SONO - Sonos: Potential Light Emerging From The Tunnel (Rating Upgrade)

2023-12-13 15:36:28 ET

Summary

- Sonos stock has remained flat for the year but has seen a 60% comeback since October.

- Positive fiscal Q4 results and positive guidance for FY24 have contributed to the stock's rally.

- Sonos is preparing to launch headphones for the first time, expanding its market scope and potentially driving growth.

- The stock trades at a relatively reasonable ~11x adjusted EBITDA multiple.

As we look ahead to a 2024 that hopefully contains interest-rate cuts, stocks have soared in the last quarter of 2023. Better yet is when these rallies have been accompanied by true fundamental catalysts.

Sonos ( SONO ), the home speaker manufacturer, has largely missed out on this year's rally. The stock is about flat for the year, though it has staged a massive +60% comeback since hitting a YTD low of ~$10 in October.

A number of positive headlines have fed this rally. First, the company has released fiscal Q4 results and initiated positive guidance for FY24 (which for Sonos is the year ending in September 2024). Second, it announced major job cuts - which help to justify the margin/adjusted EBITDA improvements that the company is pointing to for next year. And finally, the company is gearing up to launch a headphone product for the first time, widening its market scope and potentially positioning the company for a return to growth next year.

I last wrote a neutral opinion on Sonos in August, back when the stock was trading closer to $14 per share. On the bright side for Sonos, I had called out the stock's modest valuation and efforts at cost-cutting, which were paving the path toward adjusted EBITDA expansion. At the same time, however, top-line growth remained (and to some extent, does remain) challenging.

Now, however, with the promise of an entirely new category of products plus continued gross margin expansion, I am ready to be bullish on this stock again. Here are some longer-term bull case considerations to be aware of:

- Massive global audio market- Sonos estimates the global home audio market at $89 billion, which indicates that the company is currently only ~2% penetrated into this market. To grow into this space, the company champions continued innovation and product refreshes as well as extending its brand both upmarket and downmarket.

- Reputation for quality- Sonos is a heavyweight brand in the audio space and has the capacity to leverage that brand familiarity across a full product spectrum.

- Cost-minded- On top of driving gross margin improvements through economies of scale, the company has also shown a pattern of managing opex diligently, especially when top-line growth is fading.

It's worth jumping on this rally now - as I believe there is further upside to go in 2024 as more tailwinds turn in Sonos' favor.

