the company to a greater extent. Snowflake takes IT and cloud security seriously, as an example they are participating in CSA's (Cloud Security Alliance) Self-Assessment program, which is about complying with CSA-published cloud security best practices. Also, to earn the FedRAMP High authorization Snowflake must comply with strict security requirements, which also ensures that security issues are handled appropriately within the company.

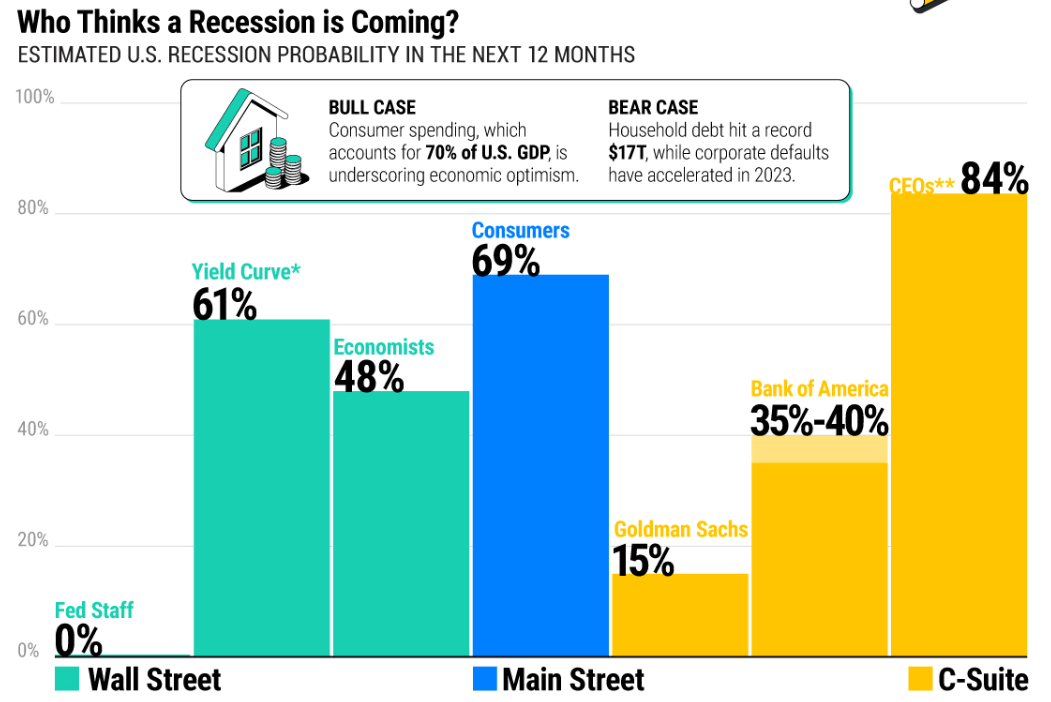

Another important risk factor for Snowflake's business could be a general economic downturn beginning in 2024. Although the odds for it have typically declined in the second half of the year, there is still a real possibility this could set in:

{kind=link}

From the chart above we can see that different actors of the economy have very different views on the topic. However, one thing is sure, technology companies used to fare better during typical recessions, where decreasing consumer spending starts to drag down the economy. So, it would be negative for Snowflake, but possibly to a lesser extent than the recent prolonged cloud optimization cycle.

Finally, a main risk factor worth considering when investing in Snowflake shares is their valuation itself. The more future growth potential is reflected in a company's valuation the more exposed the share price is to changes in this growth outlook. Typically, this leads to high volatility after earnings announcements, but also in times of perceived market stillness. Only those investors should consider investing into Snowflake's shares who can bear higher volatility, because I firmly believe it is here to stay for the upcoming years.

