SNOW - Snowflake: Unique Growth Prospects Justify Current Valuation

2023-07-27 05:35:19 ET

Summary

- Snowflake's partnership with Nvidia, along with its other AI/ML-related innovations, is expected to significantly boost its revenue in the coming years.

- Despite reaching annualized revenues of nearly $2.5 billion, Snowflake still has a long runway for growth, with a largely untapped market among existing and prospective customers.

- Despite trading at higher multiples than many SaaS companies with similar growth rates, SNOW's unique growth prospects justify its current valuation.

Investment thesis

Snowflake ( SNOW ) is transforming how enterprises interact with their data for a while now. One of the most important steps in this process has been the launch of the Snowflake Data Cloud in 2020, which united cloud data warehousing, cloud data lake, data engineering, data science, data applications, and data exchange and sharing services under one umbrella powered by one single platform. Since then, many important product innovations have been made, which received another strong push this year manifesting in several important announcements during Snowflake Summit 2023 .

Most headlines around Summit 2023 have been centered around partnerships with Microsoft ( MSFT ) and Nvidia (NVDA), but this has been only the tip of the iceberg in my opinion. The launch of Snowpark Container Services , taking the Native App Framework to public preview, or the several AI/ML related announcements on the top of the Nvidia partnership are equally exciting news. In the first part of the article, I want to provide a short analysis on these features, as they should provide significant revenue upside in the upcoming years in my opinion.

In the second part I'll discuss the more quantitative part of the Summit based on the insightful slides from the company's Investor Day, that took place on the second day of the Summit. The numbers show that despite reaching annualized revenues of almost $2.5 billion there is still a long runway for further growth both in the case of existing and prospective customers.

I believe that these unique future growth prospects within the SaaS space justify the current valuation of shares, even if they trade at significantly higher multiples than many SaaS companies with similar growth rates.

AI is coming to Snowflake

On the FY24 Q1 earnings call Snowflake management already foreshadowed that there are some significant product announcements in the pipeline for Summit 2023, but I think not many of us imagined that a partnership with Nvidia is under way. On the first day of the Summit Frank Slootman and Jenson Huang joined each other on the stage and announced that the companies will join their forces to create a unique developer experience for building AI, machine learning ((ML)) and large language models (LLMs).

On the one hand, this partnership will result in developers having access to Nvidia's GPUs within the Snowflake Data Cloud. On the other hand, Nvidia's NeMo platform, which has been built for developing LLMs will be integrated into Snowflake as well, enabling developers to build and run AI applications directly within the Snowflake Data Cloud. This way, Snowflake stays true to its main philosophy, which is bringing the workload to the data and not the opposite. Seeing the AI frenzy in recent months I believe that many organizations will utilize this opportunity to build their own, proprietary LLMs within the Snowflake Data Cloud and it will be also a good incentive to bring new data and new customers to the platform.

Besides the Nvidia partnership there have been other announcements on the AI/ML front as well. First, Snowflake announced different ML-powered functions for data practitioners including forecasting, anomaly detection and contribution explorer. These functions are meant to help customers in general business problems and are expected to increase consumption on the platform.

Second, several Python enhancements in Snowpark (developer framework for Snowflake) have been announced, which is the most common programming language for building ML models.

Third, utilizing the technology of recently acquired Applica, Snowflake introduced its Document AI feature (currently in private preview), which helps analyzing unstructured data with focus on documents like invoices or contracts. Document AI leverages a Snowflake-native purpose-built LLM, which also enables fine-tuning of the model by customers.

Fourth, Snowflake is developing several LLM-powered experiences in order to increase user productivity. Among others this includes conversational search within the Snowflake Marketplace or Snowsight (Snowflake Web Interface).

With the developments mentioned above Snowflake managed to introduce a very wide array of AI/LLM powered features within a short period of time. These span a wide spectrum of use cases like boosting productivity through LLM-powered experiences, improved data analytics with built-in LLMS, and of course building and running LLMs themselves. I believe this leaves no doubt that Snowflake managed to establish a leading position in the world's transformation through AI.

Snowflake for everyone

Snowflake announced its Native Application Framework in 2022, which enables developers to build and monetize data-intensive applications within the Snowflake Data Cloud. Snowflake customers can utilize these apps directly via the Snowflake Marketplace reducing the need for moving their own data. On Summit 2023 Snowflake announced that they are taking the Native App Framework from private to public review making the solution accessible in general.

One of the biggest announcements of Summit 2023 relates directly to the Native Apps Framework, which has been the introduction of Snowpark Container Services . This feature extends Snowflake's programmability to virtually any programming language with the help of a Kubernetes-like framework. Snowflake already supported SQL, Python, Java and Scala, but with the help of containers there will be no limits in this regard. Developers will be able to bring their code to the data stored in Snowflake without barriers, making the platform an excellent choice for building data-intensive applications and AI/ML models. Snowpark Container Services is currently available in private preview, which means that significant contribution to revenues is rather expected in the upcoming years.