Q4 download

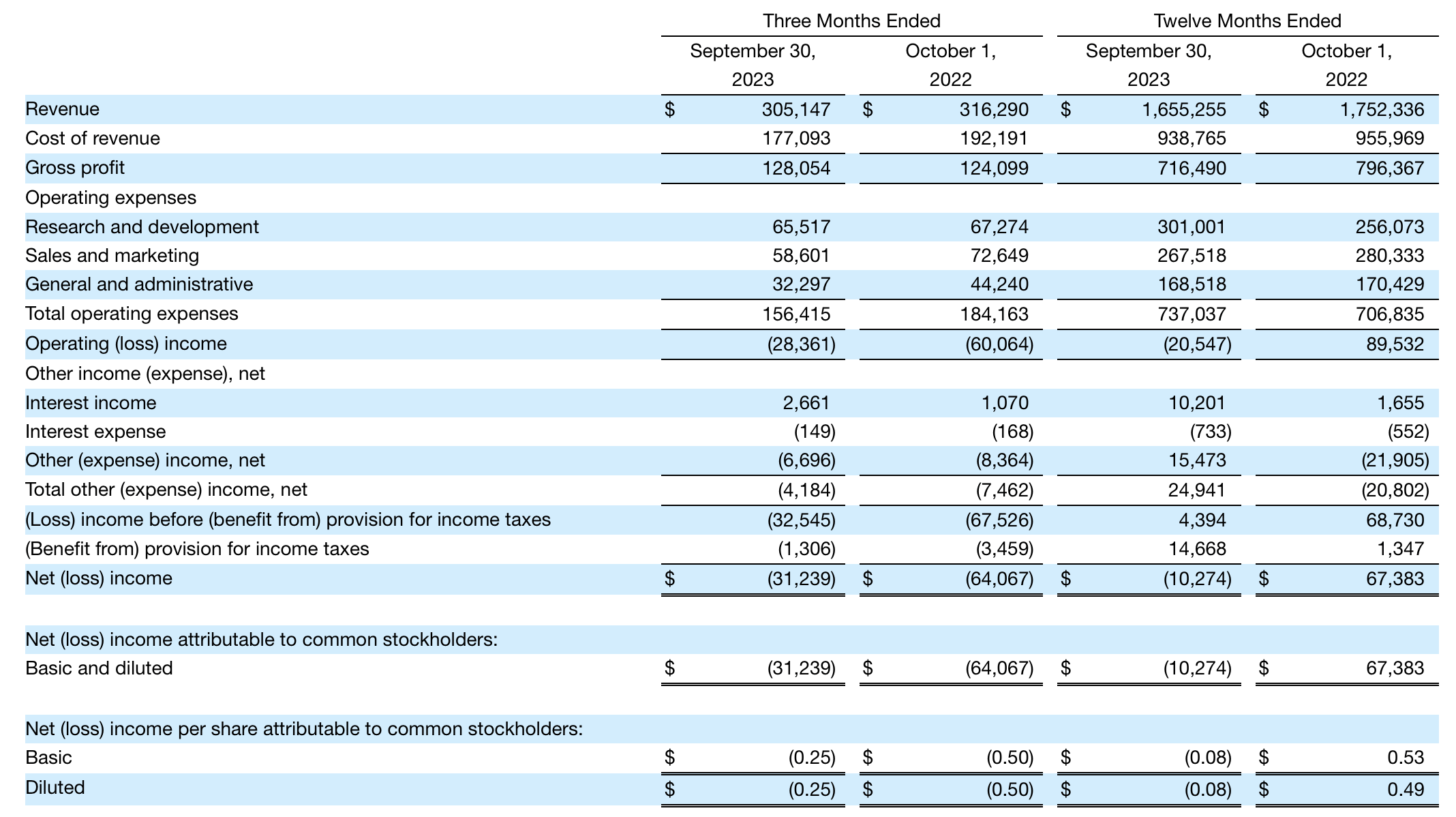

Let's now go through Sonos' latest fiscal Q4 (September quarter) results in greater detail. The Q4 earnings summary is shown below:

{kind=link}

Sonos' revenue declined -4% y/y to $305.1 million, which came in ahead of Wall Street's expectations of $299.4 million (-5% y/y). Underlying product registrations, meanwhile, fell -13% y/y and product sell-in was -8% y/y. This is still a big cause for concern for Sonos, as the company has been dealing with the overhang of post-pandemic demand for the past year. The company enjoyed temporary lifts during the pandemic as many consumers moved out of cities and furnished new homes - but this seems to have had the effect of pulling forward demand from the present. Still - the company has benefited from price increases, as ASP boosts have helped blunt the revenue declines in relation to unit sales and registrations.