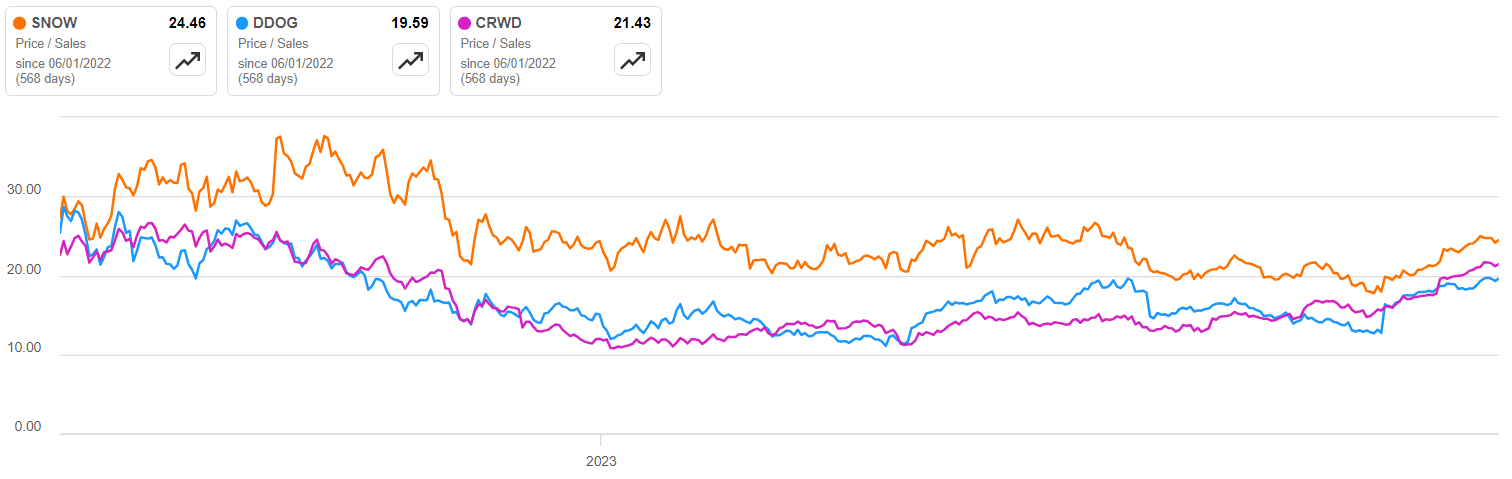

One important positive regarding valuation is that Snowflake's valuation premium compared to leading SaaS peers more or less diminished over the past year making shares more investable within this space:

{kind=link}

Looking at the TTM Price/Sales ratio, shares of Snowflake are valued 25% higher than the shares of Datadog and 14% higher than the shares of CrowdStrike. Going back only one year this has been 57% and 103%, respectively. So, the market got significantly more cautious about Snowflake. In the next paragraph I will examine what possibilities this could hold for the future.

Valuation: Make or break?

I want to keep the valuation section simple, as there are so many moving parts in the case of Snowflake that building a complex DCF model wouldn't bring us closer whether to invest in the shares or not in my opinion. For this reason, I have created 3 different scenarios ("Break", "Base case", "Make") and analyzed where the share price could be in 3 years' time based on these. My hypothetical revenue growth rates for the upcoming years look as follows:

Created by author based on own estimates

As there is only one quarter left from FY24 I used current analyst and company estimates for this year representing 35% yoy growth compared to FY23. For the Break scenario I assumed that new product launches wouldn't significantly impact Snowflake's topline, and usage trends don't improve materially from current rather depressed levels resulting in 25% yoy growth every year until FY27.

In the Base case scenario, I assumed gradually improving usage trends and slight contribution from new product launches and AI/ML workloads. This scenario assumes the same growth rate for FY25 than for FY24 and a slight acceleration from these levels for the upcoming two fiscal years.

Finally, in the Make scenario I assumed that new product launches resonate quickly with customers and general usage trends continue to improve. This results in increasing growth rates over FY25 and FY26, while revenue still grows at 50% yoy in FY27.

Based on these scenarios actual revenues for these fiscal years would look as follows:

Created by author based on own estimates

Snowflake plans to achieve product revenues of $10 billion for FY29, which should equal total revenues of ~$10.5 billion. In case of the Break scenario the company wouldn't reach this goal if it grows by the same 25% growth rate in FY28 and FY29, so this can be regarded as a conservative scenario indeed. In case of the Base case scenario this threshold could be reached by FY29, while in the case of the Make scenario already in FY28 representing a more optimistic scenario.

The different scenarios bring different valuation multiples with themselves. A company with higher perceived growth rates usually tends to be valued higher than slower growing peers. Based on this I have created the final valuation input, the hypothetical TTM P/S multiples for the end of each fiscal year:

Created by author based on own estimates

Currently, Snowflake shares are valued at ~25x FY24 expected revenues. For the Break scenario I have assumed that this multiple significantly contracts and stays at 15 for the upcoming years. For the Base case scenario, I have assumed slight expansion from current levels, while for the Make scenario more material expansion resulting from materially improving business conditions.

Calculating with 2% annual dilution the share price of Snowflake would look as follows at the end of each fiscal year based on the previously discussed scenarios:

Created by author based on own estimates

Each fiscal year equals approximately the calendar year before, so for example FY24 equals CY23. Currently, Snowflake shares trade at ~$200 levels. In case of the Break scenario, they would trade only fractionally higher in three years' time, so for those investors who don't believe in improving business conditions there are surely better opportunities out there.

Within the Base case scenario, the share price could triple in three years' time, which seems a sound investment. ¾ of this increase would result from increasing revenues, while ¼ from multiple expansion.

Finally, the Make scenario shows how much potential could be really in Snowflake's shares if business fundamentals get back on track and new product launches are well received by customers. Assuming a little bit more ambitious revenue targets and continued multiple expansion leads to a doubling share price within a year and a five-fold increase within a three-year timeframe with a $1,000+ share price.

With this, the current risk/reward setup is quite attractive in my opinion. The scenarios presented above are not the worst- or best-case scenarios, lot of things can happen within three years, especially in such a rapidly changing market.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Snowflake: Uncovering The Upside Potential From The Make-Or-Break Year(s) Ahead