I believe these solutions (together with previously discussed AI/ML features) further enhance the flexibility of the platform, which will result in significant new business/customer generation in the upcoming years. Although it's hard to quantify at this point how these innovations will impact the bottom line exactly, I think current annual revenue growth estimates of ~+31-33% for the upcoming years seem conservative in the light of these innovations.

Higher growth for longer

The innovative solutions that Snowflake continuously brings to its platform ensure in my opinion that topline growth won't level off for many years to come. However, it's also important to look at product penetration among existing customers, and the target market in general, which could serve also as a good indication for a company's future growth prospects. Analyzing these factors for Snowflake strengthens the case that a higher growth for longer scenario has a good chance to materialize in my view.

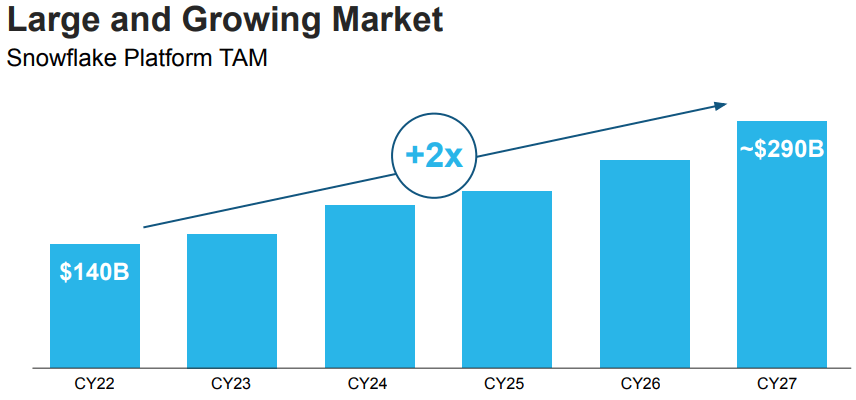

To begin from a bird's-eye view let's look at the Total Addressable Market ((TAM)) for Snowflake's platform, which has been presented by the company on its Investor Day calculated from Gartner's forecasts:

Snowflake 2023 Investor Day presentation

{kind=link}

Based on the chart above Snowflake's TAM is expected to double only within 5 years, representing a CAGR of ~15%. Disruptive companies like Snowflake used to grow their revenues significantly higher than their TAM grows in general, so this 15% should be a strong starting position.

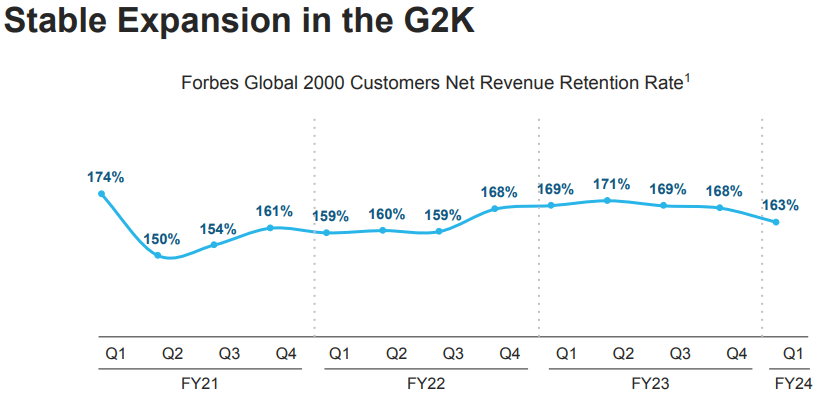

The penetration of Snowflake within this rapidly evolving market is increasing nicely, but there's still a large space left to conquer. Looking at the largest and most important customer base, the Forbes Global Top 2000 companies, penetration increased from 16% in Q1 FY21 to 30% in Q1 FY24. Although this is an impressive improvement it shows that most of Snowflake's potential market opportunity is still untapped.

Zooming in on the Forbes Global 2000 customer cohort we can see that it is characterized by exceptionally strong Net Revenue Retention ((NRR)), which held up pretty well in the previous years, still tracking at 163% in Q1 FY24:

Snowflake 2023 Investor Day presentation

{kind=link}

This shows that these customers are very valuable, as they typically grow their spending at a higher rate and also in a predictable way. The fact that 70% of them are not Snowflake customer currently should be a strong driver of future revenue growth in my opinion.