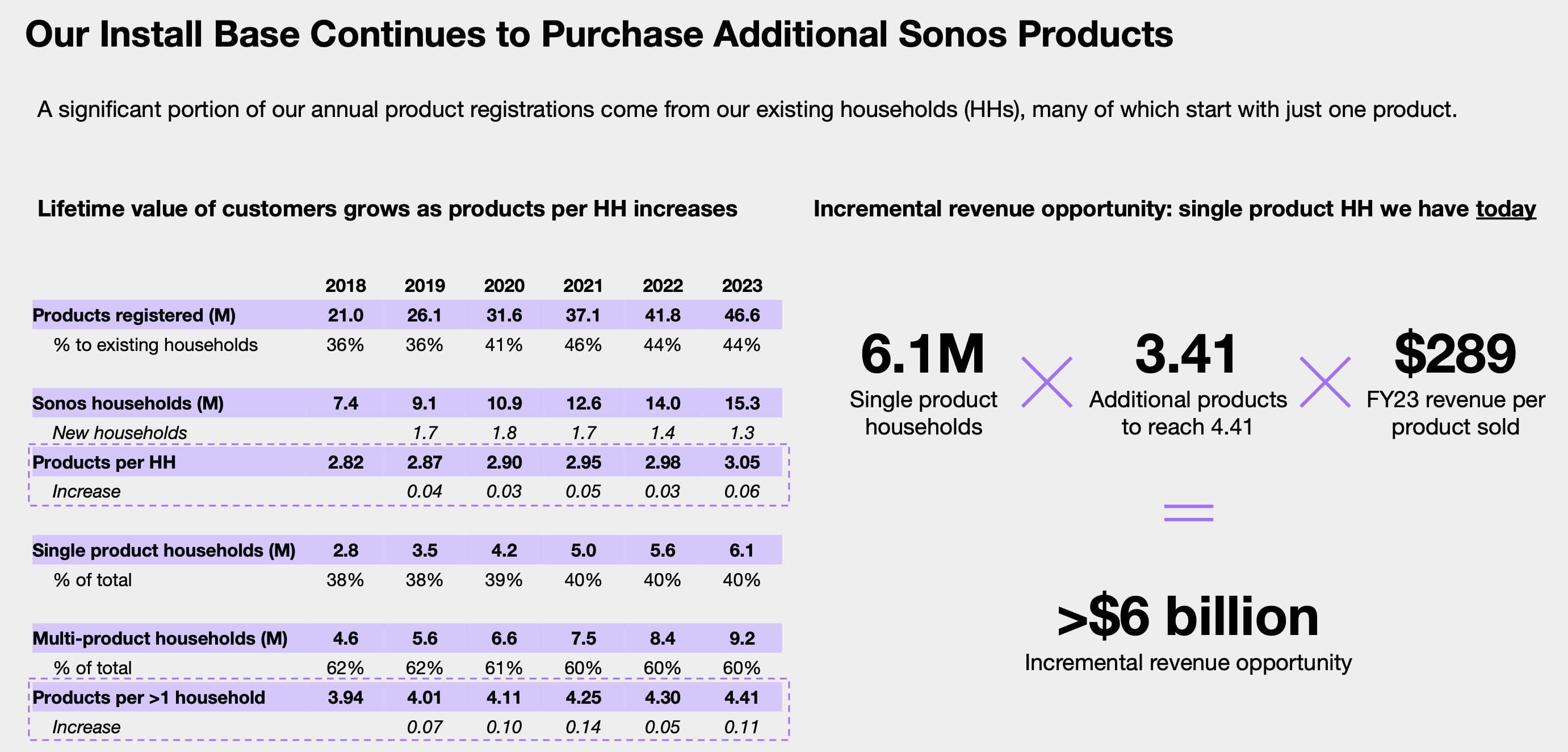

When we zoom out and look at the longer arc of time, we find a bit more confidence in Sonos' long-term trends. The chart below shows that Sonos registered 4.8 million new products in FY23:

{kind=link}

Total Sonos households, meanwhile, increased by 1.3 million - roughly in line with FY22. At the same time, a growing number of Sonos users are multi-product owners, outfitting their homes with multiple Sonos speakers in different rooms. The company has cited a ~$6 billion additional revenue opportunity from converting all of its ~6 million single-product households into multi-product owners. And with new products like headphones coming in 2024, the company has additional opportunity to penetrate deeper into the wallet share of its existing customer base.

CEO Patrick Spence, speaking on the Q4 earnings call , noted his belief that Sonos' current revenue drag is mostly macro-driven and impacts all audio manufacturers, and that the company has continued to retain or grow market share:

While our business is more resilient than many of our competitors, thanks to our strong brand and loyal customer base, it was a challenging year in the categories in which we play today.

The good news is that we retained strong market share positions in the countries we play despite our competitors offering deep discounts throughout the year. In fact, we recorded our highest market share in home theater in both the United States and Germany this year since 2019. This is a testament to the strength of our brand, our product portfolio, and the execution of our team.

We know we're in a down part of the business cycle when it comes to home audio and we know that eventually consumers will return. There are strong secular trends that will help drive our business over the long term. Work from home is going to be an enduring phenomenon. SO 2 will be increased home consumption of video content. And as the touring success of Taylor Swift and Beyonce test, music and the joy it brings remains an essential and thriving part of our culture. Sonos benefits from all of this."

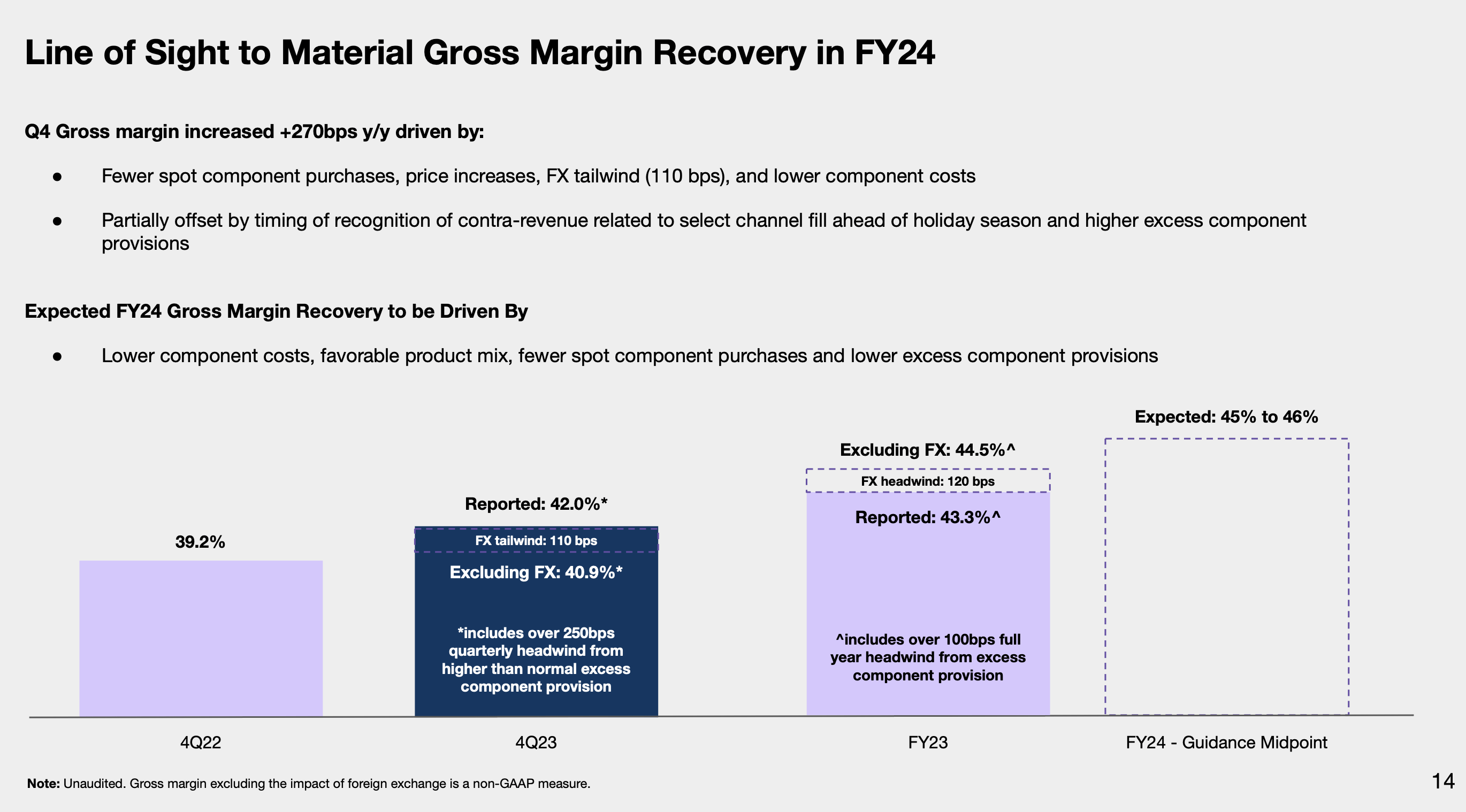

On the margin front, Sonos reported a 42.0% gross margin in the fourth quarter, up 280bps y/y. Roughly one-third of this benefit came from FX now becoming a tailwind to margin, while the remaining gross margin leverage was driven by decreased component costs and the company's price increases.