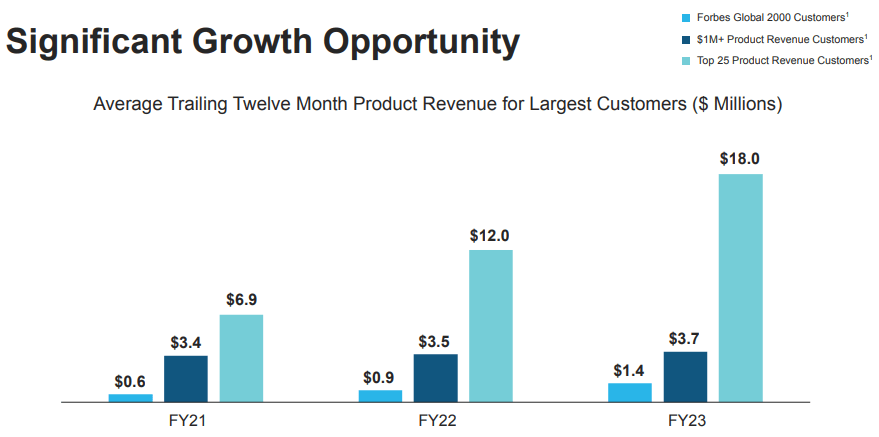

Comparing this customer cohort to Snowflake's largest customers reveals that many of those 30% who are already Snowflake customers are still in the early innings of their Snowflake journey:

Snowflake 2023 Investor Day presentation

{kind=link}

Snowflake on average, realized $1.4 million in product revenues on Forbes Global 2000 customers in FY23, only 38% of what the company realized on its customers with $1 billion+ product revenues during the same period. Comparing this to the top 25 customers results in a ratio of less than 8%, which confirms that there is still a large growth runway ahead of the Forbes Global 2000 cohort.

One important reason that these customers are usually in the early innings of their Snowflake journey is that it takes considerable time to migrate to the platform. Currently, on average 240 days pass until a typical customer reaches its initially contracted capacity. This means that many Forbes Global 2000 customers (approximately half of them joined in the past three years) have started to take their consumption to the next level only recently

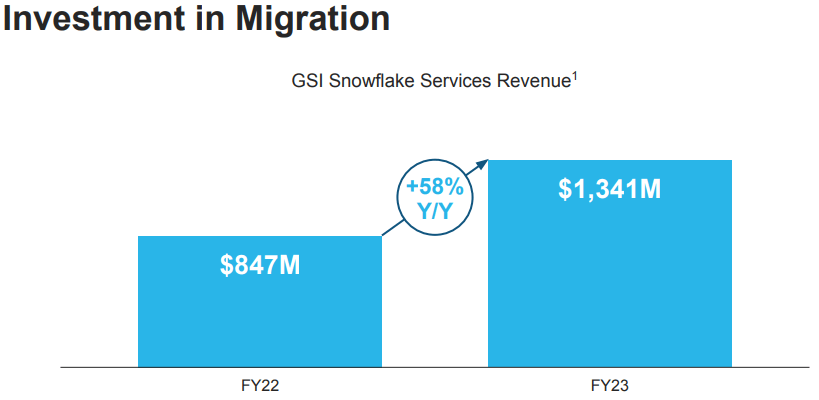

One good sign that this process should continue in the upcoming years is represented by the following chart, which has been provided by Snowflake management during Investor Day:

Snowflake 2023 Investor Day presentation

{kind=link}

It shows that global system integrators (e.g.: Deloitte) made almost $850 million dollars in FY22 from helping companies to migrate their data to Snowflake and start using the platform. This has grown by 58% yoy to more than $1.3 billion in FY23, which shows that companies are still investing heavily in becoming Snowflake customers and extract as much value from the platform as possible. As these investments in technology are usually strategic investments, which span the upcoming 5-10 years I believe they serve as a strong sign that the usage of the platform could heavily increase in the upcoming years.

Based on the data presented above I believe Snowflake has significantly better longer term growth prospects than many other companies in the SaaS space. On the one hand, they have many large customers who are only becoming acquainted with the platform leaving significant room for supporting continued strong NRR. On the other hand, the number of large prospective clients is still significant, who ones join the platform will take also a few years to ramp up consumption. These processes should result in a topline growth rate this decade, which significantly surpasses the 15% market average in my opinion.

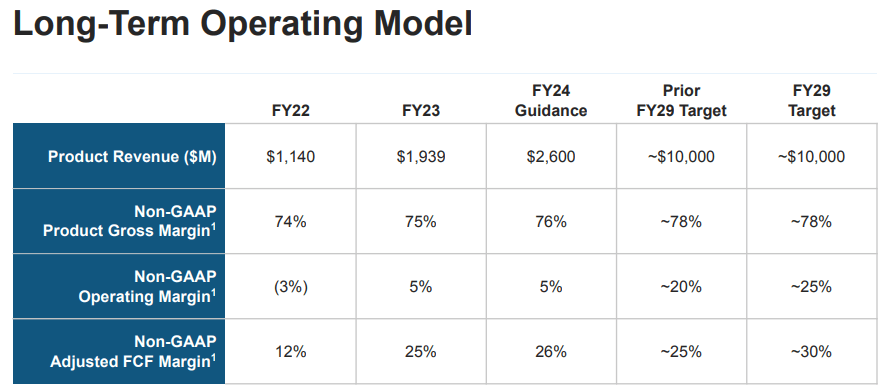

In the light of these it made me wonder, why management decided to leave its $10 billion product revenue guidance for FY29 unchanged from last year, equaling a CAGR of ~25% over this horizon:

Snowflake 2023 Investor Day presentation

{kind=link}

Based on the comments from Investor Day and a few explanatory slides from the presentation it turned out that they decided to stay conservative and applied recent slower consumption trends to the forecast. On the top of that no significant ramp up of AI/ML-related revenues has been included as most of these features are currently only available in public or private preview. Based on this I believe there is significant upside potential to this forecast, even the average analyst estimates call for ~$11 billion.

Valuation

The valuation of Snowflake's shares is usually the most common argument against investing in them. Currently, they trade at ~21x FY24 forward revenues, which is an outstanding multiple in the SaaS space. The most recent ~50% yoy revenue growth rate doesn't justify this multiple either as companies with similar growth rates (e.g.: monday.com (MNDY), CrowdStrike (CRWD)) trade usually at more conservative levels. To understand Snowflake's seemingly aggressive valuation, investors have to look further into the future.

If we take into consideration that there's a good chance that the company reaches its FY29 revenue target of $10 billion, this would result in a forward P/S ratio of ~5.8 in 5 years from now, which doesn't seem too exaggerated. If Snowflake manages to grow its revenues still at a 20-30% annual rate by then, it should rather trade at a multiple double than that, just like ServiceNow ( NOW ) trades currently at a ~13 forward P/S ratio with revenues expected to grow at a 20%+ CAGR in the upcoming years. Based on this, I believe that in a conservative scenario, where Snowflake manages only to reach its $10 billion FY29 product revenue guidance the share price could double within 5 years.

However, there is considerable upside to this in my opinion because the new product announcements, the transformation of the world through AI, the low penetration among existing and prospective clients, and the conservativism of management all could result in significantly higher revenues for FY29. This of course would result in a higher share price when calculating with the same P/S ratio.

It all depends on the belief of investors to what degree they believe that Snowflake is able to continue to disrupt the market for so many years to come. Based on the analysis presented above I believe that this is a real possibility, which is also the reason that shares represent an important holding in my growth portfolio.

Another topic, which also impacts the valuation of shares is dilution, which used to be significant over the past year, around 3% (for a detailed analysis see my following article on the topic: Snowflake: Don't Let SBC Dilute Your Thoughts ). Good news is that management shared during Investor Day that they will manage to bring back dilution to their 2% target in the upcoming years, which should make shares more investable in my opinion.

Finally, looking at margins we can see from the previous chart that management raised its long-term operating and free cash flow margin targets by 5-5%-points, respectively. An operating margin of 25% and an FCF margin of 30% is quite impressive in my opinion, which could explain some part of the valuation premium as well.

Risk factors

Staying at the topic of valuation, it represents a significant risk factor for shares. The share price of companies with higher than usual valuation multiples used to fluctuate quickly, so investors should be prepared for a high level of volatility. A good example for this is that shares lost almost 70% of their value during the correction in tech shares, which started at the end of 2021, although there hasn't been a significant change in fundamentals for a while.

Another important risk factor is competition as there are other important emerging competitors in the space (Databricks, Teradata, Amazon Redshift, etc.). In this case, I believe that besides it's unique platform that separates storage and compute Snowflake has several important differentiating features, which make their value proposition stand out from the crowd. Among others these are the possibility of Data Sharing, no limitations on programming language with recently announced container services, effective handling of unstructured data, no heavy reliance on one specific vendor (unlike solutions from big 3), targeted acquisitions to broaden product portfolio or outstanding ROI. I think these examples represent it clearly that Snowflake is constantly trying to stay ahead of the competition. Currently, I see no change in this dynamic.

Conclusion

With its innovative platform Snowflake has been the leading company in the data-as-a-service market for a while now. The company's most recent product event demonstrated that they intend to stay in the driver's seat, which should result in 30%+ annual revenue growth figures for many years to come in my opinion. This is also supported by a large untapped market potential whether looking at existing or prospective clients. For those investors whose risk tolerance is above average shares of Snowflake represent a good long-term buying opportunity at current levels in my view.

Editor's Note: This article was submitted as part of Seeking Alpha's Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Snowflake: Unique Growth Prospects Justify Current Valuation