{kind=link}

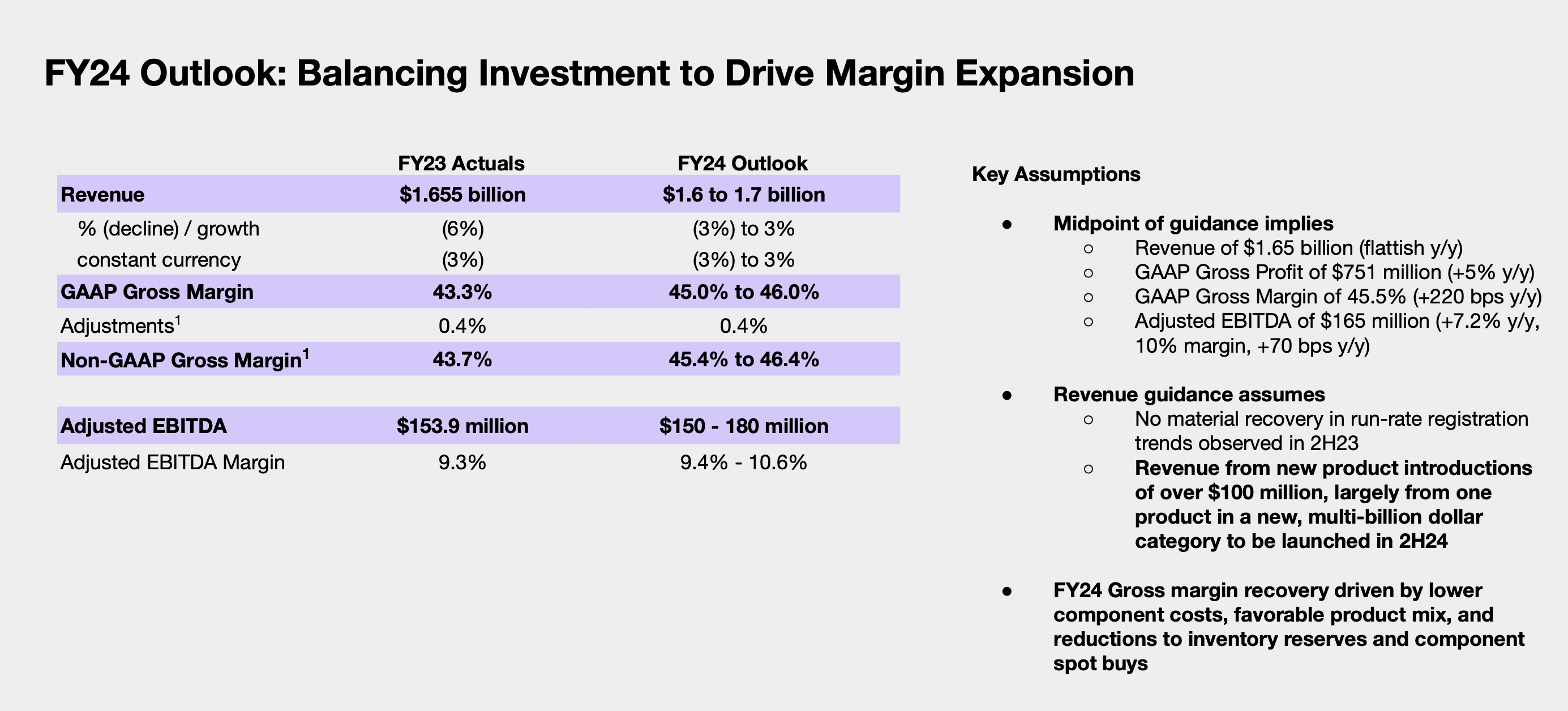

Importantly, it's worth noting that the company is pointing to further gross margin expansion in FY24, up to a range of 45-46%.

The company's full FY24 outlook is shown in the chart below:

{kind=link}

Though the midpoint of Sonos' outlook is essentially calling for flat y/y revenue growth, the combination of gross margin expansion plus the benefits of cost cuts (Q4 opex was already down -15% y/y, which came before the company announced further role eliminations in the product development org) has the company's adjusted EBITDA up to a $150-$180 million range, which would represent 17% growth at the top end of the range.

Valuation and key takeaways

Despite the recent run-up in Sonos' stock, I think the company's calls for double-digit adjusted EBITDA expansion in FY24 still make its valuation look modest on that front.

At current share prices near $16.50, Sonos trades at a market cap of $2.07 billion. After we net off the $220.3 million of cash on Sonos' most recent balance sheet, which is unencumbered of debt, the company's resulting enterprise value is $1.85 billion.

Against the midpoint of Sonos' adjusted EBITDA range for next year, Sonos trades at 11.2x EV/FY24 adjusted EBITDA - which I think is still quite an investable multiple, especially as Sonos carries multiple drivers for upside next year, including the contribution from new product launches, an easy comp versus a tough decline in FY23 that may spur more revenue growth than anticipated, and the cost benefits from deflation in component costs plus rationalized headcount levels.

Stay long here and ride the upward wave.

For further details see:

Sonos: Potential Light Emerging From The Tunnel (Rating Upgrade)